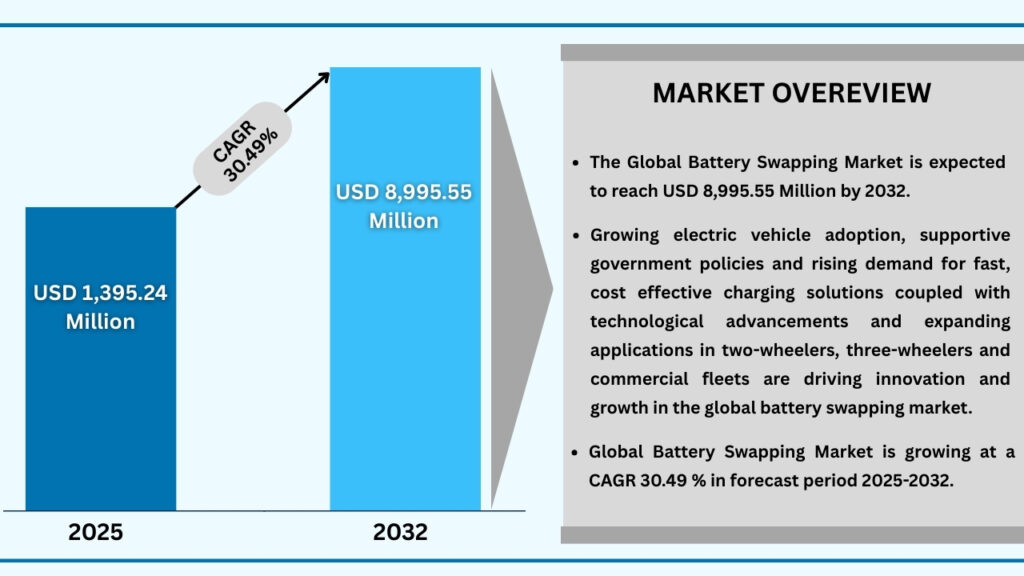

Market Synopsis

The global battery swapping market size was USD 1,069.23 million in 2024 and is expected to reach USD 8,988.55 million at a CAGR of 30.49% during the forecast period from 2025 to 2032. The global battery swapping market is witnessing rapid growth as the adoption of electric vehicles accelerates and urban populations seek fast, convenient, and cost-effective charging solutions. Battery swapping technology, allowing depleted batteries to be exchanged for fully charged ones in minutes, is being widely deployed across two-wheelers, three-wheelers, and commercial fleet vehicles due to its efficiency, reduced downtime, and operational flexibility. Demand is particularly strong in Asia-Pacific, driven by large-scale urbanization, government incentives, and extensive fleet electrification, while Europe and North America are emerging as growth regions supported by regulatory support and EV infrastructure development. Despite challenges such as high infrastructure costs, battery standardization issues, and inventory management, ongoing advancements in lithium-ion and solid-state batteries, automation, and smart station technologies are creating promising opportunities. With increasing focus on sustainability and the expansion of battery-as-a-service (BaaS) models, battery swapping is poised to become a critical enabler of the global EV ecosystem.

Global Battery Swapping Market (USD million)

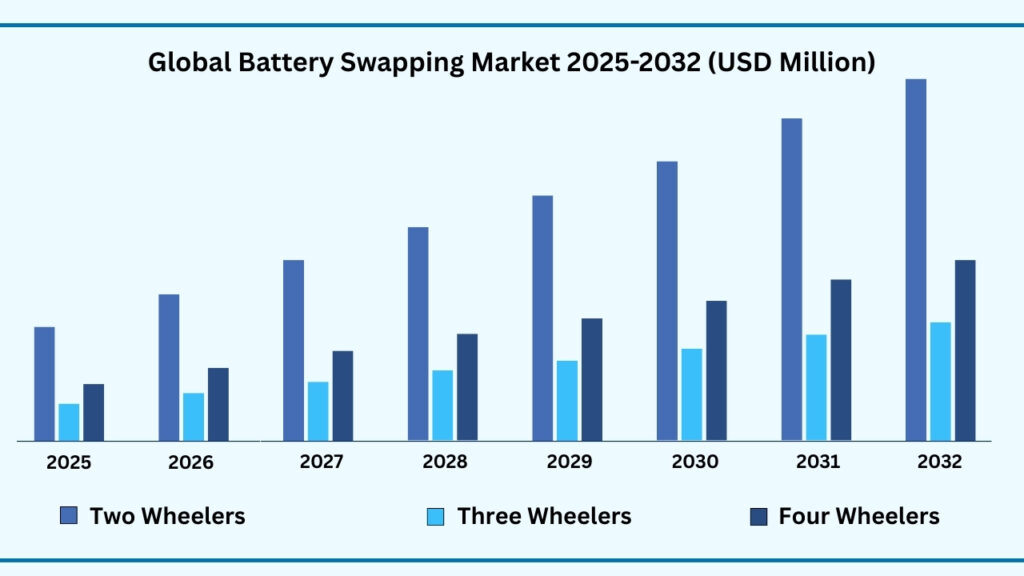

Global Battery Swapping Market by Vehicle Type Insights:

Two-Wheelers segment accounted for market share of share 54.29% in 2024 in the global Battery Swapping market.

The Two-Wheelers sub-segment holds the dominant position in the global battery swapping market, accounting for 54.29% of the segment share in 2024. Revenues in this category are projected to reach approximately USD 4,883.04 million, growing at a robust CAGR of 30.50% during the forecast period from 2025 to 2032. The strong performance of two-wheelers is largely driven by the widespread adoption of electric scooters and motorcycles, particularly in densely populated regions such as China, India, and Southeast Asia. Battery swapping provides an efficient and convenient solution for these vehicles, addressing range anxiety and minimizing downtime for daily commuters and last-mile delivery operators. Companies like NIO, Gogoro, and Okinawa are spearheading innovations in this space, developing swappable battery packs and modular designs that enhance operational efficiency and battery lifespan.

The Three-Wheelers sub-segment, while smaller in overall share, is gaining traction due to its significant presence in commercial and urban mobility sectors. E-rickshaws, cargo tricycles, and other three-wheeled EVs are increasingly adopting battery swapping to maintain continuous operation in last-mile logistics, ride-hailing services, and intra-city deliveries. The appeal of fast battery replacement and low operational costs makes this segment particularly relevant in markets such as India, Thailand, and Indonesia, where three-wheelers are a critical component of urban transportation. Industry players, including Ampere Vehicles and Bajaj Auto, are exploring partnerships and pilot programs to expand swap-station networks for three-wheelers, reflecting a growing recognition of their commercial potential.

The Four-Wheelers sub-segment, encompassing passenger cars and light commercial EVs, represents a smaller but strategically important portion of the market. Although adoption is currently limited compared with two- and three-wheelers, manufacturers and battery swapping service providers are increasingly testing solutions for urban car-sharing fleets, electric taxis, and small delivery vehicles. Initiatives by companies like CATL, NIO, and Sinopec are advancing automated and modular swapping stations for four-wheelers, aiming to reduce charging time while ensuring safety and interoperability. As technological innovation continues and battery standardization efforts mature, four-wheelers are expected to play a more prominent role in the market, complementing the growth of smaller vehicle segments and contributing to a holistic battery-as-a-service ecosystem.

