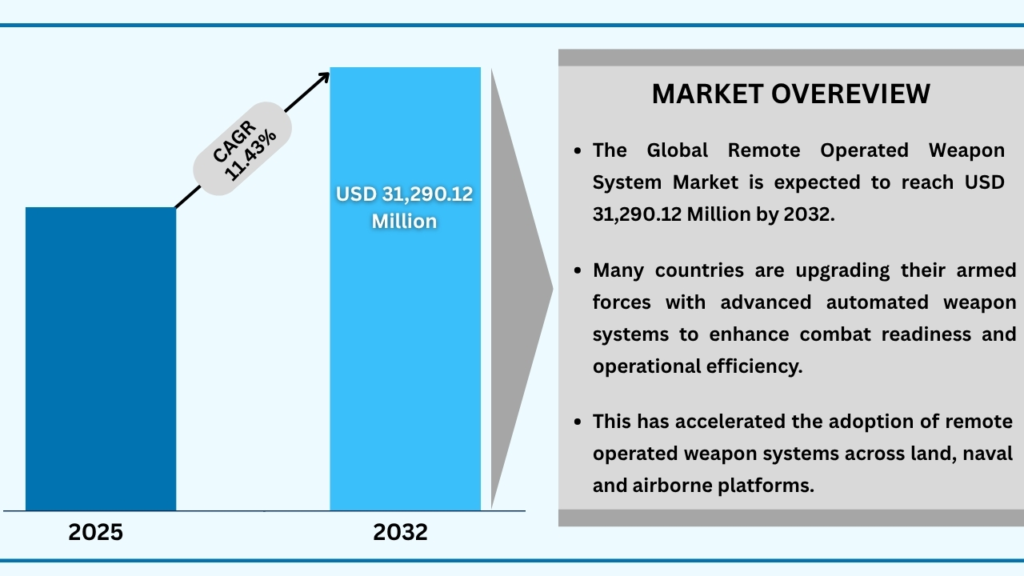

Market Synopsis

The Remote Operated Weapon System Market size was USD 13,216.22 Million in 2024 and is expected to reach USD 31,290.12 million at a CAGR of 11.43% during the forecast period. The global push for defense modernization is a major factor driving the adoption of remote operated weapon systems. Countries worldwide are increasingly investing in automated and remotely operated weapon systems to strengthen their military capabilities while minimizing risks to personnel. These systems are being integrated into naval vessels, armored vehicles, and airborne platforms, enhancing precision, operational efficiency, and situational awareness. The incorporation of advanced technologies such as artificial intelligence, robotics, and enhanced targeting solutions is making these systems a critical component of modern defense strategies.

The escalation of asymmetric warfare, border conflicts, and global terrorism has heightened the need for remote weapon systems that provide precise targeting without exposing personnel to direct threats. These systems allow armed forces and security agencies to operate weapons in high-risk zones remotely, ensuring both safety and operational effectiveness. Their tactical advantages, including rapid deployment, multi-target engagement, and integration with surveillance technologies, are driving widespread adoption. Governments and defense organizations are prioritizing investments in remotely operated systems to maintain strategic superiority, further fueling market growth.

Global Remote Operated Weapon System Market (USD Million)

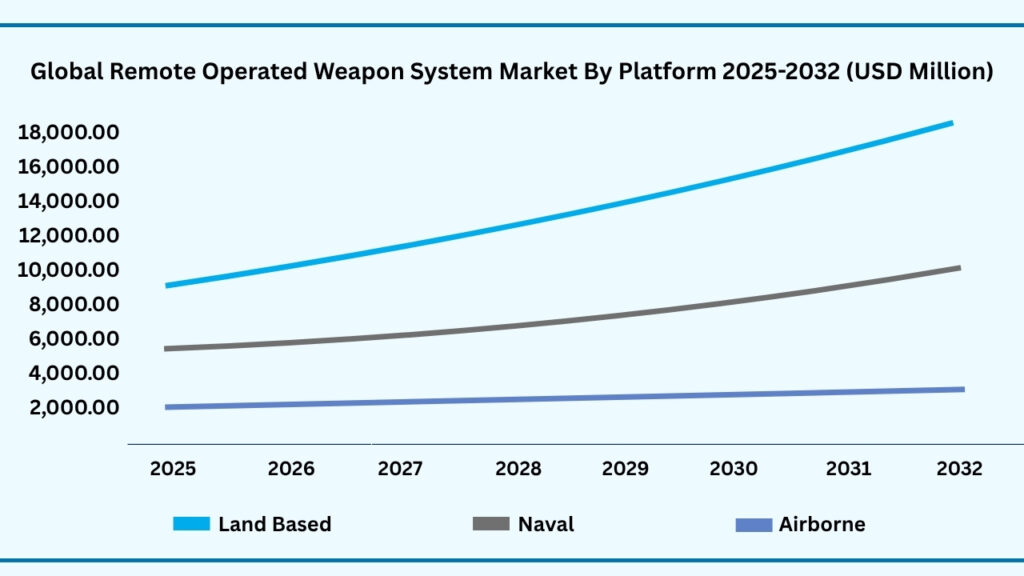

Global Remote Operated Weapon System Market by Platform Insights:

Land Based segment accounted for market share of share 54.33% in 2024 in the global Remote Operated Weapon System market.

The Land Based segment accounted for the largest share of the global Remote Operated Weapon System market in 2024, representing 54.33 % of total revenues. Land Based segment is expected to register a CAGR of 11.52% during the forecast year from 2025 to 2032. The land-based segment dominates the ROWS market due to its extensive adoption in ground combat operations. Militaries around the world are increasingly equipping armored vehicles, tanks, and stationary defense positions with remotely operated systems to enhance battlefield effectiveness while minimizing risk to personnel. These systems provide precision targeting, rapid response capabilities, and improved situational awareness, making them essential for modern ground operations. The ability to integrate advanced sensors, surveillance technologies, and automated targeting solutions further strengthens their appeal in land-based military applications.

