Back to Agriculture

Global Agricultural Biologicals Market

Published Date : November 11, 2025 Category: Agriculture

Published Date : November 11, 2025 Category: Agriculture

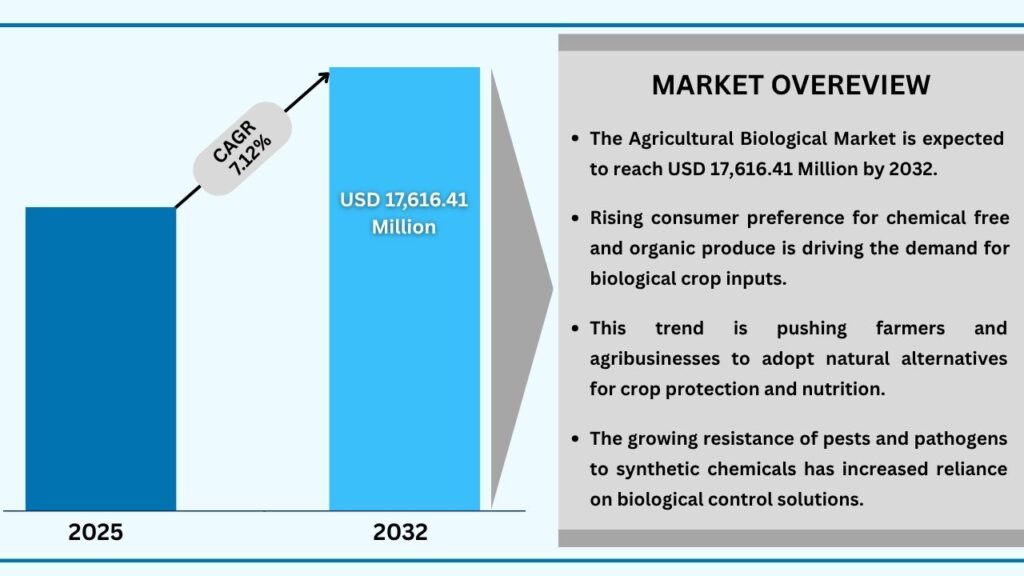

The Global Agricultural Biologicals Market is witnessing remarkable growth, driven by the growing emphasis on sustainable farming, environmental preservation, and reduced dependency on chemical-based agricultural inputs. The market was valued at USD 10,187.01 million in 2024 and is projected to reach USD 17,616.41 million by 2032, expanding at a CAGR of 7.12% during the forecast period. Agricultural biologicals — which include biofertilizers, biostimulants, and biopesticides — are gaining prominence as vital tools for enhancing crop productivity, improving soil health, and fostering resilient agricultural ecosystems.

Growing awareness about soil degradation, climate change, and food safety is fueling the adoption of these eco-friendly inputs across both developed and developing regions. As farmers, governments, and agribusinesses shift toward regenerative and organic farming systems, agricultural biologicals have evolved from supplementary products to core components of sustainable crop management practices.

Market Overview

The market’s momentum is supported by the rising demand for green and residue-free agricultural products, as consumers and regulators increasingly favor chemical-free food systems. The global movement toward carbon-neutral and regenerative agriculture is also encouraging investments in bio-based crop inputs. Additionally, improvements in biological formulation technology, microbial strain development, and field stability are enhancing the reliability and scalability of biologicals across diverse climatic conditions.

Large agribusiness corporations and innovative biotech start-ups are collaborating to build comprehensive biological portfolios, integrating microbial inoculants, seaweed extracts, enzymes, and beneficial fungi to deliver synergistic agronomic benefits. As these products continue to prove their efficacy in improving yield, quality, and soil vitality, their role in shaping the future of agriculture is becoming indispensable.

