Back to Electronics and Semiconductor

Global SiC-on-Insulator (SiCOI) Film Market

Published Date : November 27, 2025 Category: Electronics and Semiconductor

Published Date : November 27, 2025 Category: Electronics and Semiconductor

The Global SiC-on-Insulator (SiCOI) Film Market is advancing quickly as industries shift toward high-efficiency, thermally stable, and electrically isolated semiconductor platforms. The growing need for next-generation power electronics, RF systems, photonics, and high-temperature sensors is transforming SiCOI films from niche research materials into strategic components for commercial semiconductor innovation. As traditional silicon-based devices reach performance ceilings, SiCOI offers a unique pathway to higher voltage tolerance, faster switching, extreme environment reliability, and superior isolation compared to bulk SiC or SOI structures.

The transition toward EV powertrains, 5G/6G RF modules, aerospace electronics, renewable energy converters, and quantum-ready photonic platforms is accelerating the adoption of engineered SiC-on-insulator architectures. Manufacturers are investing heavily in optimized layer-transfer technologies, ultra-smooth SiC thin films, high-uniformity oxide structures, and precision-engineered substrates to achieve better device yields and performance. As digital engineering and advanced semiconductor materials converge, SiCOI films are becoming essential to enabling next-generation device scaling.

Market Overview

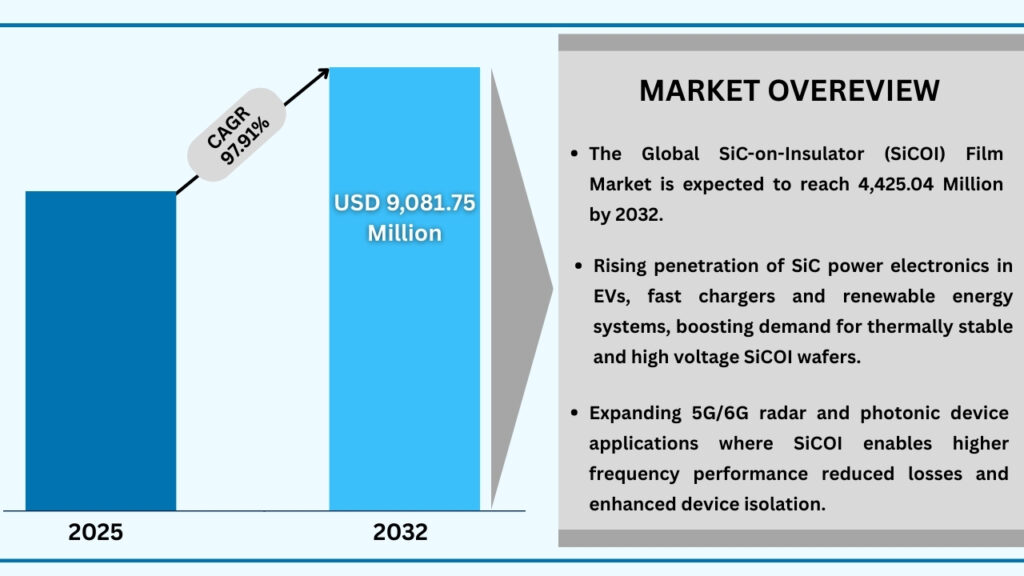

The global SiC-on-Insulator Film Market is experiencing robust growth driven by the need for highly efficient, reliable, and thermally resilient semiconductor substrates. As demand rises for wide-bandgap electronics with superior isolation, SiCOI solutions are being rapidly adopted across automotive, telecom, aerospace, industrial, and photonics sectors.

Engineers and device makers are implementing SiCOI platforms to overcome long-standing challenges associated with bulk SiC, including parasitic conduction, thermal runaway, limited isolation, and manufacturing defects. With advancements in ion-cut, Smart-Cut, direct bonding, chemical–mechanical polishing, and epitaxial engineering, SiCOI films are achieving levels of uniformity and structural integrity suitable for high-volume production.

High thermal conductivity, low leakage, enhanced breakdown strength, and mechanical stability are making SiCOI a preferred substrate for modern electronic and photonic systems. As industries invest in electrification, automation, and high-frequency systems, SiCOI adoption is poised to scale significantly.

Market Definition

The SiC-on-Insulator Film Market encompasses advanced substrates, engineered films, bonding technologies, and processing frameworks that integrate silicon carbide layers onto insulating materials such as silicon dioxide, sapphire, or engineered oxides. These materials combine the high-temperature, high-power advantages of SiC with the electrical isolation benefits of insulator platforms.

SiCOI films support a wide range of applications, including:

The market blends wafer-level bonding, epitaxial film growth, CMP planarization, substrate thinning, and advanced metrology to achieve ultra-smooth, defect-controlled SiC layers suitable for precision device fabrication.