Land-based remote weapon systems offer significant strategic advantages, allowing armed forces to maintain control over key territories and critical infrastructure. Their operational flexibility enables rapid deployment across diverse terrains and combat scenarios, from border defense to urban warfare. Additionally, the growing emphasis on reducing human exposure in high-risk areas drives continued investment in these systems. As nations focus on modernizing their ground forces, land-based ROWS remain a priority due to their combination of precision, reliability, and tactical superiority.

Global Remote Operated Weapon System Market by Platform (USD Million)

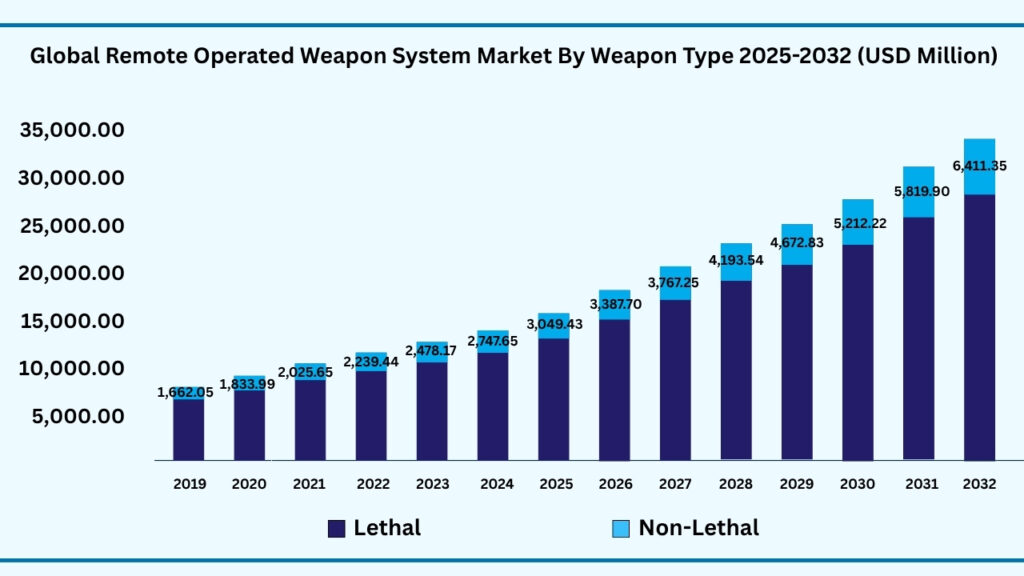

Global Remote Operated Weapon System Market by Weapon Type Insights:

Lethal segment accounted for the largest market share of share 79.21% in 2024 in the global Remote Operated Weapon System market.

Based on the Weapon type, Lethal segment held the largest revenue share of 79.21% 2024, and expected to register a CAGR of 11.49% between 2025 to 2032 and the market is expected to reach USD 24,878.77. The lethal segment dominates the ROWS market due to its widespread use in active combat scenarios. Armed forces prioritize lethal systems for their ability to deliver precise and effective firepower against threats while minimizing the need for personnel exposure. These systems are integrated into land, naval, and airborne platforms, providing superior offensive capabilities, rapid target engagement, and enhanced operational control. The demand for lethal remote weapons is further driven by their ability to respond quickly to emerging threats and maintain battlefield superiority.

Lethal remote weapon systems offer significant strategic and tactical benefits, including high accuracy, multi-target engagement, and integration with advanced surveillance and targeting technologies. Military organizations increasingly rely on these systems to strengthen defense capabilities, deter adversaries, and support modern warfare requirements. The focus on force protection, combined with advancements in automation and targeting precision, reinforces the adoption of lethal ROWS across various platforms, making this segment the largest contributor to the overall market.

Global Remote Operated Weapon System Market by Weapon Type (USD Million)

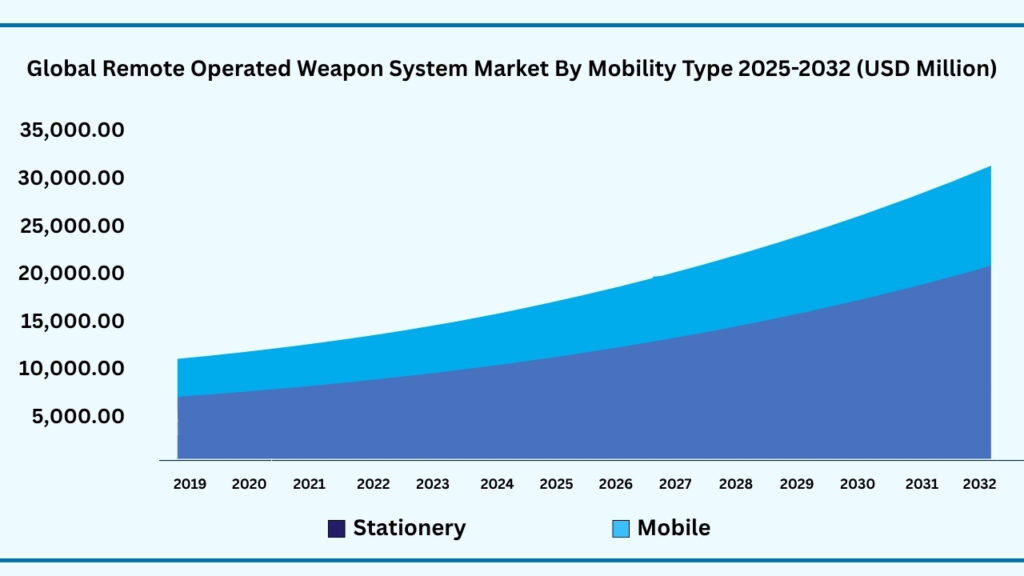

Global Remote Operated Weapon System Maret by Mobility Type Insights:

Stationery segment accounted for the largest market share of share 65.32%in 2024 in the global Remote Operated Weapon System market.

