Market Synopsis

The Automotive Electric HVAC Compressor Market size was USD 16,660.11 Million in 2024 and is expected to reach USD 16,660.11 million at a CAGR of 23.46% during the forecast period. The market growth is primarily driven by the increasing adoption of electric and hybrid vehicles, as automakers shift towards sustainable solutions to meet stringent emission regulations and rising consumer demand for energy-efficient technologies. Electric HVAC compressors are replacing traditional belt-driven systems as they offer greater efficiency, reduced energy losses, and the flexibility to operate independently of the engine. Moreover, the rise in demand for improved passenger comfort, coupled with advancements in battery technology, is further supporting the integration of advanced HVAC compressors in both passenger and commercial vehicles.

In addition, the push for eco-friendly solutions and the growing focus on reducing carbon footprints are fueling investments in innovative compressor technologies. Market players are increasingly developing compact, lightweight, and high-performance electric HVAC compressors that enhance vehicle efficiency and extend driving range for EVs. Regional markets such as Asia-Pacific and Europe are at the forefront due to strong government incentives, infrastructure development for EV adoption, and the presence of major automotive OEMs. As the industry evolves, collaborations between compressor manufacturers and automakers are expected to accelerate innovation, shaping the future of climate control systems in next-generation electric mobility.

Global Automotive Electric HVAC Compressor Market (USD Million)

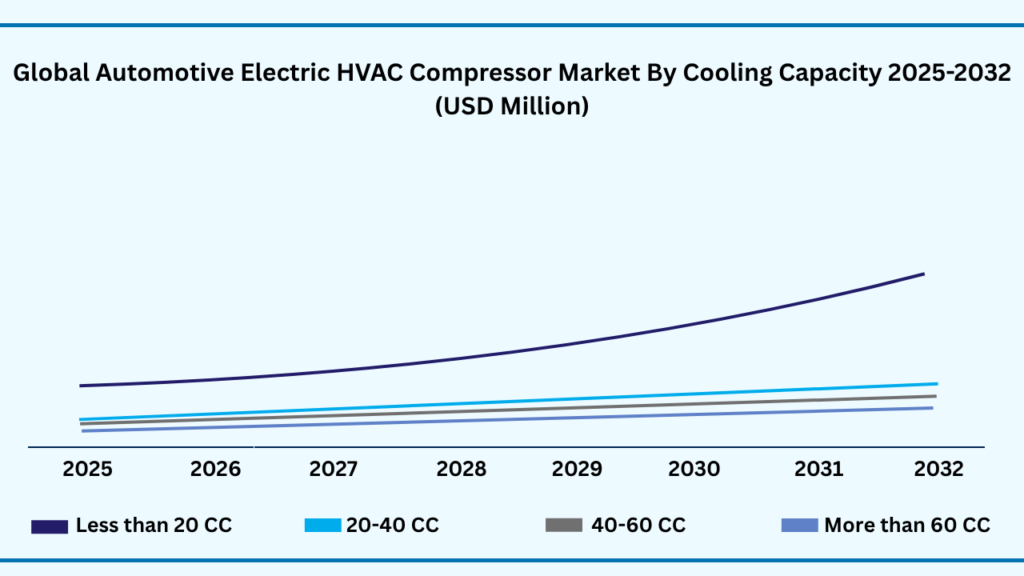

Global Automotive Electric HVAC Compressor Market by Cooling Capacity Insights:

Less than 20 CC segment accounted for market share of share 55.54% in 2024 in the global Automotive Electric HVAC Compressor market.

The Less than 20 CC segment accounted for the largest share of the global Automotive Electric HVAC Compressor market in 2024, representing 55.54 % of total revenues. Less than 20 CC segment is expected to register a CAGR of 23.53% during the forecast year from 2025 to 2032. The Less than 20 CC segment held the largest share of the global Automotive Electric HVAC Compressor market in 2024, leading overall revenues. Its dominance comes from widespread use in passenger cars and compact vehicles, where smaller, energy-efficient compressors are in high demand. Automakers prefer this segment for its lightweight design, affordability, and ability to deliver reliable cooling performance while consuming less energy. With electric vehicles gaining stronger momentum worldwide, these compact compressors have become the preferred choice to achieve the right balance between performance, efficiency, and cost.

Looking ahead, the Less than 20 CC segment is expected to maintain its leading position with steady growth through the forecast period. Its expansion will be supported by the increasing production of electric and hybrid passenger vehicles across major regions, along with stricter environmental regulations that emphasize sustainable and energy-efficient automotive components. Advances in technology, including compact modular designs and variable-speed control, are also expected to accelerate adoption. As consumer expectations rise for comfort and optimized energy use in electric vehicles, the Less than 20 CC segment will continue to shape the future trajectory of the Automotive Electric HVAC Compressor industry.

Global Automotive Electric HVAC Compressor Market by Cooling Capacity (USD Million)

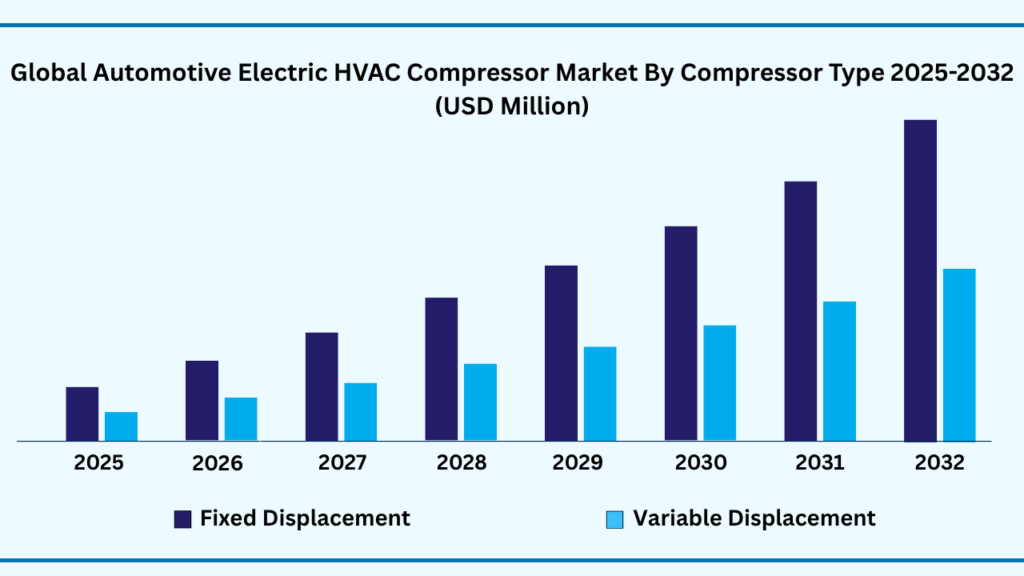

Global Automotive Electric HVAC Compressor Market by Compressor Type Insights:

Fixed Displacement segment accounted for the largest market share of share 41.25% in 2024 in the global Automotive Electric HVAC Compressor market.

