Market Synopsis

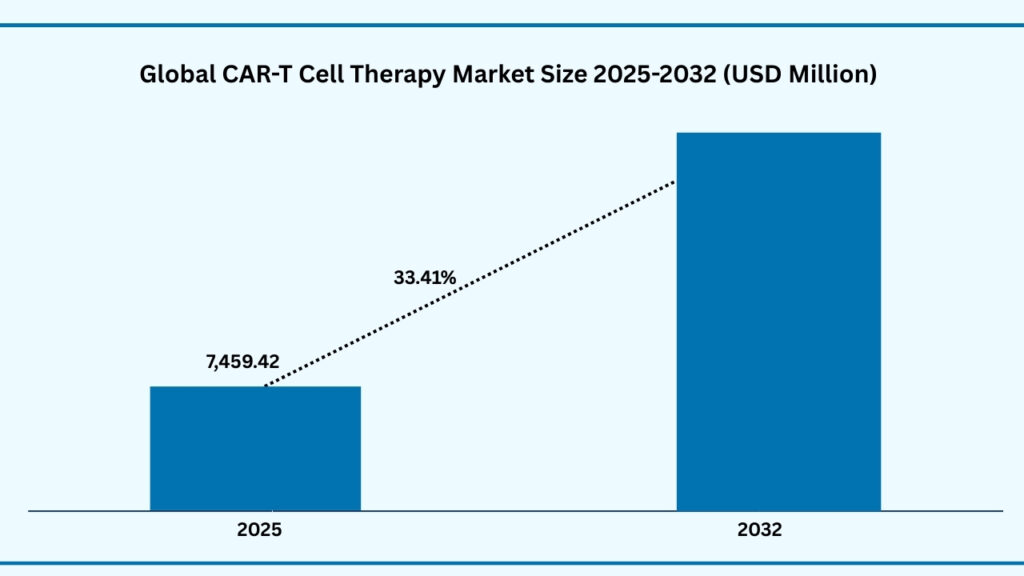

The global CAR-T Cell Therapy market size was USD 5,395.26 million in 2024 and is expected to reach USD 72,597.71 million during a forecast period from 2025-2032 at a CAGR of 38.41%. The global CAR T-cell therapy market is experiencing strong momentum, supported by the growing burden of cancer, high response rates in difficult-to-treat cases, and broader regulatory approvals. The therapy is gaining recognition as a breakthrough in personalized medicine, with ongoing innovations in gene editing and manufacturing expanding its applications into solid tumors and even autoimmune diseases. North America currently dominates the market due to advanced infrastructure and early adoption, while Asia-Pacific is emerging as the fastest-growing region with significant investments in local clinical programs. Although high treatment costs and complex manufacturing remain key challenges, advancements in automation and scalable production technologies are helping address these barriers. Together, these trends position CAR T-cell therapy as a cornerstone of future cancer treatment and long-term market growth.

Global CAR-T Cell Therapy Market (USD Million)

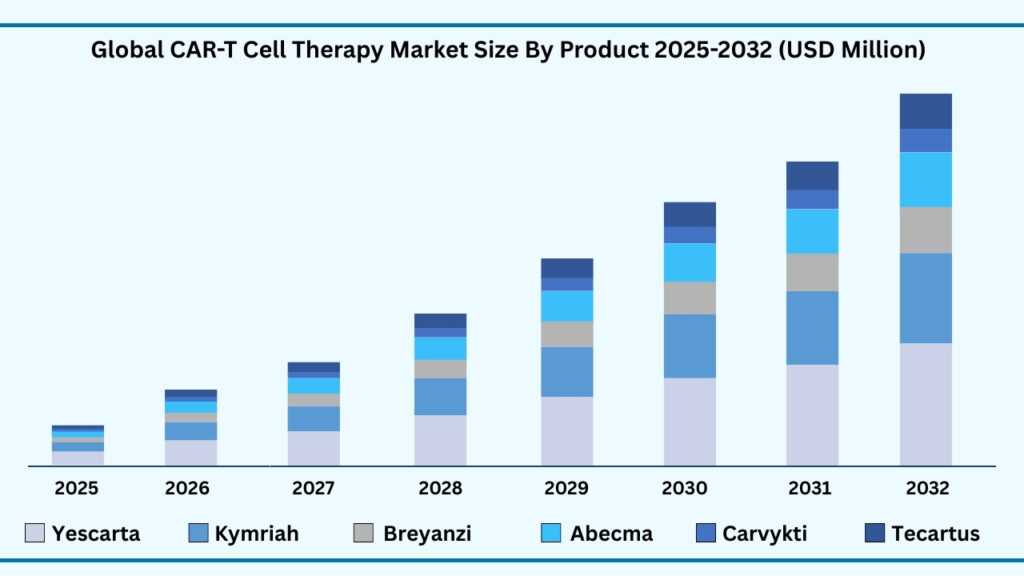

Global CAR T Cell Therapy Market by Product Type Insights:

Yescarta and Kymriah segments accounted for 54.54% of share in 2025 in Global CAR-T Cell Therapy market.

The Yescarta (Axicabtagene Ciloleucel) and Kymriah (Tisagenlecleucel) segments together accounted for the largest share of the global CAR T-cell therapy market in 2025, representing 54.54% of total revenues. Yescarta is projected to grow at a CAGR of 38.54%, while Kymriah is expected to expand at 39.02% during 2025–2032, with their combined revenues anticipated to reach USD 40,568.66 million by 2032. Their dominance stems from proven clinical outcomes, expanded regulatory approvals, and strong commercialization networks by Gilead Sciences and Novartis, ensuring global accessibility and sustained adoption. Meanwhile, Breyanzi (Lisocabtagene Maraleucel) has gained traction with its differentiated safety profile and flexible dosing strategy, making it a preferred alternative in relapsed and refractory lymphoma. Backed by Bristol Myers Squibb, it continues to grow through label expansions and global clinical trial activity.

Abecma (Idecabtagene Vicleucel) plays a vital role in multiple myeloma treatment, particularly for patients who have exhausted prior therapies. Its rapid adoption is supported by robust real-world evidence of durable responses, while Bristol Myers Squibb and 2seventy bio are investing heavily in expanding production to meet rising demand across the U.S. and Europe. At the same time, Carvykti (Ciltacabtagene Autoleucel / Cilta-cel) is emerging as the fastest-growing therapy, with efficacy rates of nearly 98% making it the preferred option in multiple myeloma. Janssen Biotech and Legend Biotech are scaling up global manufacturing capacity and patient access programs to accelerate uptake, especially across Asia and Europe, driving significant revenue growth over the forecast horizon.

Tecartus (Brexucabtagene Autoleucel), developed by Kite Pharma, has established a strong foothold in mantle cell lymphoma (MCL) and acute lymphoblastic leukemia (ALL), supported by favourable reimbursement policies and regional approvals. Its clinical value and ongoing trial programs position it for steady expansion into broader hematologic malignancy indications. Together, these six therapies illustrate how the CAR T-cell therapy market is diversifying, with Yescarta and Kymriah driving scale, Carvykti advancing on unmatched efficacy, and others like Breyanzi, Abecma, and Tecartus fulfilling critical gaps in hematologic oncology. This balance of innovation and competition underscores the dynamic growth trajectory of the global market.

Global CAR-T Cell Therapy Market, By Product Type (USD Million)

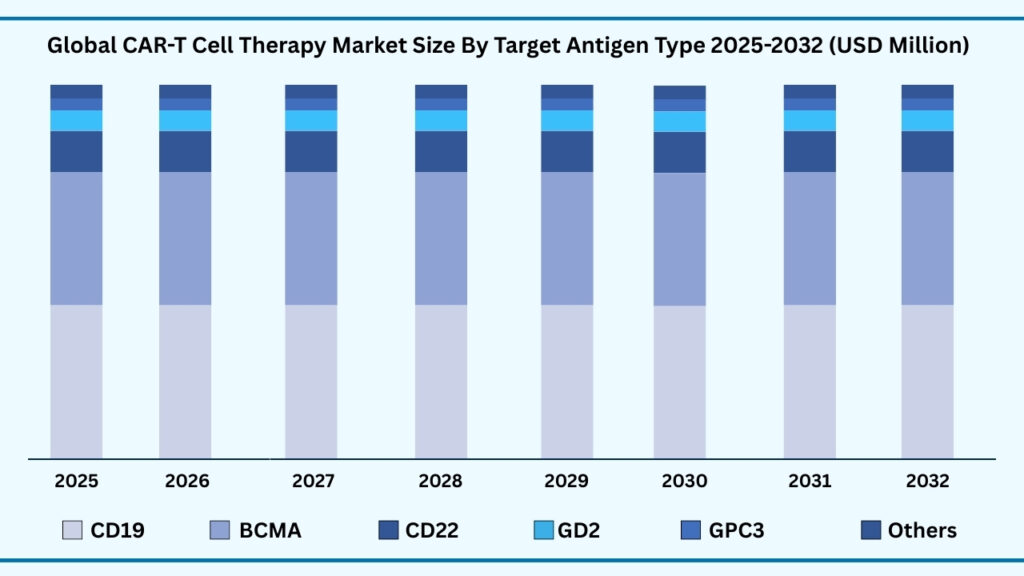

Global CAR T Cell Therapy Market by Target Antigen Type Insights:

CD19 (Cluster of Differentiation 19) segment accounted for 48.58% of share in 2025 in Global CAR-T Cell Therapy market.

The global CAR T-cell therapy market, when segmented by target antigen type, includes CD19, BCMA, CD22, GD2, HER2, GPC3, and Others (such as EGFRvIII, CD7, CD123, and mesothelin). Among these, the CD19 (Cluster of Differentiation 19) segment held the largest revenue share of 48.58% in 2025 and is projected to register a CAGR of 38.66% during the forecast period, reaching USD 36,102.21 million by 2032. CD19’s dominance is driven by its proven clinical effectiveness in treating B-cell malignancies like acute lymphoblastic leukemia (ALL) and non-Hodgkin lymphoma (NHL). Widely commercialized therapies including Yescarta, Kymriah, and Breyanzi target this antigen, ensuring strong physician confidence, broad regulatory support, and global accessibility—factors that firmly position CD19 as the foundation of the CAR T-cell therapy landscape.

BCMA (B-cell Maturation Antigen) has emerged as the next most influential target, demonstrating remarkable efficacy in multiple myeloma. Flagship therapies such as Abecma and Carvykti have accelerated market momentum, with Carvykti reporting near 98% response rates, reinforcing BCMA’s rapid growth trajectory. At the same time, CD22 and GD2 are advancing through clinical studies, showing promise in both hematological and solid tumor indications. HER2 and GPC3 are generating attention for their potential in breast and liver cancers, although their commercial maturity is still in early phases. The “Others” category—covering targets like EGFRvIII, CD7, CD123, and mesothelin—represents the frontier of innovation, with next-generation CAR T therapies aiming to address hard-to-treat cancers and reduce relapse rates in high-risk patient populations.