Based on Mobility Type, Stationery segment held the largest revenue share of 65.32% in the global Remote Operated Weapon System market in 2024 and expected to register a CAGR of 11.48% from 2025 to 2032 and expected to reach USD 20,501.29 million. The stationary segment leads the ROWS market due to its extensive deployment in fixed defense positions, such as military bases, border posts, and critical infrastructure sites. These systems provide reliable, continuous coverage and protection, allowing armed forces to secure strategic locations without the need for constant personnel presence. Their ability to integrate advanced sensors, targeting systems, and automated defense technologies enhances situational awareness and ensures rapid response to potential threats, making stationary systems highly favored for defensive applications. Stationary remote weapon systems offer significant operational advantages by reducing the need for personnel in high-risk zones while maintaining robust defensive capabilities. Their fixed deployment allows for consistent surveillance and precise engagement, supporting both deterrence and active defense strategies. Military organizations prioritize stationary systems for their reliability, ease of integration with existing infrastructure, and ability to provide a strong first line of defense, contributing to their dominant share in the global ROWS market.

Global Remote Operated Weapon System Market by Mobility Type (USD Million)

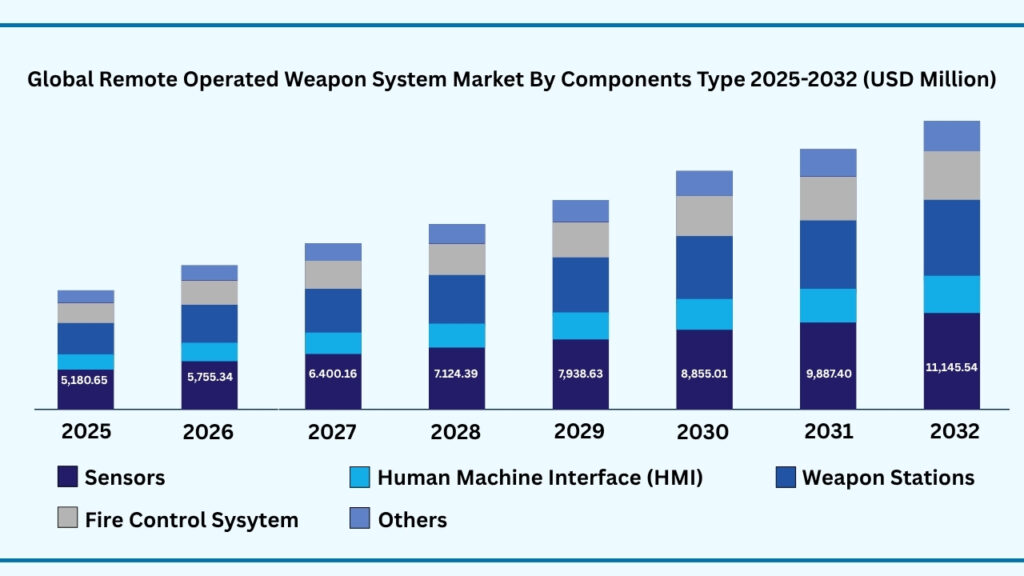

Global Remote Operated Weapon System Market by Components:

Sensors segment accounted for the largest market share of share 35.32%in 2024 in the global Remote Operated Weapon System market.

Based on Components, Sensors segment held the largest revenue share of 35.32% in the global Remote Operated Weapon System market in 2024 and expected to register a CAGR of 11.49%from 2025 to 2032 is expected to reach USD 11,145.54 million. The sensors segment leads the ROWS market due to its essential role in enhancing the operational performance of remote weapon systems. Sensors provide accurate detection, tracking, and targeting capabilities, enabling weapons to engage threats with precision while maintaining operator safety. They are integrated across land, naval, and airborne platforms to monitor environments, detect hostile activities, and provide real-time feedback to operators, making them a crucial component for modern defense systems.

Technological advancements in sensor capabilities, including thermal imaging, night vision, radar, and laser-based detection, have further strengthened their importance in ROWS. These innovations improve accuracy, reduce response time, and allow for multi-target engagement, enhancing the overall effectiveness of remote weapon systems. Military organizations increasingly rely on advanced sensors to support situational awareness, decision-making, and force protection, contributing to the dominant revenue share of the sensors component in the market.

If you want, I can also create two-paragraph factors for Weapon Stations, Fire Control Systems, and Other Components to complete the component-wise market analysis.

Global Remote Operated Weapon System Market by Components (USD Million)

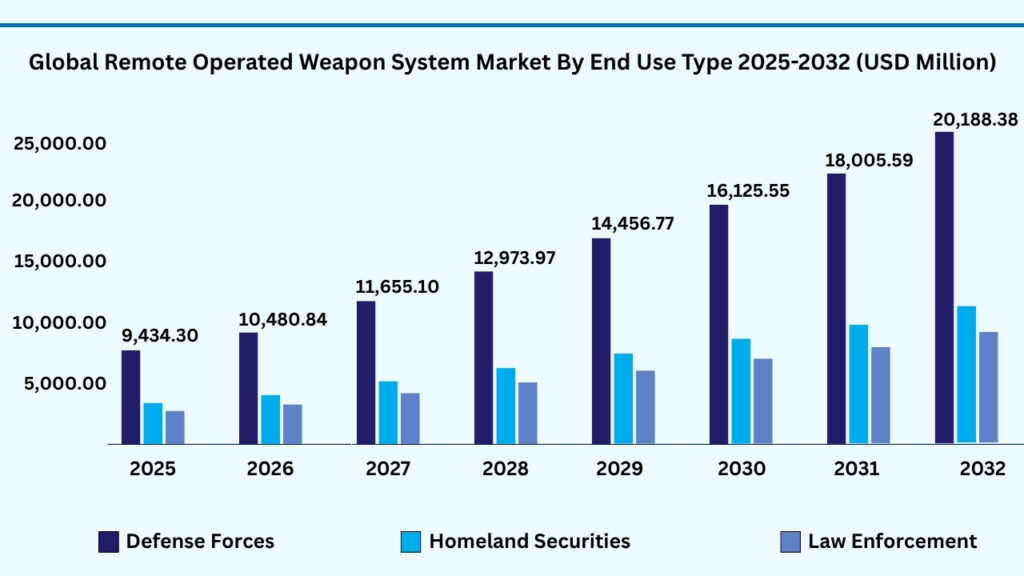

Global Remote Operated Weapon System Market by End Use Insights:

Defense Forces accounted for the largest market share of share 64.32% in 2024 in the global Remote Operated Weapon System market.