Based on the Compressor Type, Fixed Displacement segment held the largest revenue share of 62.33% 2024, and expected to register a CAGR of 23.49%% between 2025 to 2032 and the market is expected to reach USD 55,735.18 by 2032. The Fixed Displacement compressor segment emerged as the leading contributor to revenues in 2024, driven by its widespread adoption in both conventional and electric vehicles. Its dominance is attributed to simpler design, cost-effectiveness, and durability, which make it a preferred choice for many automakers. Fixed displacement compressors deliver consistent performance and are easier to integrate into existing vehicle systems, which has supported their large-scale deployment across global markets. In addition, the segment benefits from strong demand in passenger cars, where reliability and affordability remain key purchasing factors.

Looking ahead, the segment is expected to witness steady growth during the forecast period. Market expansion will be supported by rising vehicle production, particularly in emerging economies, along with the continuous push for energy-efficient and lightweight automotive components. Further, technological improvements aimed at enhancing compressor efficiency and reducing environmental impact will strengthen adoption. As the global automotive industry continues to shift toward electric and hybrid vehicles, fixed displacement compressors will maintain a strong presence due to their proven performance, adaptability, and cost advantage.

Global Automotive Electric HVAC Compressor Market by Compressor Type (USD Million)

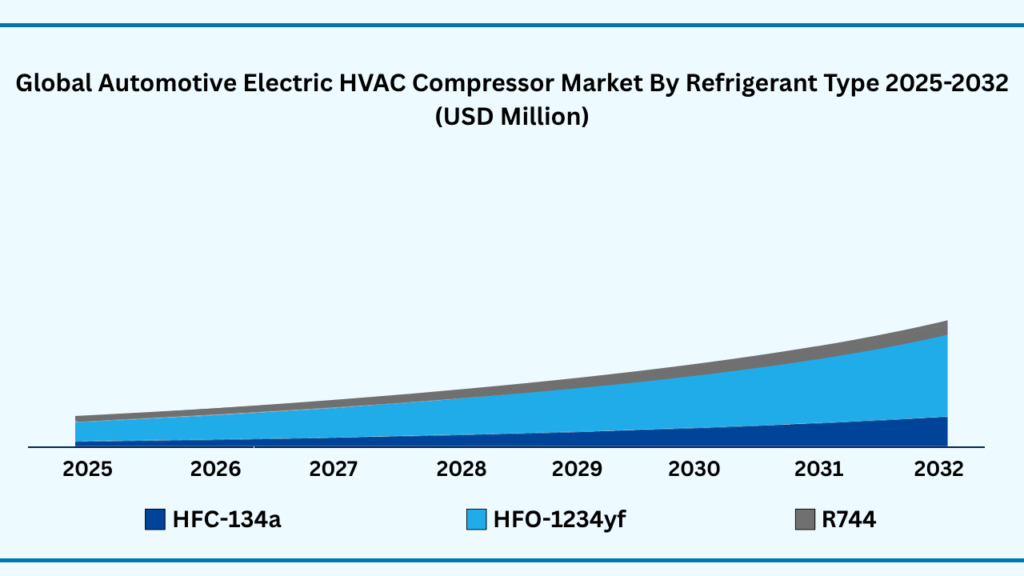

Global Automotive Electric HVAC Compressor Maret by Refrigerant Type Insights:

HFC-134a segment accounted for the largest market share of share 25.32% in 2024 in the global Automotive Electric HVAC Compressor market.

Based on function, Health & Wellness segment held the largest revenue share of 25.32% in the global Automotive Electric HVAC Compressor market in 2024 and expected to register a CAGR of 23.46% from 2025 to 2032 and expected to reach USD 22,604.75 million. The Health & Wellness segment accounted for the largest revenue share of the global Automotive Electric HVAC Compressor market in 2024, reflecting the growing emphasis on passenger comfort and well-being in modern vehicles. Automakers are increasingly integrating advanced HVAC systems that go beyond basic cooling and heating functions to include features like air purification, humidity control, and allergen filtration. This rising consumer demand for healthier cabin environments is particularly prominent in premium vehicles and electric models, where advanced climate control systems are used to enhance the overall driving experience.

Looking ahead, the Health & Wellness segment is expected to expand rapidly during the forecast period, supported by technological innovation and heightened awareness of in-cabin air quality. The development of intelligent HVAC compressors capable of regulating temperature, reducing pollutants, and improving air circulation is driving adoption across multiple vehicle categories. Additionally, regulatory initiatives and consumer expectations for sustainability and safety are further encouraging OEMs to invest in wellness-focused climate control systems. As the automotive industry continues to prioritize passenger-centric features, the Health & Wellness segment will remain a critical driver of growth in the global Automotive Electric HVAC Compressor market.

Global Automotive Electric HVAC Compressor Market by Refrigerant Type (USD Million)

Global Automotive Electric HVAC Compressor Market by Drivetrain Type:

Hybrid Electric Vehicles (HEV) segment accounted for the largest market share of share 38.55% in 2024 in the global Automotive Electric HVAC Compressor market.

Based on Drivetrain Type, Hybrid Electric Vehicles (HEV) segment held the largest revenue share of 38.55% in the global Automotive Electric HVAC Compressor market in 2024 and expected to register a CAGR of 23.28 % from 2025 to 2032 is expected to reach USD 41,781.30 million. The Hybrid Electric Vehicle (HEV) segment captured the largest revenue share of the global Automotive Electric HVAC Compressor market in 2024, owing to the rising adoption of hybrid models as a transition solution between traditional combustion vehicles and fully electric vehicles. HEVs are widely favored because they offer fuel efficiency, reduced emissions, and lower operating costs while maintaining the convenience of conventional fueling. In these vehicles, electric HVAC compressors are increasingly essential as they ensure consistent climate control, even when the engine is off, thereby improving passenger comfort and supporting energy optimization. This has made them a critical component in hybrid drivetrains, especially in regions where hybrid adoption is accelerating faster than pure EVs.