Global Agricultural Biologicals Market Overview

Market Definition

The Agricultural Biologicals Market encompasses a wide range of naturally derived inputs — including microorganisms, plant extracts, and bio-based compounds — that enhance plant growth, nutrient absorption, and pest resistance without the harmful impacts of synthetic agrochemicals. These products can be broadly categorized into biopesticides, biofertilizers, and bio stimulants, each serving a distinct but complementary role in crop enhancement and protection.

Biopesticides provide effective pest management while maintaining ecological balance; biofertilizers enhance soil fertility through microbial activity; and biostimulants improve plant metabolism and stress tolerance. The adoption of these inputs is further facilitated by their compatibility with organic certification programs, sustainable agriculture frameworks, and precision farming technologies, making them a cornerstone of modern eco-friendly agriculture.

Sustainability and Crop Productivity

Sustainability is the central theme driving the agricultural biologicals industry. These products play a pivotal role in enhancing soil biodiversity, nutrient cycling, and water-use efficiency, ensuring long-term productivity without depleting natural resources. They empower farmers to maintain consistent yields even under stress conditions such as drought, salinity, or temperature fluctuations.

For smallholder farmers, biologicals offer a cost-effective and resource-efficient solution that reduces reliance on synthetic fertilizers and pesticides. Meanwhile, commercial growers are adopting them to improve yield quality, export compliance, and brand reputation in sustainability-driven markets. By enriching soil health and promoting regenerative farming practices, agricultural biologicals support both environmental stewardship and economic viability — enabling farmers to meet global food security goals sustainably.

Technological Innovation and Product Evolution

Recent advances in biotechnology, genomics, and microbial engineering have transformed the agricultural biologicals landscape. Companies are now developing next-generation biologicals that integrate beneficial microbes, bioactive peptides, and enzyme complexes to target specific plant functions — from nutrient uptake to abiotic stress resistance.

Encapsulation technologies, nanocarriers, and precision formulation techniques are improving product shelf life and stability, addressing one of the key barriers to adoption. Additionally, AI-driven field analytics and digital agronomy platforms are enabling real-time monitoring of biological efficacy, allowing farmers to make data-based input decisions.

This technological convergence is creating an ecosystem where biologicals are no longer viewed as complementary products but as central tools in precision and climate-smart agriculture. The evolution from stand-alone products to integrated crop enhancement systems marks a critical milestone for the industry.

Policy Support and Sustainable Agriculture Initiatives

Government initiatives across multiple regions are significantly contributing to market expansion. Regulatory agencies in Europe, Asia-Pacific, and North America are actively promoting the use of bio-based inputs through subsidies, tax incentives, and certification frameworks aimed at reducing chemical dependency.

In the European Union, strict environmental regulations and the Farm to Fork Strategy are encouraging farmers to replace synthetic agrochemicals with sustainable alternatives. Similarly, countries such as India, China, and Brazil are launching national missions for organic farming, offering financial support for biofertilizer and biopesticide adoption.

These policy frameworks not only promote sustainable agricultural practices but also help build trust among farmers by ensuring quality standards, labeling transparency, and field validation. As a result, global harmonization of biological input regulations is expected to further accelerate market adoption and investment inflows.

Market Restraints and Challenges

Despite its strong growth potential, the Agricultural Biologicals Market faces several challenges. The lack of standardized global regulations often leads to inconsistent product efficacy claims, undermining farmer confidence. Limited awareness among growers in developing economies and the need for specialized knowledge for effective application also restrict market penetration.

Additionally, biological products are sensitive to storage and environmental conditions, which can affect their shelf life and field performance. The cost of R&D and commercialization remains high, particularly for companies developing microbial-based solutions that require stringent quality control. Overcoming these challenges through education programs, digital advisory tools, and improved product formulation will be key to unlocking the full market potential.