Based on End Use segment held the largest revenue share of 64.32% in the global Remote Operated Weapon System market in 2024 and expected to register a CAGR of 11.48% from 2025 to 2032 and expected to reach USD 20,188.38 million in 2032. The end-use segment leads the ROWS market primarily due to the extensive adoption by defense forces worldwide. Militaries prioritize remote operated weapon systems for their ability to enhance combat effectiveness, improve operational efficiency, and ensure personnel safety. These systems are deployed across land, naval, and aerial platforms, providing precise targeting, real-time surveillance, and rapid response capabilities. The reliance on ROWS by defense forces underscores their critical role in modern warfare strategies and drives the largest revenue share within the end-use category.

Beyond traditional military applications, ROWS are increasingly used for strategic security operations, including border protection, critical infrastructure defense, and counterterrorism activities. Their ability to operate in high-risk zones without direct human exposure makes them attractive to end-users focused on security and tactical superiority. The combination of reliability, operational flexibility, and integration with advanced technologies reinforces the segment’s leading position in the market and supports its strong growth trajectory.

Global Remote Operated Weapon System by End Use (USD Million)

Global Remote Operated Weapon System Market by Region Insights:

North America segment accounted for the largest market share of share of 35.32% in 2024 in the global Remote Operated Weapon System market.

Based on end use, the global Remote Operated Weapon System market is segmented into Europe, Asia-Pacific, North America, Latin America and Middle East & Africa. Among these, North America region held the largest revenue share of 35.32% in the global Remote Operated Weapon System market in 2024 and expected to reach USD 11,114.25 million in 2032. North America dominates the ROWS market due to significant investments in defense modernization programs. Countries in this region prioritize upgrading their military capabilities by integrating advanced remotely operated weapon systems across land, naval, and airborne platforms. This emphasis on modernization ensures that armed forces maintain technological superiority, improve operational efficiency, and enhance battlefield readiness, making the region a key contributor to the global ROWS market.

The adoption of cutting-edge technologies such as artificial intelligence, robotics, sensors, and automated targeting systems is a major factor driving market growth in North America. These technological advancements enhance the precision, situational awareness, and effectiveness of ROWS, allowing military and security forces to execute complex operations with higher accuracy and reduced personnel risk. The presence of leading defense contractors and continuous innovation further accelerates the adoption of these systems in the region.

North America’s strategic focus on homeland security, counterterrorism, and border protection contributes to the high demand for remote operated weapon systems. The region invests heavily in stationary and mobile ROWS to safeguard critical infrastructure, ports, and military installations. Additionally, the need for rapid response capabilities and enhanced operational safety in high-risk zones reinforces the region’s dominant position in the global market, ensuring sustained growth and revenue generation.

Global Remote Operated Weapon System Market by Region (USD Million)

Major Companies and Competitive Landscape

The global Remote Operated Weapon System market is highly competitive and fragmented, with leading defense contractors, system integrators, and emerging technology providers striving to capture market share. Key players are adopting strategies such as mergers and acquisitions, strategic partnerships with defense forces, and collaborations with advanced robotics and AI technology firms to expand their presence in both mature and emerging markets. Many companies are also investing heavily in product innovation, developing lightweight, high-precision, and low-power weapon systems with advanced features such as automated targeting, multi-sensor integration, and remote surveillance capabilities to meet evolving military requirements.

Additionally, market players are increasingly emphasizing operational efficiency, system reliability, and compliance with global defense standards. Efforts include designing ROWS compatible with multiple platforms such as land vehicles, naval vessels, and aerial drones, integrating advanced sensors and AI-based targeting systems, and enhancing situational awareness for operators. With growing expectations from defense forces for accuracy, rapid deployment, and force protection, manufacturers are focusing on delivering reliable, high-performance systems. The combination of technological innovation, strategic partnerships, regulatory support, and increasing defense modernization programs is expected to drive sustained growth and intensify competition across the global Remote Operated Weapon System market.

Some of the leading companies profiled in the global cultured meat market report include:

- Denso Corporation

- Kongsberg Gruppen ASA

- Raytheon Technologies Corporation

- Thales Group

- Elbit Systems Limited

- Leonardo S.p.A.

- Rheinmetall AG

- BAE Systems

- ASELSAN A.Ş.

- SAAB AB

- General Dynamics Corporation

- Rafael Advanced Defense Systems Ltd.

- Electro Optic Systems Pty Ltd.

- Hanwha Group

- Singapore Technologies Engineering Ltd.

- Israel Aerospace Industries Ltd.

- Moog Inc.

- Nexter Group

- Norinco Group

- Rostec State Corporation

- Herstal Group (FN Herstal)

Strategic Development

1. Kongsberg Gruppen ASA – PROTECTOR RWS Enhancements (2024)

In May 2024, Kongsberg Defence & Aerospace showcased advancements in its PROTECTOR Remote Weapon Station (RWS) during the 14th annual PROTECTOR Users Working Group in Kongsberg, Norway. The event highlighted the latest upgrades to the PROTECTOR systems, reinforcing Kongsberg’s position as a leading provider of RWS globally.

2. Thales Group – RAPIDFire Land System Development (2025)

In June 2025, Thales and KNDS France unveiled the RAPIDFire Land system, a land-based variant of their 40mm RAPIDFire naval defense system. The system is designed to provide enhanced protection for military bases and critical infrastructure, marking a significant expansion of Thales’s remote weapon system capabilities beyond naval applications.

3. Elbit Systems – Advanced Remote Controlled Weapon Stations (2024)

In 2024, Elbit Systems introduced its third-generation Remote Controlled Weapon Station (RCWS), offering high precision and multi-purpose capabilities for small and mid-caliber weapons. The RCWS family is designed to enhance the operational effectiveness of ground forces by providing versatile and reliable weapon solutions.