Global CAR-T Cell Therapy Market, By Target Antigen Type (USD Million)

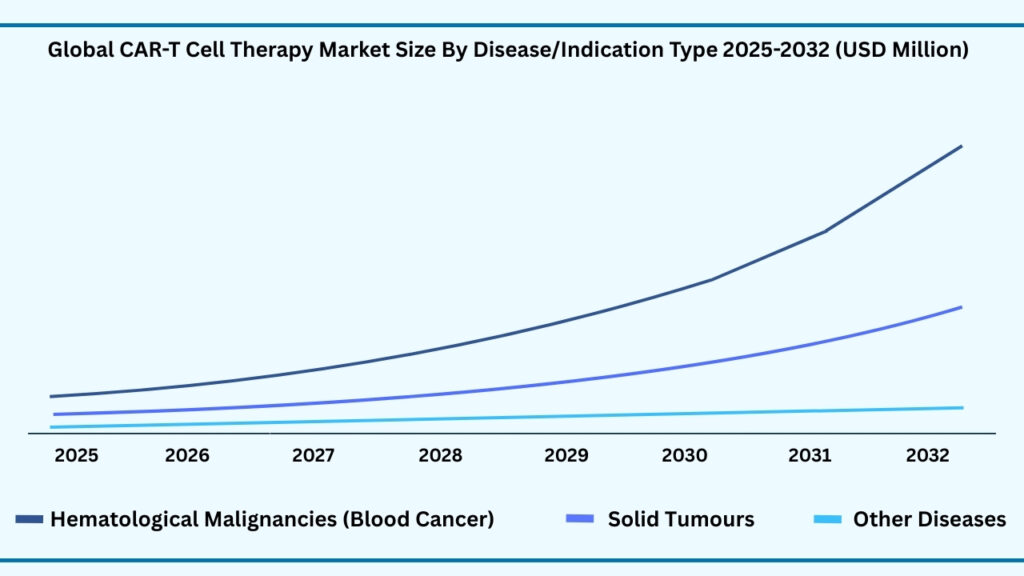

Global CAR T Cell Therapy Market by Disease/Indication Type Insights:

Hematologic Malignancies (Blood Cancers) segment accounted for 65.63% of share in 2025 in Global CAR-T Cell Therapy market.

The global CAR T-cell therapy market by disease/indication type is segmented into hematologic malignancies, solid tumors, and other diseases. Hematologic malignancies led with a 65.63% share in 2025 and are projected to grow at a CAGR of 38.69%, reaching USD 48,318.48 million by 2032. Their dominance is supported by the proven success of CAR T therapies in lymphoma, leukemia, and multiple myeloma. Within lymphoma, subtypes such as Diffuse Large B-cell Lymphoma (DLBCL), Primary Mediastinal B-cell Lymphoma (PMBCL), Mantle Cell Lymphoma (MCL), and Follicular Lymphoma (FL) respond strongly to CD19-targeted therapies like Yescarta, Kymriah, Breyanzi, and Tecartus. In leukemia, Acute Lymphoblastic Leukemia (ALL) achieved breakthroughs with Kymriah’s pediatric approval, while Chronic Lymphocytic Leukemia (CLL) is advancing in trials. Multiple myeloma, fueled by BCMA-directed therapies such as Abecma and Carvykti, is growing rapidly due to outstanding efficacy and durable responses.

In contrast, solid tumors remain an emerging frontier, limited by barriers like tumor microenvironment resistance and antigen heterogeneity. Despite these challenges, research momentum is rising across glioblastoma, pancreatic cancer, ovarian cancer, and lung cancer, with exploratory efforts in breast cancer, melanoma, prostate cancer, and colorectal cancer. Novel strategies such as dual-target CARs, localized delivery methods, and armored CAR constructs are showing promise, gradually improving clinical outcomes and signaling long-term growth potential in these indications.

The Other Diseases segment highlights CAR T’s expansion beyond oncology, with encouraging results in autoimmune disorders such as lupus and rheumatoid arthritis, and exploratory studies in infectious diseases including HIV and virus-associated cancers. Together, these advances illustrate a market where hematologic malignancies remain the growth engine, while solid tumors and other diseases represent high-reward opportunities. To sustain leadership, companies like Novartis, Gilead, Bristol Myers Squibb, and Janssen are consolidating their hematologic portfolios while strategically investing in next-generation pipelines, manufacturing scale-up, and patient access programs to drive the next wave of CAR T-cell therapy expansion.

Global CAR-T Cell Therapy Market, By Disease/Indication Type (USD Million)

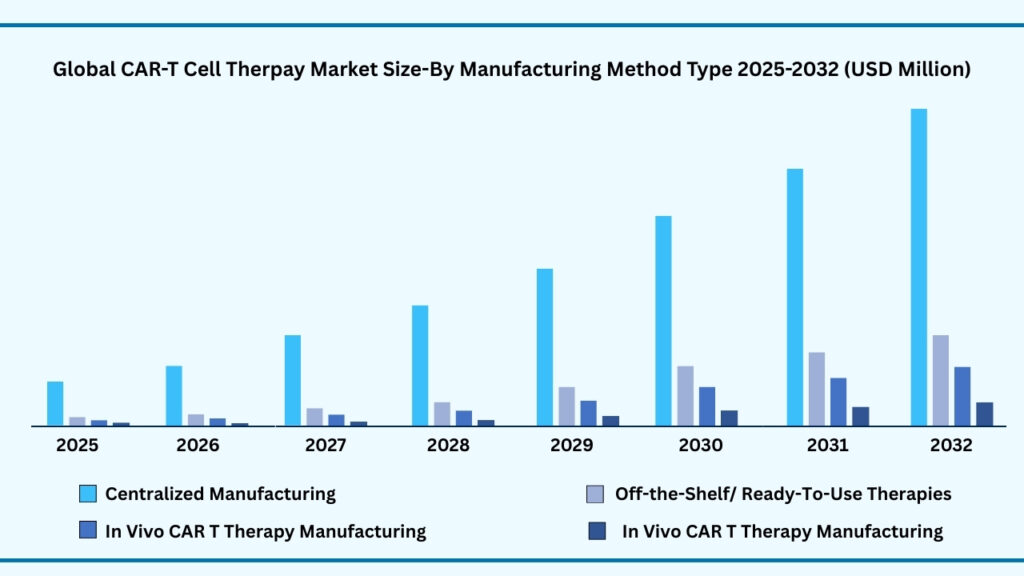

Global CAR T Cell Therapy Market by Manufacturing Method Type Insights:

Centralized Manufacturing segment accounted for 74.51% of share in 2025 in Global CAR-T Cell Therapy market.

Based on manufacturing method, the global CAR T-cell therapy market is segmented into Point-of-Care Manufacturing, Centralized Manufacturing, In-vivo CAR T Therapy Manufacturing, and Off-the-Shelf/Ready-to-Use Therapies. Among these, Centralized Manufacturing holds the largest share of 74.51% in 2025, projected to expand at a CAGR of 38.69% and reach USD 54,852.84 million by 2032. This dominance is driven by its established infrastructure, strict quality standards, and ability to deliver consistent therapies across global markets. Centralized facilities provide specialized expertise, regulatory compliance, and economies of scale, allowing leading companies to ensure reproducibility and reliability while meeting rising demand. Strong supply chains, cryopreservation advancements, and scalable production also make this model the backbone of current CAR T commercialization.

Meanwhile, other manufacturing approaches are emerging to address limitations of centralized models. Point-of-Care Manufacturing aims to reduce vein-to-vein time by producing therapies closer to patients, while In-vivo CAR T therapy manufacturing explores direct engineering of T-cells inside the body to streamline processes. Similarly, Off-the-Shelf or Ready-to-Use therapies, built on allogeneic cell platforms, promise scalable and more affordable options without the need for patient-specific cells. Though these approaches are still developing, they highlight a strong shift toward accessibility and cost-effectiveness. However, in the near term, Centralized Manufacturing will continue to dominate, offering the most reliable path to global scalability and fueling the rapid growth of the CAR T-cell therapy market.

Global CAR-T Cell Therapy MARKET, By manufacturing method Type (USD Million)

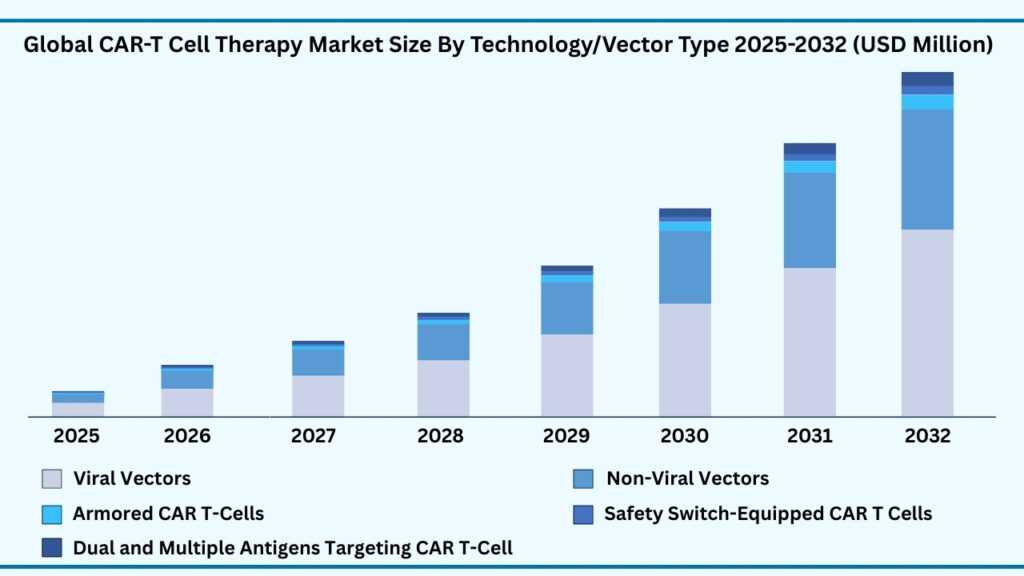

Global CAR T Cell Therapy Market by Manufacturing Method Type Insights:

Viral Vectors segment accounted for 72.34% of share in 2025 in Global CAR-T Cell Therapy market.

Based on technology/vector type, the global CAR T-cell therapy market is segmented into Viral Vectors, Non-Viral Vectors, Armored CAR T-Cells, Safety Switch-Equipped CAR T-Cells, and Dual & Multiple Antigen Targeting CAR T-Cells. Among these, Viral Vectors accounted for the largest revenue share of 73.21% in 2025 and are expected to grow at a CAGR of 38.69%, reaching USD 53,899.13 million by 2032. Their dominance is driven by the proven efficiency of lentiviral and retroviral vectors in enabling stable gene integration and robust expression of CAR constructs. Viral vector platforms are widely adopted due to their ability to generate long-lasting therapeutic effects, which is critical for sustained remission in cancer patients. This reliability has established viral vectors as the cornerstone of current CAR T-cell development and commercialization.

The growth of this segment is further fueled by continuous advancements in viral engineering that enhance safety, scalability, and production efficiency. Centralized manufacturing facilities equipped for viral vector production support large-scale clinical and commercial supply, ensuring global accessibility. While non-viral alternatives such as CRISPR/Cas9, transposons, and mRNA electroporation are gaining traction for their potential cost-effectiveness and reduced manufacturing complexity, they remain in earlier stages of adoption. At the same time, next-generation approaches like Armored CAR T-cells, Safety Switch-equipped therapies, and multi-antigen targeting platforms are shaping the future landscape by improving safety, durability, and efficacy. However, in the near-to-midterm, viral vectors are expected to retain their dominance as the most reliable and commercially viable backbone of CAR T-cell therapy manufacturing.

Global CAR-T Cell Therapy Market, By Technology/Vector Type (USD Million)

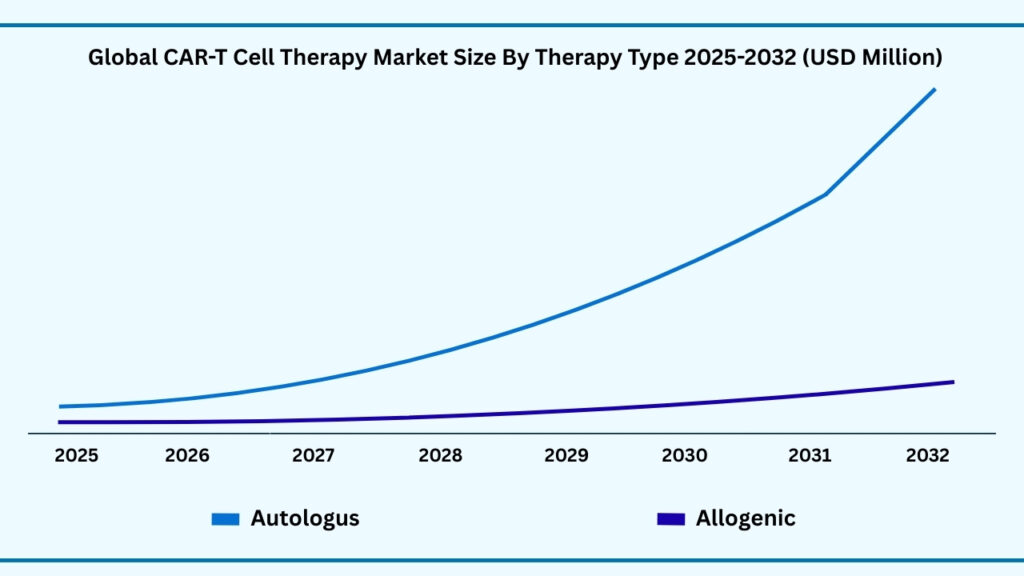

Global CAR T Cell Therapy Market by Therapy Type Insights:

Autologous segment accounted for 88.13% of share in 2025 in Global CAR-T Cell Therapy market.