Looking ahead, the HEV segment is expected to witness significant growth throughout the forecast period, driven by regulatory support, expanding hybrid vehicle production, and rising consumer interest in sustainable yet practical mobility solutions. Governments across Asia-Pacific, North America, and Europe continue to promote hybrids as an intermediate step toward full electrification, creating favorable demand for advanced HVAC compressors. Furthermore, advancements in compressor technology, such as lightweight materials, variable-speed operation, and improved cooling efficiency, will enhance performance and driving range in HEVs. With the global automotive industry steadily moving toward electrification, the HEV segment will remain a pivotal driver of the Automotive Electric HVAC Compressor market in the coming years.

Global Automotive Electric HVAC Compressor Market by Drivetrain Type (USD Million)

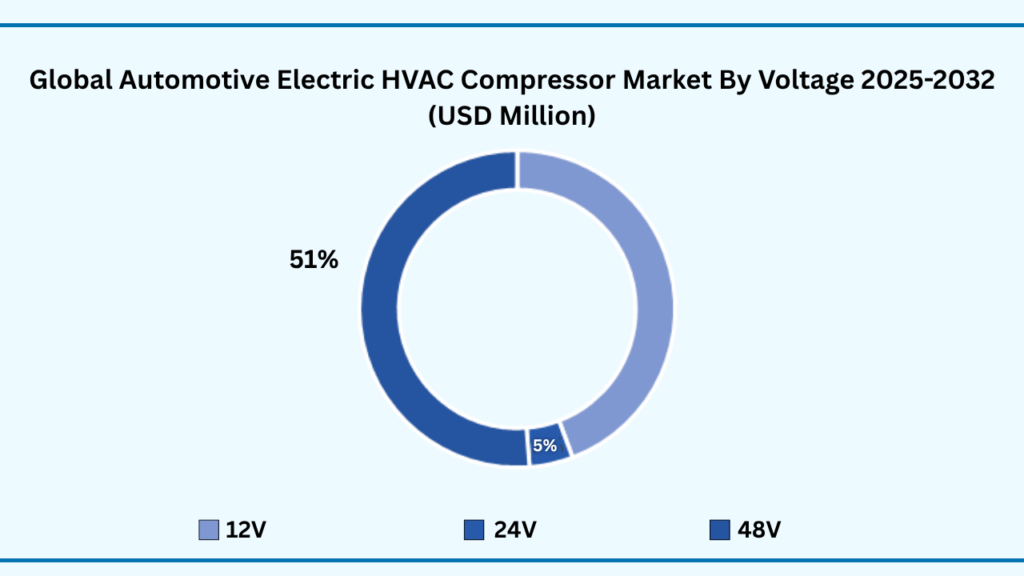

Global Automotive Electric HVAC Compressor Market by Voltage Insights:

48V accounted for the largest market share of share 51.24% in 2024 in the global Automotive Electric HVAC Compressor market.

Based on Voltage segment held the largest revenue share of 51.24% in the global Automotive Electric HVAC Compressor market in 2024 and expected to register a CAGR of 23.57% from 2025 to 2032 and expected to reach USD 46,012.99 million in 2032. The Voltage segment held the largest revenue share in the global Automotive Electric HVAC Compressor market in 2024, reflecting the growing importance of electrical systems in modern vehicles. High-voltage compressors are increasingly preferred in electric and hybrid vehicles due to their efficiency, reliability, and ability to deliver consistent cooling performance independent of engine operation. Automakers are adopting advanced voltage-based HVAC systems to meet rising consumer expectations for energy-efficient, quiet, and high-performance climate control, particularly in premium and electric vehicle models. The ability to optimize power consumption while maintaining cabin comfort has made high-voltage compressors a critical component in the evolving automotive landscape.

Looking ahead, the segment is expected to experience robust growth during the forecast period, driven by the increasing adoption of electric and hybrid vehicles worldwide. Technological advancements in voltage management, energy optimization, and lightweight component design are further enhancing the appeal of these systems. Additionally, stricter regulatory standards on emissions and fuel efficiency are motivating manufacturers to integrate high-voltage compressors to achieve better vehicle performance and sustainability. As automakers continue to focus on electrification and energy-efficient climate control solutions, the voltage segment is poised to remain a key driver of growth in the global Automotive Electric HVAC Compressor market.

Global Automotive Electric HVAC Compressor by Voltage (USD Million)

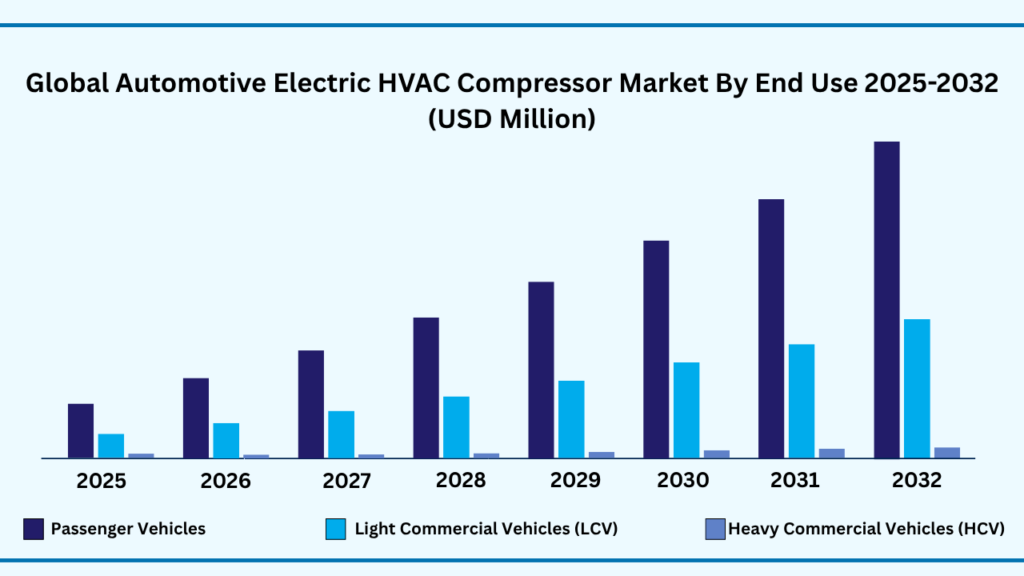

Global Automotive Electric HVAC Compressor Market by End Use Insights:

Passenger Vehicles segment accounted for the largest market share of share of 73.33% in 2024 in the global Automotive Electric HVAC Compressor market.

