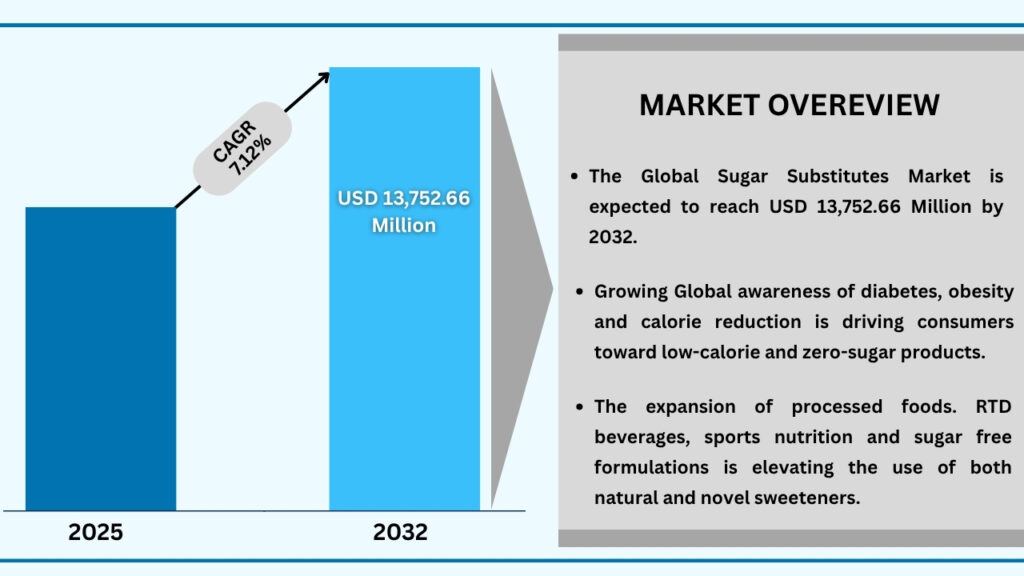

Market Synopsis

The Sugar Substitutes Market size was USD 7,952.73 Million in 2024 and is expected to reach USD 13,752.66 million at a CAGR of 7.12% during the forecast period.

Rising Demand for Low-Calorie and Sugar-Free Products

The global rise in obesity, diabetes, and lifestyle-related diseases is accelerating consumer preference for low-calorie, reduced-sugar, and zero-sugar foods and beverages. Manufacturers are increasingly incorporating sugar substitutes to meet clean-label and health-conscious demand, boosting market expansion.

Innovation in Natural and Novel Sweeteners

Rapid advancements in plant-based sweeteners like stevia, monk fruit, allulose, and tagatose are reshaping product formulations. These ingredients offer sugar-like taste and functionality, enabling food and beverage companies to replace sugar without compromising flavor.

Supportive Regulatory Approvals and Reformulation Mandates

Global food safety authorities are approving a wider range of sweetener ingredients, while several countries enforce sugar taxes and reformulation guidelines. These regulatory shifts are pushing manufacturers to adopt high-intensity, low-intensity, and novel sweeteners at a faster pace.

Growing Focus on Health, Wellness & Functional Nutrition

Increasing consumer interest in functional foods, dietary supplements, and sports nutrition is contributing to the usage of sugar substitutes in bars, beverages, RTD shakes, and gummies. The demand for healthier alternatives is driving consistent market growth across multiple applications.

Expansion of Clean-Label and Plant-Based Food Trends

Consumers are increasingly seeking natural, minimally processed, and plant-derived ingredients, boosting demand for clean-label sweeteners such as stevia, monk fruit, and allulose. This shift is encouraging manufacturers to replace artificial sweeteners with natural alternatives, further propelling market growth.

Global Sugar Substitutes Market (USD Million)

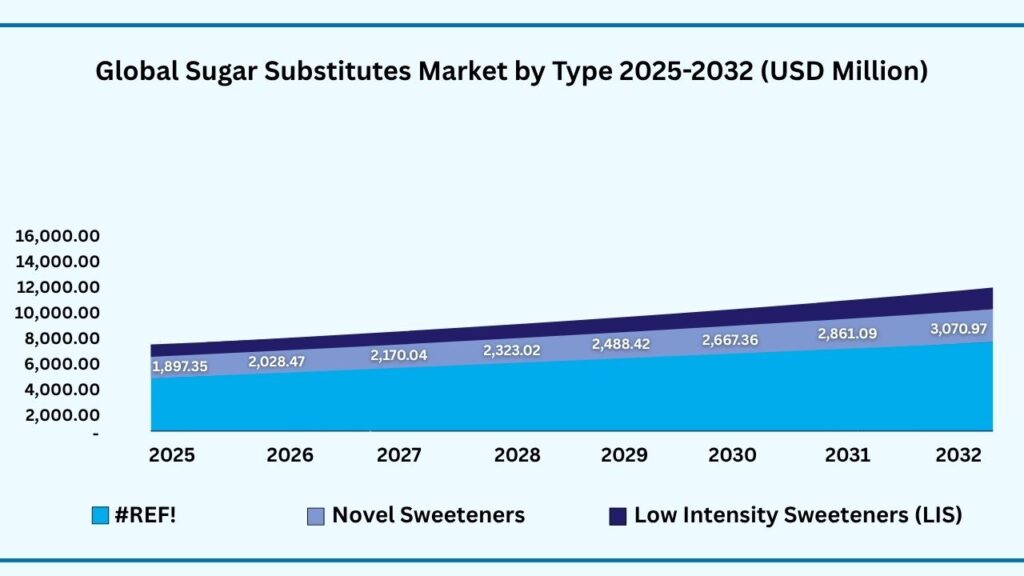

Global Sugar Substitutes Market by Type Insights:

High-Intensity Sweeteners (HIS) segment accounted for market share of share 65.44% in 2024 in the global cultured meat market.

The High-Intensity Sweeteners (HIS) segment accounted for the largest share of the global Sugar Substitutes market in 2024, representing 65.44% of total revenues. Rotary-Wing Drones (Multirotor) segment is expected to register a CAGR of 7.17% during the forecast year from 2025 to 2032.

The High-Intensity Sweeteners segment leads the global sugar substitutes market due to growing consumer demand for low-calorie and sugar-free products. Rising awareness about health issues such as obesity and diabetes is encouraging both individuals and food manufacturers to adopt HIS in beverages, baked goods, and processed foods. Innovations in formulation technology that improve taste and reduce aftertaste are further driving adoption worldwide.

Rotary-Wing Drones are gaining popularity because of their versatility and efficiency in applications like agriculture, surveillance, delivery, and cinematography. Advances in battery life, AI-assisted navigation, and payload capabilities are enhancing their performance. In addition, regulatory support for commercial drone operations and the integration of drones with IoT and data analytics platforms are expanding opportunities across industries.

