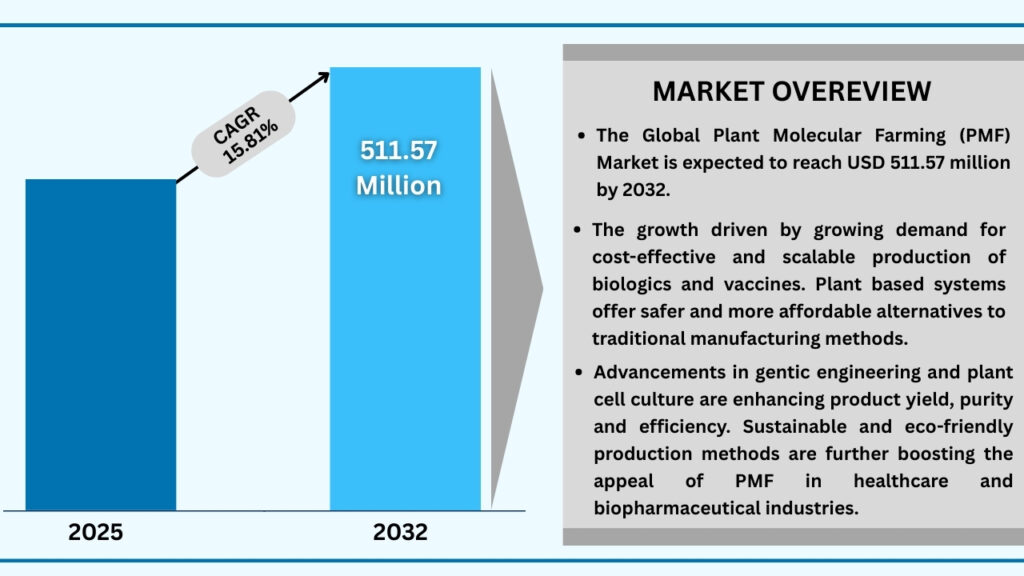

Market Synopsis

The Plant Molecular Farming (PMF) Market size was USD 158.99 Million in 2024 and is expected to reach USD 511.57 million at a CAGR of 15.81% during the forecast period. The growth of the Plant Molecular Farming (PMF) Market is being driven by increasing demand for cost-effective and scalable production of biopharmaceuticals, vaccines, and therapeutic proteins. Plant-based platforms offer an attractive alternative to traditional microbial or mammalian cell culture systems by reducing production costs, eliminating the need for expensive fermentation facilities, and allowing easier scale-up. Furthermore, the rising prevalence of chronic diseases and infectious diseases has accelerated research and development in biologics, encouraging investments in plant-derived proteins, antibodies, and vaccines. Regulatory bodies are also becoming more supportive of plant-based manufacturing due to its safety, sustainability, and lower risk of contamination compared to animal-based systems.

In addition, technological advancements in genetic engineering, plant cell culture, and expression systems are enhancing yield, product purity, and production efficiency. Several pharmaceutical companies and research institutes are collaborating to develop innovative plant-based solutions, while government funding and grants are supporting large-scale cultivation and clinical trials. Growing consumer preference for sustainable and natural ingredients in healthcare and cosmetics further boosts the adoption of plant-derived molecular products. With these factors combined, the PMF market is poised for significant expansion across North America, Europe, and emerging regions such as Asia-Pacific and Latin America.

Additionally, the increasing focus on environmentally friendly and sustainable production methods is propelling the growth of the PMF market. Plant-based manufacturing processes consume fewer resources, produce lower greenhouse gas emissions, and offer biodegradable by-products, aligning with global initiatives to reduce the environmental footprint of pharmaceutical and biotechnology industries. Moreover, the flexibility of plant systems to express complex proteins and rare compounds is attracting research in personalized medicine and niche therapeutics. As awareness of these benefits spreads among healthcare providers, investors, and policymakers, the demand for plant molecular farming solutions continues to rise, making it a promising segment within the broader biopharmaceutical landscape.

Global Plant Molecular Farming (PMF) Market (USD Million)

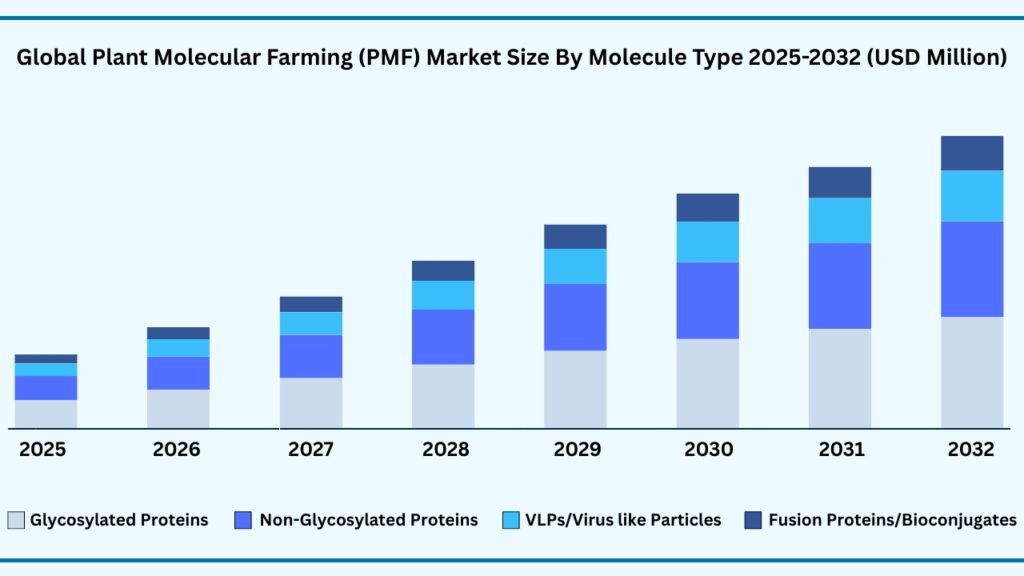

Global Plant Molecular Farming (PMF) Market by Molecule Type Insights:

Glycosylated proteins segment accounted for market share of share 52.11% in 2024 in the global Plant Molecular Farming (PMF) market.

The Glycosylated proteins segment accounted for the largest share of the global Plant Molecular Farming (PMF) market in 2024, representing 42.32 % of total revenues, as these proteins play a crucial role in the development of vaccines, therapeutic antibodies, and diagnostic agents. Plant-based systems are increasingly preferred for producing glycosylated proteins because they can replicate complex post-translational modifications, ensuring higher efficacy and stability while significantly reducing production costs compared to traditional cell culture methods. Additionally, the growing need for biologics that are free from animal-derived components is encouraging pharmaceutical companies to invest in plant molecular farming solutions.

Looking ahead to 2032, the demand for glycosylated proteins is expected to surge, driven by the rising prevalence of chronic diseases, infectious outbreaks, and the need for safer, more efficient therapies. Continuous advancements in plant expression technologies, such as improved bioreactors and optimized growth media, are enhancing yield and scalability, making plant-based platforms more commercially viable. Furthermore, increasing government initiatives, regulatory approvals, and venture capital funding are supporting research and infrastructure development, positioning glycosylated proteins as a key growth driver in the PMF market’s expansion over the coming decade.

Let me know if you want this version even more technical or investor-friendly depending on your report’s audience.

Global Plant Molecular Farming (PMF) Market by Molecule Type (USD Million)

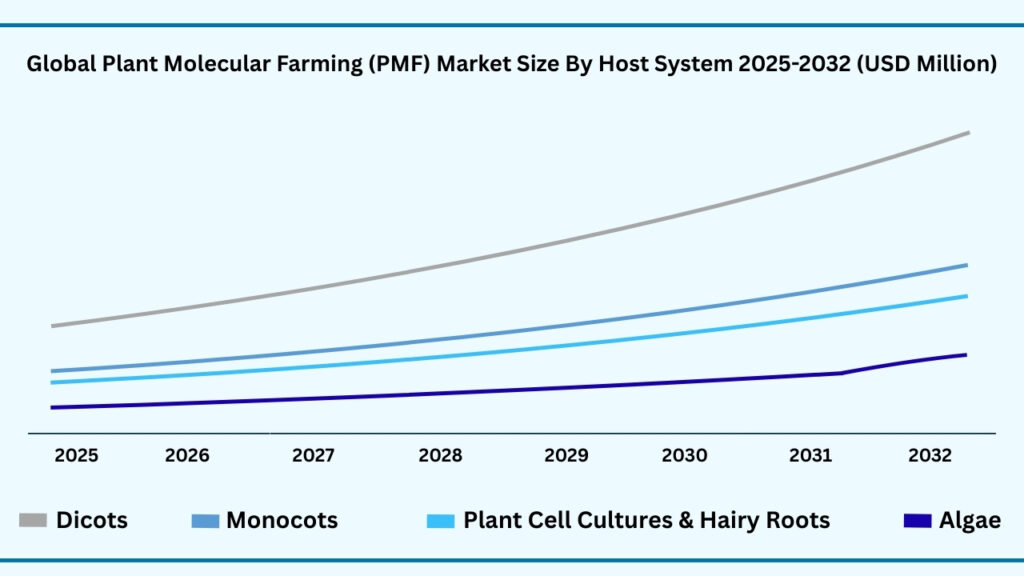

Global Plant Molecular Farming (PMF) Market by Host System Insights:

Dicots segment accounted for the largest market share of share 41.25% in 2024 in the global Plant Molecular Farming (PMF) market.

Based on the host type, Dicots segment held the largest revenue share of 44.55% 2024, and expected to register a CAGR of 15.66% between 2025 to 2032 and the market is expected to reach USD 224.87 by 2032. As these plants offer favorable biological traits for producing high-value proteins, enzymes, and vaccines. Their well-understood genetic makeup, ability to perform complex post-translational modifications, and adaptability to various cultivation environments make them ideal hosts for molecular farming. Furthermore, dicot plants like tobacco, alfalfa, and lettuce are widely used in pharmaceutical and biotechnological applications, allowing efficient scaling and cost-effective production compared to other host types. This growth will be driven by increasing investments in plant-based biologics, advancements in genetic engineering techniques, and rising demand for sustainable, animal-free protein sources. Supportive government policies, partnerships between biotech firms and research institutions, and the expansion of commercial cultivation facilities will further enhance production capabilities and boost global adoption of dicot-based molecular farming platforms.