Based on end use, the Passenger Vehicles segment held the largest revenue share of 73.33% in the global Automotive Electric HVAC Compressor market in 2024 and expected to register a CAGR of 23.43% from 2025 to 2032 and expected to reach USD 65,823.40 million in 2032. The Passenger Vehicles segment dominated the global Automotive Electric HVAC Compressor market in 2024, reflecting the widespread adoption of electric and hybrid vehicles in the passenger car category. This segment’s large share is driven by increasing consumer demand for comfort, energy-efficient climate control, and enhanced in-cabin air quality. Automakers are focusing on integrating advanced electric HVAC compressors in passenger vehicles to ensure reliable cooling and heating performance, even when the engine is off, which is particularly important for hybrid and fully electric models. The rising trend of premium and compact vehicles equipped with sophisticated climate systems further supports the dominance of this segment.

Looking ahead, the Passenger Vehicles segment is expected to maintain strong growth throughout the forecast period. Expansion will be fueled by rising vehicle production in emerging markets, coupled with technological advancements in HVAC compressors, such as variable-speed operation, lightweight designs, and intelligent climate control features. Additionally, growing awareness of passenger comfort, coupled with regulatory pushes for energy efficiency and reduced emissions, is encouraging automakers to adopt advanced electric HVAC solutions. As the global automotive industry continues to prioritize passenger-centric features, this segment will remain the primary driver of growth in the Automotive Electric HVAC Compressor market.

Global Automotive Electric HVAC Compressor by End Use (USD Million)

Global Automotive Electric HVAC Compressor Market by Region Insights:

North America segment accounted for the largest market share of share of 35.32% in 2024 in the global Automotive Electric HVAC Compressor market.

Based on end use, the global Automotive Electric HVAC Compressor market is segmented into Europe, Asia-Pacific, North America, Latin America and Middle East & Africa. Among these, Asia-Pacific region held the largest revenue share of 40.21% in the global Automotive Electric HVAC Compressor market in 2024 and expected to reach USD 36,255.10 million in 2032. The Asia-Pacific region held the largest revenue share of the global Automotive Electric HVAC Compressor market in 2024, reflecting the region’s position as a major hub for automotive production and electric vehicle adoption. Strong demand for passenger and commercial vehicles, combined with rising consumer awareness of energy-efficient and sustainable technologies, has driven the integration of advanced electric HVAC compressors across the region. Countries such as China, Japan, South Korea, and India are witnessing significant growth in hybrid and electric vehicle sales, which further fuels the need for reliable and high-performance climate control systems. Additionally, the presence of leading automotive OEMs and suppliers in the region has accelerated the development and deployment of innovative compressor technologies.

Looking ahead, the Asia-Pacific market is expected to continue its robust growth during the forecast period. Expansion will be supported by favorable government policies promoting electric mobility, incentives for energy-efficient vehicle adoption, and ongoing investments in automotive infrastructure. Technological advancements, including lightweight designs, variable-speed compressors, and intelligent climate control solutions, are further enhancing market adoption. As the automotive landscape in Asia-Pacific evolves toward electrification and sustainability, the region is poised to remain the largest and most influential market for automotive electric HVAC compressors globally.

Global Automotive Electric HVAC Compressor Market by Region (USD Million)

Major Companies and Competitive Landscape

The global Automotive Electric HVAC Compressor market is highly competitive and fragmented, with leading automotive OEMs, component suppliers, and emerging technology providers striving to capture market share. Key players are adopting strategies such as mergers and acquisitions, strategic partnerships with vehicle manufacturers, and collaborations with EV technology firms to expand their presence in both mature and emerging markets. Many companies are also investing heavily in product innovation, developing high-efficiency, lightweight, and low-noise compressors with advanced features such as variable-speed operation, smart climate control, and enhanced energy optimization to meet evolving consumer and regulatory demands.

Additionally, market players are increasingly emphasizing sustainability, energy efficiency, and compliance with global emission and safety standards. Efforts include designing compressors compatible with electric and hybrid drivetrains, integrating eco-friendly refrigerants, and improving overall system efficiency to reduce vehicle energy consumption. With growing consumer expectations for comfort, performance, and environmental responsibility, manufacturers are focusing on delivering reliable, high-performance HVAC solutions. The combination of technological innovation, strategic partnerships, regulatory support, and the rapid expansion of EV and hybrid vehicle markets is expected to drive sustained growth and intensify competition across the global Automotive Electric HVAC Compressor market.

Some of the leading companies profiled in the global cultured meat market report include:

- Denso Corporation

- Sanden Holdings / Sanden Corporation

- Hanon Systems

- MAHLE GmbH

- Valeo SA

- Toyota Industries Corporation

- Continental AG

- Keihin Corporation

- Calsonic Kansei Corporation

- Subros Limited

- Robert Bosch GmbH

- BorgWarner Inc.

- Mitsubishi Heavy Industries Ltd.

- Nidec

- Johnson Electric Holdings Limited

- Shanghai Highly (Group) Co., Ltd

- Michigan Automotive Compressor, Inc.

- Brose Fahrzeugteile SE & Co. KGE

- Aptiv plc

- Sensata Technologies

Strategic Development

1. Hanon Systems Expands Manufacturing Capability in Canada (2024)

In October 2024, Hanon Systems announced a USD155 million investment to establish a new electric compressor manufacturing facility in Woodbridge, Ontario. This 26,400-square-meter plant is expected to commence production in the first half of 2025, with an annual capacity of up to 900,000 units. The expansion aims to reinforce Hanon Systems’ competitiveness by increasing its production of key electric vehicle components in North America.