The growth of both high-intensity sweeteners and rotary-wing drones is supported by shifting consumer and industry trends. In the case of sweeteners, the emphasis on healthier lifestyles and functional foods is encouraging widespread adoption across food and beverage products. For drones, the demand for automation, precision, and real-time data insights is driving adoption across sectors, from agriculture to logistics. Overall, innovation, regulatory support, and evolving consumer preferences are key factors shaping these markets.

Global Sugar Substitutes Market by Type (USD Million)

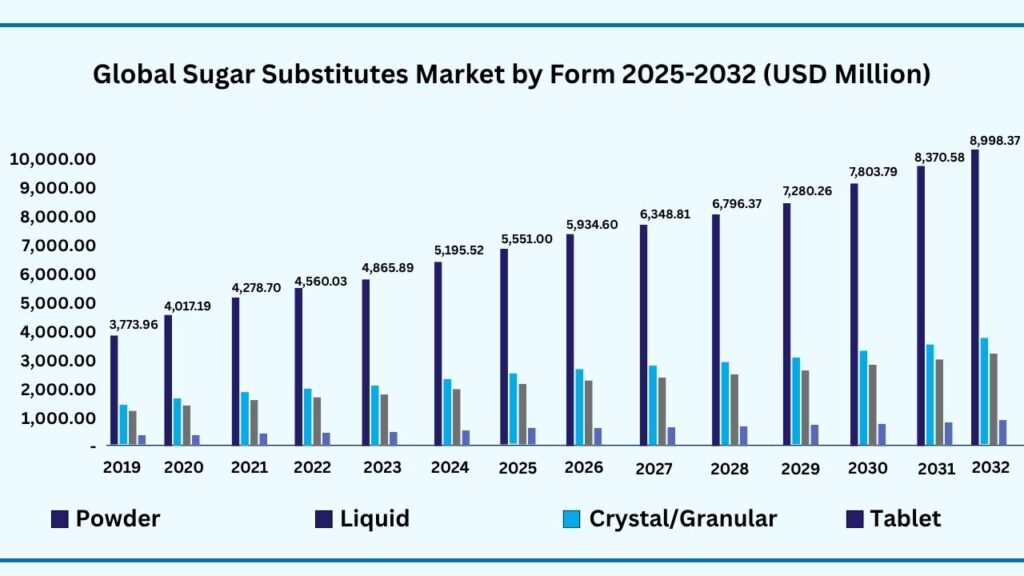

Global Sugar Substitutes Market by Form Insights:

Powder segment accounted for the largest market share of share 65.33% in 2024 in the global Sugar Substitutes market.

Based on the form, Powder held the largest revenue share of 65.33% 2024, and expected to register a CAGR of 7.14% between 2025 to 2032 and the market is expected to reach USD 8,998.37 by 2032.

Powdered products are highly convenient for both manufacturers and consumers due to their lightweight and compact nature. They occupy less storage space compared to liquids or semi-solid forms, reducing logistical and warehousing costs. Transportation is simpler, with lower risks of spillage or breakage during shipping. Handling is also easier during production processes, as powders can be measured, mixed, and processed efficiently. This convenience makes powders especially suitable for large-scale industrial applications. Overall, the ease of storage, transport, and handling significantly contributes to their preference in the market.

The powder form can be easily incorporated into a wide variety of products, including beverages, bakery items, dietary supplements, sauces, and culinary formulations. Its adaptability allows manufacturers to create customized blends, fortifications, or flavored variants without altering product stability. Powders also facilitate precise dosage and consistent quality in formulations. This versatility enables use across multiple sectors, from food and nutrition to pharmaceuticals and health products. As a result, demand for powder-based ingredients continues to grow steadily. The broad applicability of powders reinforces their strong market position globally.

Powdered products generally exhibit superior stability compared to liquid or gel forms, which are more prone to microbial growth and chemical degradation. The reduced moisture content in powders helps prevent spoilage, extending their shelf life significantly. Longer shelf life not only minimizes product wastage but also reduces the frequency of production runs and inventory turnover. This stability is particularly beneficial for global distribution and export markets where longer storage periods are needed. Enhanced shelf life also increases consumer confidence in product quality and safety. Consequently, the durability and reliability of powders remain a key factor driving their adoption in the market.

Global Sugar Substitutes Market by Form (USD Million)

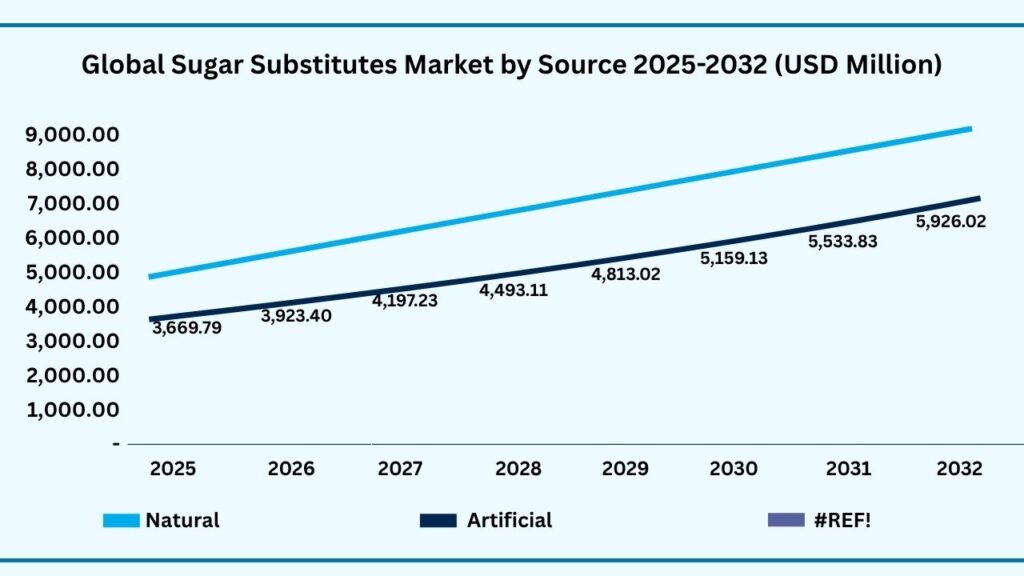

Global Sugar Substitutes Maret by Source Insights:

Natural segment accounted for the largest market share of share 56.81% in 2024 in the global Sugar Substitutes market.

Based on source, Natural segment held the largest revenue share of 56.81% in the global Sugar Substitutes market in 2024 and expected to register a CAGR of 7.15% from 2025 to 2032 and expected to reach USD 7,826.64 million. The natural sugar substitutes segment leads the market due to growing consumer preference for healthier and clean-label ingredients. Increasing awareness of the adverse health effects of excessive sugar consumption, such as obesity, diabetes, and cardiovascular issues, is driving the adoption of natural alternatives. Consumers are actively seeking products derived from plant-based sources, such as stevia, monk fruit, and agave, which are perceived as safer and more sustainable than synthetic options.