Global Battery Swapping Market, By Vehicle Type (USD million)

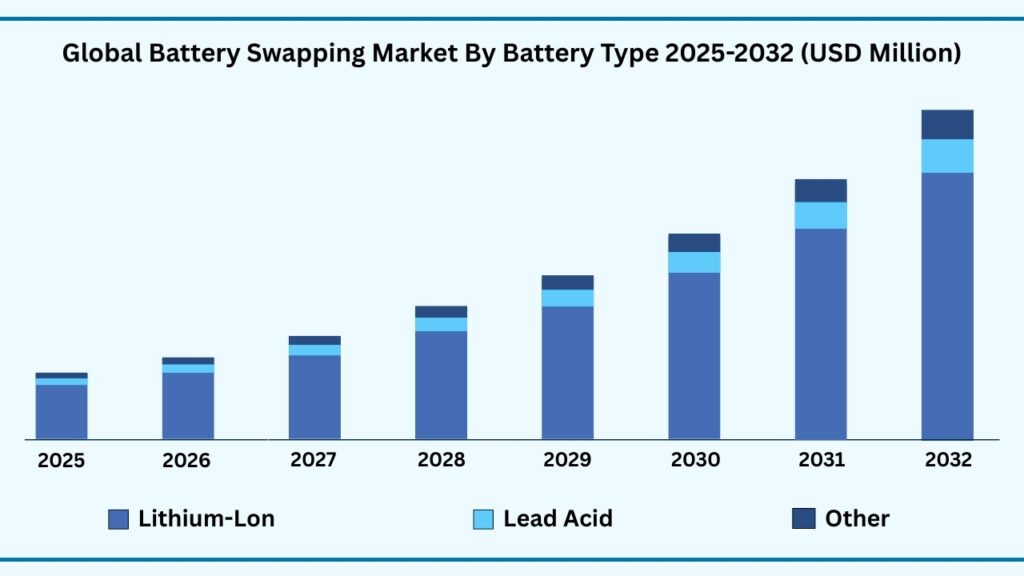

Global Battery Swapping Market by Battery Type Insights:

Lithium-Ion segment accounted for market share of share 88.83% in 2024 in the global Battery Swapping market.

The Lithium-Ion sub-segment leads the global battery swapping market, capturing the largest share of 88.83% in 2024. Revenues in this category are projected to reach approximately USD 7,992.61 million, expanding at a strong CAGR of 30.51% during the forecast period. Lithium-ion batteries dominate due to their high energy density, longer lifecycle, and faster charging capabilities, making them ideal for two-wheelers, three-wheelers, and passenger EVs in urban and fleet applications. Companies like Gogoro, NIO, and CATL are at the forefront of lithium-ion battery innovations, introducing modular and swappable pack designs that enhance operational efficiency, reduce downtime, and enable seamless integration into battery-as-a-service (BaaS) models. Their widespread adoption continues to underpin the rapid expansion of battery swapping infrastructure globally.

The Lead-Acid sub-segment, although much smaller, continues to play a role in specific niche applications. Lead-acid batteries are primarily used in lower-cost electric two- and three-wheelers, industrial carts, and rural or small-scale delivery vehicles where affordability outweighs performance metrics. While their energy density and lifecycle are limited compared with lithium-ion, lead-acid batteries remain attractive for markets with cost-sensitive users or legacy swap infrastructure. Companies focusing on this segment are exploring hybrid solutions and improved maintenance practices to extend battery life and optimize swapping frequency, particularly in emerging economies.

The Other battery category, which includes technologies such as nickel-metal hydride (NiMH), sodium-ion, and early-stage solid-state batteries, is gradually emerging as a complementary option in the market. Although these alternatives currently account for a small share, ongoing research and pilot programs are evaluating their potential benefits, including enhanced safety, lower environmental impact, and recyclability. Startups and established battery manufacturers are testing these chemistries in select two- and three-wheeler fleets, as well as in innovative urban delivery solutions. Together, the dominance of lithium-ion, the niche relevance of lead-acid, and the experimental adoption of other battery types illustrate the diverse technological strategies shaping the global battery swapping market and its adaptability to evolving EV requirements.

Global Battery Swapping Market, By Battery Type (USD million)

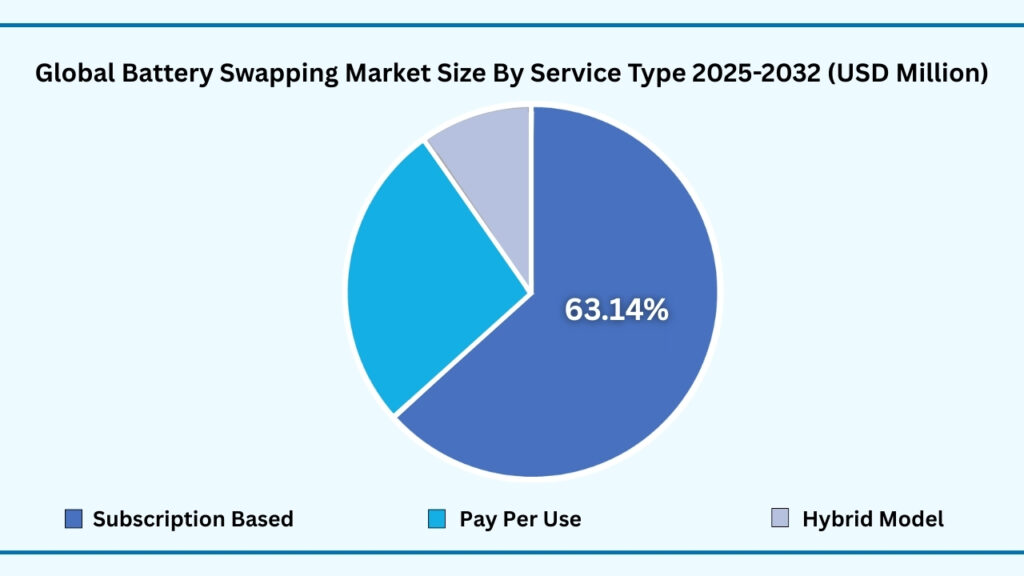

Global Battery Swapping Market by Service Type Insights:

Subscription-Based segment accounted for market share of share 63.17% in 2024 in the global Battery Swapping market.

The Subscription-Based sub-segment leads the global battery swapping market, accounting for 63.17% of the segment share in 2024. Revenues in this category are projected to reach approximately USD 5,682.18 million, expanding at a CAGR of 30.50% during the forecast period. Subscription-based services dominate due to their predictability, convenience, and cost-effectiveness, allowing users to pay a fixed monthly fee for access to swappable batteries without the burden of ownership. This model has become particularly attractive for fleet operators, ride-hailing services, and delivery companies, where minimizing downtime is critical. Companies such as Gogoro, NIO, and Okinawa are innovating subscription offerings that combine smart battery management, mobile app integrations, and flexible swap station access to enhance customer experience and operational efficiency.