2. Denso Corporation Develops High-Capacity Electric Compressor (2023)

In 2023, Denso Corporation unveiled a new electric compressor that offers a 20% higher cooling capacity compared to conventional models. This development underscores Denso’s commitment to enhancing the efficiency and performance of HVAC systems in electric vehicles, aligning with the growing demand for energy-efficient and environmentally sustainable solutions in the automotive industry

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 16,660.11 Million |

| CAGR (2024–2032) | 23.46% |

| Revenue forecast to 2033 | USD 2,728.63 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million, Volume Kiloton and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Cooling Capacity, By Compressor Type, By Refrigerant Type, By Drivetrain Type, By Voltage, By End Use, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, Rest of MEA |

| Key companies profiled | “Denso Corporation, Sanden Holdings / Sanden Corporation, Hanon Systems, MAHLE GmbH, Valeo SA, Toyota Industries Corporation, Continental AG, Keihin Corporation, Calsonic Kansei Corporation, Subros Limited, Robert Bosch GmbH, BorgWarner Inc., Mitsubishi Heavy Industries Ltd., Nidec, Johnson Electric Holdings Limited, Shanghai Highly (Group) Co., Ltd, Michigan Automotive Compressor, Inc., Brose Fahrzeugteile SE & Co. KGE, Aptiv plc, Sensata Technologies” |

| Customization scope | 10 hours of free customization and expert consultation |

Some Key Questions the Report Will Answer

- What is the expected revenue Compound Annual Growth Rate (CAGR) of the global Automotive Electric HVAC Compressor market over the forecast period (2025–2032)?

- The global Automotive Electric HVAC Compressor market revenue is expected to register a Compound Annual Growth Rate (CAGR) of 23.46% during the forecast period.

- What was the size of the global Automotive Electric HVAC Compressor in 2024?

- The global Automotive Electric HVAC Compressor market size was USD 16,660.11 Million in 2024.

- Which factors are expected to drive the global Automotive Electric HVAC Compressor market growth?

- The global Automotive Electric HVAC Compressor market is expected to grow rapidly, driven by the rising adoption of electric and hybrid vehicles, which require energy-efficient and independent climate control systems. Increasing consumer demand for enhanced passenger comfort, air quality, and smart cabin features, coupled with stringent government regulations on emissions and fuel efficiency, is pushing automakers to integrate advanced electric compressors. Additionally, technological advancements such as lightweight designs, variable-speed operation, and eco-friendly refrigerants are further supporting market growth, while the expansion of EV infrastructure and incentives in key regions like Asia-Pacific, Europe, and North America continue to fuel demand for innovative HVAC solutions.

- Which was the leading segment in the global Automotive Electric HVAC Compressor market in terms of Cooling Capacity in 2024?

- Less than 20 CC segment was leading in the Automotive Electric HVAC Compressor market on the basis of Cooling Capacity in 2024.

- What are some restraints for revenue growth of the global Automotive Electric HVAC Compressor market?

- The global Automotive Electric HVAC Compressor market faces several restraints that could hinder revenue growth. High initial costs and complex integration requirements for electric compressors compared to conventional systems pose challenges for automakers, particularly in cost-sensitive markets. Limited awareness and adoption of advanced HVAC technologies in developing regions, coupled with the dependence on consistent power supply and battery performance in electric and hybrid vehicles, can also restrict market expansion. Additionally, fluctuations in raw material prices and supply chain disruptions may impact production costs and availability, while stringent regulatory compliance and certification processes can slow down product launches and innovation.

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of Automotive Electric HVAC Compressor Market

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1.Primary

2.1.2.Secondary

2.1.3.Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1.Market value

2.3.2.Market volume

2.3.3.Exchange rate

2.3.4.Price

2.3.5.Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2025–2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10. Formulation & manufacturing

4.11. Distribution & retail

4.12. Import-export analysis

4.13. Brand comparative analysis

4.14. Technological advancements

4.15. Porter’s five force

4.15.1. Threat of new entrants

4.15.1.1. Capital requirment

4.15.1.2. Product knowledge

4.15.1.3. Technical knowledge

4.15.1.4. Customer relation

4.15.1.5. Access to appliation and technology

4.15.2. Threat of substitutes

4.15.2.1. Cost

4.15.2.2. Performance

4.15.2.3. Availability

4.15.2.4. Technical knowledge

4.15.2.5. Durability

4.15.3. Bargainning power of buyers

4.15.3.1. Numbers of buyers relative to suppliers

4.15.3.2. Product differentiation

4.15.3.3. Threat of forward integration

4.15.3.4. Buyers volume

4.15.4. Bargainning power of suppliers

4.15.4.1. Suppliers concentration

4.15.4.2. Buyers switching cost to other suppliers

4.15.4.3. Threat of backward integration

4.15.5. Bargainning power of suppliers

4.15.5.1. Industry concentration

4.15.5.2. Industry growth rate

4.15.5.3. Product differentiation

4.16. Patent analysis

4.17. Regulation coverage

4.18. Pricing analysis

4.19. Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1.Growth in Electric & Hybrid Vehicles

5.1.2.Stringent Emission Regulations

5.1.3.Consumer Demand for Comfort

5.2. Restraints

5.2.1.High Initial Cost

5.2.2.Complex Integration

5.3. Opportunities

5.3.1.Thermal Management in EV Batteries

5.3.2.Adoption in Commercial Vehicles

5.3.3.Advancements in Energy-Efficient Compressors

5.4. Threat

5.4.1.Price Pressure & Intense Competition

5.4.2.Supply Chain Disruptions

Chapter 6. Automotive Electric HVAC Compressor Market By Cooling Capacity Insights & Trends, Revenue (USD Million),

6.1. Cooling Capacity Dynamics & Market Share, 2025–2032

6.1.1.1. Less than 20 CC

6.1.1.2. 20-40 CC

6.1.1.3. 40-60 CC

6.1.1.4. More than 60 CC

Chapter 7. Automotive Electric HVAC Compressor Market By Compressor Type Insights & Trends, Revenue (USD Million),

7.1. Compressor Type Dynamics & Market Share, 2025–2032

7.1.1. Fixed Displacement

7.1.2. Variable Displacement

Chapter 8. Automotive Electric HVAC Compressor Market By Refrigerant Type Insights & Trends, Revenue (USD Million),

8.1. Refrigerant Type Dynamics & Market Share, 2025–2032

8.1.1. HFC-134a

8.1.2. HFO-1234yf

8.1.3. CO₂

Chapter 9. Automotive Electric HVAC Compressor Market By Drivetrain Type Insights & Trends, Revenue (USD Million),