Food and beverage manufacturers are increasingly incorporating natural sugar substitutes into products like beverages, confectionery, bakery items, and dairy to meet consumer demand for low-calorie and naturally sourced ingredients. Additionally, innovations in extraction, purification, and formulation technologies are enhancing the taste, solubility, and stability of these natural sweeteners, making them more appealing to both manufacturers and consumers. The combined effect of consumer preference, health consciousness, and technological advancements is reinforcing the strong position of natural sugar substitutes in the global market.

Global Sugar Substitutes Market by Farm Size (USD Million)

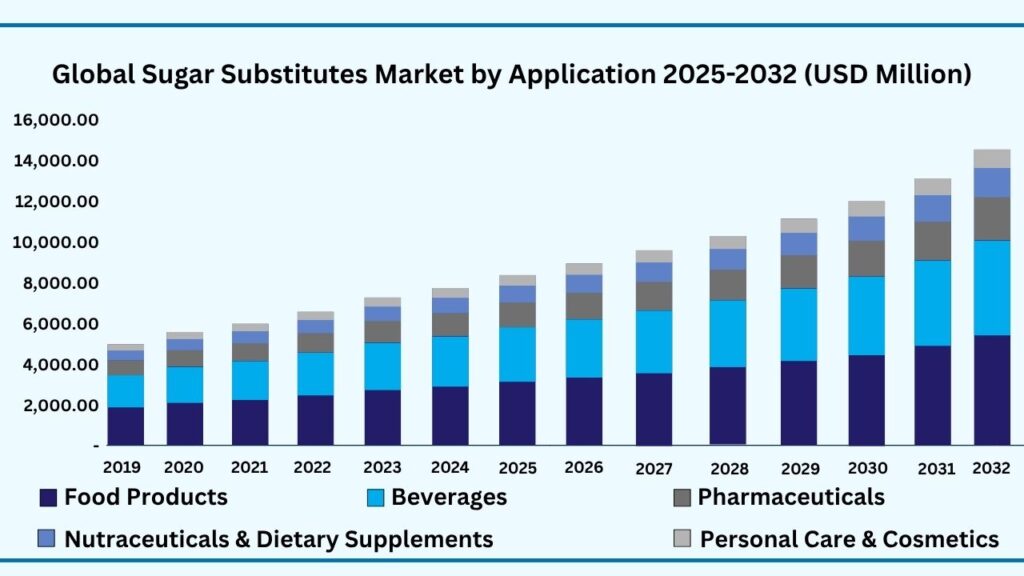

Global Sugar Substitutes Market by Application:

Food Products segment accounted for the largest market share of share 39.44% in 2024 in the global Sugar Substitutes market.

Based on application, Food Products segment held the largest revenue share of 39.44% in the global Sugar Substitutes market in 2024 and expected to register a CAGR of 7.12% from 2025 to 2032 is expected to reach USD 5,437.80 million. The food products segment leads the sugar substitutes market due to the rising demand for low-sugar and healthier food options across bakery, confectionery, dairy, and processed foods. Growing consumer awareness about lifestyle-related diseases and the increasing shift toward calorie-controlled diets are prompting manufacturers to reformulate products using sugar alternatives. This trend is further supported by the surge in clean-label, natural, and functional food offerings, where sugar substitutes are widely used to maintain sweetness without compromising nutritional goals.

Manufacturers are increasingly incorporating sugar substitutes into food products to enhance taste while reducing sugar content, driven by regulatory pressure to limit sugar levels and meet evolving consumer expectations. Advancements in formulation technologies are improving the stability, solubility, and flavor profile of sweeteners, making them suitable for a broader range of food applications. As a result, the use of sugar substitutes has expanded significantly in mainstream food categories, reinforcing the strong growth and continued dominance of the food products segment in the global market.

Global Sugar Substitutes Market by Application (USD Million)

Global Sugar Substitutes Market by End Use Insights:

Food & Beverage Manufacturers segment accounted for the largest market share of share 70.33% in 2024 in the global Sugar Substitutes market.

Based on end use segment Food & Beverage Manufacturers held the largest revenue share of 70.33% in the global Sugar Substitutes market in 2024 and expected to register a CAGR of 7.11% from 2025 to 2032 and expected to reach USD 9,686.00 million in 2032. Food and beverage manufacturers remain the leading end-use segment due to the rapid shift toward healthier product formulations and reduced-sugar alternatives. Growing consumer demand for low-calorie, clean-label, and naturally sweetened products is driving manufacturers to integrate sugar substitutes into a wide range of applications, from beverages and snacks to dairy and bakery products. This strong industry-wide reformulation trend has significantly increased the reliance on sugar substitutes in large-scale production.

Manufacturers are increasingly adopting sugar substitutes to meet regulatory guidelines aimed at reducing added sugar levels in packaged foods and beverages. Continuous innovation in sweetener technologies—such as improved taste-modulation systems, enhanced solubility, and better heat stability—is also encouraging broader adoption across different product categories. These advancements enable manufacturers to maintain taste quality while reducing sugar content, strengthening the segment’s growth and securing its position as the dominant end-use category in the global market.

Global Sugar Substitutes by End Use (USD Million)

Global Sugar Substitutes Market by Region Insights:

Asia-Pacific segment accounted for the largest market share of share of 38.44% in 2024 in the global Sugar Substitutes market.

Based on region, the global Sugar Substitutes market is segmented into Europe, Asia-Pacific, North America, Latin America and Middle East & Africa. Among these, Asia-Pacific region held the largest revenue share of 38.44% in the global Sugar Substitutes market in 2024 and expected to reach USD 5,300.28 million in 2032. The Asia-Pacific region leads the global sugar substitutes market due to rising health awareness, growing urbanization, and increasing adoption of low-calorie diets among consumers. Rapid lifestyle changes, coupled with a higher prevalence of diabetes and obesity, are driving demand for healthier sweetening alternatives across major countries. Additionally, the expanding food and beverage industry in the region, supported by a large and diverse consumer base, is accelerating the use of sugar substitutes in packaged foods, beverages, and functional nutrition products.

Manufacturers in Asia-Pacific are increasingly focusing on product innovation, including natural and clean-label sweeteners, to meet evolving consumer preferences. Government initiatives promoting sugar reduction in processed foods and beverages are also reinforcing market growth. Furthermore, the strong presence of local and international players, along with rising investments in food processing, nutraceuticals, and health-oriented product development, is boosting regional demand. These factors collectively strengthen Asia-Pacific’s position as the fastest-growing and most influential market for sugar substitutes globally.