Based on therapy type, the global CAR T-cell therapy market is segmented into Autologous and Allogeneic CAR T-cell therapies. Among these, the Autologous segment accounted for the largest revenue share of 88.13% in 2025 and is expected to register a CAGR of 38.76% during the forecast period, with revenues projected to reach USD 65,108.79 million. The dominance of this segment is attributed to its highly personalized approach, where T-cells are collected directly from the patient, genetically modified to express chimeric antigen receptors (CARs), and reinfused to specifically target cancer cells. This individualized method significantly reduces the risk of immune rejection and graft-versus-host disease, ensuring a higher safety profile and better therapeutic outcomes. Autologous CAR T therapies are particularly effective for patients with refractory or relapsed cancers, where conventional treatments have failed, making them the preferred choice in clinical practice.

The segment’s growth is further supported by its strong clinical adoption, as leading CAR T therapies currently approved and marketed globally are predominantly autologous in nature. These therapies have demonstrated remarkable remission rates in hematologic malignancies such as leukemia and lymphoma, building a strong foundation of trust among healthcare providers and patients. Moreover, advancements in manufacturing technologies are gradually reducing production times and improving scalability, which has historically been a challenge for personalized autologous treatments. At the same time, expanding clinical trials are exploring its application across solid tumors, broadening its therapeutic reach. While Allogeneic therapies promise off-the-shelf availability and faster turnaround times, Autologous CAR T-cell therapy continues to lead the market due to its established efficacy, safety, and regulatory approvals. This ensures that autologous approaches will remain the driving force behind CAR T-cell therapy growth in the coming years.

Global CAR-T Cell Therapy Market, By Therapy Type (USD Million)

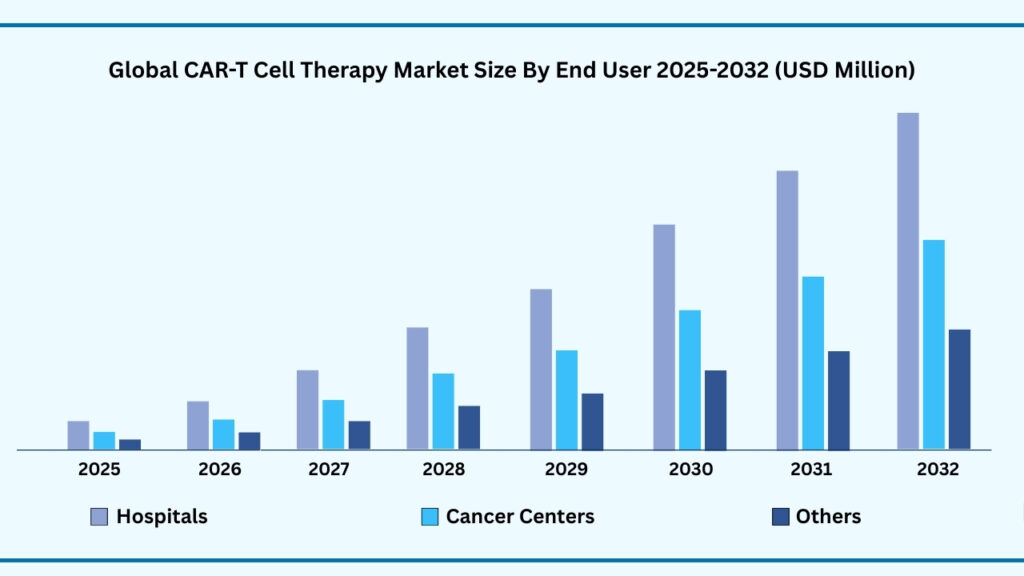

Global CAR T Cell Therapy Market by End User Insights:

Hospitals segment accounted for 49.46% of share in 2025 in Global CAR-T Cell Therapy market.

Based on end user segment, the global CAR T-cell therapy market is segmented into Hospitals, Cancer Treatment Centers, and Others (Academic & Research Institutes, Specialty Clinics). Hospitals accounted for the largest share of 49.46% in 2025 and are projected to grow at a CAGR of 38.69%, reaching USD 36,851.69 million. This leadership is driven by their advanced infrastructure, specialized oncology units, and capacity to manage complex procedures such as T-cell collection, modification, reinfusion, and post-treatment care. Hospitals also remain the most reliable settings for handling side effects like cytokine release syndrome and neurotoxicity, ensuring patient safety and treatment success.

The segment further benefits from strong collaborations with biopharma companies and research institutes, giving patients access to the latest therapies and clinical trials. Rising investments in hospital-based cell therapy units and the growing global cancer burden continue to expand demand. While cancer treatment centers and academic institutions contribute to innovation and specialty care, hospitals dominate due to their scale, comprehensive patient support, and integrated services, making them the cornerstone of CAR T-cell therapy adoption worldwide.

Global CAR-T Cell Therapy Market, By End User (USD Million)

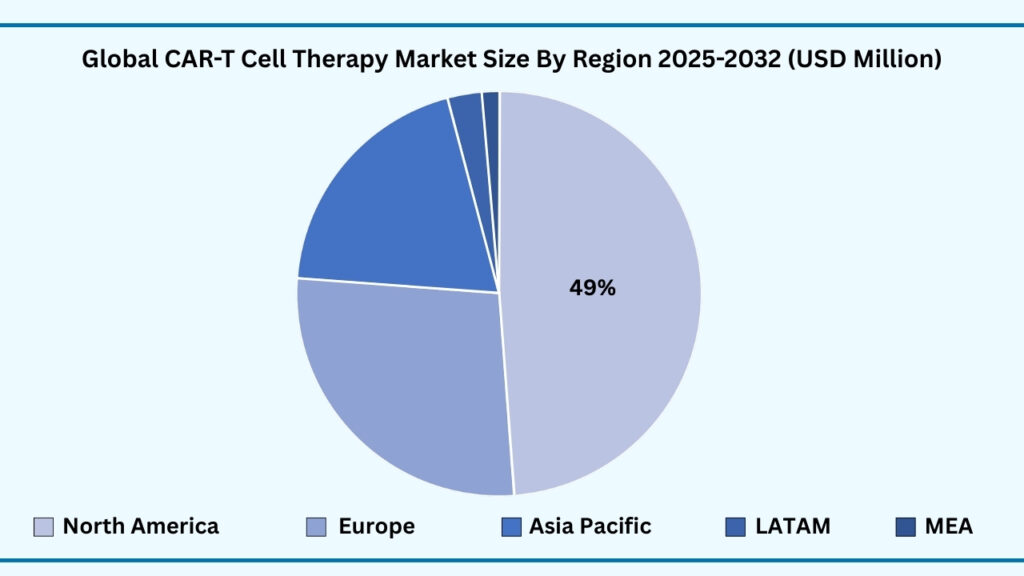

Global CAR T Cell Therapy Market by Region Insights:

North America segment accounted for 48.62% of share in 2025 in Global CAR-T Cell Therapy market.

Based on region, the global CAR T-cell therapy market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America held the largest revenue share of 48.63% in 2025 and is projected to grow at a CAGR of 38.52%, reaching USD 35,665.86 million. The region’s leadership is primarily attributed to its strong biotechnology ecosystem, presence of leading CAR T developers, and advanced healthcare infrastructure. The United States, in particular, dominates the market with FDA approvals, well-established clinical trial networks, and access to cutting-edge cell processing facilities. High cancer incidence rates, favorable reimbursement frameworks, and strong patient awareness have further accelerated adoption across hospitals and specialized cancer centers.

Additionally, North America benefits from significant R&D investments, collaborations between pharma companies and academic institutions, and government support for novel oncology therapies. The region is also witnessing rapid expansion of commercial manufacturing sites and streamlined regulatory pathways, which shorten therapy availability timelines. Robust insurance coverage and the growing integration of CAR T-cell therapies into clinical practice guidelines have reinforced patient access. While other regions such as Europe and Asia Pacific are advancing with supportive regulations and rising adoption, North America remains at the forefront due to its innovation-driven ecosystem, strong commercial presence, and comprehensive healthcare support, positioning it as the global leader in CAR T-cell therapy throughout the forecast period.

Global CAR-T Cell Therapy Market, By Region (USD Million)

Major Companies and Competitive Landscape

The global CAR T-cell therapy market is fragmented, with large and emerging players accounting for the majority of market revenue. Major companies are adopting strategies such as mergers and acquisitions, strategic collaborations, licensing agreements, and product pipeline expansions. These efforts are focused on enhancing therapeutic efficacy, improving safety, scaling manufacturing, and broadening clinical applications to meet growing patient demand. Some of the leading companies profiled in the global CAR T-cell therapy market report include:

-

- Bluebird Bio

- Celgene Corporation

- Gilead Sciences

- Cellectis

- Servier Laboratories

- Pfizer Inc.

- Merck

- Amgen

- Intellia Therapeutics

- Novartis

- Caribou Biosciences

- Celyad

- Bellicum Pharmaceuticals, Inc.

- Noile-Immune Biotech

- Nanjing Legend Biotechnology Co., Ltd.

- Johnson & Johnson

- Sangamo Therapeutics, Inc.

- Autolus Therapeutics

- Poseida Therapeutics

- Allogene Therapeutics

- BioNTech

- Cartesian Therapeutics

- Roche

- AstraZeneca

- HaemaLogiX

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 5,395.26 Million |

| CAGR (2024–2032) | 38.41% |

| Revenue forecast to 2033 | USD 72,597.71 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million, and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Product Type, By Target Antigen Type, By Disease/Indication Type, By Manufacturing Method, By Technology/Vector Type, By Therapy Type, By End User and By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, UAE, South Africa, Turkey, Rest of MEA |

| Key companies profiled | Bluebird Bio, Celgene Corporation, Gilead Sciences, Cellectis, Servier Laboratories, Pfizer Inc., Merck, Amgen, Intellia Therapeutics, Novartis, Caribou Biosciences, Celyad, Bellicum Pharmaceuticals, Inc., Noile-Immune Biotech, Nanjing Legend Biotechnology Co., Ltd., Johnson & Johnson, Sangamo Therapeutics, Inc., Autolus Therapeutics, Poseida Therapeutics, Allogene Therapeutics, BioNTech, Cartesian Therapeutics, Roche, AstraZeneca, HaemaLogiX. |

| Customization scope | 10 hours of free customization and expert consultation |

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of global CAR-T cell therapy market

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1.Primary

2.1.2.Secondary

2.1.3.Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1.Market value

2.3.2.Market volume

2.3.3.Exchange rate

2.3.4.Price

2.3.5.Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2025-2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10.Formulation & manufacturing