Global Plant Molecular Farming (PMF) Market by Host System (USD Million)

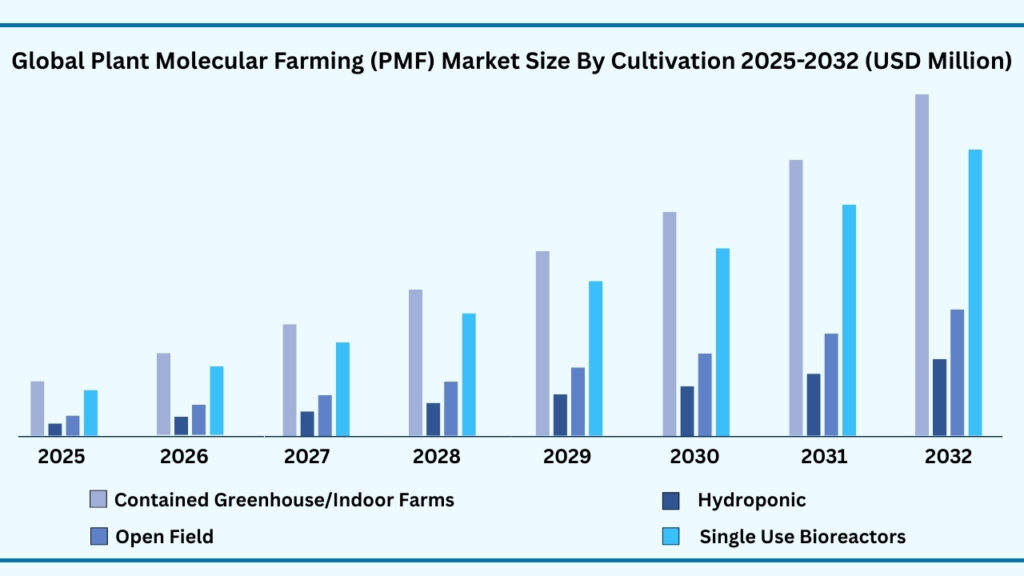

Global Plant Molecular Farming (PMF) Marekt by Cultivation Insights:

Contained greenhouse/indoor farms segment accounted for the largest market share of share 53.21% in 2024 in the global Plant Molecular Farming (PMF) market.

Based on cultivation, contained greenhouse/indoor farms segment held the largest revenue share of 53.21% in the Plant Molecular Farming (PMF) market in 2024 and expected to register a CAGR of 15.43% from 2025 to 2032 and expected to reach USD 266.07 million. The Contained greenhouse and indoor farms segment is growing due to its ability to provide controlled environments that optimize plant growth, protein expression, and overall yield. These facilities offer protection from environmental stressors, pests, and contamination, ensuring consistent and high-quality production. The scalability of indoor systems, combined with efficient resource management and automation technologies, makes them particularly suitable for producing sensitive biologics and specialized proteins required in pharmaceuticals and healthcare.

The segment’s growth is further supported by advancements in climate control systems, hydroponics, and nutrient delivery methods, which enhance plant health and protein output. Additionally, the increasing focus on sustainable and bio secure manufacturing processes is encouraging investments in contained cultivation methods. Partnerships between biotech companies, research institutes, and government bodies are also accelerating the development of infrastructure and technological solutions, enabling widespread adoption of indoor farming for plant molecular farming applications.

Global Plant Molecular Farming (PMF) Market by Cultivation (USD Million)

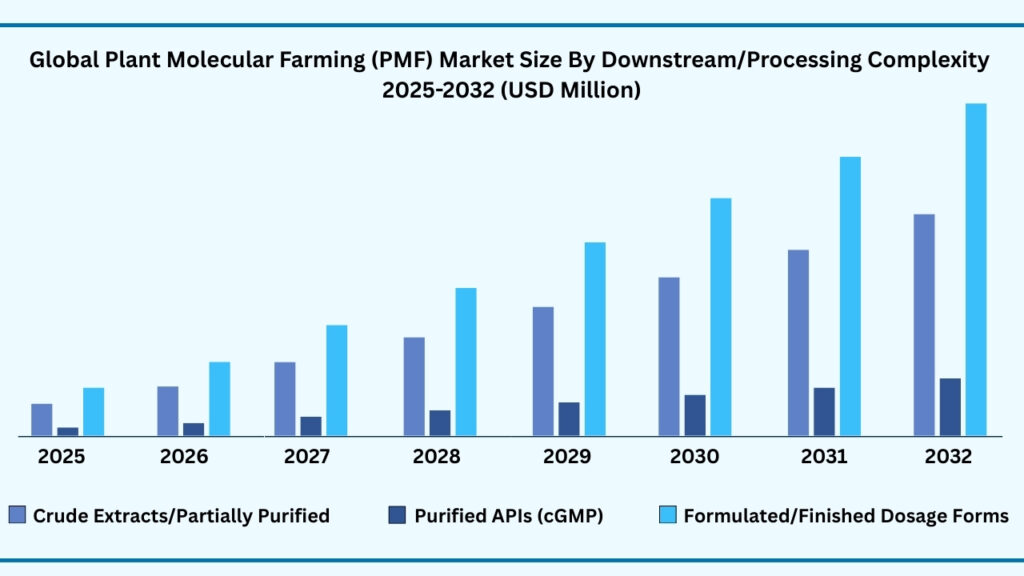

Global Plant Molecular Farming (PMF) Market by Downstream/Processing Complexity:

Crude extracts/partially purified segment accounted for the largest market share of share 37.45% in 2024 in the global Plant Molecular Farming (PMF) Market.

Based on Downstream/Processing Complexity, the Crude extracts/partially purified segment held the largest revenue share of 35.32% in the global Plant Molecular Farming (PMF) market in 2024 and expected to register a CAGR of 15.31 % from 2025 to 2032 is expected to reach USD 175.57 million. The crude extracts and partially purified segment is growing steadily as it offers a simpler and more cost-effective approach to producing plant-based proteins. Many applications, such as veterinary vaccines, diagnostics, and certain topical formulations, do not require highly purified proteins, making crude extracts a practical solution. The ease of extraction from plants, coupled with lower processing requirements, allows manufacturers to meet increasing demand quickly and efficiently. Additionally, regions with limited infrastructure or cost constraints are adopting this method, as it reduces the need for expensive purification equipment and processes.

On a global scale, the growth is being fueled by the rising interest in sustainable and alternative production methods. As companies and research organizations seek to minimize reliance on animal-based or synthetic sources, plant-derived proteins through crude extraction are becoming a preferred option. Regulatory bodies are also supporting the development of plant-made biologics, further encouraging adoption. The expanding applications across healthcare, agriculture, and wellness sectors, along with the focus on affordable and accessible solutions, are collectively driving the rise of this segment in the Plant Molecular Farming market.

Global Plant Molecular Farming (PMF) Market by Downstream/Processing Complexity (USD Million)

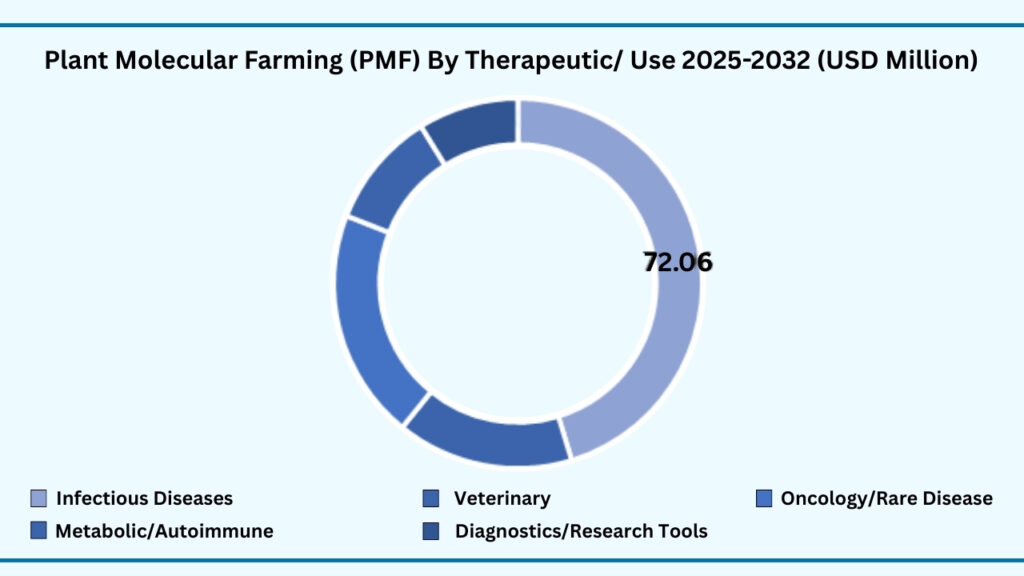

Global Plant Molecular Farming (PMF) Market by Therapeutic/Use Insights:

Infectious diseases accounted for the largest market share of share 45.32% in 2024 in the global Plant Molecular Farming (PMF) Market.

Based on Therapeutic/Use, the Infectious diseases segment held the largest revenue share of 45.32% in the global Plant Molecular Farming (PMF) market in 2024 and expected to register a CAGR of 15.73% from 2025 to 2032 and expected to reach USD 230.72 million in 2032. The infectious diseases segment is driving growth in the Plant Molecular Farming market because of the increasing global focus on developing vaccines and therapeutics to combat outbreaks and endemic diseases. Plant-based systems offer a rapid, scalable, and cost-effective method for producing vaccine candidates, especially for viral infections such as influenza, COVID-19, and HPV. The ability to quickly modify plant expression systems to target emerging pathogens makes this segment highly attractive for both public health initiatives and pharmaceutical companies. Furthermore, the demand for affordable vaccine solutions in low- and middle-income countries is prompting governments and global health organizations to invest in plant-based technologies that can be produced locally with reduced logistical and manufacturing constraints.

Additionally, regulatory support and advances in biotechnology are further fueling the adoption of plant-made biologics in infectious disease prevention and treatment. Increasing partnerships between biotech firms, research institutions, and global health bodies are facilitating faster development and distribution of plant-derived vaccines. With rising concerns about antimicrobial resistance, zoonotic diseases, and potential future pandemics, the infectious disease segment is positioned at the forefront of innovation. This, combined with efforts to enhance healthcare accessibility and sustainability, continues to expand the relevance and application of plant molecular farming in addressing global health challenges.