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 13,216.22 Million |

| CAGR (2024–2032) | 11.43% |

| Revenue forecast to 2033 | USD 31,290.12 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million, and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Platform, By Weapon Type, By Mobility Type, By Components, By End Use, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, Rest of MEA |

| Key companies profiled | “Denso Corporation, Sanden Holdings / Sanden Corporation, Hanon Systems, MAHLE GmbH, Valeo SA, Toyota Industries Corporation, Continental AG, Keihin Corporation, Calsonic Kansei Corporation, Subros Limited, Robert Bosch GmbH, BorgWarner Inc., Mitsubishi Heavy Industries Ltd., Nidec, Johnson Electric Holdings Limited, Shanghai Highly (Group) Co., Ltd, Michigan Automotive Compressor, Inc., Brose Fahrzeugteile SE & Co. KGE, Aptiv plc, Sensata Technologies” |

| Customization scope | 10 hours of free customization and expert consultation |

Some Key Questions the Report Will Answer

- What is the expected revenue Compound Annual Growth Rate (CAGR) of the global Remote Operated Weapon System market over the forecast period (2025–2032)?

- The global Remote Operated Weapon System market revenue is expected to register a Compound Annual Growth Rate (CAGR) of 11.43% during the forecast period.

- What was the size of the global Remote Operated Weapon System in 2024?

- The global Remote Operated Weapon System market size was USD 13,216.22 Million in 2024.

- Which factors are expected to drive the global Remote Operated Weapon System market growth? ·

- Increasing defense modernization and military spending across land, naval, and aerial platforms.

- Rising adoption of remote weapon systems to improve operational efficiency, enhance battlefield safety, and minimize personnel exposure in high-risk zones.

- Technological advancements such as AI-based targeting, multi-sensor integration, automation, and precision strike capabilities.

- Strategic investments by governments and defense organizations, along with collaborations and partnerships among leading system providers.

- The expansion of security applications, including border protection, critical infrastructure defense, and counter-terrorism operations.

- Which was the leading segment in the global Remote Operated Weapon System market in terms of platform in 2024?

- Land Based segment was leading in the Remote Operated Weapon System market on the basis of Cooling Capacity in 2024.

- What are some restraints for revenue growth of the global Remote Operated Weapon System market?

- The global Remote Operated Weapon System market faces several challenges that may restrain growth. Complex installation and maintenance requirements can slow adoption, particularly in cost-sensitive regions. In addition, limited awareness and adoption in developing countries due to operational and technical constraints can hinder market penetration. The performance of these systems is also highly dependent on reliable power supply, electronics, and network infrastructure. Furthermore, potential delays caused by regulatory compliance, certification processes, and export restrictions may impact timely deployment. Fluctuations in raw material costs and supply chain disruptions can additionally affect production schedules and overall market expansion.

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of Global Remote Operated Weapon System Market

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1. Primary

2.1.2. Secondary

2.1.3. Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1. Market value

2.3.2. Market volume

2.3.3. Exchange rate

2.3.4. Price

2.3.5. Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2025–2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10. Formulation & manufacturing

4.11. Distribution & retail

4.12. Import-export analysis

4.13. Brand comparative analysis

4.14. Technological advancements

4.15. Porter’s five force

4.15.1. Threat of new entrants

4.15.1.1. Capital requirement

4.15.1.2. Product knowledge

4.15.1.3. Technical knowledge

4.15.1.4. Customer relation

4.15.1.5. Access to application and technology

4.15.2. Threat of substitutes

4.15.2.1. Cost

4.15.2.2. Performance

4.15.2.3. Availability

4.15.2.4. Technical knowledge

4.15.2.5. Durability

4.15.3. Bargaining power of buyers

4.15.3.1. Numbers of buyers relative to suppliers

4.15.3.2. Product differentiation

4.15.3.3. Threat of forward integration

4.15.3.4. Buyers’ volume

4.15.4. Bargaining power of suppliers

4.15.4.1. Suppliers’ concentration

4.15.4.2. Buyers switching cost to other suppliers

4.15.4.3. Threat of backward integration

4.15.5. Bargaining power of suppliers

4.15.5.1. Industry concentration

4.15.5.2. Industry growth rate

4.15.5.3. Product differentiation

4.16. Patent analysis

4.17. Regulation coverage

4.18. Pricing analysis

4.19. Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1. Rising border threats

5.1.2. AI-enhanced targeting systems

5.1.3. Increasing focus on border security and soldier safety.

5.2. Restraints

5.2.1. High Initial Cost

5.2.2. Export and regulatory barriers

5.3. Opportunities

5.3.1. Demand for autonomous combat technology

5.3.2. Growing adoption of AI and automation in defense systems.

5.3.3. Defense modernization in emerging regions

5.4. Threat

5.4.1. Cybersecurity risks

5.4.2. Integration with legacy platform

Chapter 6. Global Remote Operated Weapon System Market By Platform Insights & Trends, Revenue (USD Million),

6.1. Platform Dynamics & Market Share, 2025–2032

6.1.1.1. Land Based

6.1.1.2. Naval

6.1.1.3. Airborne

Chapter 7. Global Remote Operated Weapon System Market By Weapon Type Insights & Trends, Revenue (USD Million),

7.1. Weapon Type Dynamics & Market Share, 2025–2032

7.1.1. Lethal

7.1.2. Non-Lethal

Chapter 8. Global Remote Operated Weapon System Market By Mobility Type Insights & Trends, Revenue (USD Million),

8.1. Mobility Type Dynamics & Market Share, 2025–2032

8.1.1. Stationery

8.1.2. Mobile

Chapter 9. Global Remote Operated Weapon System Market By Components Insights & Trends, Revenue (USD Million),

9.1. Components Dynamics & Market Share, 2025–2032

9.1.1. Sensors

9.1.2. Human-Machine Interface (HMI)

9.1.3. Weapon Stations

9.1.4. Fire Control Systems

9.1.5. Others

Chapter 10. Global Remote Operated Weapon System Market By End Use Insights & Trends, Revenue (USD Million),