The Pay-Per-Use sub-segment, while smaller in overall share, is steadily gaining adoption among individual consumers and cost-conscious urban EV users. This model allows users to pay only for the battery swaps they consume, providing flexibility without long-term commitment. It is especially popular in regions where EV penetration is still emerging, or among casual riders who do not require daily access. Operators are experimenting with dynamic pricing, micro-subscriptions, and digital wallet integrations to make pay-per-use services seamless and appealing. Examples include Ampere Vehicles and Bounce Infinity, which have introduced flexible swap plans for scooters and motorcycles, demonstrating the model’s relevance for personal mobility solutions.

The Hybrid model, which combines subscription and pay-per-use features, is gradually carving its niche as a versatile alternative for both commercial and individual users. By allowing a baseline subscription with additional pay-as-you-go flexibility, hybrid services cater to varying usage patterns and vehicle types, particularly in urban delivery fleets and shared mobility ecosystems. While this segment currently represents a smaller portion of the market, companies are exploring innovative business strategies and technology integrations such as AI-driven battery allocation and automated billing to enhance utilization and customer satisfaction. Collectively, the dominance of subscription services, the growing adoption of pay-per-use models, and the emerging hybrid solutions illustrate the adaptability of the battery swapping service landscape, positioning it to meet diverse operational and consumer needs across the EV ecosystem.

Global Battery Swapping Market, By Service Type (USD million)

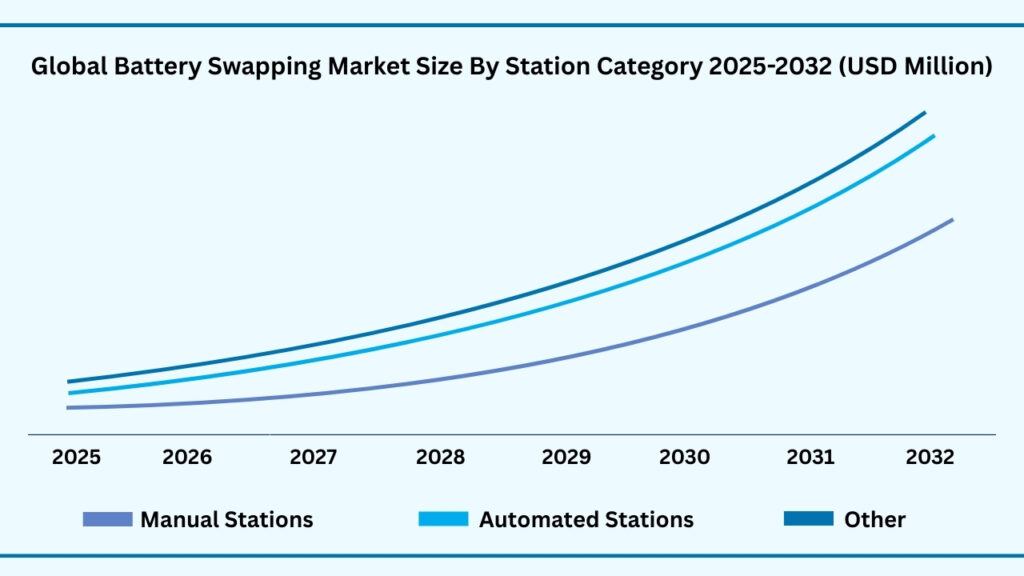

Global Battery Swapping Market by Station Category Insights:

Manual Stations segment accounted for market share of share 67.85% in 2024 in the global Battery Swapping market.

The Manual Stations sub-segment dominates the global battery swapping market, capturing the largest share of 67.85% in 2024. Revenues in this category are projected to reach approximately USD 6,120.05 million, expanding at a CAGR of 30.56% during the forecast period. Manual stations continue to lead due to their cost-effectiveness, simplicity, and faster deployment compared with automated alternatives. These stations are widely used for two- and three-wheeler fleets, particularly in urban and semi-urban regions across Asia-Pacific, where EV adoption is rapidly increasing. Companies like Okinawa, Gogoro, and Ampere Vehicles have successfully implemented manual swap stations that allow operators and riders to exchange batteries quickly, providing reliable service while keeping operational costs manageable.

In comparison, the Automated Stations sub-segment is emerging as a technologically advanced solution that enhances efficiency, safety, and scalability. Automated stations utilize robotics, IoT, and AI to manage battery swapping, reduce human intervention, and optimize inventory management. While currently accounting for a smaller share of the market, automated stations are gaining traction in high-density urban areas, fleet depots, and commercial hubs, particularly for four-wheelers and larger EV fleets. Companies such as NIO and CATL are investing in automated swapping solutions, piloting advanced stations that minimize downtime and deliver consistent, reliable battery replacement.

The Other sub-segment, which includes semi-automated, modular, and experimental station designs, is gradually contributing to the market’s expansion. These stations often serve niche applications, such as rural deployments, pilot projects, or mixed-use mobility hubs, where flexible and adaptable designs are necessary. Though their market share is smaller, these innovative stations provide valuable insights into operational optimization, cost reduction, and user experience improvements. Collectively, the dominance of manual stations, the emerging relevance of automated solutions, and the experimentation within the other category illustrate the dynamic and adaptable nature of battery swapping infrastructure, highlighting its pivotal role in supporting the growth of EV ecosystems globally.

Global Battery Swapping Market, By Station (USD million)

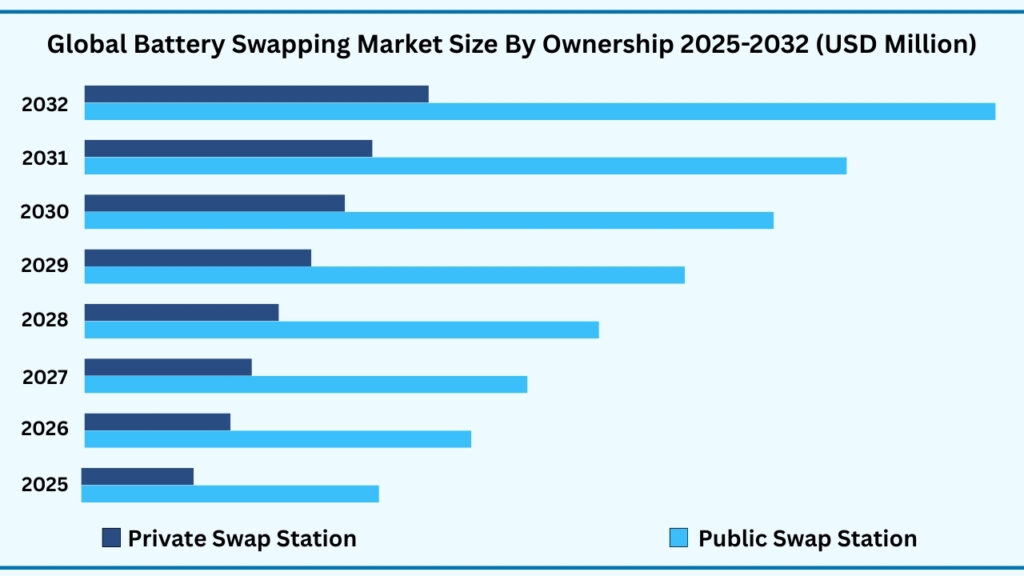

Global Battery Swapping Market by Ownership Insights:

Public Swap Station segment accounted for market share of share 74.33% in 2024 in the global Battery Swapping market.