9.1. Drivetrain Type Dynamics & Market Share, 2025–2032

9.1.1. Battery Electric Vehicles (BEV)

9.1.2. Plug-in Hybrid Electric Vehicles (PHEV)

9.1.3. Hybrid Electric Vehicles (HEV)

Chapter 10. Automotive Electric HVAC Compressor Market By Voltage Insights & Trends, Revenue (USD Million),

10.1. Voltage & Market Share, 2025–2032

10.1.1.12V

10.1.2.24V

10.1.3.48V

Chapter 11. Automotive Electric HVAC Compressor Market By End Use Insights & Trends, Revenue (USD Million),

11.1. End Use Dynamics & Market Share, 2025–2032

11.1.1.Passenger Vehicles;

11.1.2.Light Commercial Vehicles (LCV)

11.1.3.Heavy Commercial Vehicles (HCV)

Chapter 12. Automotive Electric HVAC Compressor Market Regional Outlook

12.1.Automotive Electric HVAC Compressor Share By Region, 2025–2032

12.2.North America

12.2.1.Market By Cooling Capacity, Market Estimates and Forecast, USD Million, 2025-2032

12.2.1.1. Less than 20 CC

12.2.1.2. 20-40 CC

12.2.1.3. 40-60 CC

12.2.1.4. More than 60 CC

12.2.2. Market By Packaging Compressor Type Estimates and Forecast, USD Million, 2025-2032

12.2.2.1. Fixed Displacement

12.2.2.2. Variable Displacement

12.3.Market By Refrigerant Type, Market Estimates and Forecast, USD Million, 2025-2032

12.3.1.HFC-134a

12.3.2.HFO-1234yf

12.3.3.CO₂

12.4.Market By Drivetrain Type, Market Estimates and Forecast, USD Million, 2025-2032

12.4.1.Battery Electric Vehicles (BEV)

12.4.2.Plug-in Hybrid Electric Vehicles (PHEV)

12.4.3.Hybrid Electric Vehicles (HEV)

12.5.Market By Voltage, Market Estimates and Forecast, USD Million, 2025-2032

12.5.1.12V

12.5.2.24V;

12.5.3.48V

12.6.Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

12.6.1.Passenger Vehicles;

12.6.2.Light Commercial Vehicles (LCV)

12.6.3.Heavy Commercial Vehicles (HCV)

12.7.Market By Country, Market Estimates and Forecast, USD Million, 2025-2032

12.7.1.US

12.7.2.Canada

12.7.3.Mexico

12.8. Europe

12.8.1. Market By Cooling Capacity, Market Estimates and Forecast, USD Million,2025-2032

12.8.1.1. Less than 20 CC

12.8.1.2. 20-40 CC

12.8.1.3. 40-60 CC

12.8.1.4. More than 60 CC

12.8.2. Market By Packaging Compressor Type Estimates and Forecast, USD Million, 2025-2032

12.8.2.1. Fixed Displacement

12.8.2.2. Variable Displacement

12.9.Market By Refrigerant Type, Market Estimates and Forecast, USD Million, 2025-2032

12.9.1. HFC-134a

12.9.2. HFO-1234yf

12.9.3. CO₂

12.10. Market By Drivetrain Type, Market Estimates and Forecast, USD Million, 2025-2032

12.10.1. Battery Electric Vehicles (BEV)

12.10.2. Plug-in Hybrid Electric Vehicles (PHEV)

12.10.3. Hybrid Electric Vehicles (HEV)

12.11. Market By Voltage, Market Estimates and Forecast, USD Million, 2025-2032

12.11.1. 12V

12.11.2. 24V;

12.11.3. 48V

12.12. Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

12.12.1. Passenger Vehicles;

12.12.2. Light Commercial Vehicles (LCV)

12.12.3. Heavy Commercial Vehicles (HCV)

12.13. Market By Country, Market Estimates and Forecast, USD Million,

12.13.1. Germany

12.13.2. France

12.13.3. U.K

12.13.4. Italy

12.13.5. Spain

12.13.6. Benelux

12.13.7. Russia

12.13.8. Finland

12.13.9. Sweden

12.13.10. Rest Of Europe

12.14. Asia-Pacific

12.14.1. Market By Cooling Capacity, Market Estimates and Forecast, USD Million,2025-2032

12.14.1.1. Less than 20 CC

12.14.1.2. 20-40 CC

12.14.1.3. 40-60 CC

12.14.1.4. More than 60 CC

12.14.2. Market By Packaging Compressor Type Estimates and Forecast, USD Million, 2025-2032

12.14.2.1. Fixed Displacement

12.14.2.2. Variable Displacement

12.15. Market By Refrigerant Type, Market Estimates and Forecast, USD Million, 2025-2032

12.15.1. HFC-134a

12.15.2. HFO-1234yf

12.15.3. CO₂

12.16. Market By Drivetrain Type, Market Estimates and Forecast, USD Million, 2025-2032

12.16.1. Battery Electric Vehicles (BEV)

12.16.2. Plug-in Hybrid Electric Vehicles (PHEV)

12.16.3. Hybrid Electric Vehicles (HEV)

12.17. Market By Voltage, Market Estimates and Forecast, USD Million, 2025-2032

12.17.1. 12V

12.17.2. 24V;

12.17.3. 48V

12.18. Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

12.18.1. Passenger Vehicles;

12.18.2. Light Commercial Vehicles (LCV)

12.18.3. Heavy Commercial Vehicles (HCV)

12.19. Market By Country, Market Estimates and Forecast, USD Million,

12.19.1.1. China

12.19.1.2. India

12.19.1.3. Japan

12.19.1.4. South Korea

12.19.1.5. Indonesia

12.19.1.6. Thailand

12.19.1.7. Vietnam

12.19.1.8. Australia

12.19.1.9. New Zeland

12.19.1.10. Rest of APAC

12.20. Latin America

12.20.1. Market By Cooling Capacity, Market Estimates and Forecast, USD Million,2025-2032

12.20.1.1. Less than 20 CC

12.20.1.2. 20-40 CC

12.20.1.3. 40-60 CC

12.20.1.4. More than 60 CC

12.20.2. Market By Packaging Compressor Type Estimates and Forecast, USD Million, 2025-2032

12.20.2.1. Fixed Displacement

12.20.2.2. Variable Displacement

12.21. Market By Refrigerant Type, Market Estimates and Forecast, USD Million, 2025-2032

12.21.1. HFC-134a

12.21.2. HFO-1234yf

12.21.3. CO₂

12.22. Market By Drivetrain Type, Market Estimates and Forecast, USD Million, 2025-2032

12.22.1. Battery Electric Vehicles (BEV)

12.22.2. Plug-in Hybrid Electric Vehicles (PHEV)

12.22.3. Hybrid Electric Vehicles (HEV)

12.23. Market By Voltage, Market Estimates and Forecast, USD Million, 2025-2032

12.23.1. 12V

12.23.2. 24V;