10.1. End Use Dynamics & Market Share, 2025–2032

10.1.1. Defense Forces

10.1.2. Homeland Securities

10.1.3. Law Enforcement

Chapter 11. Global Remote Operated Weapon System Market Regional Outlook

11.1. Remote Operated Weapon System Share By Region, 2025–2032

11.2. North America

11.2.1. Market By Platform, Market Estimates and Forecast, USD Million,2025-2032

11.2.1.1. Land

11.2.1.2. Naval

11.2.1.3. Airborne

11.2.2. Market By Weapon Type Estimates and Forecast, USD Million, 2025-2032

11.2.2.1. Lethal

11.2.2.2. Non-Lethal

11.2.3. Market By Mobility Type, Market Estimates and Forecast, USD Million,

2025-2032

11.2.3.1. Stationery

11.2.3.2. Mobile

11.2.4. Market By Components Type, Market Estimates and Forecast, USD Million,

2025-2032

11.2.4.1. Sensors

11.2.4.2. Weapon Systems

11.2.4.3. Fire Control Systems

11.2.4.4. Others

11.2.5. Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

11.2.5.1. Defense Forces

11.2.5.2. Homeland Securities

11.2.5.3. Law Enforcement

11.2.6. Market By Country, Market Estimates and Forecast, USD Million, 2025-2032

11.2.6.1. US

11.2.6.2. Canada

11.2.6.3. Mexico

11.3. Europe

11.3.1. Market By Platform, Market Estimates and Forecast, USD Million,2025-2032

11.3.1.1. Land

11.3.1.2. Naval

11.3.1.3. Airborne

11.3.2. Market By Weapon Type Estimates and Forecast, USD Million, 2025-2032

11.3.2.1. Lethal

11.3.2.2. Non-Lethal

11.3.3. Market By Mobility Type, Market Estimates and Forecast, USD Million,

2025-2032

11.3.3.1. Stationery

11.3.3.2. Mobile

11.3.4. Market By Components Type, Market Estimates and Forecast, USD Million,

2025-2032

11.3.4.1. Sensors

11.3.4.2. Weapon Systems

11.3.4.3. Fire Control Systems

11.3.4.4. Others

11.3.5. Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

11.3.5.1. Defense Forces

11.3.5.2. Homeland Securities

11.3.5.3. Law Enforcement

11.3.6. Market By Country, Market Estimates and Forecast, USD Million, 2025-2032

11.3.6.1. Germany

11.3.6.2. France

11.3.6.3. U.K.

11.3.6.4. Poland

11.3.6.5. Spain

11.3.6.6. Benelux

11.3.6.7. Italy

11.3.6.8. Russia

11.3.6.9. Rest of Europe

11.4. Asia-Pacific

11.4.1. Market By Platform, Market Estimates and Forecast, USD Million,2025-2032

11.4.1.1. Land

11.4.1.2. Naval

11.4.1.3. Airborne

11.4.2. Market By Weapon Type Estimates and Forecast, USD Million, 2025-2032

11.4.2.1. Lethal

11.4.2.2. Non-Lethal

11.4.3. Market By Mobility Type, Market Estimates and Forecast, USD Million,

2025-2032

11.4.3.1. Stationery

11.4.3.2. Mobile

11.4.4. Market By Components Type, Market Estimates and Forecast, USD Million,

2025-2032

11.4.4.1. Sensors

11.4.4.2. Weapon Systems

11.4.4.3. Fire Control Systems

11.4.4.4. Others

11.4.5. Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

11.4.5.1. Defense Forces

11.4.5.2. Homeland Securities

11.4.5.3. Law Enforcement

11.4.6. Market By Country, Market Estimates and Forecast, USD Million, 2025-2032

11.4.6.1. China

11.4.6.2. India

11.4.6.3. South Korea

11.4.6.4. Japan

11.4.6.5. Oceania

11.4.6.6. Rest of Asia-Pacific

11.5. Latin America

11.5.1. Market By Platform, Market Estimates and Forecast, USD Million,2025-2032

11.5.1.1. Land

11.5.1.2. Naval

11.5.1.3. Airborne

11.5.2. Market By Weapon Type Estimates and Forecast, USD Million, 2025-2032

11.5.2.1. Lethal

11.5.2.2. Non-Lethal

11.5.3. Market By Mobility Type, Market Estimates and Forecast, USD Million,

2025-2032

11.5.3.1. Stationery

11.5.3.2. Mobile

11.5.4. Market By Components Type, Market Estimates and Forecast, USD Million,

2025-2032

11.5.4.1. Sensors

11.5.4.2. Weapon Systems

11.5.4.3. Fire Control Systems

11.5.4.4. Others

11.5.5. Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

11.5.5.1. Defense Forces

11.5.5.2. Homeland Securities

11.5.5.3. Law Enforcement

11.5.6. Market By Country, Market Estimates and Forecast, USD Million, 2025-2032

11.5.6.1. Brazil

11.5.6.2. Argentina

11.5.6.3. Colombia

11.5.6.4. Rest of Latin America

11.6. Middle East & Africa

11.6.1. Market By Platform, Market Estimates and Forecast, USD Million,2025-2032

11.6.1.1. Land

11.6.1.2. Naval

11.6.1.3. Airborne

11.6.2. Market By Weapon Type Estimates and Forecast, USD Million, 2025-2032

11.6.2.1. Lethal

11.6.2.2. Non-Lethal

11.6.3. Market By Mobility Type, Market Estimates and Forecast, USD Million,

2025-2032

11.6.3.1. Stationery

11.6.3.2. Mobile

11.6.4. Market By Components Type, Market Estimates and Forecast, USD Million,

2025-2032

11.6.4.1. Sensors

11.6.4.2. Weapon Systems

11.6.4.3. Fire Control Systems

11.6.4.4. Others

11.6.5. Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

11.6.5.1. Defense Forces

11.6.5.2. Homeland Securities

11.6.5.3. Law Enforcement

11.6.6. Market By Country, Market Estimates and Forecast, USD Million, 2025-2032

11.6.6.1. Saudi Arabia

11.6.6.2. Qatar

11.6.6.3. Egypt

11.6.6.4. UAE

11.6.6.5. Israel

11.6.6.6. South Africa

11.6.6.7. Rest of Middle East & Africa

Chapter 12. Competitive Landscape

12.1. Market Revenue Share By Manufacturers

12.2. Mergers & Acquisitions

12.3. Competitor’s Positioning

12.4. Strategy Benchmarking

12.5. Vendor Landscape

12.5.1. Distributors

12.5.1.1. North America

12.5.1.2. Europe

12.5.1.3. Asia Pacific

12.5.1.4. Middle East & Africa

12.5.1.5. Latin America

Chapter 13. Company Profiles

13.1. Kongsberg Gruppen ASA

13.1.1. Company Overview

13.1.2. Product & Service Offerings

13.1.3. Strategic Initiatives

13.1.4. Financials

13.2. Raytheon Technologies Corporation

13.2.1. Company Overview

13.2.2. Product & Service Offerings

13.2.3. Strategic Initiatives

13.2.4. Financials

13.3. Thales Group

13.3.1. Company Overview

13.3.2. Product & Service Offerings

13.3.3. Strategic Initiatives

13.3.4. Financials

13.4. Elbit System Limited

13.4.1. Company Overview

13.4.2. Product & Service Offerings

13.4.3. Strategic Initiatives

13.4.4. Financials

13.5. Leonardo S.p.A.

13.5.1. Company Overview

13.5.2. Product & Service Offerings

13.5.3. Strategic Initiatives

13.5.4. Financials

13.6. Rheinmetall AG

13.6.1. Company Overview