Global Sugar Substitutes Market by Region (USD Million)

Major Companies and Competitive Landscape

The global Sugar Substitutes market is highly competitive and fragmented, with numerous established ingredient manufacturers and emerging clean-label sweetener innovators competing to expand their market presence. Leading companies are actively pursuing strategies such as mergers and acquisitions, partnerships with food and beverage manufacturers, and collaborations with biotechnology firms to strengthen their product portfolios. Many players are investing significantly in R&D to improve sweetness profiles, enhance taste-modulation technologies, and develop next-generation natural sweeteners that cater to rising health and wellness trends. The industry focus is shifting toward creating cost-efficient, stable, and scalable formulations that meet diverse application needs across beverages, bakery, dairy, confectionery, and nutritional products.

In addition, manufacturers are emphasizing sustainability, clean-label certification, and regulatory compliance to gain consumer and industry trust. Companies are introducing sugar substitutes with improved solubility, heat stability, and reduced aftertaste to support wide-scale adoption in processed foods and functional beverages. As demand continues to surge across both developed and emerging markets, key players are expanding production capacity, strengthening distribution networks, and enhancing customer support services. This blend of technological innovation, strategic collaborations, and global expansion is expected to drive intensified competition and continuous product evolution in the Sugar Substitutes market in the coming years.

Some of the leading companies profiled in the global cultured meat market report include:

- Cargill, Incorporated

- Archer Daniels Midland Company

- Tate & Lyle PLC

- Ingredion Incorporated

- Roquette Frères S.A.

- E. I. du Pont de Nemours and Company

- Ajinomoto Co., Inc.

- GLG Life Tech Corporation

- Nutrinova

- Merisant

- Whole Earth Brands, Inc.

- JK Sucralose Inc.

- PureCircle Ltd.

- Sensient Technologies Corporation

- Global Sweeteners Holdings Limited

- Niutang Chemical Co., Ltd.

- Tereos S.A.

- Cumberland Packing Corporation

- Tag Ingredients India Pvt Ltd.

- Suminter India Organics

Strategic Development

Cargill, Incorporated (U.S.)

In early 2025, Cargill announced a major expansion of its specialty sweetener production facilities to meet the surging global demand for natural and low-calorie sugar alternatives. The company is investing heavily in advanced fermentation and plant-based extraction technologies to enhance the purity and taste profile of stevia and monk fruit sweeteners. Cargill also launched a global collaboration program with leading food & beverage manufacturers to co-develop next-generation reduced-sugar formulations, supporting brands in reformulating products without compromising taste or texture. This initiative strengthens Cargill’s position as a leading provider of sustainable and clean-label sugar substitutes.

Ingredion Incorporated (U.S.)

In mid-2025, Ingredion introduced its new portfolio of clean-label, plant-derived sweetening solutions developed through extensive research in natural ingredient innovation. The company upgraded its manufacturing capabilities to produce high-performance sweeteners with improved solubility, heat stability, and reduced aftertaste, enabling broader use across bakery, beverage, dairy, and nutritional applications. Ingredion also expanded its strategic partnerships with regional food processors in Asia-Pacific and Europe to accelerate adoption of low-sugar product formulations. These initiatives align with Ingredion’s long-term strategy of supporting global brands in delivering healthier, reduced-sugar food and beverage products.

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 7,952.73 Million |

| CAGR (2024–2032) | 7.12% |

| Revenue forecast to 2033 | USD 13,752.66 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million, and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Product Type By Product Type, By Packaging Material, By Function, By Packaging Type by Distribution Channel, By End Use and by region and for 2019 to 2032 |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, Rest of MEA |

| Key companies profiled | Cargill, Incorporated | Archer Daniels Midland Company | Tate & Lyle PLC | Ingredion Incorporated | Roquette Frères S.A. | E. I. du Pont de Nemours and Company | Ajinomoto Co., Inc. | GLG Life Tech Corporation | Nutrinova | Merisant | Whole Earth Brands, Inc. | JK Sucralose Inc. | PureCircle Ltd. | Sensient Technologies Corporation | Global Sweeteners Holdings Limited | Niutang Chemical Co., Ltd. | Tereos S.A. | Cumberland Packing Corporation | Tag Ingredients India Pvt Ltd. | Suminter India Organics |

| Customization scope | 10 hours of free customization and expert consultation |

Some Key Questions the Report Will Answer

- What is the expected revenue Compound Annual Growth Rate (CAGR) of the global Sugar Substitutes market over the forecast period (2025–2032)?

- The global Sugar Substitutes market revenue is expected to register a Compound Annual Growth Rate (CAGR) of 7.12% during the forecast period.

- What was the size of the global Sugar Substitutes in 2024?

- The global Sugar Substitutes market size was USD 7,952.73 Million in 2024.

- Which factors are expected to drive the global Sugar Substitutes market growth?

- Growing consumer demand for low-calorie, sugar-free, and clean-label products is driving wider adoption of sugar substitutes. Rising awareness of lifestyle diseases such as obesity and diabetes is encouraging the shift toward healthier sweetening options. Additionally, advancements in natural sweetener extraction and formulation technologies are enhancing taste, stability, and application versatility, supporting strong market growth.

- Which was the leading segment in the global Sugar Substitutes market in terms of type in 2024?

- High-Intensity Sweeteners (HIS) segment was leading in the Sugar Substitutes market on the basis of product type in 2024.

- What are some restraints for revenue growth of the global Sugar Substitutes market?

- High production costs and complex extraction processes, especially for natural sweeteners, limit widespread affordability. Taste-related challenges such as bitterness, aftertaste, and formulation instability hinder broader adoption in certain applications. Additionally, strict regulatory approvals and varying global standards slow market expansion and delay product launches.

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of Global Sugar Substitutes Market

1.4. Currency and pricing

1.5. Limitation

1.6. Market s covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1. Primary

2.1.2. Secondary

2.1.3. Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1. Market value

2.3.2. Market volume

2.3.3. Exchange rate

2.3.4. Price

2.3.5. Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2019–2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10. Formulation & manufacturing4.11.Distribution & retail

4.12. Import-export analysis

4.13. Brand comparative analysis

4.14. Technological advancements

4.15. Porter’s five force

4.16. Threat of new entrants

4.16.1.1. Capital requirment

4.16.1.2. Product knowledge

4.16.1.3. Technical knowledge

4.16.1.4. Customer relation

4.16.1.5. Access to appliation and technology

4.16.2. Threat of substitutes

4.16.2.1. Cost

4.16.2.2. Performance

4.16.2.3. Availability

4.16.2.4. Technical knowledge

4.16.2.5. Durability

4.16.3. Bargainning power of buyers

4.16.3.1. Numbers of buyers relative to suppliers

4.16.3.2. Product differentiation

4.16.3.3. Threat of forward integration

4.16.3.4. Buyers volume

4.16.4. Bargainning power of suppliers

4.16.4.1. Suppliers concentration

4.16.4.2. Buyers switching cost to other suppliers

4.16.4.3. Threat of backward integration

4.16.5. Bargainning power of suppliers

4.16.5.1. Industry concentration

4.16.5.2. Industry growth rate

4.16.5.3. Product differentiation

4.17. Patent analysis

4.18. Regulation coverage

4.19. Pricing analysis

4.20. Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1. Rising Health Awareness and Lifestyle Diseases