The Public Swap Station sub-segment leads the global battery swapping market, capturing the largest share of 74.33% in 2024. Revenues in this category are projected to reach approximately USD 6,687.21 million, expanding at a CAGR of 30.51% during the forecast period. Public swap stations dominate due to strong government support, regulatory incentives, and strategic partnerships with state-owned enterprises and utilities. These stations are widely deployed in high-density urban areas and along key transport corridors, particularly in Asia-Pacific countries such as China and India, where governments are actively promoting EV infrastructure. Operators like Sinopec and State Grid Corporation of China are leading the rollout of public swap networks, ensuring wide accessibility, consistent service, and reliability for commuters, commercial fleets, and shared mobility services.

In contrast, the Private Swap Station sub-segment, while smaller in overall share, plays a critical role in commercial and fleet operations. Private stations are primarily operated by OEMs, energy companies, and mobility service providers, catering to high-utilization vehicles such as delivery fleets, ride-hailing services, and corporate EV programs. These stations offer flexibility, operational control, and brand-specific services, allowing companies to optimize battery management and reduce operational costs. Organizations like NIO, Gogoro, and Okinawa are investing in private swap infrastructure, piloting innovative approaches such as modular stations and subscription-based access for their customers, reflecting the growing relevance of privately-owned networks.

The Ownership segment also includes emerging hybrid and partnership models, where public-private collaborations aim to combine wide accessibility with operational efficiency. These arrangements enable shared use of swap stations while distributing costs and risks between stakeholders. While currently representing a smaller portion of the market, such hybrid strategies are gaining attention for their potential to accelerate infrastructure deployment and enhance user convenience. Collectively, the dominance of public swap stations, the strategic deployment of private stations, and the experimentation with hybrid ownership models illustrate the dynamic and adaptable nature of battery swapping infrastructure, reinforcing its critical role in supporting the global EV ecosystem.

Global Battery Swapping Market, By Ownership (USD million)

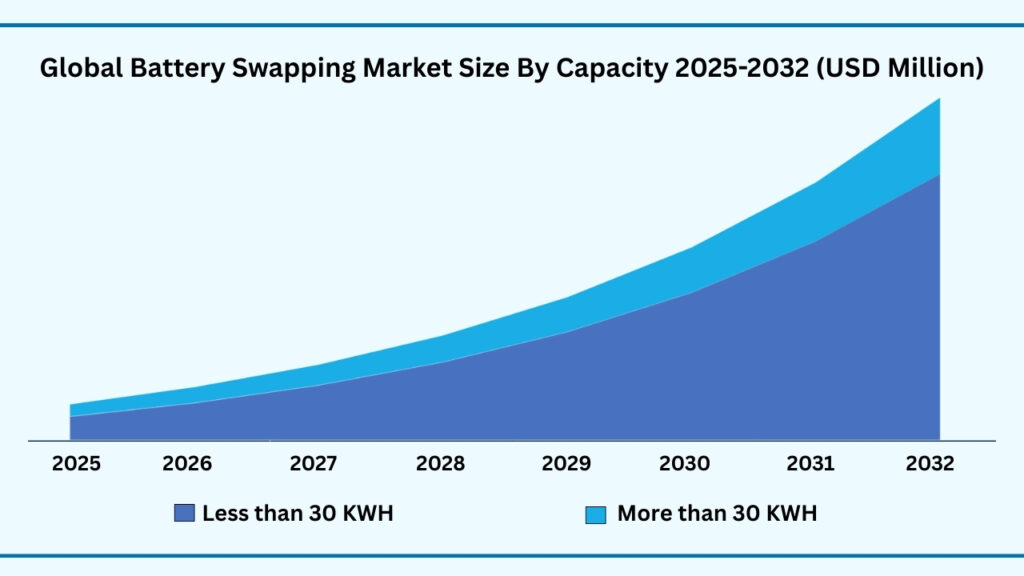

Global Battery Swapping Market by Capacity Insights:

Less than 30 kWh segment accounted for market share of share 78.85% in 2024 in the global Battery Swapping market.

The Less than 30 kWh sub-segment leads the global battery swapping market, capturing the largest share of 78.75% in 2024. Revenues in this category are projected to reach approximately USD 7,093.23 million, growing at a CAGR of 30.53% during the forecast period. This dominance is primarily driven by the widespread use of compact and lightweight batteries in two-wheelers, three-wheelers, and small commercial EVs. These batteries are well-suited for urban commuting and last-mile delivery applications, where frequent short trips and quick turnaround times make battery swapping highly efficient. Companies like Gogoro, Okinawa, and Ampere Vehicles are leading the adoption of sub-30 kWh batteries, developing modular, swappable packs that enable faster charging cycles and minimize vehicle downtime for both individual riders and fleet operators.

In comparison, the More than 30 kWh sub-segment, while currently smaller in market share, serves a critical role in supporting larger electric vehicles, including four-wheelers, light commercial vehicles, and high-capacity fleet vehicles. These higher-capacity batteries enable longer range and heavier payloads, which are particularly valuable for ride-hailing fleets, logistics, and commercial transportation where distance and energy efficiency are key considerations. Companies like NIO, CATL, and Sinopec are experimenting with advanced battery packs and hybrid swapping models for these vehicles, focusing on safety, thermal management, and extended battery life to ensure consistent performance under heavy usage.

Together, the dominance of less than 30 kWh batteries, the growing adoption of higher-capacity packs, and innovations in modular design and energy management illustrate the dynamic and adaptable nature of the battery swapping market. Smaller batteries drive rapid urban adoption and frequent usage, while larger batteries expand the ecosystem to commercial and long-distance mobility solutions. Collectively, these sub-segments highlight the market’s versatility in meeting diverse EV requirements, supporting both daily commuters and commercial operators while enabling scalable growth of battery-as-a-service (BaaS) infrastructure worldwide.