Global Plant Molecular Farming (PMF) by Therapeutic/Use (USD Million)

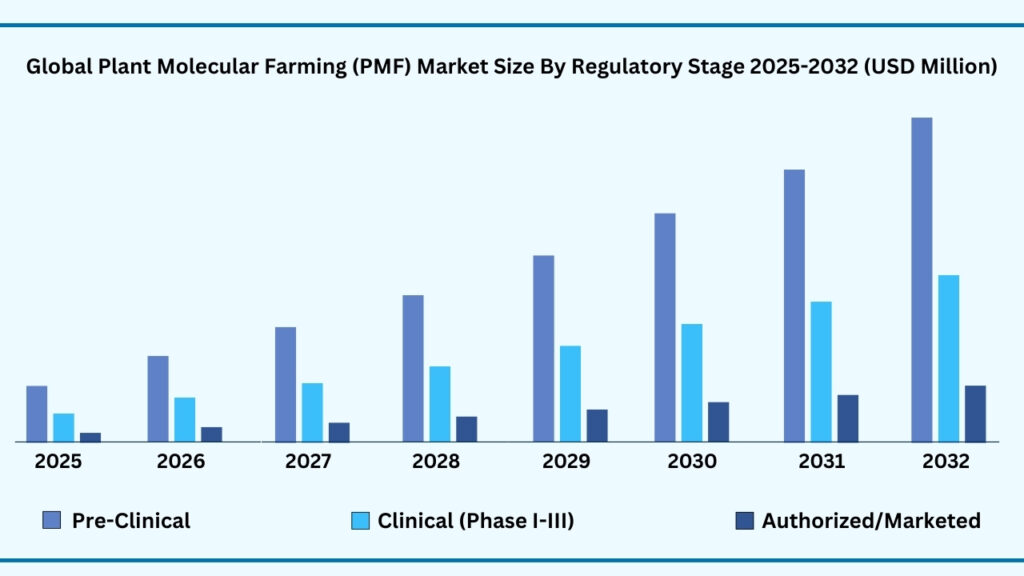

Global Plant Molecular Farming (PMF) Market by Regulatory Stage Insights:

Pre-clinical segment accounted for the largest market share of share of 49.20% in 2024 in the global Plant Molecular Farming (PMF) Market.

Based on Regulatory Stage, the adult segment held the largest revenue share of 65.45% in the global Plant Molecular Farming (PMF) market in 2024 and expected to register a CAGR of 15.70% from 2025 to 2032 and expected to reach USD 334.21 million in 2032. The adult segment is experiencing significant growth as plant-made biologics are increasingly being used to address health conditions that predominantly affect adult populations. Vaccines, therapeutic proteins, and antibodies targeted at diseases such as influenza, cardiovascular disorders, metabolic diseases, and cancer are in high demand. Adults represent the largest healthcare consumer base globally, and the rise in chronic and infectious diseases among this population is prompting greater investments in novel treatment options. Plant molecular farming offers scalable, cost-effective solutions that can meet the growing need for accessible therapies, especially in aging populations and regions with limited healthcare infrastructure.

Moreover, regulatory frameworks in several countries are evolving to support the use of plant-based biologics for adult healthcare applications. Streamlined approval processes, coupled with increased funding for research and development, are encouraging pharmaceutical companies to explore plant-derived vaccines and therapeutics. In addition, partnerships between governments, research institutions, and private sector players are accelerating clinical trials and bringing products closer to market. The focus on improving treatment affordability, reducing production time, and ensuring supply chain resilience further strengthens the position of plant-based solutions in adult healthcare, driving sustained growth in this segment.

Global Plant Molecular Farming (PMF) by Regulatory Stage (USD Million)

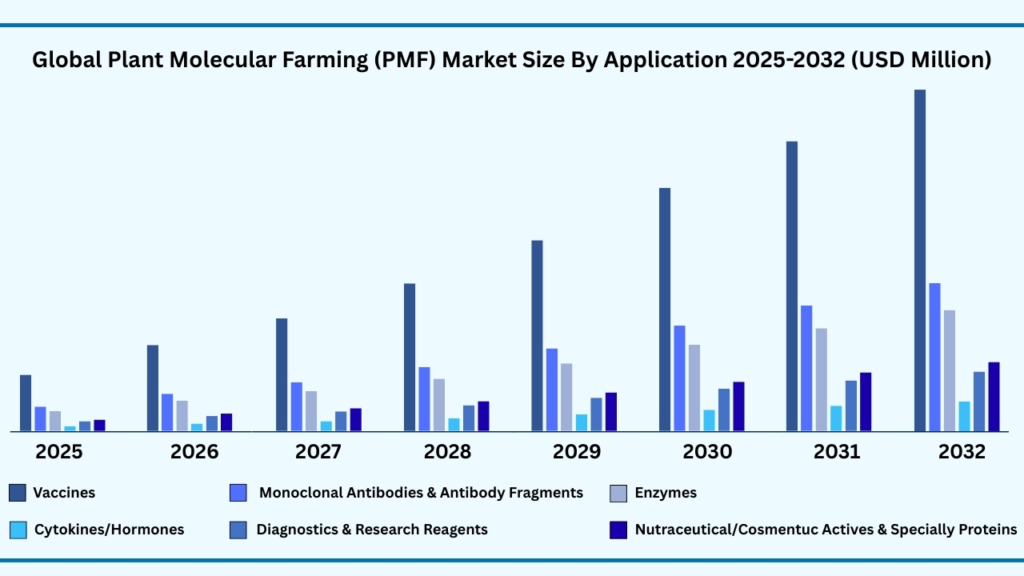

Global Plant Molecular Farming (PMF) Market by Application Insights:

Vaccines segment accounted for the largest market share of share of 49.20% in 2024 in the global Plant Molecular Farming (PMF) Market.

Based on Application, the Vaccines segment held the largest revenue share of 40.22% in the global Plant Molecular Farming (PMF) market in 2024 and expected to register a CAGR of 15.69% from 2025 to 2032 and expected to reach USD 205.24 million in 2032. The Vaccines segment is witnessing significant growth due to increasing demand for cost-effective and scalable vaccine production platforms. Plant molecular farming offers a promising alternative to traditional vaccine manufacturing methods, which are often expensive, time-consuming, and reliant on complex infrastructure. The ability to produce vaccines in plants reduces the risk of contamination from animal-derived pathogens and simplifies the downstream processing steps. Moreover, growing global health concerns such as infectious diseases and pandemic outbreaks are driving governments and pharmaceutical companies to invest in innovative technologies like PMF that can accelerate vaccine development and distribution.

Additionally, technological advancements in genetic engineering and molecular biology are enhancing the efficiency and yield of plant-based vaccines. Regulatory frameworks are evolving to support faster approval and deployment of plant-derived pharmaceuticals, further boosting market adoption. The expanding biopharmaceutical sector and rising awareness about preventive healthcare are also contributing to the increased focus on plant-based vaccines.

Global Plant Molecular Farming (PMF) by Application (USD Million)

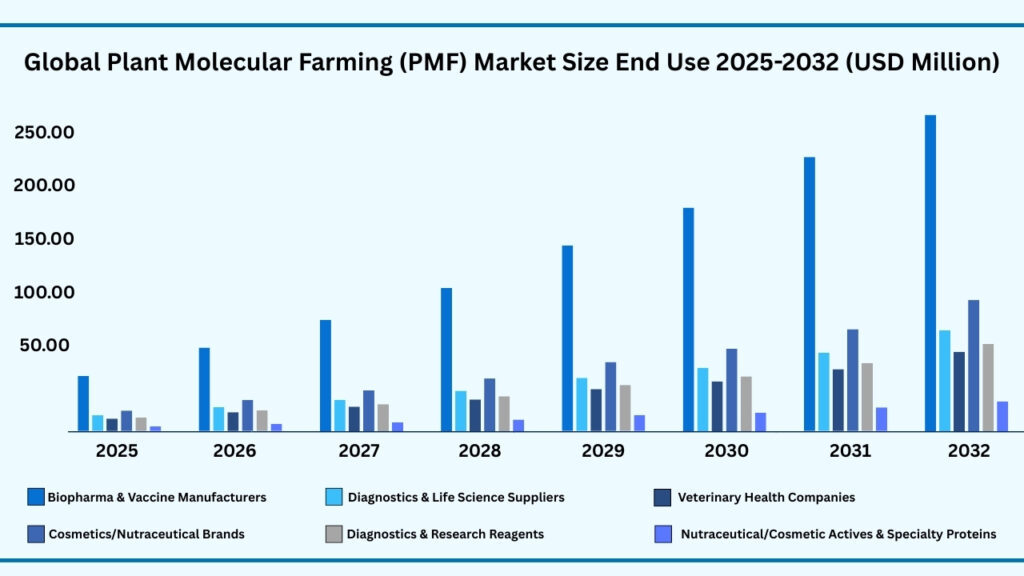

Global Plant Molecular Farming (PMF) Market by End Use Insights:

Biopharma & vaccine manufacturers segment accounted for the largest market share of share of 42.22% in 2024 in the global Plant Molecular Farming (PMF) Market.

Based on end use, the Biopharma & vaccine manufacturers segment held the largest revenue share of 40.22% in the global Plant Molecular Farming (PMF) market in 2024 and expected to register a CAGR of 15.34% from 2025 to 2032 and expected to reach USD 205.24 million in 2032. The Vaccines segment is witnessing significant growth due to increasing demand for cost-effective and scalable vaccine production platforms. Plant molecular farming offers a promising alternative to traditional vaccine manufacturing methods, which are often expensive, time-consuming, and reliant on complex infrastructure. The ability to produce vaccines in plants reduces the risk of contamination from animal-derived pathogens and simplifies the downstream processing steps. Moreover, growing global health concerns such as infectious diseases and pandemic outbreaks are driving governments and pharmaceutical companies to invest in innovative technologies like PMF that can accelerate vaccine development and distribution.

Additionally, technological advancements in genetic engineering and molecular biology are enhancing the efficiency and yield of plant-based vaccines. Regulatory frameworks are evolving to support faster approval and deployment of plant-derived pharmaceuticals, further boosting market adoption. The expanding biopharmaceutical sector and rising awareness about preventive healthcare are also contributing to the increased focus on plant-based vaccines.

Global Plant Molecular Farming (PMF) by End Use (USD Million)

Global Plant Molecular Farming (PMF) Market by Region Insights:

North America segment accounted for the largest market share of share of 34.11% in 2024 in the global Functional Shots & Mini Beverages market.

Based on end use, the global Plant Molecular Farming (PMF) market is segmented into Europe, Asia-Pacific, North America, Latin America and Middle East & Africa. Among these, North America region held the largest revenue share of 34.11% in the global Plant Molecular Farming (PMF) market in 2024 and expected to reach USD 174.50 million in 2032. The region is home to a well-established pharmaceutical and biotechnology industry with strong infrastructure, advanced research facilities, and significant investments in R&D. North American companies and research institutions are at the forefront of developing innovative plant-based production technologies, which has accelerated the adoption of PMF solutions in vaccine development, therapeutic proteins, and other biopharmaceutical applications. The region’s focus on personalized medicine, preventive healthcare, and sustainable production methods further boosts demand for plant-derived pharmaceutical products.

Additionally, supportive government initiatives, favorable regulatory frameworks, and partnerships between academic institutions and industry players are contributing to the market’s growth. The presence of key biopharma companies that are actively exploring plant molecular farming as an alternative production platform also enhances the region’s competitiveness. Rising awareness of plant-based therapeutics among healthcare providers and consumers, along with an increasing focus on reducing environmental impact in pharmaceutical manufacturing, is further driving market expansion.