5.1.2. Expansion of Functional and Health-Oriented Foods

5.1.3. Favorable Regulatory Support and Product Innovation

5.2. Restraints

5.2.1. Health Concerns and Safety Perceptions

5.2.2. High Production Cost of Natural Sweeteners

5.3. Opportunities

5.3.1. Growth in Clean-Label and Natural Ingredient Demand

5.3.2. Expansion in Emerging Markets

5.3.3. Application Diversification Beyond Beverages

5.4. Challenges

5.4.1. Taste and Formulation Issues

5.4.2. Regulatory and Labeling Complexity Across Regions

Chapter 6. Global Sugar Substitutes Market By Type Insights & Trends, Revenue (USD Million)

6.1. Type Dynamics & Market Share, 2019–2032

6.1.1. High-Intensity Sweeteners (HIS)

6.1.1.1. Aspartame

6.1.1.2. Sucralose

6.1.1.3. Saccharin

6.1.1.4. Acesulfame-K

6.1.1.5. Stevia

6.1.1.6. Monk Fruit

6.1.1.7. Neotame

6.1.1.8. Advantame

6.1.2. Low-Intensity Sweeteners (LIS)

6.1.2.1. Sorbitol

6.1.2.2. Xylitol

6.1.2.3. Mannitol

6.1.2.4. Erythritol

6.1.2.5. Maltitol

6.1.2.6. Lactitol

6.1.3. Novel Sweeteners

6.1.3.1. Allulose

6.1.3.2. Tagatose

6.1.3.3. Brazzein

6.1.3.4. Thaumatin

Chapter 7. Global Sugar Substitutes Market By Source Insights & Trends, Revenue (USD Million)

7.1.1. Natural

7.1.2. Artificial

Chapter 8. Global Sugar Substitutes Market By Form Insights & Trends, Revenue (USD Million)

8.1. By Form Dynamics & Market Share, 2019–2032

8.1.1. Powder

8.1.2. Liquid

8.1.3. Crystal/Granular

8.1.4. Tablet

Chapter 9. Global Sugar Substitutes Market By Application Insights & Trends, Revenue (USD Million)

9.1. Application Dynamics & Market Share, 2019–2032

9.1.1. Food Products

9.1.1.1. Bakery & Confectionery

9.1.1.2. Dairy & Frozen Desserts

9.1.1.3. Snacks & Cereals

9.1.2. Beverages

9.1.2.1. Soft Drinks

9.1.2.2. Juices

9.1.2.3. Energy Drinks

9.1.2.4. Functional Beverages

9.1.3. Pharmaceuticals

9.1.3.1. Syrups

9.1.3.2. Tablets & Lozenges

9.1.4. Nutraceuticals & Dietary Supplements

9.1.5. Personal Care & Cosmetics

9.1.5.1. Toothpaste

9.1.5.2. Mouthwash

9.1.5.3. Sugar-free chewing gums)

Chapter 10. Global Sugar Substitutes Market By End Use Insights & Trends, Revenue (USD Million)

10.1. End Use Dynamics & Market Share, 2019–2032

10.1.1. Food & Beverage Manufacturers

10.1.2. Pharmaceutical Companies

10.1.3. Nutraceutical & Dietary Supplement Producers

10.1.4. Household Consumers

Chapter 11. Global Sugar Substitutes Market Regional Outlook

11.1. Sugar Substitutes Market Share By Region, 2019–2032

11.2. North America

11.2.1. North America Market By Type Insights & Trends, Revenue (USD Million)

11.2.2. High-Intensity Sweeteners (HIS)

11.2.2.1. Aspartame

11.2.2.2. Sucralose

11.2.2.3. Saccharin

11.2.2.4. Acesulfame-K

11.2.2.5. Stevia

11.2.2.6. Monk Fruit

11.2.2.7. Neotame

11.2.2.8. Advantame

11.2.3. Low-Intensity Sweeteners (LIS)

11.2.3.1. Sorbitol

11.2.3.2. Xylitol

11.2.3.3. Mannitol

11.2.3.4. Erythritol

11.2.3.5. Maltitol

11.2.3.6. Lactitol

11.2.4. Novel Sweeteners

11.2.4.1. Allulose

11.2.4.2. Tagatose

11.2.4.3. Brazzein

11.2.4.4. Thaumatin

11.2.5. North America Sugar Substitutes Market By Source Insights & Trends, Revenue (USD Million)

11.2.5.1. Natural

11.2.5.2. Artificial

11.2.6. North America Sugar Substitutes Market By Form Insights & Trends, Revenue (USD Million)

11.2.6.1. Powder

11.2.6.2. Liquidza

11.2.6.3. Crystal/Granular

11.2.6.4. Tablet

11.2.7. North America Sugar Substitutes Market By Application Insights & Trends, Revenue (USD Million)

11.2.7.1. Food Products

11.2.7.1.1. Bakery & Confectionery

11.2.7.1.2. Dairy & Frozen Desserts

11.2.7.1.3. Snacks & Cereals

11.2.7.2. Beverages

11.2.7.2.1. Soft Drinks

11.2.7.2.2. Juices

11.2.7.2.3. Energy Drinks

11.2.7.2.4. Functional Beverages

11.2.7.3. Pharmaceuticals

11.2.7.3.1. Syrups

11.2.7.3.2. Tablets & Lozenges

11.2.7.4. Nutraceuticals & Dietary Supplements

11.2.7.5. Personal Care & Cosmetics

11.2.7.5.1. Toothpaste

11.2.7.5.2. Mouthwash

11.2.7.5.3. Sugar-free chewing gums)

11.2.8. North America Sugar Substitutes Market By End Use Insights & Trends,

Revenue (USD Million)