12.23.3. 48V

12.24. Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

12.24.1. Passenger Vehicles;

12.24.2. Light Commercial Vehicles (LCV)

12.24.3. Heavy Commercial Vehicles (HCV)

12.24.4. Market By Country, Market Estimates and Forecast, USD Million,

12.24.4.1. Brazil

12.24.4.2. Rest of LATAM

12.25. Middle East & Africa

12.25.1. Market By Cooling Capacity, Market Estimates and Forecast, USD Million, 2025-2032

12.25.1.1. Less than 20 CC

12.25.1.2. 20-40 CC

12.25.1.3. 40-60 CC

12.25.1.4. More than 60 CC

12.25.2. Market By Packaging Compressor Type Estimates and Forecast, USD Million, 2025-2032

12.25.2.1. Fixed Displacement

12.25.2.2. Variable Displacement

12.26. Market By Refrigerant Type, Market Estimates and Forecast, USD Million, 2025-2032

12.26.1. HFC-134a

12.26.2. HFO-1234yf

12.26.3. CO₂

12.27. Market By Drivetrain Type, Market Estimates and Forecast, USD Million, 2025-2032

12.27.1. Battery Electric Vehicles (BEV)

12.27.2. Plug-in Hybrid Electric Vehicles (PHEV)

12.27.3. Hybrid Electric Vehicles (HEV)

12.28. Market By Voltage, Market Estimates and Forecast, USD Million, 2025-2032

12.28.1. 12V

12.28.2. 24V;