Global Plant Molecular Farming (PMF) by Region (USD Million)

Major Companies and Competitive Landscape

The global Plant Molecular Farming (PMF) market is highly fragmented, with established biopharmaceutical corporations and emerging biotech startups competing to deliver efficient and sustainable solutions. Leading players are actively pursuing strategies such as research collaborations, strategic partnerships with vaccine manufacturers, and alliances with academic institutions to accelerate innovation and expand their footprint. Many companies are investing heavily in developing advanced plant-based platforms for producing vaccines, therapeutic proteins, and other biopharmaceuticals — aiming to enhance yield, reduce production costs, and ensure scalability. These innovations focus on improving purity, bioavailability, and patient safety while addressing pressing global healthcare challenges.

Moreover, organizations are emphasizing sustainable agricultural practices, environmentally friendly processing techniques, and transparent supply chains to build trust among stakeholders. With increasing demand for cost-effective, contamination-free, and rapidly deployable solutions, especially in response to global health emergencies, the PMF sector is refining its offerings to meet the needs of healthcare providers and patients alike. Supportive regulatory frameworks, expanding investments in plant biotechnology, and growing collaborations between industry and research centers are driving adoption. This convergence of innovation, sustainability, and healthcare demand is expected to propel the growth of the Plant Molecular Farming market across regions, ensuring wider accessibility and long-term resilience.

Some of the leading companies profiled in the global Plant Molecular Farming (PMF) market report include:

- Medicago Inc.

- iBio Inc.

- Kentucky BioProcessing

- Protalix BioTherapeutics

- Ventria Bioscience

- Planet Biotechnology Inc.

- Leaf Expression Systems Ltd.

- ICON Genetics GmbH

- Protalix BioTherapeutics, Inc.

- ORF Genetics

- Miruku

- Mozza

- Nobell Foods (Alpine Bio).

- Bright Biotech

- Tiamat Sciences

- Moolec Science SA.

- PoLoPo (Israel)

- VelozBio (Mexico)

- Forte Protein

- IngredientWerks

- Elo Life Systems

- Transactiva Srl

- Bright Biotech

- Guardian Biotechnologies

- ReaGenics

Strategic Development

Medicago Inc. (Canada) – In early 2025, Medicago Inc. announced the closure of its operations after previously developing plant-based vaccine platforms, including the approved Covifenz™ COVID-19 vaccine. The company is working on transferring key technologies and intellectual property to strategic partners to ensure continuity in plant-based vaccine research and therapeutics.

iBio Inc. (USA) – In August 2025, iBio completed an in-licensing agreement to acquire two advanced therapeutic assets, IBIO-600 and IBIO-610, from AstralBio. The company is advancing its pipeline with long-acting anti-myostatin antibody formulations aimed at muscle growth and wasting disorders, positioning itself to address unmet medical needs with innovative plant-derived solutions.

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 158.99 Million |

| CAGR (2024–2032) | 15.81% |

| Revenue forecast to 2033 | USD 511.57 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million, and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Product Type, By Molecule Type, By Host System, By Cultivation, By Downstream/Processing Complexity, By Therapeutic/Use, By Regulatory Stage, By Application, By End Use and By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, UAE, South Africa, Turkey, Rest of MEA |

| Key companies profiled | “Medicago Inc., iBio Inc., Kentucky BioProcessing, Protalix BioTherapeutics, Ventria Bioscience, Planet Biotechnology Inc., Leaf Expression Systems Ltd., ICON Genetics GmbH, Protalix BioTherapeutics, Inc., ORF Genetics, Miruku, Mozza, Nobell Foods., Bright Biotech , Tiamat Sciences, Moolec Science SA., PoLoPo, VelozBio (Mexico), Forte Protein, IngredientWerks, Elo Life Systems Transactiva Srl, Bright Biotech, Guardian Biotechnologies ReaGenics” |

| Customization scope | 10 hours of free customization and expert consultation |

Some Key Questions the Report Will Answer

- What is the expected revenue Compound Annual Growth Rate (CAGR) of the global Plant Molecular Farming (PMF) market over the forecast period (2025–2032)?

- The global Plant Molecular Farming (PMF) market revenue is expected to register a Compound Annual Growth Rate (CAGR) of 15.81% during the forecast period.

- What was the size of the global Plant Molecular Farming (PMF) in 2024?

- The global Plant Molecular Farming (PMF) market size was USD 158.99 Million in 2024.

- Which factors are expected to drive the global Plant Molecular Farming (PMF) market growth?

- The global Plant Molecular Farming (PMF) market is expected to be driven by factors such as the growing demand for cost-effective and scalable biologics production, increasing prevalence of infectious diseases, and the need for rapid vaccine development. Advances in genetic engineering and plant biotechnology are improving yield, purity, and bioavailability of plant-derived vaccines and therapeutic proteins, while reducing production costs and contamination risks. Supportive government policies, rising investments in healthcare innovation, and expanding collaborations between pharmaceutical companies and research institutions are further accelerating adoption. Additionally, the focus on sustainable and eco-friendly manufacturing processes, along with rising awareness of preventive healthcare and personalized medicine, is propelling the market’s growth across regions.

- Which was the leading segment in the global Plant Molecular Farming (PMF) market in terms of Molecule type in 2024?

- Glycosylated proteins was leading in the global Plant Molecular Farming (PMF) market on the basis of Molecule type in 2024.

- What are some restraints for revenue growth of the global Plant Molecular Farming (PMF) market?

- The revenue growth of the global Plant Molecular Farming (PMF) market faces restraints such as stringent regulatory requirements, high initial research and development costs, and challenges related to scaling up production while maintaining consistent quality. Limited awareness and acceptance of plant-derived biologics among healthcare providers and patients, along with competition from well-established conventional manufacturing methods, also hinder market expansion. Additionally, supply chain complexities, dependency on specific plant species, and potential risks of genetic instability or cross-contamination create operational and financial uncertainties. These factors, combined with reimbursement issues and intellectual property concerns, pose significant challenges to widespread adoption and revenue growth in the PMF sector.

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of Plant Molecular Farming (PMF)

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1.Primary

2.1.2.Secondary

2.1.3.Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1.Market value

2.3.2.Market volume

2.3.3.Exchange rate

2.3.4.Price

2.3.5.Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2025–2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10. Formulation & manufacturing4.11.Distribution & retail

4.12. Import-export analysis

4.13. Brand comparative analysis

4.14. Technological advancements

4.15. Porter’s five force

4.15.1. Threat of new entrants

4.15.1.1. Capital requirment

4.15.1.2. Product knowledge

4.15.1.3. Technical knowledge

4.15.1.4. Customer relation

4.15.1.5. Access to appliation and technology

4.15.2. Threat of substitutes

4.15.2.1. Cost

4.15.2.2. Performance

4.15.2.3. Availability

4.15.2.4. Technical knowledge

4.15.2.5. Durability

4.15.3. Bargainning power of buyers

4.15.3.1. Numbers of buyers relative to suppliers

4.15.3.2. Product differentiation

4.15.3.3. Threat of forward integration

4.15.3.4. Buyers volume

4.15.4. Bargainning power of suppliers

4.15.4.1. Suppliers concentration

4.15.4.2. Buyers switching cost to other suppliers

4.15.4.3. Threat of backward integration

4.15.5. Bargainning power of suppliers

4.15.5.1. Industry concentration

4.15.5.2. Industry growth rate

4.15.5.3. Product differentiation

4.16. Patent analysis

4.17. Regulation coverage

4.18. Pricing analysis

4.19. Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1.Growing Demand for Recombinant Proteins & Biopharmaceuticals

5.1.2.Advancements in Plant Biotechnology

5.1.3.Rising Focus on Sustainable Production

5.2. Restraints

5.2.1.Regulatory Complexities

5.2.2.High Initial R&D Costs

5.3. Opportunities

5.3.1.Vaccine & Therapeutic Development

5.3.2.Plant-Based Biomanufacturing Expansion

5.3.3.Partnerships & Collaborations

5.4. Threat

5.4.1.Public Perception & Acceptance

5.4.2.Scalability & Yield Consistency

Chapter 6. Plant Molecular Farming (PMF) By Molecule Type Insights & Trends, Revenue (USD

Million),

6.1. Molecule Type Dynamics & Market Share, 2025–2032

6.1.1.1. Glycosylated proteins

6.1.1.2. Non-glycosylated proteins

6.1.1.3. VLPs/virus-like particles

6.1.1.4. Fusion proteins/bioconjugates

Chapter 7. Plant Molecular Farming (PMF) By Host System Insights & Trends, Revenue (USD

Million),

7.1. Host System Dynamics & Market Share, 2025–2032

7.1.1. Dicots

7.1.2. Monocots

7.1.3. Plant cell cultures & hairy roots

7.1.4. Algae

Chapter 8. Plant Molecular Farming (PMF) By Cultivation Insights & Trends, Revenue (USD

Million),

8.1. Cultivation Dynamics & Market Share, 2025–2032

8.1.1. Contained greenhouse/indoor farms

8.1.2. Hydroponic

8.1.3. Open-field

8.1.4. Single-use bioreactors

Chapter 9. Plant Molecular Farming (PMF) By Downstream/Processing Complexity Insights &

Trends, Revenue (USD Million),

9.1. Downstream/Processing Complexity Type Dynamics & Market Share, 2025–2032

9.1.1. Crude extracts/partially purified

9.1.2. Purified APIs (cGMP)

9.1.3. Formulated/finished dosage forms

Chapter 10. Plant Molecular Farming (PMF) By Therapeutic/Use Area Insights & Trends, Revenue

(USD Million),

10.1. Therapeutic/Use Area & Market Share, 2025–2032

10.1.1.Infectious diseases

10.1.2.Veterinary

10.1.3.Oncology/rare diseases

10.1.4.Metabolic/autoimmune

10.1.5.Diagnostics/research tools

Chapter 11. Plant Molecular Farming (PMF) By Regulatory Stage Insights & Trends, Revenue (USD

Million),

11.1. Regulatory Dynamics & Market Share, 2025–2032

11.1.1.Pre-clinical

11.1.2.Clinical (Phase I–III)

11.1.3.Authorized/marketed

Chapter 12. Plant Molecular Farming (PMF) By Application Insights & Trends, Revenue (USD

Million),

12.1. Application Dynamics & Market Share, 2025–2032

12.1.1. Vaccines

12.1.2.Monoclonal antibodies & antibody fragments

12.1.3.Enzymes

12.1.4.Cytokines/hormones

12.1.5.Diagnostics & research reagents

12.1.6.Nutraceutical/cosmetic actives & specialty proteins

Chapter 13. Plant Molecular Farming (PMF) By End Use Insights & Trends, Revenue (USD Million),