11.2.9. Food Products

11.2.9.1. Bakery & Confectionery

11.2.9.2. Dairy & Frozen Desserts

11.2.9.3. Snacks & Cereals

11.2.10. Beverages

11.2.10.1. Soft Drinks

11.2.10.2. Juices

11.2.10.3. Energy Drinks

11.2.10.4. Functional Beverages

11.2.11. Pharmaceuticals

11.2.11.1. Syrups

11.2.11.2. Tablets & Lozenges

11.2.12. Nutraceuticals & Dietary Supplements

11.2.13. Personal Care & Cosmetics

11.2.13.1. Toothpaste

11.2.13.2. Mouthwash

11.2.13.3. Sugar-free chewing gums

11.2.14. North America Market By Country, Market Estimates and Forecast, USD Million, 2025-2032

11.2.14.1. US

11.2.14.2. Canada

11.2.14.3. Mexico

11.3. Europe

11.3.1. Europe Market By Type Insights & Trends, Revenue (USD Million)

11.3.2. High-Intensity Sweeteners (HIS)

11.3.2.1. Aspartame

11.3.2.2. Sucralose

11.3.2.3. Saccharin

11.3.2.4. Acesulfame-K

11.3.2.5. Stevia

11.3.2.6. Monk Fruit

11.3.2.7. Neotame

11.3.2.8. Advantame

11.3.3. Low-Intensity Sweeteners (LIS)

11.3.3.1. Sorbitol

11.3.3.2. Xylitol

11.3.3.3. Mannitol

11.3.3.4. Erythritol

11.3.3.5. Maltitol

11.3.3.6. Lactitol

11.3.4. Novel Sweeteners

11.3.4.1. Allulose

11.3.4.2. Tagatose

11.3.4.3. Brazzein

11.3.4.4. Thaumatin

11.3.5. Europe Sugar Substitutes Market By Source Insights & Trends, Revenue (USD Million)

11.3.5.1. Natural

11.3.5.2. Artificial

11.3.6. Europe Sugar Substitutes Market By Form Insights & Trends, Revenue (USD Million)

11.3.6.1. Powder

11.3.6.2. Liquidza

11.3.6.3. Crystal/Granular

11.3.6.4. Tablet

11.3.7. Europe Sugar Substitutes Market By Application Insights & Trends, Revenue (USD Million)

11.3.7.1. Food Products

11.3.7.1.1. Bakery & Confectionery

11.3.7.1.2. Dairy & Frozen Desserts

11.3.7.1.3. Snacks & Cereals

11.3.7.2. Beverages

11.3.7.2.1. Soft Drinks

11.3.7.2.2. Juices

11.3.7.2.3. Energy Drinks

11.3.7.2.4. Functional Beverages

11.3.7.3. Pharmaceuticals

11.3.7.3.1. Syrups

11.3.7.3.2. Tablets & Lozenges

11.3.7.4. Nutraceuticals & Dietary Supplements

11.3.7.5. Personal Care & Cosmetics

11.3.7.5.1. Toothpaste

11.3.7.5.2. Mouthwash

11.3.7.5.3. Sugar-free chewing gums)

11.3.8. Europe Sugar Substitutes Market By End Use Insights & Trends, Revenue

(USD Million)

11.3.9. Food Products

11.3.9.1. Bakery & Confectionery

11.3.9.2. Dairy & Frozen Desserts

11.3.9.3. Snacks & Cereals

11.3.10. Beverages

11.3.10.1. Soft Drinks

11.3.10.2. Juices

11.3.10.3. Energy Drinks

11.3.10.4. Functional Beverages

11.3.11. Pharmaceuticals

11.3.11.1. Syrups

11.3.11.2. Tablets & Lozenges

11.3.12. Nutraceuticals & Dietary Supplements

11.3.13. Personal Care & Cosmetics

11.3.13.1. Toothpaste

11.3.13.2. Mouthwash

11.3.13.3. Sugar-free chewing gums

11.3.14. Europe Market By Country, Market Estimates and Forecast, USD Million,

11.3.14.1. Germany

11.3.14.2. France

11.3.14.3. U.K

11.3.14.4. Italy

11.3.14.5. Spain

11.3.14.6. Benelux

11.3.14.7. Russia

11.3.14.8. Finland

11.3.14.9. Sweden

11.3.14.10. Rest Of Europe

11.4. Asia-Pacific

11.4.1. Asia-Pacific Market By Type Insights & Trends, Revenue (USD Million)

11.4.2. High-Intensity Sweeteners (HIS)

11.4.2.1. Aspartame

11.4.2.2. Sucralose

11.4.2.3. Saccharin

11.4.2.4. Acesulfame-K

11.4.2.5. Stevia

11.4.2.6. Monk Fruit

11.4.2.7. Neotame

11.4.2.8. Advantame

11.4.3. Low-Intensity Sweeteners (LIS)

11.4.3.1. Sorbitol

11.4.3.2. Xylitol

11.4.3.3. Mannitol

11.4.3.4. Erythritol

11.4.3.5. Maltitol

11.4.3.6. Lactitol

11.4.4. Novel Sweeteners

11.4.4.1. Allulose

11.4.4.2. Tagatose

11.4.4.3. Brazzein

11.4.4.4. Thaumatin

11.4.5. Asia-Pacific Sugar Substitutes Market By Source Insights & Trends, Revenue

(USD Million)

11.4.5.1. Natural

11.4.5.2. Artificial

11.4.6. Asia-Pacific Sugar Substitutes Market By Form Insights & Trends, Revenue

(USD Million)

11.4.6.1. Powder

11.4.6.2. Liquidza

11.4.6.3. Crystal/Granular

11.4.6.4. Tablet

11.4.7. Asia-Pacific Sugar Substitutes Market By Application Insights & Trends,

Revenue (USD Million)

11.4.7.1. Food Products

11.4.7.1.1. Bakery & Confectionery

11.4.7.1.2. Dairy & Frozen Desserts

11.4.7.1.3. Snacks & Cereals

11.4.7.2. Beverages

11.4.7.2.1. Soft Drinks

11.4.7.2.2. Juices

11.4.7.2.3. Energy Drinks

11.4.7.2.4. Functional Beverages

11.4.7.3. Pharmaceuticals

11.4.7.3.1. Syrups

11.4.7.3.2. Tablets & Lozenges

11.4.7.4. Nutraceuticals & Dietary Supplements

11.4.7.5. Personal Care & Cosmetics

11.4.7.5.1. Toothpaste

11.4.7.5.2. Mouthwash

11.4.7.5.3. Sugar-free chewing gums)

11.4.8. Asia-Pacific Sugar Substitutes Market By End Use Insights & Trends, Revenue (USD Million)

11.4.9. Food Products

11.4.9.1. Bakery & Confectionery

11.4.9.2. Dairy & Frozen Desserts

11.4.9.3. Snacks & Cereals

11.4.10. Beverages

11.4.10.1. Soft Drinks

11.4.10.2. Juices

11.4.10.3. Energy Drinks

11.4.10.4. Functional Beverages

11.4.11. Pharmaceuticals

11.4.11.1. Syrups

11.4.11.2. Tablets & Lozenges

11.4.12. Nutraceuticals & Dietary Supplements

11.4.13. Personal Care & Cosmetics

11.4.13.1. Toothpaste

11.4.13.2. Mouthwash

11.4.13.3. Sugar-free chewing gums

11.4.14. Asia-Pacific Market By Country, Market Estimates and Forecast, USD Million,

11.4.14.1. China

11.4.14.2. India

11.4.14.3. Japan

11.4.14.4. South Korea

11.4.14.5. Indonesia

11.4.14.6. Thailand

11.4.14.7. Vietnam

11.4.14.8. Australia

11.4.14.9. New Zeland

11.4.14.10. Rest of APAC

11.5. Latin America

11.5.1. Latin America Market By Type Insights & Trends, Revenue (USD Million)

11.5.2. High-Intensity Sweeteners (HIS)

11.5.2.1. Aspartame

11.5.2.2. Sucralose

11.5.2.3. Saccharin

11.5.2.4. Acesulfame-K

11.5.2.5. Stevia

11.5.2.6. Monk Fruit

11.5.2.7. Neotame

11.5.2.8. Advantame

11.5.3. Low-Intensity Sweeteners (LIS)

11.5.3.1. Sorbitol

11.5.3.2. Xylitol

11.5.3.3. Mannitol

11.5.3.4. Erythritol

11.5.3.5. Maltitol

11.5.3.6. Lactitol

11.5.4. Novel Sweeteners

11.5.4.1. Allulose

11.5.4.2. Tagatose

11.5.4.3. Brazzein

11.5.4.4. Thaumatin

11.5.5. Latin America Sugar Substitutes Market By Source Insights & Trends, Revenue (USD Million)

11.5.5.1. Natural

11.5.5.2. Artificial

11.5.6. Latin America Sugar Substitutes Market By Form Insights & Trends, Revenue

(USD Million)