13.6.2. Product & Service Offerings

13.6.3. Strategic Initiatives

13.6.4. Financials

13.7. BAE Systems

13.7.1. Company Overview

13.7.2. Product & Service Offerings

13.7.3. Strategic Initiatives

13.7.4. Financials

13.7.5. Conclusion

13.8. ASELSAN A.Ş.

13.8.1. Company Overview

13.8.2. Product & Service Offerings

13.8.3. Strategic Initiatives

13.8.4. Financials

13.8.5. Conclusion

13.9. SAAB AB

13.9.1. Company Overview

13.9.2. Product & Service Offerings

13.9.3. Strategic Initiatives

13.9.4. Financials

13.9.5. Conclusion

13.10. General Dynamics Corporation

13.10.1. Company Overview

13.10.2. Product & Service Offerings

13.10.3. Strategic Initiatives

13.10.4. Financials

13.10.5. Conclusion

13.11. Rafael Advanced Defense Systems Ltd.

13.11.1. Company Overview

13.11.2. Product & Service Offerings

13.11.3. Strategic Initiatives

13.11.4. Financials

13.11.5. Conclusion

13.12. Electro Optic Systems Pty Ltd.

13.12.1. Company Overview

13.12.2. Product & Service Offerings

13.12.3. Strategic Initiatives

13.12.4. Financials

13.12.5. Conclusion

13.13. Hanwha Group

13.13.1. Company Overview

13.13.2. Product & Service Offerings

13.13.3. Strategic Initiatives

13.13.4. Financials

13.13.5. Conclusion

13.14. Singapore Technologies Engineering Ltd.

13.14.1. Company Overview

13.14.2. Product & Service Offerings

13.14.3. Strategic Initiatives

13.14.4. Financials

13.14.5. Conclusion

13.15. Israel Aerospace Industries Ltd.

13.15.1. Company Overview

13.15.2. Product & Service Offerings

13.15.3. Strategic Initiatives

13.15.4. Financials

13.15.5. Conclusion

13.16. Moog Inc.

13.16.1. Company Overview

13.16.2. Product & Service Offerings

13.16.3. Strategic Initiatives

13.16.4. Financials

13.16.5. Conclusion

13.17. Nexter Group

13.17.1. Company Overview

13.17.2. Product & Service Offerings

13.17.3. Strategic Initiatives

13.17.4. Financials

13.17.5. Conclusion

13.18. Norinco Group

13.18.1. Company Overview

13.18.2. Product & Service Offerings

13.18.3. Strategic Initiatives

13.18.4. Financials

13.18.5. Conclusion

13.19. Rostec State Corporation

13.19.1. Company Overview

13.19.2. Product & Service Offerings

13.19.3. Strategic Initiatives

13.19.4. Financials

13.19.5. Conclusion

13.20. Herstal Group (FN Herstal)

13.20.1. Company Overview

13.20.2. Product & Service Offerings

13.20.3. Strategic Initiatives

13.20.4. Financials

13.20.5. Conclusion

Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP. has segmented global Remote Operated Weapon System Market on the basis of By Platform, By Weapon Type, By Mobility Type, By Components, By End Use and by region for 2019 to 2032

Global Remote Operated Weapon System Market By Platform Outlook (Revenue, USD Million 2019-2032)

-

- Land

- Naval

- Airborne

Global Remote Operated Weapon System Market, By Weapon Type Outlook (Revenue, USD Million; 2019-2032)

-

- Lethal

- Non-Lethal

Global Remote Operated Weapon System Market By Mobility Type Outlook (Revenue, USD Million; 2019-2032)

-

- Stationary

- Mobile

Global Remote Operated Weapon System By Components Market (Revenue, USD Million; 2019-2032)

-

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

Global Remote Operated Weapon System Market By End Use (Revenue, USD Million; 2019-2032)

-

- Defense Forces

- Homeland Securities

- Law Enforcement

- North America

- North America Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- North America Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- North America Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- North America Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- North America End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- North America Platform Type Outlook (Revenue, USD Million 2019-2032)

- U.S.

- U.S. Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- U.S. Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- U.S. Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- U.S. Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- U.S. End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- U.S. Platform Type Outlook (Revenue, USD Million 2019-2032)

- Canada

- Canada Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Canada Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Canada Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Canada Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Canada End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Canada Platform Type Outlook (Revenue, USD Million 2019-2032)

- Mexico

- Mexico Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Mexico Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Mexico Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Mexico Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Mexico End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Mexico Platform Type Outlook (Revenue, USD Million 2019-2032)

- Europe

- Europe Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Europe Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Europe Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Europe Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Europe End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Europe Platform Type Outlook (Revenue, USD Million 2019-2032)

- Germany

- Germany Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Germany Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Germany Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Germany Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Germany End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Germany Platform Type Outlook (Revenue, USD Million 2019-2032)

- France

- France Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- France Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- France Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- France Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- France End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- France Platform Type Outlook (Revenue, USD Million 2019-2032)

- U.K.