13.1. End Use Dynamics & Market Share, 2025–2032

13.1.1. Biopharma & vaccine manufacturers

13.1.2.Diagnostics & life-science suppliers

13.1.3.Veterinary health companies

13.1.4.Cosmetics/nutraceutical brands

13.1.5.Diagnostics & research reagents

13.1.6.Academic & government research institutes

Chapter 14. Plant Molecular Farming (PMF) Regional Outlook

14.1. Functional Shots & Mini Beverages Share By Region, 2025–2032

14.2. North America

14.2.1. Market By Molecule Type, Market Estimates and Forecast, USD Million,2025-

2032

14.2.1.1. Energy Glycosylated proteins

14.2.1.2. Non-glycosylated proteins

14.2.1.3. VLPs/virus-like particles

14.2.1.4. Fusion proteins/bioconjugates

14.3.Market By Host System Estimates and Forecast, USD Million, 2025-2032

14.3.1.Dicots

14.3.2.Monocots

14.3.3.Plant cell cultures & hairy roots

14.3.4.Algae

14.4.Market By Cultivation, Market Estimates and Forecast, USD Million, 2025-2032

14.4.1.Contained greenhouse/indoor farms

14.4.2.Hydroponic

14.4.3.Open-field

14.4.4.Single-use bioreactors

14.5.Market By Downstream/Processing Complexity, Market Estimates and Forecast, USD

Million, 2025-2032

14.5.1.Crude extracts/partially purified

14.5.2.Purified APIs (cGMP)

14.5.3.Formulated/finished dosage forms

14.6.Market By Therapeutic/Use Area, Market Estimates and Forecast, USD Million,

2025-2032

14.6.1.Infectious diseases

14.6.2.Veterinary

14.6.3.Oncology/rare diseases

14.6.4.Metabolic/autoimmune

14.6.5.Diagnostics/research tools

14.7.Market By Regulatory Stage, Market Estimates and Forecast, USD Million, 2025-2032

14.7.1.Pre-clinical

14.7.2.Clinical (Phase I–III)

14.7.3.Authorized/marketed

14.8.Market By Application, Market Estimates and Forecast, USD Million, 2025-2032