11.5.6.1. Powder

11.5.6.2. Liquidza

11.5.6.3. Crystal/Granular

11.5.6.4. Tablet

11.5.7. Latin America Sugar Substitutes Market By Application Insights & Trends,

Revenue (USD Million)

11.5.7.1. Food Products

11.5.7.1.1. Bakery & Confectionery

11.5.7.1.2. Dairy & Frozen Desserts

11.5.7.1.3. Snacks & Cereals

11.5.7.2. Beverages

11.5.7.2.1. Soft Drinks

11.5.7.2.2. Juices

11.5.7.2.3. Energy Drinks

11.5.7.2.4. Functional Beverages

11.5.7.3. Pharmaceuticals

11.5.7.3.1. Syrups

11.5.7.3.2. Tablets & Lozenges

11.5.7.4. Nutraceuticals & Dietary Supplements

11.5.7.5. Personal Care & Cosmetics

11.5.7.5.1. Toothpaste

11.5.7.5.2. Mouthwash

11.5.7.5.3. Sugar-free chewing gums)

11.5.8. Latin America Sugar Substitutes Market By End Use Insights & Trends,

Revenue (USD Million)

11.5.9. Food Products

11.5.9.1. Bakery & Confectionery

11.5.9.2. Dairy & Frozen Desserts

11.5.9.3. Snacks & Cereals

11.5.10. Beverages

11.5.10.1. Soft Drinks

11.5.10.2. Juices

11.5.10.3. Energy Drinks

11.5.10.4. Functional Beverages

11.5.11. Pharmaceuticals

11.5.11.1. Syrups

11.5.11.2. Tablets & Lozenges

11.5.12. Nutraceuticals & Dietary Supplements

11.5.13. Personal Care & Cosmetics

11.5.13.1. Toothpaste

11.5.13.2. Mouthwash

11.5.13.3. Sugar-free chewing gums

11.5.14. Latin America Market By Country, Market Estimates and Forecast, USD

Million,

11.5.14.1. Brazil

11.5.14.2. Rest of LATAM

11.6. Middle East & Africa

11.6.1. Middle East & Africa Market By Type Insights & Trends, Revenue (USD Million)

11.6.2. High-Intensity Sweeteners (HIS)

11.6.2.1. Aspartame

11.6.2.2. Sucralose

11.6.2.3. Saccharin

11.6.2.4. Acesulfame-K

11.6.2.5. Stevia

11.6.2.6. Monk Fruit

11.6.2.7. Neotame

11.6.2.8. Advantame

11.6.3. Low-Intensity Sweeteners (LIS)

11.6.3.1. Sorbitol

11.6.3.2. Xylitol

11.6.3.3. Mannitol

11.6.3.4. Erythritol

11.6.3.5. Maltitol

11.6.3.6. Lactitol

11.6.4. Novel Sweeteners

11.6.4.1. Allulose

11.6.4.2. Tagatose

11.6.4.3. Brazzein

11.6.4.4. Thaumatin

11.6.5. Middle East & Africa Sugar Substitutes Market By Source Insights & Trends,

Revenue (USD Million)

11.6.5.1. Natural

11.6.5.2. Artificial

11.6.6. Middle East & Africa Sugar Substitutes Market By Form Insights & Trends,

Revenue (USD Million)

11.6.6.1. Powder

11.6.6.2. Liquidza

11.6.6.3. Crystal/Granular

11.6.6.4. Tablet

11.6.7. Middle East & Africa Sugar Substitutes Market By Application Insights & Trends, Revenue (USD Million)

11.6.7.1. Food Products

11.6.7.1.1. Bakery & Confectionery

11.6.7.1.2. Dairy & Frozen Desserts

11.6.7.1.3. Snacks & Cereals

11.6.7.2. Beverages

11.6.7.2.1. Soft Drinks

11.6.7.2.2. Juices

11.6.7.2.3. Energy Drinks

11.6.7.2.4. Functional Beverages

11.6.7.3. Pharmaceuticals

11.6.7.3.1. Syrups

11.6.7.3.2. Tablets & Lozenges

11.6.7.4. Nutraceuticals & Dietary Supplements

11.6.7.5. Personal Care & Cosmetics

11.6.7.5.1. Toothpaste

11.6.7.5.2. Mouthwash

11.6.7.5.3. Sugar-free chewing gums)

11.6.8. Middle East & Africa Sugar Substitutes Market By End Use Insights & Trends, Revenue (USD Million)

11.6.9. Food Products

11.6.9.1. Bakery & Confectionery

11.6.9.2. Dairy & Frozen Desserts

11.6.9.3. Snacks & Cereals

11.6.10. Beverages

11.6.10.1. Soft Drinks

11.6.10.2. Juices

11.6.10.3. Energy Drinks

11.6.10.4. Functional Beverages

11.6.11. Pharmaceuticals

11.6.11.1. Syrups

11.6.11.2. Tablets & Lozenges

11.6.12. Nutraceuticals & Dietary Supplements

11.6.13. Personal Care & Cosmetics

11.6.13.1. Toothpaste

11.6.13.2. Mouthwash

11.6.13.3. Sugar-free chewing gums

11.6.13.3.1.