4.11.Distribution & retail

4.12.Import-export analysis4.13.Brand comparative analysis

4.14.Technological advancements

4.15.Porter’s five force

4.15.1.Threat of new entrants

4.15.1.1.Capital requirment

4.15.1.2.Product knowledge

4.15.1.3.Technical knowledge

4.15.1.4.Customer relation

4.15.1.5.Access to appliation and technology

4.15.2.Threat of substitutes

4.15.2.1.Cost

4.15.2.2.Performance

4.15.2.3.Availability

4.15.2.4.Technical knowledge

4.15.2.5.Durability

4.15.3.Bargainning power of buyers

4.15.3.1.Numbers of buyers relative to suppliers

4.15.3.2.Product differentiation

4.15.3.3.Threat of forward integration

4.15.3.4.Buyers volume

4.15.4.Bargainning power of suppliers

4.15.4.1.Suppliers concentration

4.15.4.2.Buyers switching cost to other suppliers

4.15.4.3.Threat of backward integration

4.15.5.Bargainning power of suppliers

4.15.5.1.Industry concentration

4.15.5.2.Industry growth rate

4.15.5.3.Product differentiation

4.15.6.Patent analysis

4.16.Patent quality and strength

4.17.Regulation coverage

4.18.Pricing analysis

4.19.Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1.Rising demand for advanced cancer treatments

5.1.2.Strong clinical outcomes and regulatory approvals

5.1.3.Growing investments and collaborations

5.2. Restraints

5.2.1.High cost of therapy

5.2.2.Complex manufacturing process

5.3. Opportunities

5.3.1.Expansion beyond blood cancers

5.3.2.Technological advancements in manufacturing

5.3.3.Rising demand in Asia-Pacific

5.4. Threat

5.4.1.Competition from alternative cancer therapies

5.4.2.Safety concerns and side effects

Chapter 6. Global CAR-T Cell Therapy Market By Product Type Insights & Trends, Revenue (USD Million)

6.1. Product Type Dynamics & Market Share, 2025-2032

6.1.1.Yescarta (Axicabtagene Ciloleucel)

6.1.2.Kymriah (Tisagenlecleucel)

6.1.3.Breyanzi (Lisocabtagene Maraleucel)

6.1.4.Abecma (Idecabtagene Vicleucel)

6.1.5.Carvykti (Ciltacabtagene Autoleucel / Cilta-cel)

6.1.6.Tecartus (Brexucabtagene Autoleucel)

Chapter 7. Global CAR-T Cell Therapy Market By Target Antigen Type Insights & Trends, Revenue (USD Million)

7.1. Target Antigen Dynamics & Market Share, 2025–2032

7.1.1.CD19 (Cluster of Differentiation 19)

7.1.2.BCMA (B-cell Maturation Antigen)

7.1.3.CD22 (Cluster of Differentiation 22)

7.1.4.GD2 (Disialoganglioside GD2)

7.1.5.HER2 (Human Epidermal Growth Factor Receptor 2)

7.1.6.GPC3 (Glypican-3)

7.1.7.Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

Chapter 8. Global CAR-T Cell Therapy Market By Disease/Indication Type Insights & Trends, Revenue (USD Million)

8.1. Disease/Indication Dynamics & Market Share, 2025–2032

8.1.1.Hematologic Malignancies (Blood Cancers)

8.1.1.1.Lymphoma

8.1.1.1.1.Diffuse Large B-cell Lymphoma (DLBCL)

8.1.1.1.2.Primary Mediastinal B-cell Lymphoma (PMBCL)

8.1.1.1.3.Mantle Cell Lymphoma (MCL)

8.1.1.1.4.Follicular Lymphoma (FL)

8.1.1.1.5.Other (Non-Hodgkin Lymphomas (NHLs))

8.1.1.2.Leukemia

8.1.1.2.1.Acute Lymphoblastic Leukemia (ALL)

8.1.1.2.2.Chronic Lymphocytic Leukemia (CLL)

8.1.1.3.Multiple Myeloma

8.1.1.3.1.B-cell Maturation Antigen (BCMA)

8.1.2.Solid Tumours

8.1.2.1.Glioblastoma

8.1.2.2.Pancreatic Cancer

8.1.2.3.Ovarian Cancer

8.1.2.4.Breast Cancer

8.1.2.5.Lung Cancer

8.1.2.6.Melanoma

8.1.2.7.Prostate Cancer

8.1.2.8.Others (Neuroblastoma Cancer, Colorectal Cancer)

8.1.3.Other Diseases

8.1.3.1.Autoimmune Diseases

8.1.3.2.Infectious Diseases

Chapter 9. Global CAR-T Cell Therapy Market By Manufacturing Method Type Insights & Trends, Revenue (USD Million)

9.1. Manufacturing Method Dynamics & Market Share, 2025–2032

9.1.1.Point-of-Care Manufacturing

9.1.2.Centralized manufacturing

9.1.3.In vivo CAR-T therapy manufacturing

9.1.4.Off-the-shelf / Ready-to-use therapies

Chapter 10. Global CAR-T Cell Therapy Market By Technology/Vector Type Insights & Trends, Revenue (USD Million)

10.1.Technology/Vector Dynamics & Market Share, 2025–2032

10.1.1.Viral Vectors

10.1.1.1.Lentiviral vectors

10.1.1.2.Retroviral vectors

10.1.2.Non- Viral Vectors

10.1.2.1.CRISPR/Cas9 gene editing

10.1.2.2.Transposons (Sleeping Beauty, PiggyBac)

10.1.2.3.mRNA electroporation

10.1.3.Armored CAR-T-Cells (enhanced T-cell persistence/activity)

10.1.4.Safety Switch-Equipped CAR-T Cells

10.1.5.Dual and multiple antigens targeting CAR-T-cell

Chapter 11. Global CAR-T Cell Therapy Market By Therapy Type Insights & Trends, Revenue (USD Million)

11.1.Therapy Dynamics & Market Share, 2025–2032

11.1.1.Autologous CAR-T cell therapy

11.1.2.Allogeneic CAR-T cell therapy

Chapter 12. Global CAR-T Cell Therapy Market By End User Insights & Trends, Revenue (USD Million)

12.1.End Use Dynamics & Market Share, 2025–2032

12.1.1.Hospitals

12.1.2.Cancer Treatment Centers

12.1.3.Contract Development and Manufacturing Organization

12.1.4.Academic & Research Institutes

12.1.5.Specialty Clinics

13. Global CAR-T Cell Therapy Market Regional Outlook

13.1. Global CAR-T Cell Therapy Market Share By Region, 2025–2032

13.2. North America

13.2.1. Market By ProductType, Market Estimates and Forecast, USD Million

13.2.2.Yescarta (Axicabtagene Ciloleucel)

13.2.3.Kymriah (Tisagenlecleucel)

13.2.4.Breyanzi (Lisocabtagene Maraleucel)

13.2.5.Abecma (Idecabtagene Vicleucel)

13.2.6.Carvykti (Ciltacabtagene Autoleucel / Cilta-cel)

13.2.7.Tecartus (Brexucabtagene Autoleucel)

13.3.Market By Target Antigen, Market Estimates and Forecast, USD Million

13.3.1.CD19 (Cluster of Differentiation 19)

13.3.2.BCMA (B-cell Maturation Antigen)

13.3.3.CD22 (Cluster of Differentiation 22)

13.3.4.GD2 (Disialoganglioside GD2)

13.3.5.HER2 (Human Epidermal Growth Factor Receptor 2)

13.3.6.GPC3 (Glypican-3)

13.3.7.Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

13.4.Market By Disease/Indication Type, Market Estimates and Forecast, USD Million

13.4.1.Hematologic Malignancies (Blood Cancers)

13.4.1.1.Lymphoma

13.4.1.1.1.Diffuse Large B-cell Lymphoma (DLBCL)

13.4.1.1.2.Primary Mediastinal B-cell Lymphoma (PMBCL)

13.4.1.1.3.Mantle Cell Lymphoma (MCL)

13.4.1.1.4.Follicular Lymphoma (FL)

13.4.1.1.5.Other (Non-Hodgkin Lymphomas (NHLs))

13.4.1.2.Leukemia

13.4.1.2.1.Acute Lymphoblastic Leukemia (ALL)

13.4.1.2.2.Chronic Lymphocytic Leukemia (CLL)

13.4.1.3.Multiple Myeloma

13.4.1.3.1.B-cell Maturation Antigen (BCMA)

13.4.2.Solid Tumours

13.4.2.1.Glioblastoma

13.4.2.2.Pancreatic Cancer

13.4.2.3.Ovarian Cancer

13.4.2.4.Breast Cancer

13.4.2.5.Lung Cancer

13.4.2.6.Melanoma

13.4.2.7.Prostate Cancer

13.4.2.8.Others (Neuroblastoma Cancer, Colorectal Cancer)

13.4.3.Other Diseases

13.4.3.1.Autoimmune Diseases

13.4.3.2.Infectious Diseases

13.5.Market By Manufacturing Method, Market Estimates and Forecast, USD Million

13.5.1.Point-of-Care Manufacturing

13.5.2.Centralized manufacturing

13.5.3.In vivo CAR-T therapy manufacturing

13.5.4.Off-the-shelf / Ready-to-use therapies

13.6.Market By Technology/Vector, Market Estimates and Forecast, USD Million

13.6.1.Viral Vectors

13.6.1.1.Lentiviral vectors

13.6.1.2.Retroviral vectors

13.6.2.Non- Viral Vectors

13.6.2.1.CRISPR/Cas9 gene editing

13.6.2.2.Transposons (Sleeping Beauty, PiggyBac)

13.6.2.3.mRNA electroporation

13.6.3.Armored CAR-T-Cells (enhanced T-cell persistence/activity)

13.6.4.Safety Switch-Equipped CAR-T Cells

13.6.5.Dual and multiple antigens targeting CAR-T-cell

13.7.Market By Therapy Type, Market Estimates and Forecast, USD Million

13.7.1.Autologous CAR-T cell therapy

13.7.2.Allogeneic CAR-T cell therapy

13.8.Market By End User, Market Estimates and Forecast, USD Million

13.8.1.Hospitals

13.8.2.Cancer Treatment Centers

13.8.3.Contract Development and Manufacturing Organization

13.8.4.Academic & Research Institutes

13.8.5.Specialty Clinics

13.9.Market By Country, Market Estimates and Forecast, USD Million

13.9.1.US

13.9.2.Canada

13.9.3.Mexico

13.10. Europe

13.11.Market By ProductType, Market Estimates and Forecast, USD Million

13.11.1.Yescarta (Axicabtagene Ciloleucel)

13.11.2.Kymriah (Tisagenlecleucel)

13.11.3.Breyanzi (Lisocabtagene Maraleucel)

13.11.4.Abecma (Idecabtagene Vicleucel)

13.11.5.Carvykti (Ciltacabtagene Autoleucel / Cilta-cel)

13.11.6.Tecartus (Brexucabtagene Autoleucel)

13.12.Market By Target Antigen, Market Estimates and Forecast, USD Million

13.12.1.CD19 (Cluster of Differentiation 19)

13.12.2.BCMA (B-cell Maturation Antigen)

13.12.3.CD22 (Cluster of Differentiation 22)

13.12.4.GD2 (Disialoganglioside GD2)

13.12.5.HER2 (Human Epidermal Growth Factor Receptor 2)

13.12.6.GPC3 (Glypican-3)

13.12.7.Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

13.13.Market By Target Antigen, Market Estimates and Forecast, USD Million,

13.13.1.CD19 (Cluster of Differentiation 19)

13.13.2.BCMA (B-cell Maturation Antigen)

13.13.3.CD22 (Cluster of Differentiation 22)

13.13.4.GD2 (Disialoganglioside GD2)

13.13.5.HER2 (Human Epidermal Growth Factor Receptor 2)

13.13.6.GPC3 (Glypican-3)

13.13.7.Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

13.14.Market By Disease/Indication Type, Market Estimates and Forecast, USD Million

13.14.1.Hematologic Malignancies (Blood Cancers)

13.14.1.1.Lymphoma

13.14.1.1.1.Diffuse Large B-cell Lymphoma (DLBCL)

13.14.1.1.2.Primary Mediastinal B-cell Lymphoma (PMBCL)

13.14.1.1.3.Mantle Cell Lymphoma (MCL)

13.14.1.1.4.Follicular Lymphoma (FL)