12.28.3. 48V

12.29. Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

12.29.1. Passenger Vehicles;

12.29.2. Light Commercial Vehicles (LCV)

12.29.3. Heavy Commercial Vehicles (HCV)

12.29.4. Market By Country, Market Estimates and Forecast, USD Million,

12.29.4.1. Saudi Arabia

12.29.4.2. Rest of MEA

Chapter 13. Competitive Landscape

13.1. Market Revenue Share By Manufacturers

13.2. Mergers & Acquisitions

13.3. Competitor’s Positioning

13.4. Strategy Benchmarking

13.5. Vendor Landscape

13.5.1. Distributors

13.5.1.1. North America

13.5.1.2. Europe

13.5.1.3. Asia Pacific

13.5.1.4. Middle East & Africa

13.5.1.5. Latin America

Chapter 14. Company Profiles

14.1. Denso Corporation

14.1.1. Company Overview

14.1.2. Product & Service Offerings

14.1.3. Strategic Initiatives

14.1.4. Financials

14.1.5. Emergen Research Insights

14.2. Sanden Holdings / Sanden Corporation

14.2.1. Company Overview

14.2.2. Product & Service Offerings

14.2.3. Strategic Initiatives

14.2.4. Financials

14.2.5. Emergen Research Insights

14.3. Hanon Systems

14.3.1. Company Overview

14.3.2. Product & Service Offerings

14.3.3. Strategic Initiatives

14.3.4. Financials

14.3.5. Emergen Research Insights

14.4. MAHLE GmbH

14.4.1. Company Overview

14.4.2. Product & Service Offerings

14.4.3. Strategic Initiatives

14.4.4. Financials

14.4.5. Emergen Research Insights

14.5. Valeo SA

14.5.1. Company Overview

14.5.2. Product & Service Offerings

14.5.3. Strategic Initiatives

14.5.4. Financials

14.5.5. Emergen Research Insights

14.6. Toyota Industries Corporation

14.6.1. Company Overview

14.6.2. Product & Service Offerings

14.6.3. Strategic Initiatives

14.6.4. Financials

14.6.5. Emergen Research Insights

14.7. Continental AG

14.7.1. Company Overview

14.7.2. Product & Service Offerings

14.7.3. Strategic Initiatives

14.7.4. Financials

14.7.5. Conclusion

14.8. Keihin Corporation

14.8.1. Company Overview

14.8.2. Product & Service Offerings

14.8.3. Strategic Initiatives

14.8.4. Financials

14.8.5. Conclusion

14.9. Calsonic Kansei Corporation

14.9.1. Company Overview

14.9.2. Product & Service Offerings

14.9.3. Strategic Initiatives

14.9.4. Financials

14.9.5. Conclusion

14.10. Subros LimitedThe

14.10.1. Company Overview

14.10.2. Product & Service Offerings

14.10.3. Strategic Initiatives

14.10.4. Financials

14.10.5. Conclusion

14.11. Robert Bosch GmbH

14.11.1. Company Overview

14.11.2. Product & Service Offerings

14.11.3. Strategic Initiatives

14.11.4. Financials

14.11.5. Conclusion

14.12. BorgWarner Inc.

14.12.1. Company Overview

14.12.2. Product & Service Offerings

14.12.3. Strategic Initiatives

14.12.4. Financials

14.12.5. Conclusion

14.13. Mitsubishi Heavy Industries Ltd.

14.13.1. Company Overview

14.13.2. Product & Service Offerings

14.13.3. Strategic Initiatives

14.13.4. Financials

14.13.5. Conclusion

14.14. Nidec

14.14.1. Company Overview

14.14.2. Product & Service Offerings

14.14.3. Strategic Initiatives

14.14.4. Financials

14.14.5. Conclusion

14.15. Johnson Electric Holdings Limited

14.15.1. Company Overview

14.15.2. Product & Service Offerings

14.15.3. Strategic Initiatives

14.15.4. Financials

14.15.5. Conclusion

14.16. Shanghai Highly (Group) Co., Ltd

14.16.1. Company Overview

14.16.2. Product & Service Offerings

14.16.3. Strategic Initiatives

14.16.4. Financials

14.16.5. Conclusion

14.17. Michigan Automotive Compressor, Inc.

14.17.1. Company Overview

14.17.2. Product & Service Offerings

14.17.3. Strategic Initiatives

14.17.4. Financials

14.17.5. Conclusion

14.18. Brose Fahrzeugteile SE & Co. KGE

14.18.1. Company Overview

14.18.2. Product & Service Offerings

14.18.3. Strategic Initiatives

14.18.4. Financials

14.18.5. Conclusion

14.19. Aptiv plc

14.19.1. Company Overview

14.19.2. Product & Service Offerings

14.19.3. Strategic Initiatives

14.19.4. Financials

14.19.5. Conclusion

14.20. Sensata Technologies

14.20.1. Company Overview

14.20.2. Product & Service Offerings

14.20.3. Strategic Initiatives

14.20.4. Financials

14.20.5. Conclusion

Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP. has segmented global Automotive Electric HVAC Compressor Market on the basis of By Cooling Capacity, By Compressor Type, By Refrigerant Type, By Drivetrain Type, By Voltage, By End Use and by region for 2019 to 2032

Global Automotive Electric HVAC Compressor Market By Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

-

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

Global Automotive Electric HVAC Compressor Market, By Compressor Type Outlook (Revenue, USD Million; 2019-2032)

-

- Fixed Displacement

- Variable Displacement

Global Automotive Electric HVAC Compressor Market By Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

-

- HFC-134a

- HFO-1234yf

- CO₂

Global Automotive Electric HVAC Compressor By Drivetrain Type Market (Revenue, USD Million; 2019-2032)

-

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

Global Automotive Electric HVAC Compressor Market By Voltage (Revenue, USD Million; 2019-2032)

-

- 2V

- 24V

- 48V

Global Automotive Electric HVAC Compressor Market By End Use (Revenue, USD Million; 2019-2032)

-

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- North America

- North America Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- North America Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- North America Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- North America Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- North America Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- North America End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- North America Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- U.S

- U.S Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- U.S Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- U.S Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- U.S Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- U.S Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- U.S End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- U.S Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Canada

- Canada Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Canada Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Canada Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Canada Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Canada Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Canada End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Canada Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Mexico

- Mexico Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Mexico Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Mexico Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Mexico Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Mexico Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Mexico End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Mexico Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Europe

- Europe Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Europe Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Europe Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Europe Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Europe Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Europe End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Europe Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Germany

- Germany Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Germany Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Germany Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Germany Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Germany Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Germany End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Germany Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- France

- France Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- France Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- France Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- France Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- France Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- France End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- France Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- U.K

- U.K Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- U.K Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- U.K Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- U.K Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- U.K Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- U.K End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- U.K Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Italy

- Italy Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Italy Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Italy Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Italy Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Italy Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Italy End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Italy Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Spain

- Spain Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Spain Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Spain Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Spain Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Spain Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Spain End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Spain Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Benelux

- Benelux Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Benelux Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Benelux Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Benelux Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Benelux Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Benelux End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Benelux Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Russia

- Russia Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Russia Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Russia Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Russia Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Russia Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Russia End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Russia Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Finland

- Finland Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Finland Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Finland Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Finland Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Finland Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Finland End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Finland Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Sweden

- Sweden Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Sweden Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Sweden Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Sweden Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Sweden Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Sweden End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Sweden Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Rest of Europe

- Rest of Europe Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Rest of Europe Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Rest of Europe Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Rest of Europe Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Rest of Europe Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Rest of Europe End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Rest of Europe Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- Asia-Pacific

- Asia-Pacific Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Asia-Pacific Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Asia-Pacific Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Asia-Pacific Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Asia-Pacific Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Asia-Pacific End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Asia-Pacific Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- China

- China Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- China Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- China Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- China Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- China Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- China End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- China Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- India

- India Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- India Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- India Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- India Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- India Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- India End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- India Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- Japan

- Japan Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Japan Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Japan Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Japan Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Japan Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Japan End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Japan Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- Indonesia

- Indonesia Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Indonesia Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Indonesia Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Indonesia Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Indonesia Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Indonesia End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Indonesia Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- Thailand

- Thailand Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Thailand Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Thailand Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Thailand Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Thailand Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Thailand End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Thailand Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- Vietnam

- Vietnam Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Vietnam Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Vietnam Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Vietnam Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Vietnam Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Vietnam End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Vietnam Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- Australia

- Australia Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Australia Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Australia Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Australia Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Australia Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Australia End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Australia Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- New Zealand

- New Zealand Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- New Zealand Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- New Zealand Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- New Zealand Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- New Zealand Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- New Zealand End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- New Zealand Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- Asia-Pacific

- Asia-Pacific Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Asia-Pacific Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Asia-Pacific Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Asia-Pacific Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Asia-Pacific Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Asia-Pacific End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Asia-Pacific Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- Middle East & Africa

- Middle East & Africa Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Middle East & Africa Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Middle East & Africa Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Middle East & Africa Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Middle East & Africa Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Middle East & Africa End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Middle East & Africa Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- Saudi Arabia

- Saudi Arabia Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Saudi Arabia Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Saudi Arabia Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Saudi Arabia Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Saudi Arabia Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Saudi Arabia End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Saudi Arabia Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- Rest of Middle East & Africa

- Rest of Middle East & Africa Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Rest of Middle East & Africa Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Rest of Middle East & Africa Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Rest of Middle East & Africa Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Rest of Middle East & Africa Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Rest of Middle East & Africa End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Rest of Middle East & Africa Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- Latin America

- Latin America Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Latin America Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Latin America Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Latin America Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Latin America Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Latin America End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Latin America Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- Brazil

- Brazil Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Brazil Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Brazil Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Brazil Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Brazil Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Brazil End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Brazil Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

Heavy Commercial Vehicles (HCV)

- Rest of Latin America

- Rest of Latin America Cooling Capacity Outlook (Revenue, USD Million 2019-2032)

- Less than 20 CC

- 20-40 CC

- 40-60 CC

- More than 60 CC

- Rest of Latin America Compressor Type Outlook (Revenue, USD Million; 2019-2032)

- Fixed Displacement

- Variable Displacement

- Rest of Latin America Refrigerant Type Outlook (Revenue, USD Million; 2019-2032)

- HFC-134a

- HFO-1234yf

- CO₂

- Rest of Latin America Drivetrain Type Outlook (Revenue, USD Million; 2019-2032)

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Rest of Latin America Voltage Outlook (Revenue, USD Million; 2019-2032)

- 2V

- 24V

- 48V

- Rest of Latin America End Use Outlook (Revenue, USD Million; 2019-2032)

- Passenger Vehicles;

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Rest of Latin America Cooling Capacity Outlook (Revenue, USD Million 2019-2032)