Regional Outlook

Europe

Europe continues to dominate the global Agricultural Biologicals Market, holding the largest share due to its proactive sustainability policies, strong organic farming base, and high adoption of eco-friendly inputs. Countries such as Spain, France, Italy, and Germany are leading in both production and consumption, driven by advanced horticulture and viticulture sectors. The region’s stringent environmental policies and focus on residue-free crops have created a highly supportive ecosystem for biological innovation.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing regional market, propelled by the rapid modernization of agriculture, rising food demand, and government-led initiatives promoting sustainable practices. India, China, Japan, and Australia are at the forefront of this growth, driven by increasing adoption of microbial fertilizers, bio-based pest management, and seaweed-derived products.

Major Companies and Competitive Landscape

The global Agricultural Biologicals Market is moderately fragmented and highly competitive, comprising a mix of multinational corporations, specialized bio-input manufacturers, and innovative start-ups. Key players include:

BASF SE, UPL Limited, Valagro S.p.A. (Syngenta Group), FMC Corporation, Lallemand Plant Care, Biolchim S.p.A., Isagro S.p.A., Novozymes A/S, Rallis India Limited, Koppert Biological Systems, Bayer AG, Marrone Bio Innovations (Bioceres Crop Solutions), Corteva Agriscience, Acadian Plant Health, Andermatt Biocontrol AG, Certis Biologicals, Symborg, Agrinos AS (Yara International), Tradecorp International (Rovensa Group), and Agronutrition (De Sangosse Group).

These companies are focusing on strategic mergers, acquisitions, and R&D collaborations to expand product portfolios and improve regional distribution. Increasing investments in microbial consortia development, fermentation technology, and precision delivery systems are reshaping market dynamics, with emphasis on biological efficacy, scalability, and environmental compatibility.

Strategic Developments

Strategic Expansion (2025)

In early 2025, a leading agricultural biological manufacturer announced the launch of a new innovation and production facility in Pune, India, aimed at strengthening its foothold in the Asia-Pacific region. The facility focuses on the development of liquid and microbial-based biofertilizers and biostimulants, addressing crop-specific needs in tropical and subtropical regions. This move enhances local sourcing efficiency, supports government sustainability programs, and fosters collaboration with agritech startups and agricultural universities.

Strategic Collaboration (2025)

In mid-2025, a European agro-biological leader entered into a strategic partnership with a North American biotechnology firm specializing in microbial and enzymatic crop enhancement. The collaboration aims to co-develop next-generation biologicals designed for improved nutrient use efficiency, stress tolerance, and soil microbiome restoration. This partnership also integrates joint marketing strategies and digital monitoring platforms to optimize farmer engagement and field validation.

Future Market Direction and Strategic Insights

The future of the Agricultural Biologicals Market lies in the integration of biotechnology, digital farming, and sustainable crop management systems. As agriculture transitions toward regenerative and climate-resilient models, biologicals will play a central role in improving input efficiency and reducing environmental impact.

Companies focusing on scientific validation, precision application technologies, and scalable production models will gain a competitive edge. Moreover, emerging areas such as carbon farming, biological nitrogen fixation, and AI-assisted crop analytics are set to redefine the next phase of agricultural innovation. The convergence of data-driven agronomy with bio-based inputs will accelerate the market’s evolution into a mainstream component of modern agriculture.

Conclusion

The Global Agricultural Biologicals Market is at the forefront of the agricultural transformation, bridging productivity, profitability, and sustainability. With growing environmental awareness, technological innovation, and supportive policy frameworks, biologicals are transitioning from niche alternatives to essential agricultural inputs.

Their capacity to rejuvenate soil, enhance crop resilience, and reduce chemical dependency aligns perfectly with global sustainability goals. As investments in research, digital integration, and farmer education expand, the market is poised to become a cornerstone of future-ready, climate-smart, and regenerative agriculture worldwide.

Advantia Business Consulting supports agri-technology companies, investors, and policymakers with actionable market intelligence, regulatory insight, and go-to-market strategies tailored to the agricultural biologicals sector. Our team combines technical expertise in microbial and plant-based solutions with commercial experience in formulation scale-up, field validation, and channel development to help clients de-risk product launches and accelerate farmer adoption.