13.14.1.1.5.Other (Non-Hodgkin Lymphomas (NHLs))

13.14.1.2.Leukemia

13.14.1.2.1.Acute Lymphoblastic Leukemia (ALL)

13.14.1.2.2.Chronic Lymphocytic Leukemia (CLL)

13.14.1.3.Multiple Myeloma

13.14.1.3.1.B-cell Maturation Antigen (BCMA)

13.14.2.Solid Tumours

13.14.2.1.Glioblastoma

13.14.2.2.Pancreatic Cancer

13.14.2.3.Ovarian Cancer

13.14.2.4.Breast Cancer

13.14.2.5.Lung Cancer

13.14.2.6.Melanoma

13.14.2.7.Prostate Cancer

13.14.2.8.Others (Neuroblastoma Cancer, Colorectal Cancer)

13.14.3.Other Diseases

13.14.3.1.Autoimmune Diseases

13.14.3.2.Infectious Diseases

13.15.Market By Manufacturing Method, Market Estimates and Forecast, USD Million,

13.15.1.Point-of-Care Manufacturing

13.15.2.Centralized manufacturing

13.15.3.In vivo CAR-T therapy manufacturing

13.15.4.Off-the-shelf / Ready-to-use therapies

13.16.Market By Technology/Vector Type, Market Estimates and Forecast, USD Million

13.16.1. Viral Vectors

13.16.1.1.Lentiviral vectors

13.16.1.2.Retroviral vectors

13.16.2.Non- Viral Vectors

13.16.2.1.CRISPR/Cas9 gene editing

13.16.2.2.Transposons (Sleeping Beauty, PiggyBac)

13.16.2.3.mRNA electroporation

13.16.3.Armored CAR-T-Cells (enhanced T-cell persistence/activity)

13.16.4.Safety Switch-Equipped CAR-T Cells

13.16.5.Dual and multiple antigens targeting CAR-T-cell

13.17.Market By Therapy Type, Market Estimates and Forecast, USD Million

13.17.1.Autologous CAR-T cell therapy

13.17.2.Allogeneic CAR-T cell therapy

13.18.Market By End User, Market Estimates and Forecast, USD Million

13.18.1.Hospitals

13.18.2.Cancer Treatment Centers

13.18.3.Contract Development and Manufacturing Organization

13.18.4.Academic & Research Institutes

13.18.5.Specialty Clinics

13.19.Market By Country, Market Estimates and Forecast, USD Million

13.19.1.Germany

13.19.2.France

13.19.3.U.K

13.19.4.Italy

13.19.5.Spain

13.19.6.Turkey

13.19.7.Benelux

13.19.8.Russia

13.19.9.Finland

13.19.10.Sweden

13.19.11.Rest Of Europe

13.20. Asia-Pacific

13.20.1. Market By ProductType, Market Estimates and Forecast, USD Million

13.20.2.Yescarta (Axicabtagene Ciloleucel)

13.20.3.Kymriah (Tisagenlecleucel)

13.20.4.Breyanzi (Lisocabtagene Maraleucel)

13.20.5.Abecma (Idecabtagene Vicleucel)

13.20.6.Carvykti (Ciltacabtagene Autoleucel / Cilta-cel)

13.20.7.Tecartus (Brexucabtagene Autoleucel)

13.21.Market By Target Antigen, Market Estimates and Forecast, USD Million

13.21.1.CD19 (Cluster of Differentiation 19)

13.21.2.BCMA (B-cell Maturation Antigen)

13.21.3.CD22 (Cluster of Differentiation 22)

13.21.4.GD2 (Disialoganglioside GD2)

13.21.5.HER2 (Human Epidermal Growth Factor Receptor 2)

13.21.6.GPC3 (Glypican-3)

13.21.7.Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

13.22.Market By Disease/Indiaction Type, Market Estimates and Forecast, USD Million,

13.22.1.Hematologic Malignancies (Blood Cancers)

13.22.1.1.Lymphoma

13.22.1.1.1.Diffuse Large B-cell Lymphoma (DLBCL)

13.22.1.1.2.Primary Mediastinal B-cell Lymphoma (PMBCL)

13.22.1.1.3.Mantle Cell Lymphoma (MCL)

13.22.1.1.4.Follicular Lymphoma (FL)

13.22.1.1.5.Other (Non-Hodgkin Lymphomas (NHLs))

13.22.1.2.Leukemia

13.22.1.2.1.Acute Lymphoblastic Leukemia (ALL)

13.22.1.2.2.Chronic Lymphocytic Leukemia (CLL)

13.22.1.3.Multiple Myeloma

13.22.1.3.1.B-cell Maturation Antigen (BCMA)

13.22.2.Solid Tumours

13.22.2.1.Glioblastoma

13.22.2.2.Pancreatic Cancer

13.22.2.3.Ovarian Cancer

13.22.2.4.Breast Cancer

13.22.2.5.Lung Cancer

13.22.2.6.Melanoma

13.22.2.7.Prostate Cancer

13.22.2.8.Others (Neuroblastoma Cancer, Colorectal Cancer)

13.22.3.Other Diseases

13.22.3.1.Autoimmune Diseases

13.22.3.2.Infectious Diseases

13.23.Market By Manufacturing method, Market Estimates and Forecast, USD Million

13.23.1.Point-of-Care Manufacturing

13.23.2.Centralized manufacturing

13.23.3.In vivo CAR-T therapy manufacturing

13.23.4.Off-the-shelf / Ready-to-use therapies

13.24.Market By Technology/Vector, Market Estimates and Forecast, USD Million

13.24.1.Viral Vectors

13.24.1.1.Lentiviral vectors

13.24.1.2.Retroviral vectors

13.24.2.Non- Viral Vectors

13.24.2.1.CRISPR/Cas9 gene editing

13.24.2.2.Transposons (Sleeping Beauty, PiggyBac)

13.24.2.3.mRNA electroporation

13.24.3.Armored CAR-T-Cells (enhanced T-cell persistence/activity)

13.24.4.Safety Switch-Equipped CAR-T Cells

13.24.5.Dual and multiple antigens targeting CAR-T-cell

13.25.Market By Therapy Type, Market Estimates and Forecast, USD Million

13.25.1.Autologous CAR-T cell therapy

13.25.2.Allogeneic CAR-T cell therapy

13.26.Market By End User, Market Estimates and Forecast, USD Million

13.26.1.Hospitals

13.26.2.Cancer Treatment Centers

13.26.3.Contract Development and Manufacturing Organization

13.26.4.Academic & Research Institutes

13.26.5.Specialty Clinics

13.27.Market By Country, Market Estimates and Forecast, USD Million

13.27.1.1.China

13.27.1.2.India

13.27.1.3.Japan

13.27.1.4.South Korea

13.27.1.5.Indonesia

13.27.1.6.Thailand

13.27.1.7.Vietnam

13.27.1.8.Australia

13.27.1.9.New Zeland

13.27.1.10.Rest of APAC

Chapter 14. Latin America

14.1.1. Market By Product Type, Market Estimates and Forecast, USD Million

14.1.2.Yescarta (Axicabtagene Ciloleucel)

14.1.3.Kymriah (Tisagenlecleucel)

14.1.4.Breyanzi (Lisocabtagene Maraleucel)

14.1.5.Abecma (Idecabtagene Vicleucel)

14.1.6.Carvykti (Ciltacabtagene Autoleucel / Cilta-cel)

14.1.7.Tecartus (Brexucabtagene Autoleucel)

14.2.Market By Target Antigen, Market Estimates and Forecast, USD Million

14.2.1.CD19 (Cluster of Differentiation 19)

14.2.2.BCMA (B-cell Maturation Antigen)

14.2.3.CD22 (Cluster of Differentiation 22)

14.2.4.GD2 (Disialoganglioside GD2)

14.2.5.HER2 (Human Epidermal Growth Factor Receptor 2)

14.2.6.GPC3 (Glypican-3)

14.2.7.Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

14.3.Market By Disease/Indication Type, Market Estimates and Forecast, USD Million

14.4. Disease/Indication Dynamics & Market Share, 2025–2032

14.4.1.Hematologic Malignancies (Blood Cancers)

14.4.1.1.Lymphoma

14.4.1.1.1.Diffuse Large B-cell Lymphoma (DLBCL)

14.4.1.1.2.Primary Mediastinal B-cell Lymphoma (PMBCL)

14.4.1.1.3.Mantle Cell Lymphoma (MCL)

14.4.1.1.4.Follicular Lymphoma (FL)

14.4.1.1.5.Other (Non-Hodgkin Lymphomas (NHLs))

14.4.1.2.Leukemia

14.4.1.2.1.Acute Lymphoblastic Leukemia (ALL)

14.4.1.2.2.Chronic Lymphocytic Leukemia (CLL)

14.4.1.3.Multiple Myeloma

14.4.1.3.1.B-cell Maturation Antigen (BCMA)

14.4.2.Solid Tumours

14.4.2.1.Glioblastoma

14.4.2.2.Pancreatic Cancer

14.4.2.3.Ovarian Cancer

14.4.2.4.Breast Cancer

14.4.2.5.Lung Cancer

14.4.2.6.Melanoma

14.4.2.7.Prostate Cancer

14.4.2.8.Others (Neuroblastoma Cancer, Colorectal Cancer)

14.4.3.Other Diseases

14.4.3.1.Autoimmune Diseases

14.4.3.2.Infectious Diseases

14.5.Market By Manufacturing method, Market Estimates and Forecast, USD Million

14.5.1.Point-of-Care Manufacturing

14.5.2.Centralized manufacturing

14.5.3.In vivo CAR-T therapy manufacturing

14.5.4.Off-the-shelf / Ready-to-use therapies

14.6.Market By Technology/Vector, Market Estimates and Forecast, USD Million

14.6.1.Viral Vectors

14.6.1.1.Lentiviral vectors

14.6.1.2.Retroviral vectors

14.6.2.Non- Viral Vectors

14.6.2.1.CRISPR/Cas9 gene editing

14.6.2.2.Transposons (Sleeping Beauty, PiggyBac)

14.6.2.3.mRNA electroporation

14.6.3.Armored CAR-T-Cells (enhanced T-cell persistence/activity)

14.6.4.Safety Switch-Equipped CAR-T Cells

14.6.5.Dual and multiple antigens targeting CAR-T-cell

14.7.Market By End User, Market Estimates and Forecast, USD Million

14.7.1. Hospitals

14.7.2.Cancer Treatment Centers

14.7.3.Contract Development and Manufacturing Organization

14.7.4.Academic & Research Institutes

14.7.5.Specialty Clinics

14.8.Market By Therapy Type, Market Estimates and Forecast, USD Million

14.8.1.Autologous CAR-T cell therapy

14.8.2.Allogeneic CAR-T cell therapy

14.9.Market By Country, Market Estimates and Forecast, USD Million

14.9.1.Brazil

14.9.2.Rest of LATAM

14.10.Middle East & Africa

14.10.1. Market By ProductType, Market Estimates and Forecast, USD Million

14.10.2.Yescarta (Axicabtagene Ciloleucel)

14.10.3.Kymriah (Tisagenlecleucel)

14.10.4.Breyanzi (Lisocabtagene Maraleucel)

14.10.5.Abecma (Idecabtagene Vicleucel)

14.10.6.Carvykti (Ciltacabtagene Autoleucel / Cilta-cel)

14.10.7.Tecartus (Brexucabtagene Autoleucel)

14.11.Market By Target Antigen, Market Estimates and Forecast, USD Million

14.11.1.CD19 (Cluster of Differentiation 19)

14.11.2.BCMA (B-cell Maturation Antigen)

14.11.3.CD22 (Cluster of Differentiation 22)

14.11.4.GD2 (Disialoganglioside GD2)

14.11.5.HER2 (Human Epidermal Growth Factor Receptor 2)

14.11.6.GPC3 (Glypican-3)

14.11.7.Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

14.12.Market By Disease/Indication, Market Estimates and Forecast, USD Million

14.12.1.Hematologic Malignancies (Blood Cancers)