14.8.1.Vaccines

14.8.2.Monoclonal antibodies & antibody fragments

14.8.3.Enzymes

14.8.4.Cytokines/hormones

14.8.5.Diagnostics & research reagents

14.8.6.Nutraceutical/cosmetic actives & specialty proteins

14.9.Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

14.9.1.Biopharma & vaccine manufacturers

14.9.2.Diagnostics & life-science suppliers

14.9.3.Veterinary health companies

14.9.4.Cosmetics/nutraceutical brands

14.9.5.Diagnostics & research reagents

14.9.6.Academic & government research institutes

14.10. Market By Country, Market Estimates and Forecast, USD Million, 2025-2032

14.10.1. US

14.10.2. Canada

14.10.3. Mexico

14.11. Europe

14.11.1. Market By Molecule Type, Market Estimates and Forecast, USD

Million,2025-2032

14.11.1.1. Energy Glycosylated proteins

14.11.1.2. Non-glycosylated proteins

14.11.1.3. VLPs/virus-like particles

14.11.1.4. Fusion proteins/bioconjugates

14.12. Market By Host System Estimates and Forecast, USD Million, 2025-2032

14.12.1. Dicots

14.12.2. Monocots

14.12.3. Plant cell cultures & hairy roots

14.12.4. Algae

14.13. Market By Cultivation, Market Estimates and Forecast, USD Million, 2025-2032

14.13.1. Contained greenhouse/indoor farms

14.13.2. Hydroponic

14.13.3. Open-field

14.13.4. Single-use bioreactors

14.14. Market By Downstream/Processing Complexity, Market Estimates and Forecast, USD

Million, 2025-2032

14.14.1. Crude extracts/partially purified

14.14.2. Purified APIs (cGMP)

14.14.3. Formulated/finished dosage forms

14.15. Market By Therapeutic/Use Area, Market Estimates and Forecast, USD Million,

2025-2032

14.15.1. Infectious diseases

14.15.2. Veterinary

14.15.3. Oncology/rare diseases

14.15.4. Metabolic/autoimmune

14.15.5. Diagnostics/research tools

14.16. Market By Regulatory Stage, Market Estimates and Forecast, USD Million, 2025-2032

14.16.1. Pre-clinical

14.16.2. Clinical (Phase I–III)

14.16.3. Authorized/marketed

14.17. Market By Application, Market Estimates and Forecast, USD Million, 2025-2032

14.17.1. Vaccines

14.17.2. Monoclonal antibodies & antibody fragments

14.17.3. Enzymes

14.17.4. Cytokines/hormones

14.17.5. Diagnostics & research reagents

14.17.6. Nutraceutical/cosmetic actives & specialty proteins

14.18. Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

14.18.1. Biopharma & vaccine manufacturers

14.18.2. Diagnostics & life-science suppliers

14.18.3. Veterinary health companies

14.18.4. Cosmetics/nutraceutical brands

14.18.5. Diagnostics & research reagents

14.18.6. Academic & government research institutes

14.19. Market By Country, Market Estimates and Forecast, USD Million,

14.19.1. Germany

14.19.2. France

14.19.3. U.K

14.19.4. Italy

14.19.5. Spain

14.19.6. Benelux

14.19.7. Russia

14.19.8. Finland

14.19.9. Sweden

14.19.10. Rest Of Europe

14.20. Asia-Pacific

14.20.1. Market By Molecule Type, Market Estimates and Forecast, USD

Million,2025-2032

14.20.1.1. Energy Glycosylated proteins

14.20.1.2. Non-glycosylated proteins

14.20.1.3. VLPs/virus-like particles

14.20.1.4. Fusion proteins/bioconjugates

14.21. Market By Host System Estimates and Forecast, USD Million, 2025-2032

14.21.1. Dicots

14.21.2. Monocots

14.21.3. Plant cell cultures & hairy roots

14.21.4. Algae

14.22. Market By Cultivation, Market Estimates and Forecast, USD Million, 2025-2032

14.22.1. Contained greenhouse/indoor farms

14.22.2. Hydroponic

14.22.3. Open-field

14.22.4. Single-use bioreactors

14.23. Market By Downstream/Processing Complexity, Market Estimates and Forecast, USD

Million, 2025-2032

14.23.1. Crude extracts/partially purified

14.23.2. Purified APIs (cGMP)

14.23.3. Formulated/finished dosage forms

14.24. Market By Therapeutic/Use Area, Market Estimates and Forecast, USD Million,

2025-2032

14.24.1. Infectious diseases

14.24.2. Veterinary

14.24.3. Oncology/rare diseases

14.24.4. Metabolic/autoimmune

14.24.5. Diagnostics/research tools

14.25. Market By Regulatory Stage, Market Estimates and Forecast, USD Million, 2025-2032

14.25.1. Pre-clinical

14.25.2. Clinical (Phase I–III)

14.25.3. Authorized/marketed

14.26. Market By Application, Market Estimates and Forecast, USD Million, 2025-2032

14.26.1. Vaccines

14.26.2. Monoclonal antibodies & antibody fragments

14.26.3. Enzymes

14.26.4. Cytokines/hormones

14.26.5. Diagnostics & research reagents

14.26.6. Nutraceutical/cosmetic actives & specialty proteins

14.27. Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

14.27.1. Biopharma & vaccine manufacturers

14.27.2. Diagnostics & life-science suppliers

14.27.3. Veterinary health companies

14.27.4. Cosmetics/nutraceutical brands

14.27.5. Diagnostics & research reagents

14.27.6. Academic & government research institutes

14.28. Market By Country, Market Estimates and Forecast, USD Million,

14.28.1.1. China

14.28.1.2. India

14.28.1.3. Japan

14.28.1.4. South Korea

14.28.1.5. Indonesia

14.28.1.6. Thailand

14.28.1.7. Vietnam

14.28.1.8. Australia

14.28.1.9. New Zeland

14.28.1.10. Rest of APAC

14.29. Latin America

14.29.1. Market By Molecule Type, Market Estimates and Forecast, USD

Million,2025-2032

14.29.1.1. Energy Glycosylated proteins

14.29.1.2. Non-glycosylated proteins

14.29.1.3. VLPs/virus-like particles

14.29.1.4. Fusion proteins/bioconjugates

14.30. Market By Host System Estimates and Forecast, USD Million, 2025-2032

14.30.1. Dicots

14.30.2. Monocots

14.30.3. Plant cell cultures & hairy roots

14.30.4. Algae

14.31. Market By Cultivation, Market Estimates and Forecast, USD Million, 2025-2032

14.31.1. Contained greenhouse/indoor farms

14.31.2. Hydroponic

14.31.3. Open-field

14.31.4. Single-use bioreactors

14.32. Market By Downstream/Processing Complexity, Market Estimates and Forecast, USD

Million, 2025-2032

14.32.1. Crude extracts/partially purified

14.32.2. Purified APIs (cGMP)

14.32.3. Formulated/finished dosage forms

14.33. Market By Therapeutic/Use Area, Market Estimates and Forecast, USD Million,

2025-2032

14.33.1. Infectious diseases

14.33.2. Veterinary

14.33.3. Oncology/rare diseases

14.33.4. Metabolic/autoimmune

14.33.5. Diagnostics/research tools

14.34. Market By Regulatory Stage, Market Estimates and Forecast, USD Million, 2025-2032

14.34.1. Pre-clinical

14.34.2. Clinical (Phase I–III)

14.34.3. Authorized/marketed

14.35. Market By Application, Market Estimates and Forecast, USD Million, 2025-2032

14.35.1. Vaccines

14.35.2. Monoclonal antibodies & antibody fragments

14.35.3. Enzymes

14.35.4. Cytokines/hormones

14.35.5. Diagnostics & research reagents

14.35.6. Nutraceutical/cosmetic actives & specialty proteins

14.36. Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

14.36.1. Biopharma & vaccine manufacturers

14.36.2. Diagnostics & life-science suppliers

14.36.3. Veterinary health companies

14.36.4. Cosmetics/nutraceutical brands

14.36.5. Diagnostics & research reagents

14.36.6. Academic & government research institutes

14.36.7. Market By Country, Market Estimates and Forecast, USD Million,

14.36.7.1. Brazil

14.36.7.2. Rest of LATAM

14.37. Middle East & Africa

14.37.1. Market By Molecule Type, Market Estimates and Forecast, USD

Million,2025-2032

14.37.1.1. Energy Glycosylated proteins

14.37.1.2. Non-glycosylated proteins

14.37.1.3. VLPs/virus-like particles

14.37.1.4. Fusion proteins/bioconjugates

14.38. Market By Host System Estimates and Forecast, USD Million, 2025-2032

14.38.1. Dicots

14.38.2. Monocots

14.38.3. Plant cell cultures & hairy roots

14.38.4. Algae

14.39. Market By Cultivation, Market Estimates and Forecast, USD Million, 2025-2032

14.39.1. Contained greenhouse/indoor farms

14.39.2. Hydroponic

14.39.3. Open-field

14.39.4. Single-use bioreactors

14.40. Market By Downstream/Processing Complexity, Market Estimates and Forecast, USD

Million, 2025-2032

14.40.1. Crude extracts/partially purified

14.40.2. Purified APIs (cGMP)

14.40.3. Formulated/finished dosage forms

14.41. Market By Therapeutic/Use Area, Market Estimates and Forecast, USD Million,

2025-2032

14.41.1. Infectious diseases

14.41.2. Veterinary

14.41.3. Oncology/rare diseases

14.41.4. Metabolic/autoimmune

14.41.5. Diagnostics/research tools

14.42. Market By Regulatory Stage, Market Estimates and Forecast, USD Million, 2025-2032

14.42.1. Pre-clinical

14.42.2. Clinical (Phase I–III)

14.42.3. Authorized/marketed

14.43. Market By Application, Market Estimates and Forecast, USD Million, 2025-2032

14.43.1. Vaccines

14.43.2. Monoclonal antibodies & antibody fragments

14.43.3. Enzymes

14.43.4. Cytokines/hormones

14.43.5. Diagnostics & research reagents

14.43.6. Nutraceutical/cosmetic actives & specialty proteins

14.44. Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

14.44.1. Biopharma & vaccine manufacturers

14.44.2. Diagnostics & life-science suppliers

14.44.3. Veterinary health companies

14.44.4. Cosmetics/nutraceutical brands

14.44.5. Diagnostics & research reagents

14.44.6. Academic & government research institutes

14.44.6.1. UAE

14.44.6.2. Rest of MEA

Chapter 15. Competitive Landscape

15.1. Market Revenue Share By Manufacturers

15.2. Mergers & Acquisitions

15.3. Competitor’s Positioning

15.4. Strategy Benchmarking

15.5. Vendor Landscape

15.5.1. Distributors

15.5.1.1. North America

15.5.1.2. Europe

15.5.1.3. Asia Pacific

15.5.1.4. Middle East & Africa

15.5.1.5. Latin America

Chapter 16. Company Profiles

16.1. Medicago Inc.

16.1.1. Company Overview

16.1.2. Product & Service Offerings

16.1.3. Strategic Initiatives

16.1.4. Financials

16.1.5. Research Insights

16.2. iBio Inc.

16.2.1. Company Overview

16.2.2. Product & Service Offerings

16.2.3. Strategic Initiatives

16.2.4. Financials

16.2.5. Research Insights

16.3. Kentucky BioProcessing

16.3.1. Company Overview

16.3.2. Product & Service Offerings

16.3.3. Strategic Initiatives

16.3.4. Financials

16.3.5. Research Insights

16.4. Protalix BioTherapeutics

16.4.1. Company Overview

16.4.2. Product & Service Offerings

16.4.3. Strategic Initiatives

16.4.4. Financials

16.4.5. Research Insights

16.5. Ventria Bioscience

16.5.1. Company Overview

16.5.2. Product & Service Offerings

16.5.3. Strategic Initiatives

16.5.4. Financials

16.5.5. Research Insights

16.6. Planet Biotechnology Inc.

16.6.1. Company Overview

16.6.2. Product & Service Offerings

16.6.3. Strategic Initiatives

16.6.4. Financials

16.6.5. Research Insights

16.7. Leaf Expression Systems Ltd.

16.7.1. Company Overview

16.7.2. Product & Service Offerings

16.7.3. Strategic Initiatives

16.7.4. Financials

16.7.5. Conclusion

16.8. ICON Genetics GmbH

16.8.1. Company Overview

16.8.2. Product & Service Offerings

16.8.3. Strategic Initiatives

16.8.4. Financials

16.8.5. Conclusion

16.9. Protalix BioTherapeutics, Inc.

16.9.1. Company Overview

16.9.2. Product & Service Offerings

16.9.3. Strategic Initiatives

16.9.4. Financials

16.9.5. Conclusion

16.10. ORF Genetics

16.10.1. Company Overview

16.10.2. Product & Service Offerings

16.10.3. Strategic Initiatives

16.10.4. Financials

16.10.5. Conclusion

16.11. Miruku

16.11.1. Company Overview

16.11.2. Product & Service Offerings

16.11.3. Strategic Initiatives

16.11.4. Financials

16.11.5. Conclusion

16.12. Mozza

16.12.1. Company Overview

16.12.2. Product & Service Offerings

16.12.3. Strategic Initiatives

16.12.4. Financials

16.12.5. Conclusion

16.13. Nobell Foods

16.13.1. Company Overview

16.13.2. Product & Service Offerings

16.13.3. Strategic Initiatives

16.13.4. Financials

16.13.5. Conclusion

16.14. Bright Biotech

16.14.1. Company Overview

16.14.2. Product & Service Offerings

16.14.3. Strategic Initiatives

16.14.4. Financials

16.14.5. Conclusion

16.15. Tiamat Sciences

16.15.1. Company Overview

16.15.2. Product & Service Offerings

16.15.3. Strategic Initiatives

16.15.4. Financials

16.15.5. Conclusion

16.16. Moolec Science SA.

16.16.1. Company Overview

16.16.2. Product & Service Offerings

16.16.3. Strategic Initiatives

16.16.4. Financials

16.16.5. Conclusion

16.17. PoLoPo

16.17.1. Company Overview

16.17.2. Product & Service Offerings

16.17.3. Strategic Initiatives

16.17.4. Financials

16.17.5. Conclusion

16.18. VelozBio

16.18.1. Company Overview

16.18.2. Product & Service Offerings

16.18.3. Strategic Initiatives

16.18.4. Financials

16.18.5. Conclusion

16.19. Forte Protein

16.19.1. Company Overview

16.19.2. Product & Service Offerings

16.19.3. Strategic Initiatives

16.19.4. Financials

16.19.5. Conclusion

16.20. IngredientWerks

16.20.1. Company Overview

16.20.2. Product & Service Offerings

16.20.3. Strategic Initiatives

16.20.4. Financials

16.20.5. Conclusion

16.21. Elo Life Systems

16.21.1. Company Overview

16.21.2. Product & Service Offerings

16.21.3. Strategic Initiatives

16.21.4. Financials

16.21.5. Conclusion

16.22. Transactiva Srl

16.22.1. Company Overview

16.22.2. Product & Service Offerings

16.22.3. Strategic Initiatives

16.22.4. Financials

16.22.5. Conclusion

16.23. Bright Biotech

16.23.1. Company Overview

16.23.2. Product & Service Offerings

16.23.3. Strategic Initiatives

16.23.4. Financials

16.23.5. Conclusion

16.24. Guardian Biotechnologies (Canada)

16.24.1. Company Overview

16.24.2. Product & Service Offerings

16.24.3. Strategic Initiatives

16.24.4. Financials

16.24.5. Conclusion

16.25. ReaGenics

16.25.1. Company Overview

16.25.2. Product & Service Offerings

16.25.3. Strategic Initiatives

16.25.4. Financials

16.25.5. Conclusion

Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP. has segmented global Functional Shots & Mini Beverages Market on the basis of By Molecule Type, By Host System, By Cultivation, By Downstream/Processing Complexity, By Therapeutic/Use Area, By Regulatory Stage, By Application, By Distribution Channel, By End Use and by region for 2019 to 2032

Global Molecule Type Outlook (Revenue, USD Million 2019-2032)

-

- Glycosylated proteins

-

- Non-glycosylated proteins

-

- VLPs/virus-like particles

-

- Fusion proteins/bioconjugates

Global Host System Outlook (Revenue, USD Million; 2019-2032)

-

- Dicots

-

- Monocots

-

- Plant cell cultures & hairy roots

-

- Algae

Global Cultivation Outlook (Revenue, USD Million; 2019-2032)

-

- Contained greenhouse/indoor farms

-

- Hydroponic

-

- Open-field

-

- Single-use bioreactors

Global Downstream/Processing Complexity Insights (Revenue, USD Million; 2019-2032)

-

- Crude extracts/partially purified

-

- Purified APIs (cGMP)

-

- Formulated/finished dosage forms

Global Therapeutic/Use Area (Revenue, USD Million; 2019-2032)

-

- Infectious diseases

-

- Veterinary

-

- Oncology/rare diseases

-

- Metabolic/autoimmune

-

- Diagnostics/research tools

Global Regulatory Stage (Revenue, USD Million; 2019-2032)

-

- Pre-clinical

-

- Clinical (Phase I–III)

-

- Authorized/marketed

Global Application (Revenue, USD Million; 2019-2032)

-

- Vaccines

-

- Monoclonal antibodies & antibody fragments

-

- Enzymes

-

- Cytokines/hormones

-

- Diagnostics & research reagents

-

- Nutraceutical/cosmetic actives & specialty proteins

Global End Use (Revenue, USD Million; 2019-2032)

-

- Biopharma & vaccine manufacturers

-

- Diagnostics & life-science suppliers

-

- Veterinary health companies

-

- Cosmetics/nutraceutical brands

-

- Diagnostics & research reagents

-

- Academic & government research institutes

- North America

- North America Molecule Type Outlook (Revenue, USD Million 2019-2032)

- Molecule Type & Market Share, 2025–2032

-

- Glycosylated proteins

-

- Non-glycosylated proteins

-

- VLPs/virus-like particles

-

- Fusion proteins/bioconjugates

- North America Host System Outlook (Revenue, USD Million; 2019-2032)

- Host System & Market Share, 2025–2032

-

- Dicots

-

- Monocots

-

- Plant cell cultures & hairy roots

-

- Algae

- North America Cultivation Outlook (Revenue, USD Million; 2019-2032)

- Cultivation & Market Share, 2025–2032

-

- Contained greenhouse/indoor farms

-

- Hydroponic

-

- Open-field

-

- Single-use bioreactors

- North America Downstream/Processing Complexity Outlook (Revenue, USD Million; 2019-2032)

- Downstream/Processing Complexity & Market Share, 2025–2032

-

- Crude extracts/partially purified

-

- Purified APIs (cGMP)

-

- Formulated/finished dosage forms

- North America Therapeutic/Use Outlook (Revenue, USD Million; 2019-2032)

- Therapeutic/Use & Market Share, 2025–2032

-

- Infectious diseases

-

- Veterinary

-

- Oncology/rare diseases

-

- Metabolic/autoimmune

-

- Diagnostics/research tools

- North America Regulatory Stage Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Pre-clinical

-

- Clinical (Phase I–III)

-

- Authorized/marketed

- North America Application Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Vaccines

-

- Monoclonal antibodies & antibody fragments

-

- Enzymes

-

- Cytokines/hormones

-

- Diagnostics & research reagents

-

- Nutraceutical/cosmetic actives & specialty proteins

- North America End Use Outlook (Revenue, USD Million; 2019-2032)