Advancements in SiCOI Engineering & Film Architecture Evolution

Recent technological progress has transformed SiCOI engineering from exploratory research to highly structured commercial development. Innovations are emerging in film uniformity, defect minimization, and interface optimization.

Key advancements include:

Performance improvements now extend to controlling thermal interface resistance, managing film stress, and optimizing optical and electrical properties for high-frequency systems. As GPU-accelerated computing and digital metrology advance, fabrication cycles are becoming more repeatable and scalable.

Market Challenges, Structural Limitations & Technical Barriers

Despite strong momentum, the SiCOI film market faces material, engineering, and economic challenges that may constrain near-term adoption. Producing highly uniform, low-defect SiC films requires sophisticated equipment, highly skilled personnel, and multi-step bonding and thinning processes.

Key issues include:

Manufacturers must also invest in precision bonding tools, metrology solutions, high-temperature annealing systems, and advanced CMP infrastructure. Standardization, scale-up, and cost reduction remain essential for wider commercial penetration.

Policy, Industry Shifts & Evolution of Semiconductor Testing Ecosystems

Governments, regulatory bodies, and semiconductor consortiums are increasingly prioritizing wide-bandgap materials—including SiC, GaN, and SiCOI—as essential technologies for national energy goals, EV electrification, aerospace missions, and advanced telecommunications.

Initiatives include:

These policy movements, combined with the semiconductor industry’s shift toward digital engineering, are accelerating adoption of engineered substrates like SiCOI.

Integration of AI, Automation & Advanced Digital Processing

AI is redefining how SiCOI films are engineered, inspected, and optimized. Machine learning algorithms assist in:

Digital twins and simulation-based engineering are helping manufacturers predict film performance under electrical, thermal, and mechanical loads. These technologies are reducing trial-and-error cycles, improving wafer yields, and lowering production costs.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing region for SiCOI due to strong semiconductor manufacturing bases in China, Japan, South Korea, Taiwan, and India. Investment in EVs, 5G networks, robotics, and power electronics is boosting demand. Governments are funding wide-bandgap material research and next-gen fab infrastructure.

Europe

Europe is a significant market driven by automotive electrification, aerospace programs, industrial automation, and high-frequency technologies. Germany, France, Italy, Sweden, and the UK are advancing SiCOI R&D through university–industry collaborations and state-supported innovation programs.

North America

North America leads in early-stage SiCOI research, defense-grade electronics, and high-performance RF applications. Strong demand from EV manufacturers, aerospace agencies, industrial OEMs, and quantum photonics startups is shaping rapid adoption.

Competitive Landscape

The SiCOI market is moderately consolidated, with participation from engineered substrate companies, SiC material specialists, semiconductor fabs, and advanced packaging providers. Competition centers on wafer uniformity, bonding precision, defect reduction, intellectual property, and cost-effective scaling.

Key players include:

Companies are focusing on refined Smart-Cut techniques, hybrid bonding, AI-powered metrology, and collaborations with power electronics and RF device manufacturers to expand market presence.

Strategic Industry Developments

Scale-Up of Large-Diameter SiCOI Wafers (2025)

A major substrate manufacturer expanded its 150mm and 200mm SiCOI wafer production line to support rising demand from automotive and telecom power device makers. The initiative enhances uniformity, yield, and high-volume throughput.

Joint Engineering Initiatives for Advanced Film Bonding (2025)

In 2025, a semiconductor equipment provider partnered with a leading SiC substrate company to co-develop next-generation bonding systems, CMP optimization protocols, and advanced dielectric stack architectures to improve SiCOI reliability.

Future Market Outlook & Emerging Opportunities

The SiCOI Film Market is transitioning toward high-volume commercialization supported by:

Long-term growth will be driven by increasing electrification, 5G/6G expansion, renewable energy conversion, industrial automation, and quantum photonic device development.

Conclusion

The Global SiC-on-Insulator (SiCOI) Film Market is entering a phase of rapid technological and commercial evolution. With advancements in engineered substrates, bonding technology, digital metrology, and AI-driven manufacturing, SiCOI is becoming a transformational material for next-generation semiconductors. As industries demand higher performance, extreme reliability, and energy-efficient solutions, SiCOI films will play a vital role in the future of power electronics, RF systems, aerospace electronics, and photonic integration.

At Advantia Business Consulting, we help semiconductor leaders turn SiCOI opportunity into strategic advantage. From market intelligence and partner scouting to commercialization roadmaps and scale-up risk mitigation, our advisory services bridge the gap between research breakthroughs and high-volume production. Contact Advantia Business Consulting to explore a tailored strategy that accelerates SiCOI adoption and captures value across EV power, RF, photonics, and aerospace applications.