14.12.1.1.Lymphoma

14.12.1.1.1.Diffuse Large B-cell Lymphoma (DLBCL)

14.12.1.1.2.Primary Mediastinal B-cell Lymphoma (PMBCL)

14.12.1.1.3.Mantle Cell Lymphoma (MCL)

14.12.1.1.4.Follicular Lymphoma (FL)

14.12.1.1.5.Other (Non-Hodgkin Lymphomas (NHLs))

14.12.1.2.Leukemia

14.12.1.2.1.Acute Lymphoblastic Leukemia (ALL)

14.12.1.2.2.Chronic Lymphocytic Leukemia (CLL)

14.12.1.3.Multiple Myeloma

14.12.1.3.1.B-cell Maturation Antigen (BCMA)

14.12.2.Solid Tumours

14.12.2.1.Glioblastoma

14.12.2.2.Pancreatic Cancer

14.12.2.3.Ovarian Cancer

14.12.2.4.Breast Cancer

14.12.2.5.Lung Cancer

14.12.2.6.Melanoma

14.12.2.7.Prostate Cancer

14.12.2.8.Others (Neuroblastoma Cancer, Colorectal Cancer)

14.12.3.Other Diseases

14.12.3.1.Autoimmune Diseases

14.12.3.2.Infectious Diseases

14.13.Market By Manufacturing method, Market Estimates and Forecast, USD Million

14.13.1.Point-of-Care Manufacturing

14.13.2.Centralized manufacturing

14.13.3.In vivo CAR-T therapy manufacturing

14.13.4.Off-the-shelf / Ready-to-use therapies

14.14.Market By Technology/Vector, Market Estimates and Forecast, USD Million

14.14.1.Viral Vectors

14.14.1.1.Lentiviral vectors

14.14.1.2.Retroviral vectors

14.14.2.Non- Viral Vectors

14.14.2.1.CRISPR/Cas9 gene editing

14.14.2.2.Transposons (Sleeping Beauty, PiggyBac)

14.14.2.3.mRNA electroporation

14.14.3.Armored CAR-T-Cells (enhanced T-cell persistence/activity)

14.14.4.Safety Switch-Equipped CAR-T Cells

14.14.5.Dual and multiple antigens targeting CAR-T-cell

14.15.Market By Therapy Type, Market Estimates and Forecast, USD Million

14.15.1.Autologous CAR-T cell therapy

14.15.2.Allogeneic CAR-T cell therapy

14.16.Market By End User, Market Estimates and Forecast, USD Million

14.16.1.Hospitals

14.16.2.Cancer Treatment Centers

14.16.3.Contract Development and Manufacturing Organization

14.16.4.Academic & Research Institutes

14.16.5.Specialty Clinics

14.17.Market By Country, Market Estimates and Forecast, USD Million

14.17.1.Saudi Arabia

14.17.2.UAE

14.17.3.South Africa

14.17.4.Turkey

14.17.5.Rest of MEA

Chapter 15. Competitive Landscape

15.1. Market Revenue Share By Manufacturers

15.2. Mergers & Acquisitions

15.3. Competitor’s Positioning

15.4. Strategy Benchmarking

15.5. Vendor Landscape

15.5.1.Distributors

15.5.1.1.North America

15.5.1.2.Europe

15.5.1.3.Asia Pacific

15.5.1.4.Middle East & Africa

15.5.1.5.Latin America

15.5.2.Others

Chapter 16. Company Profiles

16.1.Bluebird Bio

16.1.1.Company Overview

16.1.2.Product & Service Offerings

16.1.3.Strategic Initiatives

16.1.4.Financials

16.1.5.Research Insights

16.2.Celgene Corporation

16.2.1.Company Overview

16.2.2.Product & Service Offerings

16.2.3.Strategic Initiatives

16.2.4.Financials

16.2.5.Research Insights

16.3.Gilead Sciences

16.3.1.Company Overview

16.3.2.Product & Service Offerings

16.3.3.Strategic Initiatives

16.3.4.Financials

16.3.5.Research Insights

16.4.Cellectis

16.4.1.Company Overview

16.4.2.Product & Service Offerings

16.4.3.Strategic Initiatives

16.4.4.Financials

16.4.5.Research Insights

16.5.Servier Laboratories

16.5.1.Company Overview

16.5.2.Product & Service Offerings

16.5.3.Strategic Initiatives

16.5.4.Financials

16.5.5.Research Insights

16.6.Pfizer Inc.

16.6.1.Company Overview

16.6.2.Product & Service Offerings

16.6.3.Strategic Initiatives

16.6.4.Financials

16.6.5.Research Insights

16.7.Merck

16.7.1.Company Overview

16.7.2.Product & Service Offerings

16.7.3.Strategic Initiatives

16.7.4.Financials

16.7.5.Conclusion

16.8.Amgen

16.8.1.Company Overview

16.8.2.Product & Service Offerings

16.8.3.Strategic Initiatives

16.8.4.Financials

16.8.5.Conclusion

16.9.Intellia Therapeutics

16.9.1.Company Overview

16.9.2.Product & Service Offerings

16.9.3.Strategic Initiatives

16.9.4.Financials

16.9.5.Conclusion

16.10.Novartis

16.10.1.Company Overview

16.10.2.Product & Service Offerings

16.10.3.Strategic Initiatives

16.10.4.Financials

16.10.5.Conclusion

16.11.Caribou Biosciences

16.11.1.Company Overview

16.11.2.Product & Service Offerings

16.11.3.Strategic Initiatives

16.11.4.Financials

16.11.5.Conclusion

16.12.Celyad

16.12.1.Company Overview

16.12.2.Product & Service Offerings

16.12.3.Strategic Initiatives

16.12.4.Financials

16.12.5.Conclusion

16.13.Bellicum Pharmaceuticals, Inc.

16.13.1.Company Overview

16.13.2.Product & Service Offerings

16.13.3.Strategic Initiatives

16.13.4.Financials

16.13.5.Conclusion

16.14.Noile-Immune Biotech

16.14.1.Company Overview

16.14.2.Product & Service Offerings

16.14.3.Strategic Initiatives

16.14.4.Financials

16.14.5.Conclusion

16.15.Nanjing Legend Biotechnology Co., Ltd.

16.15.1.Company Overview

16.15.2.Product & Service Offerings

16.15.3.Strategic Initiatives

16.15.4.Financials

16.15.5.Conclusion

16.16.Johnson & Johnson

16.16.1.Company Overview

16.16.2.Product & Service Offerings

16.16.3.Strategic Initiatives

16.16.4.Financials

16.16.5.Conclusion

16.17.Sangamo Therapeutics, Inc.

16.17.1.Company Overview

16.17.2.Product & Service Offerings

16.17.3.Strategic Initiatives

16.17.4.Financials

16.17.5.Conclusion

16.18.Autolus Therapeutics

16.18.1.Company Overview

16.18.2.Product & Service Offerings

16.18.3.Strategic Initiatives

16.18.4.Financials

16.18.5.Conclusion

16.19.Poseida Therapeutics

16.19.1.Company Overview

16.19.2.Product & Service Offerings

16.19.3.Strategic Initiatives

16.19.4.Financials

16.19.5.Conclusion

16.20.Allogene Therapeutics

16.20.1.Company Overview

16.20.2.Product & Service Offerings

16.20.3.Strategic Initiatives

16.20.4.Financials

16.20.5.Conclusion

16.21.Arcellx.

16.21.1.Company Overview

16.21.2.Product & Service Offerings

16.21.3.Strategic Initiatives

16.21.4.Financials

16.21.5.Conclusion

16.22.JW Therapeutics

16.22.1.Company Overview

16.22.2.Product & Service Offerings

16.22.3.Strategic Initiatives

16.22.4.Financials

16.22.5.Conclusion

16.23.Gracell Biotechnologies

16.23.1.Company Overview

16.23.2.Product & Service Offerings

16.23.3.Strategic Initiatives

16.23.4.Financials

16.23.5.Conclusion

16.24.Mustang Bio.

16.24.1.Company Overview

16.24.2.Product & Service Offerings

16.24.3.Strategic Initiatives

16.24.4.Financials

16.24.5.Conclusion

16.25.Cellular Biomedicine Group

16.25.1.Company Overview

16.25.2.Product & Service Offerings

16.25.3.Strategic Initiatives

16.25.4.Financials

16.25.5.Conclusion

Segments covered in report

For the purpose of this report, Advantia Business Consulting LLP. has segmented global CAR-T cell therapy market on the basis of Product Type, By Target Antigen Type, By Disease/Indication Type, By Manufacturing Method, By Technology/Vector Type, By Therapy Type, By End User and By Region.

- Global Type Product Outlook (Revenue, USD Million; 2025-2032)

-

- Yescarta (Axicabtagene Ciloleucel)

-

- Kymriah (Tisagenlecleucel)

-

- Breyanzi (Lisocabtagene Maraleucel)

-

- Abecma (Idecabtagene Vicleucel)

-

- Carvykti (Ciltacabtagene Autoleucel / Cilta-cel)

-

- Tecartus (Brexucabtagene Autoleucel)

- Global Type Target Antigen Outlook (Revenue, USD Million; 2025-2032)

-

- CD19 (Cluster of Differentiation 19)

-

- BCMA (B-cell Maturation Antigen)

-

- CD22 (Cluster of Differentiation 22)

-

- GD2 (Disialoganglioside GD2)

-

- HER2 (Human Epidermal Growth Factor Receptor 2)

-

- GPC3 (Glypican-3)

-

- Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

- Global Type Disease/Indication Outlook (Revenue, USD Million; 2025-2032)

-

- Hematologic Malignancies (Blood Cancers)

-

-

- Lymphoma

-

-

-

-

- Diffuse Large B-cell Lymphoma (DLBCL)

-

-

-

-

-

- Primary Mediastinal B-cell Lymphoma (PMBCL)

-

-

-

-

-

- Mantle Cell Lymphoma (MCL)

-

-

-

-

-

- Follicular Lymphoma (FL)

-

-

-

-

-

- Other (Non-Hodgkin Lymphomas (NHLs)

-

-

-

-

- Leukemia

-

-

-

-

- Acute Lymphoblastic Leukemia (ALL)

-

-

-

-

-

- Chronic Lymphocytic Leukemia (CLL)

-

-

-

-

- Multiple Myeloma

-

-

-

-

- B-cell Maturation Antigen (BCMA)

-

-

- Solid Tumours

-

- Glioblastoma

-

- Pancreatic Cancer

-

- Ovarian Cancer

-

- Breast Cancer

-

- Lung Cancer

-

- Melanoma

-

- Prostate Cancer

-

- Others (Neuroblastoma Cancer, Colorectal Cancer)

- Other Diseases

-

- Autoimmune Diseases

-

- Infectious Diseases

- Global Type Manufacturing Method Outlook (Revenue, USD Million; 2025-2032)

-

- Point-of-Care Manufacturing

-

- Centralized manufacturing

-

- In-vivo CAR T therapy manufacturing

-

- Off-the-shelf / Ready-to-use therapies

- Global Type Technology/Vector Outlook (Revenue, USD Million; 2025-2032)

-

- Viral Vectors

-

-

-

- Lentiviral vectors)

-

-

-

-

-

- Retroviral vectors

-

-

-

- Non- Viral Vectors

-

-

-

- CRISPR/Cas9 gene editing

-

-

-

-

-

- Transposons (Sleeping Beauty, PiggyBac)

-

-

-

-

-

- mRNA electroporation

-

-

-

- Armored CAR T-Cells (enhanced T-cell persistence/activity)

-

- Safety Switch-Equipped CAR T Cells

-

- Dual and multiple antigens targeting CAR T-cell

- Global Type Therapy Outlook (Revenue, USD Million; 2025-2032)

-

- Autologous CAR-T cell therapy

-

- Allogeneic CAR-T cell therapy

- Global Type End User Outlook (Revenue, USD Million; 2025-2032)