Global Battery Swapping Market, By Capacity (USD million)

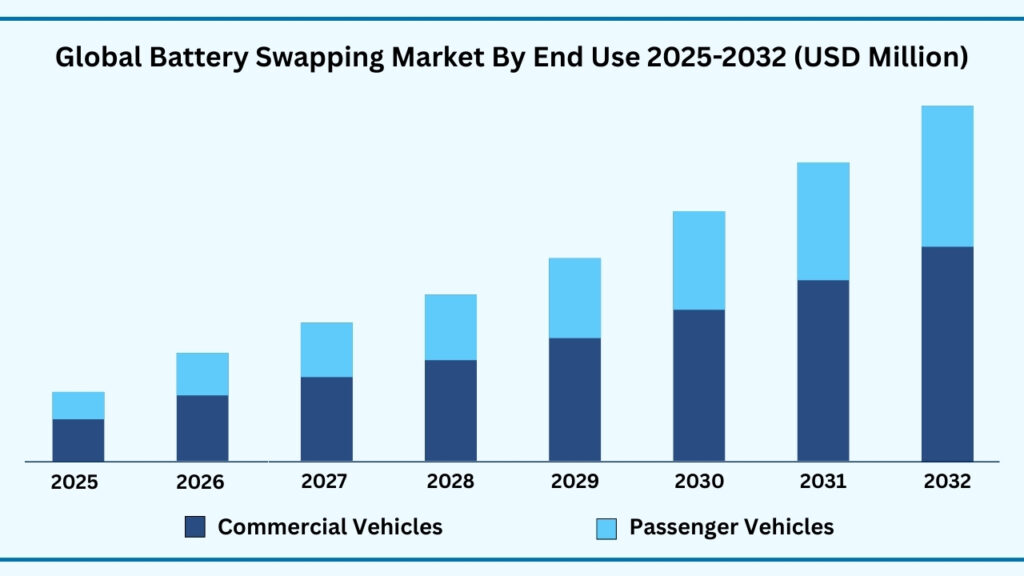

Global Battery Swapping Market by End Use Insights:

Commercial Vehicles segment accounted for market share of share 62.66% in 2024 in the global Battery Swapping market.

The Commercial Vehicles sub-segment holds the largest share of the global battery swapping market, accounting for 62.66% in 2024. Revenues in this category are projected to reach approximately USD 5,645.54 million, expanding at a CAGR of 30.53% during the forecast period. Commercial vehicles, including delivery vans, electric taxis, and fleet trucks, are increasingly adopting battery swapping due to its ability to minimize downtime and maximize operational efficiency. Fast and convenient battery exchange allows logistics operators and ride-hailing services to maintain continuous operations, improving service reliability and reducing total cost of ownership. Companies like NIO, CATL, and Okinawa are actively developing dedicated swap stations and subscription-based services tailored for commercial fleets, supporting large-scale adoption and operational scalability.

Beyond commercial vehicles, Passenger Vehicles are gradually emerging as an important sub-segment, particularly in urban environments where private EV adoption is rising. Swappable batteries offer private EV owners reduced charging times, convenience for daily commuting, and flexibility in long-distance travel. While currently smaller in market share, passenger vehicle adoption is being encouraged by OEM-led initiatives and pilot programs, such as those by Gogoro and NIO, which integrate automated or semi-automated swap stations for cars and light EVs. The availability of battery-as-a-service (BaaS) options and flexible subscription models is making battery swapping increasingly accessible and attractive for individual users.

Together, the dominance of commercial vehicles, the growing adoption among passenger vehicles, and the expansion of tailored infrastructure illustrate the versatility and strategic importance of the end-use segment in the battery swapping ecosystem. Commercial fleets drive immediate revenue and operational efficiencies, while passenger vehicles expand the market’s reach into individual mobility. Collectively, these sub-segments reinforce the role of battery swapping as a reliable, scalable, and user-friendly solution for diverse transportation needs, supporting the broader adoption of electric vehicles across both commercial and private sectors.

Global Battery Swapping Market, By End Use (USD million)

Global Battery Swapping Market by Region Insights:

Asia-Pacific segment accounted for market share of share 51.30% in 2024 in the global Battery Swapping market.

The Asia-Pacific sub-segment holds the largest share of the global battery swapping market, accounting for 51.30% in 2024. Revenues in this region are projected to reach approximately USD 4,617.70 million, growing at a CAGR of 30.52% during the forecast period. The region’s dominance is driven by high urbanization, strong EV adoption, and supportive government policies promoting sustainable transportation. Countries such as China, India, and Japan have established extensive battery swapping networks for two-wheelers, three-wheelers, and commercial fleets, enabling rapid deployment and reliable service. Companies like Gogoro, NIO, and Okinawa are actively expanding infrastructure in the region, leveraging modular swap stations and subscription-based services to meet growing consumer and commercial demand.

In comparison, North America and Europe represent significant but smaller shares of the market, focusing primarily on advanced technological adoption and fleet electrification. North America is witnessing growth in ride-hailing fleets and urban delivery services adopting battery swapping to reduce vehicle downtime, with companies like NIO and Tesla exploring pilot programs for swappable battery packs. Europe, meanwhile, benefits from government incentives, strict emission regulations, and strong EV penetration, particularly in countries such as Germany, Norway, and France. Operators are developing automated and semi-automated swap stations for both passenger and commercial vehicles, aiming to enhance efficiency and convenience while supporting sustainable mobility initiatives.

The LATAM and MEA regions, though currently smaller in market share, are emerging as promising growth areas due to increasing EV adoption, infrastructure development, and urbanization. Countries such as Brazil, Mexico, and the UAE are piloting battery swapping initiatives to support commercial fleets, public transportation, and last-mile logistics. These markets provide opportunities for flexible and innovative station models, including partnerships between OEMs and energy providers. Collectively, the dominance of Asia-Pacific, the technological advancements in North America and Europe, and the emerging adoption in LATAM and MEA illustrate the global and dynamic nature of the battery swapping market, highlighting its potential to support sustainable transportation and diverse mobility needs across regions.

Global Battery Swapping Market, By Region (USD million)

Major Companies and Competitive Landscape

The global battery swapping market is growing rapidly, driven by increasing electric vehicle adoption, rising demand for fast and convenient energy solutions, and supportive government policies promoting sustainable transportation. Companies are focusing on partnerships, acquisitions, and technological collaborations to expand swap station networks, develop advanced battery management systems, and innovate modular and automated swapping solutions. Efforts are also directed toward enhancing battery lifecycle, optimizing operational efficiency, and exploring new business models such as subscription-based and hybrid services. Key companies active in the global battery swapping market include:

- NIO Inc.

- Gogoro Inc.

- CATL (Contemporary Amperex Technology Co., Ltd.)

- Sun Mobility Pvt. Ltd.

- Battery Smart

- Aulton New Energy Automotive Technology Co., Ltd.

- Honda

- KYMCO (Ionex)

- Yadea Technology Group

- RACEnergy

- Ample

- Oyika

- Chargeup

- Quantum Energy

- Terpel

- Hero MotoCorp

- Ola Electric Mobility Pvt. Ltd.

- Honda Power Pack Energy India Pvt. Ltd.

- Tata Sons

- BattSwap Inc.