- End Use & Market Share, 2025–2032

-

- Biopharma & vaccine manufacturers

-

- Diagnostics & life-science suppliers

-

- Veterinary health companies

-

- Cosmetics/nutraceutical brands

-

- Diagnostics & research reagents

-

- Academic & government research institutes

- U.S

- U.S Molecule Type Outlook (Revenue, USD Million 2019-2032)

- Molecule Type & Market Share, 2025–2032

-

- Glycosylated proteins

-

- Non-glycosylated proteins

-

- VLPs/virus-like particles

-

- Fusion proteins/bioconjugates

- U.S Host System Outlook (Revenue, USD Million; 2019-2032)

- Host System & Market Share, 2025–2032

-

- Dicots

-

- Monocots

-

- Plant cell cultures & hairy roots

-

- Algae

- U.S Cultivation Outlook (Revenue, USD Million; 2019-2032)

- Cultivation & Market Share, 2025–2032

-

- Contained greenhouse/indoor farms

-

- Hydroponic

-

- Open-field

-

- Single-use bioreactors

- U.S Downstream/Processing Complexity Outlook (Revenue, USD Million; 2019-2032)

- Downstream/Processing Complexity & Market Share, 2025–2032

-

- Crude extracts/partially purified

-

- Purified APIs (cGMP)

-

- Formulated/finished dosage forms

- U.S Therapeutic/Use Outlook (Revenue, USD Million; 2019-2032)

- Therapeutic/Use & Market Share, 2025–2032

-

- Infectious diseases

-

- Veterinary

-

- Oncology/rare diseases

-

- Metabolic/autoimmune

-

- Diagnostics/research tools

- U.S Regulatory Stage Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Pre-clinical

-

- Clinical (Phase I–III)

-

- Authorized/marketed

- U.S Application Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Vaccines

-

- Monoclonal antibodies & antibody fragments

-

- Enzymes

-

- Cytokines/hormones

-

- Diagnostics & research reagents

-

- Nutraceutical/cosmetic actives & specialty proteins

- U.S End Use Outlook (Revenue, USD Million; 2019-2032)

- End Use & Market Share, 2025–2032

-

- Biopharma & vaccine manufacturers

-

- Diagnostics & life-science suppliers

-

- Veterinary health companies

-

- Cosmetics/nutraceutical brands

-

- Diagnostics & research reagents

-

- Academic & government research institutes

- Canada

- Canada Molecule Type Outlook (Revenue, USD Million 2019-2032)

- Molecule Type & Market Share, 2025–2032

-

- Glycosylated proteins

-

- Non-glycosylated proteins

-

- VLPs/virus-like particles

-

- Fusion proteins/bioconjugates

- Canada Host System Outlook (Revenue, USD Million; 2019-2032)

- Host System & Market Share, 2025–2032

-

- Dicots

-

- Monocots

-

- Plant cell cultures & hairy roots

-

- Algae

- Canada Cultivation Outlook (Revenue, USD Million; 2019-2032)

- Cultivation & Market Share, 2025–2032

-

- Contained greenhouse/indoor farms

-

- Hydroponic

-

- Open-field

-

- Single-use bioreactors

- Canada Downstream/Processing Complexity Outlook (Revenue, USD Million; 2019-2032)

- Downstream/Processing Complexity & Market Share, 2025–2032

-

- Crude extracts/partially purified

-

- Purified APIs (cGMP)

-

- Formulated/finished dosage forms

- Canada Therapeutic/Use Outlook (Revenue, USD Million; 2019-2032)

- Therapeutic/Use & Market Share, 2025–2032

-

- Infectious diseases

-

- Veterinary

-

- Oncology/rare diseases

-

- Metabolic/autoimmune

-

- Diagnostics/research tools

- Canada Regulatory Stage Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Pre-clinical

-

- Clinical (Phase I–III)

-

- Authorized/marketed

- Canada Application Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Vaccines

-

- Monoclonal antibodies & antibody fragments

-

- Enzymes

-

- Cytokines/hormones

-

- Diagnostics & research reagents

-

- Nutraceutical/cosmetic actives & specialty proteins

- Canada End Use Outlook (Revenue, USD Million; 2019-2032)

- End Use & Market Share, 2025–2032

-

- Biopharma & vaccine manufacturers

-

- Diagnostics & life-science suppliers

-

- Veterinary health companies

-

- Cosmetics/nutraceutical brands

-

- Diagnostics & research reagents

-

- Academic & government research institutes

- Mexico

- Mexico Molecule Type Outlook (Revenue, USD Million 2019-2032)

- Molecule Type & Market Share, 2025–2032

-

- Glycosylated proteins

-

- Non-glycosylated proteins

-

- VLPs/virus-like particles

-

- Fusion proteins/bioconjugates

- Mexico Host System Outlook (Revenue, USD Million; 2019-2032)

- Host System & Market Share, 2025–2032

-

- Dicots

-

- Monocots

-

- Plant cell cultures & hairy roots

-

- Algae

- Mexico Cultivation Outlook (Revenue, USD Million; 2019-2032)

- Cultivation & Market Share, 2025–2032

-

- Contained greenhouse/indoor farms

-

- Hydroponic

-

- Open-field

-

- Single-use bioreactors

- Mexico Downstream/Processing Complexity Outlook (Revenue, USD Million; 2019-2032)

- Downstream/Processing Complexity & Market Share, 2025–2032

-

- Crude extracts/partially purified

-

- Purified APIs (cGMP)

-

- Formulated/finished dosage forms

- Mexico Therapeutic/Use Outlook (Revenue, USD Million; 2019-2032)

- Therapeutic/Use & Market Share, 2025–2032

-

- Infectious diseases

-

- Veterinary

-

- Oncology/rare diseases

-

- Metabolic/autoimmune

-

- Diagnostics/research tools

- Mexico Regulatory Stage Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Pre-clinical

-

- Clinical (Phase I–III)

-

- Authorized/marketed

- Mexico Application Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Vaccines

-

- Monoclonal antibodies & antibody fragments

-

- Enzymes

-

- Cytokines/hormones

-

- Diagnostics & research reagents

-

- Nutraceutical/cosmetic actives & specialty proteins

- Mexico End Use Outlook (Revenue, USD Million; 2019-2032)

- End Use & Market Share, 2025–2032

-

- Biopharma & vaccine manufacturers

-

- Diagnostics & life-science suppliers

-

- Veterinary health companies

-

- Cosmetics/nutraceutical brands

-

- Diagnostics & research reagents

-

- Academic & government research institutes

- Europe

- Europe Molecule Type Outlook (Revenue, USD Million 2019-2032)

- Molecule Type & Market Share, 2025–2032

-

- Glycosylated proteins

-

- Non-glycosylated proteins

-

- VLPs/virus-like particles

-

- Fusion proteins/bioconjugates

- Europe Host System Outlook (Revenue, USD Million; 2019-2032)

- Host System & Market Share, 2025–2032

-

- Dicots

-

- Monocots

-

- Plant cell cultures & hairy roots

-

- Algae

- Europe Cultivation Outlook (Revenue, USD Million; 2019-2032)

- Cultivation & Market Share, 2025–2032

-

- Contained greenhouse/indoor farms

-

- Hydroponic

-

- Open-field

-

- Single-use bioreactors

- Europe Downstream/Processing Complexity Outlook (Revenue, USD Million; 2019-2032)

- Downstream/Processing Complexity & Market Share, 2025–2032

-

- Crude extracts/partially purified

-

- Purified APIs (cGMP)

-

- Formulated/finished dosage forms

- Europe Therapeutic/Use Outlook (Revenue, USD Million; 2019-2032)

- Therapeutic/Use & Market Share, 2025–2032

-

- Infectious diseases

-

- Veterinary

-

- Oncology/rare diseases

-

- Metabolic/autoimmune

-

- Diagnostics/research tools

- Europe Regulatory Stage Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Pre-clinical

-

- Clinical (Phase I–III)

-

- Authorized/marketed

- Europe Application Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Vaccines

-

- Monoclonal antibodies & antibody fragments

-

- Enzymes

-

- Cytokines/hormones

-

- Diagnostics & research reagents

-

- Nutraceutical/cosmetic actives & specialty proteins

- Europe End Use Outlook (Revenue, USD Million; 2019-2032)

- End Use & Market Share, 2025–2032

-

- Biopharma & vaccine manufacturers

-

- Diagnostics & life-science suppliers

-

- Veterinary health companies

-

- Cosmetics/nutraceutical brands

-

- Diagnostics & research reagents

-

- Academic & government research institutes

- Germany

- Germany Molecule Type Outlook (Revenue, USD Million 2019-2032)

- Molecule Type & Market Share, 2025–2032

-

- Glycosylated proteins

-

- Non-glycosylated proteins

-

- VLPs/virus-like particles

-

- Fusion proteins/bioconjugates

- Germany Host System Outlook (Revenue, USD Million; 2019-2032)

- Host System & Market Share, 2025–2032

-

- Dicots

-

- Monocots

-

- Plant cell cultures & hairy roots

-

- Algae

- Germany Cultivation Outlook (Revenue, USD Million; 2019-2032)

- Cultivation & Market Share, 2025–2032

-

- Contained greenhouse/indoor farms

-

- Hydroponic

-

- Open-field

-

- Single-use bioreactors

- Germany Downstream/Processing Complexity Outlook (Revenue, USD Million; 2019-2032)

- Downstream/Processing Complexity & Market Share, 2025–2032

-

- Crude extracts/partially purified

-

- Purified APIs (cGMP)

-

- Formulated/finished dosage forms

- Germany Therapeutic/Use Outlook (Revenue, USD Million; 2019-2032)

- Therapeutic/Use & Market Share, 2025–2032

-

- Infectious diseases

-

- Veterinary

-

- Oncology/rare diseases

-

- Metabolic/autoimmune

-

- Diagnostics/research tools

- Germany Regulatory Stage Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Pre-clinical

-

- Clinical (Phase I–III)

-

- Authorized/marketed

- Germany Application Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Vaccines

-

- Monoclonal antibodies & antibody fragments

-

- Enzymes

-

- Cytokines/hormones

-

- Diagnostics & research reagents

-

- Nutraceutical/cosmetic actives & specialty proteins

- Germany End Use Outlook (Revenue, USD Million; 2019-2032)

- End Use & Market Share, 2025–2032

-

- Biopharma & vaccine manufacturers

-

- Diagnostics & life-science suppliers

-

- Veterinary health companies

-

- Cosmetics/nutraceutical brands

-

- Diagnostics & research reagents

-

- Academic & government research institutes

- France

- France Molecule Type Outlook (Revenue, USD Million 2019-2032)