-

- Hospitals

-

- Cancer Treatment Centers

-

- Other (Academic & Research Institutes, Speciality Clinics)

- North America

- Dual and multiple antigens targeting CAR T-cell

-

- Yescarta (Axicabtagene Ciloleucel)

-

- Kymriah (Tisagenlecleucel)

-

- Breyanzi (Lisocabtagene Maraleucel)

-

- Abecma (Idecabtagene Vicleucel)

-

- Carvykti (Ciltacabtagene Autoleucel / Cilta-cel)

-

- Tecartus (Brexucabtagene Autoleucel)

- North America Type Target Antigen Outlook (Revenue, USD Million; 2025-2032)

-

- CD19 (Cluster of Differentiation 19)

-

- BCMA (B-cell Maturation Antigen)

-

- CD22 (Cluster of Differentiation 22)

-

- GD2 (Disialoganglioside GD2)

-

- HER2 (Human Epidermal Growth Factor Receptor 2)

-

- GPC3 (Glypican-3)

-

- Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

- North America Type Disease/Indication Outlook (Revenue, USD Million; 2025-2032)

-

- Hematologic Malignancies (Blood Cancers)

-

-

- Lymphoma

- Diffuse Large B-cell Lymphoma (DLBCL)

- Lymphoma

-

-

-

-

- Primary Mediastinal B-cell Lymphoma (PMBCL)

-

-

-

-

-

- Mantle Cell Lymphoma (MCL)

-

-

-

-

-

- Follicular Lymphoma (FL)

-

-

-

-

-

- Other (Non-Hodgkin Lymphomas (NHLs)

-

-

-

-

- Leukemia

-

-

-

-

- Acute Lymphoblastic Leukemia (ALL)

-

-

-

-

-

- Chronic Lymphocytic Leukemia (CLL)

-

-

-

-

- Multiple Myeloma

-

-

-

-

- B-cell Maturation Antigen (BCMA)

-

-

- Solid Tumours

-

- Yescarta (Axicabtagene Ciloleucel)

-

- Kymriah (Tisagenlecleucel)

-

- Breyanzi (Lisocabtagene Maraleucel)

-

- Abecma (Idecabtagene Vicleuce

- Other Diseases

-

- Autoimmune Diseases

-

- Infectious Diseases

- North America Type Manufacturing Method Outlook (Revenue, USD Million; 2025-2032)

-

- Point-of-Care Manufacturing

-

- Centralized manufacturing

-

- In-vivo CAR T therapy manufacturing

-

- Off-the-shelf / Ready-to-use therapies

- North America Type Technology/Vector Outlook (Revenue, USD Million; 2025-2032)

-

- Viral Vectors

-

-

-

- Lentiviral vectors)

-

-

-

-

-

- Retroviral vectors

-

-

-

- Non- Viral Vectors

-

-

-

- CRISPR/Cas9 gene editing

-

-

-

-

-

- Transposons (Sleeping Beauty, PiggyBac)

-

-

-

-

-

- mRNA electroporation

-

-

-

- Armored CAR T-Cells (enhanced T-cell persistence/activity)

-

- Safety Switch-Equipped CAR T Cells

-

- Dual and multiple antigens targeting CAR T-cell

- North America Type Therapy Outlook (Revenue, USD Million; 2025-2032)

-

- Autologous CAR-T cell therapy

-

- Allogeneic CAR-T cell therapy

- North America Type End User Outlook (Revenue, USD Million; 2025-2032)

-

- Hospitals

-

- Cancer Treatment Centers

-

- Other (Academic & Research Institutes, Speciality Clinics)

- U.S.

- U.S. Type Product Outlook (Revenue, USD Million; 2025-2032)

-

- Yescarta (Axicabtagene Ciloleucel)

-

- Kymriah (Tisagenlecleucel)

-

- Breyanzi (Lisocabtagene Maraleucel)

-

- Abecma (Idecabtagene Vicleucel)

-

- Carvykti (Ciltacabtagene Autoleucel / Cilta-cel)

-

- Tecartus (Brexucabtagene Autoleucel)

- U.S. Type Target Antigen Outlook (Revenue, USD Million; 2025-2032)

-

- CD19 (Cluster of Differentiation 19)

-

- BCMA (B-cell Maturation Antigen)

-

- CD22 (Cluster of Differentiation 22)

-

- GD2 (Disialoganglioside GD2)

-

- HER2 (Human Epidermal Growth Factor Receptor 2)

-

- GPC3 (Glypican-3)

-

- Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

- U.S. Type Disease/Indication Outlook (Revenue, USD Million; 2025-2032)

-

- Hematologic Malignancies (Blood Cancers)

-

-

- Lymphoma

-

-

-

-

- Diffuse Large B-cell Lymphoma (DLBCL)

-

-

-

-

-

- Primary Mediastinal B-cell Lymphoma (PMBCL)

-

-

-

-

-

- Mantle Cell Lymphoma (MCL)

-

-

-

-

-

- Follicular Lymphoma (FL)

-

-

-

-

-

- Other (Non-Hodgkin Lymphomas (NHLs)

-

-

-

-

- Leukemia

-

-

-

-

- Acute Lymphoblastic Leukemia (ALL)

-

-

-

-

-

- Chronic Lymphocytic Leukemia (CLL)

-

-

-

-

- Multiple Myeloma

-

-

-

-

- B-cell Maturation Antigen (BCMA)

-

-

- Solid Tumours

-

- Glioblastoma

-

- Pancreatic Cancer

-

- Ovarian Cancer

-

- Breast Cancer

-

- Lung Cancer

-

- Melanoma

-

- Prostate Cancer

-

- Others (Neuroblastoma Cancer, Colorectal Cancer)

- Other Diseases

-

- Autoimmune Diseases

-

- Infectious Diseases

- U.S. Type Manufacturing Method Outlook (Revenue, USD Million; 2025-2032)

-

- Point-of-Care Manufacturing

-

- Centralized manufacturing

-

- In-vivo CAR T therapy manufacturing

-

- Off-the-shelf / Ready-to-use therapies

- U.S. Type Technology/Vector Outlook (Revenue, USD Million; 2025-2032)

-

- Viral Vectors

-

-

-

- Lentiviral vectors)

-

-

-

-

-

- Retroviral vectors

-

-

-

- Non- Viral Vectors

-

-

-

- CRISPR/Cas9 gene editing

-

-

-

-

-

- Transposons (Sleeping Beauty, PiggyBac)

-

-

-

-

-

- mRNA electroporation

-

-

-

- Armored CAR T-Cells (enhanced T-cell persistence/activity)

-

- Safety Switch-Equipped CAR T Cells

-

- Dual and multiple antigens targeting CAR T-cell

- U.S. Type Therapy Outlook (Revenue, USD Million; 2025-2032)

-

- Autologous CAR-T cell therapy

-

- Allogeneic CAR-T cell therapy

- U.S. Type End User Outlook (Revenue, USD Million; 2025-2032)

-

- Hospitals

-

- Cancer Treatment Centers

-

- Other (Academic & Research Institutes, Speciality Clinics)

- Canada

- Canada Type Product Outlook (Revenue, USD Million; 2025-2032)

-

- Yescarta (Axicabtagene Ciloleucel)

-

- Kymriah (Tisagenlecleucel)

-

- Breyanzi (Lisocabtagene Maraleucel)

-

- Abecma (Idecabtagene Vicleucel)

-

- Carvykti (Ciltacabtagene Autoleucel / Cilta-cel)

-

- Tecartus (Brexucabtagene Autoleucel)

- Canada Type Target Antigen Outlook (Revenue, USD Million; 2025-2032)

-

- CD19 (Cluster of Differentiation 19)

-

- BCMA (B-cell Maturation Antigen)

-

- CD22 (Cluster of Differentiation 22)

-

- GD2 (Disialoganglioside GD2)

-

- HER2 (Human Epidermal Growth Factor Receptor 2)

-

- GPC3 (Glypican-3)

-

- Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

- Canada Type Disease/Indication Outlook (Revenue, USD Million; 2025-2032)

-

- Hematologic Malignancies (Blood Cancers)

-

-

- Lymphoma

-

-

-

-

- Diffuse Large B-cell Lymphoma (DLBCL)

-

-

-

-

-

- Primary Mediastinal B-cell Lymphoma (PMBCL)

-

-

-

-

-

- Mantle Cell Lymphoma (MCL)

-

-

-

-

-

- Follicular Lymphoma (FL)

-

-

-

-

-

- Other (Non-Hodgkin Lymphomas (NHLs)

-

-

-

-

- Leukemia

-

-

-

-

- Acute Lymphoblastic Leukemia (ALL)

-

-

-

-

-

- Chronic Lymphocytic Leukemia (CLL)

-

-

-

-

- Multiple Myeloma

-

-

-

-

- B-cell Maturation Antigen (BCMA)

-

-

- Solid Tumours

-

- Glioblastoma

-

- Pancreatic Cancer

-

- Ovarian Cancer

-

- Breast Cancer

-

- Lung Cancer

-

- Melanoma

-

- Prostate Cancer

-

- Others (Neuroblastoma Cancer, Colorectal Cancer)

- Other Diseases

-

- Autoimmune Diseases

-

- Infectious Diseases

- Canada Type Manufacturing Method Outlook (Revenue, USD Million; 2025-2032)

-

- Point-of-Care Manufacturing

-

- Centralized manufacturing

-

- In-vivo CAR T therapy manufacturing

-

- Off-the-shelf / Ready-to-use therapies

- Canada Type Technology/Vector Outlook (Revenue, USD Million; 2025-2032)

-

- Viral Vectors

-

-

-

- Lentiviral vectors)

-

-

-

-

-

- Retroviral vectors

-

-

-

- Non- Viral Vectors

-

-

-

- CRISPR/Cas9 gene editing

-

-

-

-

-

- Transposons (Sleeping Beauty, PiggyBac)

-

-

-

-

-

- mRNA electroporation

-

-

-

- Armored CAR T-Cells (enhanced T-cell persistence/activity)

-

- Safety Switch-Equipped CAR T Cells

-

- Dual and multiple antigens targeting CAR T-cell

- Canada Type Therapy Outlook (Revenue, USD Million; 2025-2032)

-

- Autologous CAR-T cell therapy

-

- Allogeneic CAR-T cell therapy

- Canada Type End User Outlook (Revenue, USD Million; 2025-2032)

-

- Hospitals

-

- Cancer Treatment Centers

-

- Other (Academic & Research Institutes, Speciality Clinics)

- Mexico

- Mexico Type Product Outlook (Revenue, USD Million; 2025-2032)

-

- Yescarta (Axicabtagene Ciloleucel)

-

- Kymriah (Tisagenlecleucel)

-

- Breyanzi (Lisocabtagene Maraleucel)

-

- Abecma (Idecabtagene Vicleucel)

-

- Carvykti (Ciltacabtagene Autoleucel / Cilta-cel)

-

- Tecartus (Brexucabtagene Autoleucel)

- Mexico Type Target Antigen Outlook (Revenue, USD Million; 2025-2032)

-

- CD19 (Cluster of Differentiation 19)

-

- BCMA (B-cell Maturation Antigen)

-

- CD22 (Cluster of Differentiation 22)

-

- GD2 (Disialoganglioside GD2)

-

- HER2 (Human Epidermal Growth Factor Receptor 2)

-

- GPC3 (Glypican-3)

-

- Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

- Mexico Type Disease/Indication Outlook (Revenue, USD Million; 2025-2032)

-

- Hematologic Malignancies (Blood Cancers)

-

-

- Lymphoma

-

-

-

-

- Diffuse Large B-cell Lymphoma (DLBCL)

-

-

-

-

-

- Primary Mediastinal B-cell Lymphoma (PMBCL)

-

-

-

-

-

- Mantle Cell Lymphoma (MCL)

-

-

-

-

-

- Follicular Lymphoma (FL)

-

-

-

-

-

- Other (Non-Hodgkin Lymphomas (NHLs)