- Lithion Power

- VoltUp

- Esmito Solutions

- Immotor

- FENY Energy

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 1,395.24 Million |

| CAGR (2024–2032) | 30.49% |

| Revenue forecast to 2033 | USD 8,988.55 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Vehicle Type, By Battery Type, By Service Type, By Station, By Ownership, By Capacity, By End Use and By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, Rest of MEA |

| Key companies profiled | NIO Inc., Gogoro Inc., CATL, Sun Mobility Pvt. Ltd., Battery Smart, Aulton New Energy Automotive Technology Co., Ltd., Honda, KYMCO, Yadea Technology Group, RACEnergy, Ample, Oyika, Chargeup, Quantum Energy, Terpel, Hero MotoCorp, Ola Electric Mobility Pvt. Ltd., Honda Power Pack Energy India Pvt. Ltd., Tata Sons, BattSwap Inc., Lithion Power, VoltUp, Esmito Solutions, Immotor, and FENY Energy. |

| Customization scope | 10 hours of free customization and expert consultation |

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of global Human battery swapping market

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1.Primary

2.1.2.Secondary

2.1.3.Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1.Market value

2.3.2.Market volume

2.3.3.Exchange rate

2.3.4.Price

2.3.5.Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2019-2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10. Formulation & manufacturing

4.11. Distribution & retail

4.12. Import-export analysis

4.13. Brand comparative analysis

4.14. Technological advancements

4.15. Porter’s five force

4.15.1. Threat of new entrants

4.15.1.1. Capital requirment

4.15.1.2. Product knowledge

4.15.1.3. Technical knowledge

4.15.1.4. Customer relation

4.15.1.5. Access to appliation and technology

4.15.2. Threat of substitutes

4.15.2.1. Cost

4.15.2.2. Performance

4.15.2.3. Availability

4.15.2.4. Technical knowledge

4.15.2.5. Durability

4.15.3. Bargainning power of buyers

4.15.3.1. Numbers of buyers relative to suppliers

4.15.3.2. Product differentiation

4.15.3.3. Threat of forward integration

4.15.3.4. Buyers volume

4.15.4. Bargainning power of suppliers

4.15.4.1. Suppliers concentration

4.15.4.2. Buyers switching cost to other suppliers

4.15.4.3. Threat of backward integration

4.15.5. Bargainning power of suppliers

4.15.5.1. Industry concentration

4.15.5.2. Industry growth rate

4.15.5.3. Product differentiation

4.15.6. Patent analysis

4.16. Patent quality and strength

4.17. Regulation coverage

4.18. Pricing analysis

4.19. Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1.Rising adoption of electric vehicles (EVs) due to government incentives, emission

regulations, and growing environmental concerns fueling demand for fast-charging

alternatives like battery swapping

5.1.2.Increasing investments by EV manufacturers, energy companies, and mobility service

providers to build battery swapping infrastructure

5.1.3.Growing demand from commercial fleets, two-wheelers, and three-wheelers for cost-

effective, time-saving energy solutions

5.2. Restraints

5.2.1.High initial capital expenditure required for establishing battery swapping stations and

infrastructure

5.2.2.Lack of standardization in battery design, size, and compatibility across different EV

models

5.3. Opportunities

5.3.1.Emerging market potential in densely populated urban areas, last-mile delivery services,

and ride-hailing fleets

5.3.2.Integration of renewable energy and smart grid solutions with battery swapping networks

for sustainable energy use

5.3.3.Development of advanced battery technologies (solid-state, modular, and AI-enabled

monitoring) to enhance efficiency and safety in swapping systems

5.4. Threat

5.4.1.Competition from fast-charging infrastructure and advancements in ultra-fast charging

technologies

5.4.2.Policy and regulatory uncertainties regarding standardization, subsidies, and safety

guidelines for battery swapping

5.4.3.Supply chain risks related to critical raw materials (lithium, cobalt, nickel) and geopolitical

dependencies

Chapter 6. Global Battery Swapping Market By Vehicle Type Insights & Trends, Revenue (USD

Million)

6.1. Vehicle Type Dynamics & Market Share, 2019–2032

6.1.1.Two-Wheelers

6.1.2.Three-Wheelers

6.1.3.Four-Wheelers

Chapter 7. Global Battery Swapping Market By Battery Type Insights & Trends, Revenue (USD

Million)

7.1. Battery Type Dynamics & Market Share, 2019-2032

7.1.1.Lithium-Ion

7.1.2.Lead-Acid

7.1.3.Other

Chapter 8. Global Battery Swapping Market By Service Type Insights & Trends, Revenue (USD

Million)

8.1. Service Type Dynamics & Market Share, 2019-2032

8.1.1.Subscription-Based

8.1.2.Pay-Per-Use

8.1.3.Hybrid model

Chapter 9. Global Battery Swapping Market By Station Category Insights & Trends, Revenue

(USD Million)

9.1. Station Dynamics & Market Share, 2019-2032

9.1.1.Manual stations

9.1.2.Automated stations

9.1.3.Other

Chapter 10. Global Battery Swapping Market By Ownership Insights & Trends, Revenue (USD

Million)

10.1. Ownership Dynamics & Market Share, 2019-2032

10.1.1. Public swap station

10.1.2. Private swap station

Chapter 11. Global Battery Swapping Market By Capacity Insights & Trends, Revenue (USD

Million)

11.1. Capacity Dynamics & Market Share, 2019-2032

11.1.1. Less than 30 kWh

11.1.2. More than 30 kWh

Chapter 12. Global Battery Swapping Market By End Use Insights & Trends, Revenue (USD

Million)