- U.K. Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- U.K. Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- U.K. Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- U.K. Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- U.K. End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- U.K. Platform Type Outlook (Revenue, USD Million 2019-2032)

- Poland

- Poland Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Poland Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Poland Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Poland Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Poland End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Poland Platform Type Outlook (Revenue, USD Million 2019-2032)

- Spain

- Spain Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Spain Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Spain Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Spain Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Spain End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Spain Platform Type Outlook (Revenue, USD Million 2019-2032)

- Benelux

- Benelux Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Benelux Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Benelux Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Benelux Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Benelux End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Benelux Platform Type Outlook (Revenue, USD Million 2019-2032)

- Italy

- Italy Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Italy Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Italy Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Italy Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Italy End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Italy Platform Type Outlook (Revenue, USD Million 2019-2032)

- Russia

- Russia Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Russia Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Russia Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Russia Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Russia End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Russia Platform Type Outlook (Revenue, USD Million 2019-2032)

- Rest of Europe

- Rest of Europe Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Rest of Europe Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Rest of Europe Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Rest of Europe Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Rest of Europe End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Rest of Europe Platform Type Outlook (Revenue, USD Million 2019-2032)

- Asia-Pacific

- Asia-Pacific Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Asia-Pacific Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Asia-Pacific Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Asia-Pacific Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Asia-Pacific End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Asia-Pacific Platform Type Outlook (Revenue, USD Million 2019-2032)

- China

- China Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- China Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- China Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- China Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- China End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- China Platform Type Outlook (Revenue, USD Million 2019-2032)

- India

- India Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- India Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- India Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- India Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- India End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- India Platform Type Outlook (Revenue, USD Million 2019-2032)

- South Korea

- South Korea Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- South Korea Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- South Korea Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- South Korea Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- South Korea End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- South Korea Platform Type Outlook (Revenue, USD Million 2019-2032)

- Japan

- Japan Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Japan Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Japan Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Japan Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Japan End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Japan Platform Type Outlook (Revenue, USD Million 2019-2032)

- Turkey

- Turkey Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Turkey Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Turkey Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Turkey Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Turkey End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Turkey Platform Type Outlook (Revenue, USD Million 2019-2032)

- Iran

- Iran Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Iran Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Iran Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Iran Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Iran End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Iran Platform Type Outlook (Revenue, USD Million 2019-2032)

- Oceania

- Oceania Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Oceania Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Oceania Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Oceania Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Oceania End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Oceania Platform Type Outlook (Revenue, USD Million 2019-2032)

- Rest of Asia-Pacific

- Rest of Asia-Pacific Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Rest of Asia-Pacific Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Rest of Asia-Pacific Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Rest of Asia-Pacific Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Rest of Asia-Pacific End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Rest of Asia-Pacific Platform Type Outlook (Revenue, USD Million 2019-2032)

- Latin America

- Latin America Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Latin America Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Latin America Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Latin America Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Latin America End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Latin America Platform Type Outlook (Revenue, USD Million 2019-2032)

- Brazil

- Brazil Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Brazil Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Brazil Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Brazil Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Brazil End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Brazil Platform Type Outlook (Revenue, USD Million 2019-2032)

- Argentina

- Argentina Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Argentina Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Argentina Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Argentina Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Argentina End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Argentina Platform Type Outlook (Revenue, USD Million 2019-2032)

- Colombia

- Colombia Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Colombia Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Colombia Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Colombia Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Colombia End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Colombia Platform Type Outlook (Revenue, USD Million 2019-2032)

- Rest of Latin America

- Rest of Latin America Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Rest of Latin America Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Rest of Latin America Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Rest of Latin America Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Rest of Latin America End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Rest of Latin America Platform Type Outlook (Revenue, USD Million 2019-2032)

- Middle East & Africa

- Middle East & Africa Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Middle East & Africa Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Middle East & Africa Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Middle East & Africa Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Middle East & Africa End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Middle East & Africa Platform Type Outlook (Revenue, USD Million 2019-2032)

- Saudi Arabia

- Saudia Arabia Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Saudia Arabia Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Saudia Arabia Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Saudia Arabia Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Saudia Arabia End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Saudia Arabia Platform Type Outlook (Revenue, USD Million 2019-2032)

- Qatar

- Qatar Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Qatar Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Qatar Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Qatar Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Qatar End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Qatar Platform Type Outlook (Revenue, USD Million 2019-2032)

- Egypt

- Egypt Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Egypt Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Egypt Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Egypt Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Egypt End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Egypt Platform Type Outlook (Revenue, USD Million 2019-2032)

- UAE

- UAE Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- UAE Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- UAE Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- UAE Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- UAE End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- UAE Platform Type Outlook (Revenue, USD Million 2019-2032)

- Israel

- Israel Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Israel Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Israel Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Israel Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Israel End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Israel Platform Type Outlook (Revenue, USD Million 2019-2032)

- South Africa

- South Africa Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- South Africa Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- South Africa Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- South Africa Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- South Africa End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- South Africa Platform Type Outlook (Revenue, USD Million 2019-2032)

- Rest of Middle East & Africa

- Rest of Middle East & Africa Platform Type Outlook (Revenue, USD Million 2019-2032)

- Land

- Airborne

- Naval

- Rest of Middle East & Africa Weapon Type Outlook (Revenue, USD Million; 2019-2032)

- Lethal

- Non-Lethal

- Rest of Middle East & Africa Mobility Type Outlook (Revenue, USD Million; 2019-2032)

- Stationary

- Mobile

- Rest of Middle East & Africa Components Type Outlook (Revenue, USD Million; 2019-2032)

- Sensors

- Weapon Systems

- Fire Control Systems

- Others

- Rest of Middle East & Africa End Use Outlook (Revenue, USD Million; 2019-2032)

- Defense Forces

- Homeland Securities

- Law Enforcement

- Rest of Middle East & Africa Platform Type Outlook (Revenue, USD Million 2019-2032)