-

-

-

-

- Leukemia

-

-

-

-

- Acute Lymphoblastic Leukemia (ALL)

-

-

-

-

-

- Chronic Lymphocytic Leukemia (CLL)

-

-

-

-

- Multiple Myeloma

-

-

-

-

- B-cell Maturation Antigen (BCMA)

-

-

- Solid Tumours

-

- Glioblastoma

-

- Pancreatic Cancer

-

- Ovarian Cancer

-

- Breast Cancer

-

- Lung Cancer

-

- Melanoma

-

- Prostate Cancer

-

- Others (Neuroblastoma Cancer, Colorectal Cancer)

- Other Diseases

-

- Autoimmune Diseases

-

- Infectious Diseases

- Mexico Type Manufacturing Method Outlook (Revenue, USD Million; 2025-2032)

-

- Point-of-Care Manufacturing

-

- Centralized manufacturing

-

- In-vivo CAR T therapy manufacturing

-

- Off-the-shelf / Ready-to-use therapies

- Mexico Type Technology/Vector Outlook (Revenue, USD Million; 2025-2032)

-

- Viral Vectors

-

-

-

- Lentiviral vectors)

-

-

-

-

-

- Retroviral vectors

-

-

-

- Non- Viral Vectors

-

-

-

- CRISPR/Cas9 gene editing

-

-

-

-

-

- Transposons (Sleeping Beauty, PiggyBac)

-

-

-

-

-

- mRNA electroporation

-

-

-

- Armored CAR T-Cells (enhanced T-cell persistence/activity)

-

- Safety Switch-Equipped CAR T Cells

-

- Dual and multiple antigens targeting CAR T-cell

- Mexico Type Therapy Outlook (Revenue, USD Million; 2025-2032)

-

- Autologous CAR-T cell therapy

-

- Allogeneic CAR-T cell therapy

- Mexico Type End User Outlook (Revenue, USD Million; 2025-2032)

-

- Hospitals

-

- Cancer Treatment Centers

-

- Other (Academic & Research Institutes, Speciality Clinics)

Europe

- Europe Type Product Outlook (Revenue, USD Million; 2025-2032)

-

- Yescarta (Axicabtagene Ciloleucel)

-

- Kymriah (Tisagenlecleucel)

-

- Breyanzi (Lisocabtagene Maraleucel)

-

- Abecma (Idecabtagene Vicleucel)

-

- Carvykti (Ciltacabtagene Autoleucel / Cilta-cel)

-

- Tecartus (Brexucabtagene Autoleucel)

- Europe Type Target Antigen Outlook (Revenue, USD Million; 2025-2032)

-

- CD19 (Cluster of Differentiation 19)

-

- BCMA (B-cell Maturation Antigen)

-

- CD22 (Cluster of Differentiation 22)

-

- GD2 (Disialoganglioside GD2)

-

- HER2 (Human Epidermal Growth Factor Receptor 2)

-

- GPC3 (Glypican-3)

-

- Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

- Europe Type Disease/Indication Outlook (Revenue, USD Million; 2025-2032)

-

- Hematologic Malignancies (Blood Cancers)

-

-

- Lymphoma

-

-

-

-

- Diffuse Large B-cell Lymphoma (DLBCL)

-

-

-

-

-

- Primary Mediastinal B-cell Lymphoma (PMBCL)

-

-

-

-

-

- Mantle Cell Lymphoma (MCL)

-

-

-

-

-

- Follicular Lymphoma (FL)

-

-

-

-

-

- Other (Non-Hodgkin Lymphomas (NHLs)

-

-

-

-

- Leukemia

-

-

-

-

- Acute Lymphoblastic Leukemia (ALL)

-

-

-

-

-

- Chronic Lymphocytic Leukemia (CLL)

-

-

-

-

- Multiple Myeloma

-

-

-

-

- B-cell Maturation Antigen (BCMA)

-

-

- Solid Tumours

-

- Glioblastoma

-

- Pancreatic Cancer

-

- Ovarian Cancer

-

- Breast Cancer

-

- Lung Cancer

-

- Melanoma

-

- Prostate Cancer

-

- Others (Neuroblastoma Cancer, Colorectal Cancer)

- Other Diseases

-

- Autoimmune Diseases

-

- Infectious Diseases

- Europe Type Manufacturing Method Outlook (Revenue, USD Million; 2025-2032)

-

- Point-of-Care Manufacturing

-

- Centralized manufacturing

-

- In-vivo CAR T therapy manufacturing

-

- Off-the-shelf / Ready-to-use therapies

- Europe Type Technology/Vector Outlook (Revenue, USD Million; 2025-2032)

-

- Viral Vectors

-

-

-

- Lentiviral vectors)

-

-

-

-

-

- Retroviral vectors

-

-

-

- Non- Viral Vectors

-

-

-

- CRISPR/Cas9 gene editing

-

-

-

-

-

- Transposons (Sleeping Beauty, PiggyBac)

-

-

-

-

-

- mRNA electroporation

-

-

-

- Armored CAR T-Cells (enhanced T-cell persistence/activity)

-

- Safety Switch-Equipped CAR T Cells

-

- Dual and multiple antigens targeting CAR T-cell

- Europe Type Therapy Outlook (Revenue, USD Million; 2025-2032)

-

- Autologous CAR-T cell therapy

-

- Allogeneic CAR-T cell therapy

- Europe Type End User Outlook (Revenue, USD Million; 2025-2032)

-

- Hospitals

-

- Cancer Treatment Centers

-

- Other (Academic & Research Institutes, Speciality Clinics)

- Germany

- Germany Type Product Outlook (Revenue, USD Million; 2025-2032)

-

- Yescarta (Axicabtagene Ciloleucel)

-

- Kymriah (Tisagenlecleucel)

-

- Breyanzi (Lisocabtagene Maraleucel)

-

- Abecma (Idecabtagene Vicleucel)

-

- Carvykti (Ciltacabtagene Autoleucel / Cilta-cel)

-

- Tecartus (Brexucabtagene Autoleucel)

- Germany Type Target Antigen Outlook (Revenue, USD Million; 2025-2032)

-

- CD19 (Cluster of Differentiation 19)

-

- BCMA (B-cell Maturation Antigen)

-

- CD22 (Cluster of Differentiation 22)

-

- GD2 (Disialoganglioside GD2)

-

- HER2 (Human Epidermal Growth Factor Receptor 2)

-

- GPC3 (Glypican-3)

-

- Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

- Germany Type Disease/Indication Outlook (Revenue, USD Million; 2025-2032)

-

- Hematologic Malignancies (Blood Cancers)

-

-

- Lymphoma

-

-

-

-

- Diffuse Large B-cell Lymphoma (DLBCL)

-

-

-

-

-

- Primary Mediastinal B-cell Lymphoma (PMBCL)

-

-

-

-

-

- Mantle Cell Lymphoma (MCL)

-

-

-

-

-

- Follicular Lymphoma (FL)

-

-

-

-

-

- Other (Non-Hodgkin Lymphomas (NHLs)

-

-

-

-

- Leukemia

-

-

-

-

- Acute Lymphoblastic Leukemia (ALL)

-

-

-

-

-

- Chronic Lymphocytic Leukemia (CLL)

-

-

-

-

- Multiple Myeloma

-

-

-

-

- B-cell Maturation Antigen (BCMA)

-

-

- Solid Tumours

-

- Glioblastoma

-

- Pancreatic Cancer

-

- Ovarian Cancer

-

- Breast Cancer

-

- Lung Cancer

-

- Melanoma

-

- Prostate Cancer

-

- Others (Neuroblastoma Cancer, Colorectal Cancer)

- Other Diseases

-

- Autoimmune Diseases

-

- Infectious Diseases

- Germany Type Manufacturing Method Outlook (Revenue, USD Million; 2025-2032)

-

- Point-of-Care Manufacturing

-

- Centralized manufacturing

-

- In-vivo CAR T therapy manufacturing

-

- Off-the-shelf / Ready-to-use therapies

- Germany Type Technology/Vector Outlook (Revenue, USD Million; 2025-2032)

-

- Viral Vectors

-

-

-

- Lentiviral vectors)

-

-

-

-

-

- Retroviral vectors

-

-

-

- Non- Viral Vectors

-

-

-

- CRISPR/Cas9 gene editing

-

-

-

-

-

- Transposons (Sleeping Beauty, PiggyBac)

-

-

-

-

-

- mRNA electroporation

-

-

-

- Armored CAR T-Cells (enhanced T-cell persistence/activity)

-

- Safety Switch-Equipped CAR T Cells

-

- Dual and multiple antigens targeting CAR T-cell

- Germany Type Therapy Outlook (Revenue, USD Million; 2025-2032)

-

- Autologous CAR-T cell therapy

-

- Allogeneic CAR-T cell therapy

- Germany Type End User Outlook (Revenue, USD Million; 2025-2032)

-

- Hospitals

-

- Cancer Treatment Centers

-

- Other (Academic & Research Institutes, Speciality Clinics)

- France

- France Type Product Outlook (Revenue, USD Million; 2025-2032)

-

- Yescarta (Axicabtagene Ciloleucel)

-

- Kymriah (Tisagenlecleucel)

-

- Breyanzi (Lisocabtagene Maraleucel)

-

- Abecma (Idecabtagene Vicleucel)

-

- Carvykti (Ciltacabtagene Autoleucel / Cilta-cel)

-

- Tecartus (Brexucabtagene Autoleucel)

- France Type Target Antigen Outlook (Revenue, USD Million; 2025-2032)

-

- CD19 (Cluster of Differentiation 19)

-

- BCMA (B-cell Maturation Antigen)

-

- CD22 (Cluster of Differentiation 22)

-

- GD2 (Disialoganglioside GD2)

-

- HER2 (Human Epidermal Growth Factor Receptor 2)

-

- GPC3 (Glypican-3)

-

- Others (EGFRvIII, CD7(Cluster of Differentiation 7), CD123(Cluster of Differentiation 123), mesothelin)

- France Type Disease/Indication Outlook (Revenue, USD Million; 2025-2032)

-

- Hematologic Malignancies (Blood Cancers)

-

-

- Lymphoma

-

-

-

-

- Diffuse Large B-cell Lymphoma (DLBCL)

-

-

-

-

-

- Primary Mediastinal B-cell Lymphoma (PMBCL)

-

-

-

-

-

- Mantle Cell Lymphoma (MCL)

-

-

-

-

-

- Follicular Lymphoma (FL)

-

-

-

-

-

- Other (Non-Hodgkin Lymphomas (NHLs)

-

-

-

-

- Leukemia

-

-

-

-

- Acute Lymphoblastic Leukemia (ALL)

-

-

-

-

-

- Chronic Lymphocytic Leukemia (CLL)

-

-

-

-

- Multiple Myeloma

-

-

-

-

- B-cell Maturation Antigen (BCMA)

-

-

- Solid Tumours

-

- Glioblastoma

-

- Pancreatic Cancer

-

- Ovarian Cancer

-

- Breast Cancer

-

- Lung Cancer

-

- Melanoma

-

- Prostate Cancer

-

- Others (Neuroblastoma Cancer, Colorectal Cancer)

- Other Diseases

-

- Autoimmune Diseases

-

- Infectious Diseases

- France Type Manufacturing Method Outlook (Revenue, USD Million; 2025-2032)

-

- Point-of-Care Manufacturing

-

- Centralized manufacturing

-

- In-vivo CAR T therapy manufacturing

-

- Off-the-shelf / Ready-to-use therapies

- France Type Technology/Vector Outlook (Revenue, USD Million; 2025-2032)

-

- Viral Vectors

-

-

-

- Lentiviral vectors)

-

-

-

-

-

- Retroviral vectors

-

-

-

- Non- Viral Vectors

-

-

-

- CRISPR/Cas9 gene editing

-

-

-

-

-

- Transposons (Sleeping Beauty, PiggyBac)

-

-

-

-

-

- mRNA electroporation

-

-

-