12.1. End Use Dynamics & Market Share, 2019-2032

12.1.1. Commercial Vehicles

12.1.1.1. Two-Wheelers

12.1.1.2. Three-Wheelers

12.1.1.3. Four-Wheelers

12.1.2. Passenger Vehicles

12.1.2.1. Two-Wheelers

12.1.2.2. Three-Wheelers

12.1.2.3. Four-Wheelers

Chapter 13. Global Battery Swapping Market Regional Outlook

13.1.Global Battery Swapping Market Share By Region, 2019-2032

13.2. North America

13.3. Market By Vehicle Type, Market Estimates and Forecast, USD Million

13.3.1. Two-Wheelers

13.3.2. Three-Wheelers

13.3.3. Four-Wheelers

13.4. Market By Battery Type, Market Estimates and Forecast, USD Million

13.4.1. Lithium-Ion

13.4.2. Lead-Acid

13.4.3. Other

13.5. Market By Service Type, Market Estimates and Forecast, USD Million

13.5.1. Subscription-Based

13.5.2. Pay-Per-Use

13.5.3. Hybrid model

13.6. Market By Station Category, Market Estimates and Forecast, USD Million

13.6.1. Manual stations

13.6.2. Automated stations

13.6.3. Other

13.7. Market By Ownership, Market Estimates and Forecast, USD Million

13.7.1. Public swap station

13.7.2. Private swap station

13.8. Market By Capacity, Market Estimates and Forecast, USD Million

13.8.1. Less than 30 kWh

13.8.2. More than 30 kWh

13.9. Market End Use, Market Estimates and Forecast, USD Million

13.9.1. Commercial Vehicles

13.9.1.1. Two-Wheelers

13.9.1.2. Three-Wheelers

13.9.1.3. Four-Wheelers

13.9.2. Passenger Vehicles

13.9.2.1. Two-Wheelers

13.9.2.2. Three-Wheelers

13.9.2.3. Four-Wheelers

13.10. Market By Country, Market Estimates and Forecast, USD Million

13.10.1. US

13.10.2. Canada

13.10.3. Mexico

13.11. Europe

13.12. Market By Vehicle Type, Market Estimates and Forecast, USD Million

13.12.1. Two-Wheelers

13.12.2. Three-Wheelers

13.12.3. Four-Wheelers

13.13. Market By Battery Type, Market Estimates and Forecast, USD Million

13.13.1. Lithium-Ion

13.13.2. Lead-Acid

13.13.3. Other

13.14. Market By Service Type, Market Estimates and Forecast, USD Million

13.14.1. Subscription-Based

13.14.2. Pay-Per-Use

13.14.3. Hybrid model

13.15. Market By Station Category, Market Estimates and Forecast, USD Million

13.15.1. Manual stations

13.15.2. Automated stations

13.15.3. Other

13.16. Market By Ownership, Market Estimates and Forecast, USD Million

13.16.1. Public swap station

13.16.2. Private swap station

13.17. Market By Capacity, Market Estimates and Forecast, USD Million

13.17.1. Less than 30 kWh

13.17.2. More than 30 kWh

13.18. Market End Use, Market Estimates and Forecast, USD Million

13.18.1. Commercial Vehicles

13.18.1.1.Two-Wheelers

13.18.1.2.Three-Wheelers

13.18.1.3.Four-Wheelers

13.18.2. Passenger Vehicles

13.18.2.1.Two-Wheelers

13.18.2.2.Three-Wheelers

13.18.2.3.Four-Wheelers

13.18.3.Market By Country, Market Estimates and Forecast, USD Million

13.18.3.1. Germany

13.18.3.2. France

13.18.3.3. U.K

13.18.3.4. Italy

13.18.3.5. Spain

13.18.3.6. Benelux

13.18.3.7. Russia

13.18.3.8. Finland

13.18.3.9. Sweden

13.18.3.10. Rest Of Europe

13.19. Asia-Pacific

13.20. Market By Vehicle Type, Market Estimates and Forecast, USD Million

13.20.1. Two-Wheelers

13.20.2. Three-Wheelers

13.20.3. Four-Wheelers

13.21. Market By Battery Type, Market Estimates and Forecast, USD Million

13.21.1. Lithium-Ion

13.21.2. Lead-Acid

13.21.3. Other

13.22. Market By Service Type, Market Estimates and Forecast, USD Million

13.22.1. Subscription-Based

13.22.2. Pay-Per-Use

13.22.3. Hybrid model

13.23. Market By Station Category, Market Estimates and Forecast, USD Million

13.23.1. Manual stations

13.23.2. Automated stations

13.23.3. Other

13.24. Market By Ownership, Market Estimates and Forecast, USD Million

13.24.1. Public swap station

13.24.2. Private swap station

13.25. Market By Capacity, Market Estimates and Forecast, USD Million

13.25.1. Less than 30 kWh

13.25.2. More than 30 kWh

13.26. Market End Use, Market Estimates and Forecast, USD Million

13.26.1. Commercial Vehicles

13.26.1.1.Two-Wheelers

13.26.1.2.Three-Wheelers

13.26.1.3.Four-Wheelers

13.26.2. Passenger Vehicles

13.26.2.1.Two-Wheelers

13.26.2.2.Three-Wheelers

13.26.2.3.Four-Wheelers

13.27. Market By Country, Market Estimates and Forecast, USD Million

13.27.1. China

13.27.2. India

13.27.3. Japan

13.27.4. South Korea

13.27.5. Indonesia

13.27.6. Thailand

13.27.7. Vietnam

13.27.8. Australia

13.27.9. New Zeland

13.27.10. Rest of APAC

13.28. Latin America

13.29. Market By Vehicle Type, Market Estimates and Forecast, USD Million

13.29.1. Two-Wheelers

13.29.2. Three-Wheelers

13.29.3. Four-Wheelers

13.30. Market By Battery Type, Market Estimates and Forecast, USD Million

13.30.1. Lithium-Ion

13.30.2. Lead-Acid

13.30.3. Other

13.31. Market By Service Type, Market Estimates and Forecast, USD Million

13.31.1. Subscription-Based

13.31.2. Pay-Per-Use

13.31.3. Hybrid model

13.32. Market By Station Category, Market Estimates and Forecast, USD Million

13.32.1. Manual stations

13.32.2. Automated stations

13.32.3. Other

13.33. Market By Ownership, Market Estimates and Forecast, USD Million

13.33.1. Public swap station

13.33.2. Private swap station

13.34. Market By Capacity, Market Estimates and Forecast, USD Million

13.34.1. Less than 30 kWh

13.34.2. More than 30 kWh

13.35. Market End Use, Market Estimates and Forecast, USD Million

13.35.1. Commercial Vehicles

13.35.1.1.Two-Wheelers

13.35.1.2.Three-Wheelers

13.35.1.3.Four-Wheelers

13.35.2. Passenger Vehicles

13.35.2.1.Two-Wheelers

13.35.2.2.Three-Wheelers

13.35.2.3.Four-Wheelers

13.36. Market By Country, Market Estimates and Forecast, USD Million

13.36.1. Brazil

13.36.2. Rest of LATAM

13.37. Middle East & Africa

13.38. Market By Vehicle Type, Market Estimates and Forecast, USD Million

13.38.1. Two-Wheelers

13.38.2. Three-Wheelers

13.38.3. Four-Wheelers

13.39. Market By Battery Type, Market Estimates and Forecast, USD Million

13.39.1. Lithium-Ion

13.39.2. Lead-Acid

13.39.3. Other

13.40. Market By Service Type, Market Estimates and Forecast, USD Million

13.40.1. Subscription-Based

13.40.2. Pay-Per-Use

13.40.3. Hybrid model

13.41. Market By Station Category, Market Estimates and Forecast, USD Million

13.41.1. Manual stations

13.41.2. Automated stations

13.41.3. Other

13.42. Market By Ownership, Market Estimates and Forecast, USD Million

13.42.1. Public swap station

13.42.2. Private swap station

13.43. Market By Capacity, Market Estimates and Forecast, USD Million

13.43.1. Less than 30 kWh

13.43.2. More than 30 kWh

13.44. Market End Use, Market Estimates and Forecast, USD Million

13.44.1. Commercial Vehicles

13.44.1.1.Two-Wheelers

13.44.1.2.Three-Wheelers

13.44.1.3.Four-Wheelers

13.44.2. Passenger Vehicles

13.44.2.1.Two-Wheelers

13.44.2.2.Three-Wheelers

13.44.2.3.Four-Wheelers

13.45. Market By Country, Market Estimates and Forecast, USD Million

13.45.1. Saudi Arabia

13.45.2. UAE

13.45.3. South Africa

13.45.4. Turkey

13.45.5. Rest of MEA

Chapter 14. Competitive Landscape

14.1. Market Revenue Share By Manufacturers

14.2. Mergers & Acquisitions

14.3. Competitor’s Positioning

14.4. Strategy Benchmarking

14.5. Vendor Landscape

14.6. Distributors

14.6.1.North America

14.6.2.Europe

14.6.3.Asia Pacific

14.6.4.Middle East & Africa

14.6.5.Latin America

14.7. Others

Chapter 15. Company Profiles

15.1. NIO Inc.

15.1.1. Company Overview

15.1.2. Product & Service Offerings

15.1.3. Strategic Initiatives

15.1.4. Financials

15.1.5. Conclusion

15.2. Gogoro Inc.

15.2.1. Company Overview

15.2.2. Product & Service Offerings

15.2.3. Strategic Initiatives

15.2.4. Financials

15.2.5. Conclusion

15.3. CATL (Contemporary Amperex Technology Co., Ltd.)

15.3.1. Company Overview

15.3.2. Product & Service Offerings

15.3.3. Strategic Initiatives

15.3.4. Financials

15.3.5. Conclusion

15.4. Sun Mobility Pvt. Ltd.

15.4.1. Company Overview

15.4.2. Product & Service Offerings

15.4.3. Strategic Initiatives

15.4.4. Financials

15.4.5. Conclusion

15.5. Battery Smart

15.5.1. Company Overview

15.5.2. Product & Service Offerings

15.5.3. Strategic Initiatives

15.5.4. Financials

15.5.5. Conclusion

15.6. Aulton New Energy Automotive Technology Co., Ltd.

15.6.1. Company Overview

15.6.2. Product & Service Offerings

15.6.3. Strategic Initiatives

15.6.4. Financials

15.6.5. Conclusion

15.7. Honda

15.7.1. Company Overview

15.7.2. Product & Service Offerings

15.7.3. Strategic Initiatives

15.7.4. Financials

15.7.5. Conclusion

15.8. KYMCO (Ionex)

15.8.1. Company Overview

15.8.2. Product & Service Offerings

15.8.3. Strategic Initiatives

15.8.4. Financials

15.8.5. Conclusion

15.9. Yadea Technology Group

15.9.1. Company Overview

15.9.2. Product & Service Offerings

15.9.3. Strategic Initiatives

15.9.4. Financials

15.9.5. Conclusion

15.10. RACEnergy

15.10.1. Company Overview

15.10.2. Product & Service Offerings

15.10.3. Strategic Initiatives

15.10.4. Financials

15.10.5. Conclusion

15.11. Ample

15.11.1. Company Overview

15.11.2. Product & Service Offerings

15.11.3. Strategic Initiatives

15.11.4. Financials

15.11.5. Conclusion

15.12. Oyika

15.12.1. Company Overview

15.12.2. Product & Service Offerings

15.12.3. Strategic Initiatives

15.12.4. Financials

15.12.5. Conclusion

15.13. Chargeup

15.13.1. Company Overview

15.13.2. Product & Service Offerings

15.13.3. Strategic Initiatives

15.13.4. Financials

15.13.5. Conclusion

15.14. Quantum Energy

15.14.1. Company Overview

15.14.2. Product & Service Offerings

15.14.3. Strategic Initiatives

15.14.4. Financials

15.14.5. Conclusion

15.15. Terpel

15.15.1. Company Overview

15.15.2. Product & Service Offerings

15.15.3. Strategic Initiatives

15.15.4. Financials

15.15.5. Conclusion

15.16. Hero MotoCorp

15.16.1. Company Overview

15.16.2. Product & Service Offerings

15.16.3. Strategic Initiatives

15.16.4. Financials

15.16.5. Conclusion

15.17. Ola Electric Mobility Pvt. Ltd.

15.17.1. Company Overview

15.17.2. Product & Service Offerings

15.17.3. Strategic Initiatives

15.17.4. Financials

15.17.5. Conclusion

15.18. Honda Power Pack Energy India Pvt. Ltd.

15.18.1. Company Overview

15.18.2. Product & Service Offerings

15.18.3. Strategic Initiatives

15.18.4. Financials

15.18.5. Conclusion

15.19. Tata Sons

15.19.1. Company Overview

15.19.2. Product & Service Offerings

15.19.3. Strategic Initiatives

15.19.4. Financials

15.19.5. Conclusion

15.20. BattSwap Inc.

15.20.1. Company Overview

15.20.2. Product & Service Offerings

15.20.3. Strategic Initiatives

15.20.4. Financials

15.20.5. Conclusion

15.21. Lithion Power

15.21.1. Company Overview

15.21.2. Product & Service Offerings