11.6.14. Middle East & Africa Market By Country, Market Estimates and Forecast, USD Million,

11.6.14.1. Saudi Arabia

11.6.14.2. Rest of MEA

Chapter 12. Competitive Landscape

12.1. Market Revenue Share By Manufacturers

12.2. Mergers & Acquisitions

12.3. Competitor’s Positioning

12.4. Strategy Benchmarking

12.5. Vendor Landscape

12.6. Distributors

12.6.1.1. North America

12.6.1.2. Europe

12.6.1.3. Asia Pacific

12.6.1.4. Middle East & Africa

12.6.1.5. Latin America

Chapter 13. Company Profiles

13.1. Cargill, Incorporated

13.1.1. Company Overview

13.1.2. Product & Service Offerings

13.1.3. Strategic Initiatives

13.1.4. Financials

13.2. Archer Daniels Midland Company

13.2.1. Company Overview

13.2.2. Product & Service Offerings

13.2.3. Strategic Initiatives

13.2.4. Financials

13.3. Tate & Lyle PLC

13.3.1. Company Overview

13.3.2. Product & Service Offerings

13.3.3. Strategic Initiatives

13.3.4. Financials

13.4. Ingredion Incorporated

13.4.1. Company Overview

13.4.2. Product & Service Offerings

13.4.3. Strategic Initiatives

13.4.4. Financials

13.5. Roquette Frères S.A.

13.5.1. Company Overview

13.5.2. Product & Service Offerings

13.5.3. Strategic Initiatives

13.5.4. Financials

13.6. E. I. du Pont de Nemours and Company

13.6.1. Company Overview

13.6.2. Product & Service Offerings

13.6.3. Strategic Initiatives

13.6.4. Financials

13.7. Ajinomoto Co., Inc.

13.7.1. Company Overview

13.7.2. Product & Service Offerings

13.7.3. Strategic Initiatives

13.7.4. Financials

13.7.5. Conclusion

13.8. GLG Life Tech Corporation

13.8.1. Company Overview

13.8.2. Product & Service Offerings

13.8.3. Strategic Initiatives

13.8.4. Financials

13.8.5. Conclusion

13.9. Nutrinova

13.9.1. Company Overview

13.9.2. Product & Service Offerings

13.9.3. Strategic Initiatives

13.9.4. Financials

13.9.5. Conclusion

13.10. Merisant

13.10.1. Company Overview

13.10.2. Product & Service Offerings

13.10.3. Strategic Initiatives

13.10.4. Financials

13.10.5. Conclusion

13.11. Whole Earth Brands, Inc.

13.11.1. Company Overview

13.11.2. Product & Service Offerings

13.11.3. Strategic Initiatives

13.11.4. Financials

13.11.5. Conclusion

13.12. JK Sucralose Inc.

13.12.1. Company Overview

13.12.2. Product & Service Offerings

13.12.3. Strategic Initiatives

13.12.4. Financials

13.12.5. Conclusion

13.13. PureCircle Ltd.

13.13.1. Company Overview

13.13.2. Product & Service Offerings

13.13.3. Strategic Initiatives

13.13.4. Financials

13.13.5. Conclusion

13.14. Sensient Technologies Corporation

13.14.1. Company Overview

13.14.2. Product & Service Offerings

13.14.3. Strategic Initiatives

13.14.4. Financials

13.14.5. Conclusion

13.15. Global Sweeteners Holdings Limited

13.15.1. Company Overview

13.15.2. Product & Service Offerings

13.15.3. Strategic Initiatives

13.15.4. Financials

13.15.5. Conclusion

13.16. Niutang Chemical Co., Ltd.

13.16.1. Company Overview

13.16.2. Product & Service Offerings

13.16.3. Strategic Initiatives

13.16.4. Financials

13.16.5. Conclusion

13.17. Tereos S.A.

13.17.1. Company Overview

13.17.2. Product & Service Offerings

13.17.3. Strategic Initiatives

13.17.4. Financials

13.17.5. Conclusion

13.18. Cumberland Packing Corporation

13.18.1. Company Overview

13.18.2. Product & Service Offerings

13.18.3. Strategic Initiatives

13.18.4. Financials

13.18.5. Conclusion

13.19. Tag Ingredients India Pvt Ltd.

13.19.1. Company Overview

13.19.2. Product & Service Offerings

13.19.3. Strategic Initiatives

13.19.4. Financials

13.19.5. Conclusion

13.20. Suminter India Organics

1. Company Overview

2. Product & Service Offerings

3. Strategic Initiatives

4. Financials

5. Conclusion

Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP has segmented Global Sugar Substitutes market on the basis of By Type, By Source, By Form, By Application, By End Use and By region for 2019 to 2032

Global Sugar Substitutes Systems Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Global Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Global Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Global Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Global Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

North America

North America Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

North America Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

North America Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

North America Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

North America Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

U.S

U.S Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

U.S Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

U.S Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

U.S Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

U.S Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Canada

Canada Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Canada Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Canada Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Canada Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Canada Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Mexico

Mexico Drones Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Mexico Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Mexico Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Mexico Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Mexico Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Europe

Europe Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Europe Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Europe Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Europe Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Europe Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Germany

Germany Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Germany Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Germany Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Germany Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Germany Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

France

France Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

France Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

France Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

France Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

France Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

U.K

U.K Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

U.K Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

U.K Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

U.K Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

U.K Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Italy

Italy Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Italy Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Italy Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Italy Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Italy Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Benelux

Benelux Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Benelux Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Benelux Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Benelux Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Benelux Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Russia

Russia Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Russia Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Russia Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Russia Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Russia Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Finland

Finland Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Finland Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Finland Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Finland Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Finland Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Sweden

Sweden Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Sweden Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Sweden Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Sweden Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Sweden Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Rest of Europe

Rest of Europe Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Rest of Europe Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Rest of Europe Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Rest of Europe Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Rest of Europe Sugar Substitutes Systems Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Asia-Pacific

Asia-Pacific Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Asia-Pacific Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Asia-Pacific Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Asia-Pacific Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Asia-Pacific Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

China

China Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

China Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

China Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

China Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

China Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

India

India Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

India Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

India Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

India Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

India Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Japan

Japan Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Japan Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Japan Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Japan Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Japan Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Indonesia

Indonesia Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Indonesia Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Indonesia Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Indonesia Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Indonesia Sugar Substitutes Systems Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Thailand

Thailand Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Thailand Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Thailand Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Thailand Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Thailand Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Vietnam

Vietnam Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Vietnam Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Vietnam Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Vietnam Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Vietnam Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

Australia

Australia Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

Australia Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

Australia Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet

Australia Sugar Substitutes Market By Application Outlook, Revenue (USD Million)

- Food Products

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Cereals

- Beverages

- Soft Drinks

- Juices

- Energy Drinks

- Functional Beverages

- Pharmaceuticals

- Syrups

- Tablets & Lozenges

- Nutraceuticals & Dietary Supplements

- Personal Care & Cosmetics

- Toothpaste

- Mouthwash

- Sugar-free chewing gums

Australia Sugar Substitutes Market By End Use Outlook, Revenue (USD Million)

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Nutraceutical & Dietary Supplement Producers

- Household Consumers

New Zealand

New Zealand Sugar Substitutes Market By Type Outlook (Revenue, USD Million)

- High-Intensity Sweeteners (HIS)

- Aspartame

- Sucralose

- Saccharin

- Acesulfame-K

- Stevia

- Monk Fruit

- Neotame

- Advantame

- Low-Intensity Sweeteners (LIS)

- Sorbitol

- Xylitol

- Mannitol

- Erythritol

- Maltitol

- Lactitol

- Novel Sweeteners

- Allulose

- Tagatose

- Brazzein

- Thaumatin

New Zealand Sugar Substitutes By Source Outlook (Revenue, USD Million)

- Natural

- Artificial

New Zealand Sugar Substitutes By Form (Revenue, USD Million

- Powder

- Liquid

- Crystal/Granular

- Tablet