- Molecule Type & Market Share, 2025–2032

-

- Glycosylated proteins

-

- Non-glycosylated proteins

-

- VLPs/virus-like particles

-

- Fusion proteins/bioconjugates

- France Host System Outlook (Revenue, USD Million; 2019-2032)

- Host System & Market Share, 2025–2032

-

- Dicots

-

- Monocots

-

- Plant cell cultures & hairy roots

-

- Algae

- France Cultivation Outlook (Revenue, USD Million; 2019-2032)

- Cultivation & Market Share, 2025–2032

-

- Contained greenhouse/indoor farms

-

- Hydroponic

-

- Open-field

-

- Single-use bioreactors

- France Downstream/Processing Complexity Outlook (Revenue, USD Million; 2019-2032)

- Downstream/Processing Complexity & Market Share, 2025–2032

-

- Crude extracts/partially purified

-

- Purified APIs (cGMP)

-

- Formulated/finished dosage forms

- France Therapeutic/Use Outlook (Revenue, USD Million; 2019-2032)

- Therapeutic/Use & Market Share, 2025–2032

-

- Infectious diseases

-

- Veterinary

-

- Oncology/rare diseases

-

- Metabolic/autoimmune

-

- Diagnostics/research tools

- France Regulatory Stage Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Pre-clinical

-

- Clinical (Phase I–III)

-

- Authorized/marketed

- France Application Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Vaccines

-

- Monoclonal antibodies & antibody fragments

-

- Enzymes

-

- Cytokines/hormones

-

- Diagnostics & research reagents

-

- Nutraceutical/cosmetic actives & specialty proteins

- France End Use Outlook (Revenue, USD Million; 2019-2032)

- End Use & Market Share, 2025–2032

-

- Biopharma & vaccine manufacturers

-

- Diagnostics & life-science suppliers

-

- Veterinary health companies

-

- Cosmetics/nutraceutical brands

-

- Diagnostics & research reagents

-

- Academic & government research institutes

- U.K

- U.K Molecule Type Outlook (Revenue, USD Million 2019-2032)

- Molecule Type & Market Share, 2025–2032

-

- Glycosylated proteins

-

- Non-glycosylated proteins

-

- VLPs/virus-like particles

-

- Fusion proteins/bioconjugates

- U.K Host System Outlook (Revenue, USD Million; 2019-2032)

- Host System & Market Share, 2025–2032

-

- Dicots

-

- Monocots

-

- Plant cell cultures & hairy roots

-

- Algae

- U.K Cultivation Outlook (Revenue, USD Million; 2019-2032)

- Cultivation & Market Share, 2025–2032

-

- Contained greenhouse/indoor farms

-

- Hydroponic

-

- Open-field

-

- Single-use bioreactors

- U.K Downstream/Processing Complexity Outlook (Revenue, USD Million; 2019-2032)

- Downstream/Processing Complexity & Market Share, 2025–2032

-

- Crude extracts/partially purified

-

- Purified APIs (cGMP)

-

- Formulated/finished dosage forms

- U.K Therapeutic/Use Outlook (Revenue, USD Million; 2019-2032)

- Therapeutic/Use & Market Share, 2025–2032

-

- Infectious diseases

-

- Veterinary

-

- Oncology/rare diseases

-

- Metabolic/autoimmune

-

- Diagnostics/research tools

- U.K Regulatory Stage Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Pre-clinical

-

- Clinical (Phase I–III)

-

- Authorized/marketed

- U.K Application Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Vaccines

-

- Monoclonal antibodies & antibody fragments

-

- Enzymes

-

- Cytokines/hormones

-

- Diagnostics & research reagents

-

- Nutraceutical/cosmetic actives & specialty proteins

- U.K End Use Outlook (Revenue, USD Million; 2019-2032)

- End Use & Market Share, 2025–2032

-

- Biopharma & vaccine manufacturers

-

- Diagnostics & life-science suppliers

-

- Veterinary health companies

-

- Cosmetics/nutraceutical brands

-

- Diagnostics & research reagents

-

- Academic & government research institutes

- Italy

- Italy Molecule Type Outlook (Revenue, USD Million 2019-2032)

- Molecule Type & Market Share, 2025–2032

-

- Glycosylated proteins

-

- Non-glycosylated proteins

-

- VLPs/virus-like particles

-

- Fusion proteins/bioconjugates

- Italy Host System Outlook (Revenue, USD Million; 2019-2032)

- Host System & Market Share, 2025–2032

-

- Dicots

-

- Monocots

-

- Plant cell cultures & hairy roots

-

- Algae

- Italy Cultivation Outlook (Revenue, USD Million; 2019-2032)

- Cultivation & Market Share, 2025–2032

-

- Contained greenhouse/indoor farms

-

- Hydroponic

-

- Open-field

-

- Single-use bioreactors

- Italy Downstream/Processing Complexity Outlook (Revenue, USD Million; 2019-2032)

- Downstream/Processing Complexity & Market Share, 2025–2032

-

- Crude extracts/partially purified

-

- Purified APIs (cGMP)

-

- Formulated/finished dosage forms

- North America Therapeutic/Use Outlook (Revenue, USD Million; 2019-2032)

- Therapeutic/Use & Market Share, 2025–2032

-

- Infectious diseases

-

- Veterinary

-

- Oncology/rare diseases

-

- Metabolic/autoimmune

-

- Diagnostics/research tools

- Italy Regulatory Stage Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Pre-clinical

-

- Clinical (Phase I–III)

-

- Authorized/marketed

- Italy Application Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Vaccines

-

- Monoclonal antibodies & antibody fragments

-

- Enzymes

-

- Cytokines/hormones

-

- Diagnostics & research reagents

-

- Nutraceutical/cosmetic actives & specialty proteins

- Italy End Use Outlook (Revenue, USD Million; 2019-2032)

- End Use & Market Share, 2025–2032

-

- Biopharma & vaccine manufacturers

-

- Diagnostics & life-science suppliers

-

- Veterinary health companies

-

- Cosmetics/nutraceutical brands

-

- Diagnostics & research reagents

-

- Academic & government research institutes

- Spain

- Spain Molecule Type Outlook (Revenue, USD Million 2019-2032)

- Molecule Type & Market Share, 2025–2032

-

- Glycosylated proteins

-

- Non-glycosylated proteins

-

- VLPs/virus-like particles

-

- Fusion proteins/bioconjugates

- Spain Host System Outlook (Revenue, USD Million; 2019-2032)

- Host System & Market Share, 2025–2032

-

- Dicots

-

- Monocots

-

- Plant cell cultures & hairy roots

-

- Algae

- Spain Cultivation Outlook (Revenue, USD Million; 2019-2032)

- Cultivation & Market Share, 2025–2032

-

- Contained greenhouse/indoor farms

-

- Hydroponic

-

- Open-field

-

- Single-use bioreactors

- Spain Downstream/Processing Complexity Outlook (Revenue, USD Million; 2019-2032)

- Downstream/Processing Complexity & Market Share, 2025–2032

-

- Crude extracts/partially purified

-

- Purified APIs (cGMP)

-

- Formulated/finished dosage forms

- Spain Therapeutic/Use Outlook (Revenue, USD Million; 2019-2032)

- Therapeutic/Use & Market Share, 2025–2032

-

- Infectious diseases

-

- Veterinary

-

- Oncology/rare diseases

-

- Metabolic/autoimmune

-

- Diagnostics/research tools

- Spain Regulatory Stage Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Pre-clinical

-

- Clinical (Phase I–III)

-

- Authorized/marketed

- Spain Application Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Vaccines

-

- Monoclonal antibodies & antibody fragments

-

- Enzymes

-

- Cytokines/hormones

-

- Diagnostics & research reagents

-

- Nutraceutical/cosmetic actives & specialty proteins

- Spain End Use Outlook (Revenue, USD Million; 2019-2032)

- End Use & Market Share, 2025–2032

-

- Biopharma & vaccine manufacturers

-

- Diagnostics & life-science suppliers

-

- Veterinary health companies

-

- Cosmetics/nutraceutical brands

-

- Diagnostics & research reagents

-

- Academic & government research institutes

- Benelux

- Benelux Molecule Type Outlook (Revenue, USD Million 2019-2032)

- Molecule Type & Market Share, 2025–2032

-

- Glycosylated proteins

-

- Non-glycosylated proteins

-

- VLPs/virus-like particles

-

- Fusion proteins/bioconjugates

- Benelux Host System Outlook (Revenue, USD Million; 2019-2032)

- Host System & Market Share, 2025–2032

-

- Dicots

-

- Monocots

-

- Plant cell cultures & hairy roots

-

- Algae

- Benelux Cultivation Outlook (Revenue, USD Million; 2019-2032)

- Cultivation & Market Share, 2025–2032

-

- Contained greenhouse/indoor farms

-

- Hydroponic

-

- Open-field

-

- Single-use bioreactors

- Benelux Downstream/Processing Complexity Outlook (Revenue, USD Million; 2019-2032)

- Downstream/Processing Complexity & Market Share, 2025–2032

-

- Crude extracts/partially purified

-

- Purified APIs (cGMP)

-

- Formulated/finished dosage forms

- Benelux Therapeutic/Use Outlook (Revenue, USD Million; 2019-2032)

- Therapeutic/Use & Market Share, 2025–2032

-

- Infectious diseases

-

- Veterinary

-

- Oncology/rare diseases

-

- Metabolic/autoimmune

-

- Diagnostics/research tools

- Benelux Regulatory Stage Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Pre-clinical

-

- Clinical (Phase I–III)

-

- Authorized/marketed

- Benelux Application Outlook (Revenue, USD Million; 2019-2032)

- Regulatory Stage & Market Share, 2025–2032

-

- Vaccines

-

- Monoclonal antibodies & antibody fragments

-

- Enzymes

-

- Cytokines/hormones

-

- Diagnostics & research reagents

-

- Nutraceutical/cosmetic actives & specialty proteins

- Benelux End Use Outlook (Revenue, USD Million; 2019-2032)

- End Use & Market Share, 2025–2032

-

- Biopharma & vaccine manufacturers

-

- Diagnostics & life-science suppliers

-

- Veterinary health companies

-

- Cosmetics/nutraceutical brands

-

- Diagnostics & research reagents

-

- Academic & government research institutes

- Russia

- Russia Molecule Type Outlook (Revenue, USD Million 2019-2032)

- Molecule Type & Market Share, 2025–2032

-

- Glycosylated proteins

-

- Non-glycosylated proteins

-

- VLPs/virus-like particles

-

- Fusion proteins/bioconjugates

- Russia Host System Outlook (Revenue, USD Million; 2019-2032)

- Host System & Market Share, 2025–2032

-

- Dicots

-

- Monocots

-

- Plant cell cultures & hairy roots

-

- Algae

- Russia Cultivation Outlook (Revenue, USD Million; 2019-2032)

- Cultivation & Market Share, 2025–2032

-