15.21.3. Strategic Initiatives

15.21.4. Financials

15.21.5. Conclusion

15.22. VoltUp

15.22.1. Company Overview

15.22.2. Product & Service Offerings

15.22.3. Strategic Initiatives

15.22.4. Financials

15.22.5. Conclusion

15.23. Esmito Solutions

15.23.1. Company Overview

15.23.2. Product & Service Offerings

15.23.3. Strategic Initiatives

15.23.4. Financials

15.23.5. Conclusion

15.24. Immotor

15.24.1. Company Overview

15.24.2. Product & Service Offerings

15.24.3. Strategic Initiatives

15.24.4. Financials

15.24.5. Conclusion

15.25. FENY Energy

15.25.1. Company Overview

15.25.2. Product & Service Offerings

15.25.3. Strategic Initiatives

15.25.4. Financials

15.25.5. Conclusion

Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP. has segmented global Battery Swapping market on the basis of By Vehicle Type, By Battery Type, By Service Type, By Station Category, By Ownership, By Capacity, By End Use and by region for 2019 to 2032.

- Global Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Global Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Global Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Global Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Global Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Global Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Global End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- North America

- North America Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- North America Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- North America Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- North America Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- North America Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- North America Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- North America End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- U.S

- U.S Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- U.S Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- U.S Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- U.S Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- U.S Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- U.S Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- U.S End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Canada

- Canada Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Canada Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Canada Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Canada Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Canada Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Canada Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Canada End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Mexico

- Mexico Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Mexico Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Mexico Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Mexico Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Mexico Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Mexico Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Mexico End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Europe

- Europe Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Europe Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Europe Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Europe Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Europe Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Europe Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Europe End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Germany

- Germany Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Germany Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Germany Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Germany Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Germany Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Germany Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Germany End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- France

- France Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- France Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- France Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- France Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- France Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- France Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- France End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- U.K

- U.K Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- U.K Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- U.K Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- U.K Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- U.K Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- U.K Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- U.K End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Italy

- Italy Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Italy Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Italy Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Italy Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Italy Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Italy Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Italy End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Spain

- Spain Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Spain Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Spain Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Spain Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Spain Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Spain Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Spain End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Benelux

- Benelux Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Benelux Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Benelux Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Benelux Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Benelux Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Benelux Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Benelux End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Russia

- Russia Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Russia Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Russia Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Russia Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Russia Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Russia Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Russia End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Finland

- Finland Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Finland Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Finland Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Finland Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Finland Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Finland Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Finland End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Sweden

- Sweden Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Sweden Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Sweden Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Sweden Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Sweden Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Sweden Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Sweden End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Rest of Europe

- Rest of Europe Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Rest of Europe Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Rest of Europe Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Rest of Europe Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Rest of Europe Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Rest of Europe Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Rest of Europe End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Asia-Pacific

- Asia-Pacific Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Asia-Pacific Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Asia-Pacific Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Asia-Pacific Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Asia-Pacific Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Asia-Pacific Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Asia-Pacific End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- China

- China Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- China Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- China Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- China Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- China Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- China Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- China End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- India

- India Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- India Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- India Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- India Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- India Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- India Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- India End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Japan

- Japan Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Japan Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Japan Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Japan Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Japan Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Japan Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Japan End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- South Korea

- South Korea Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- South Korea Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- South Korea Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- South Korea Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- South Korea Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- South Korea Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- South Korea End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Indonesia

- Indonesia Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Indonesia Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Indonesia Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Indonesia Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Indonesia Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Indonesia Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Indonesia End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Vietnam

- Vietnam Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Vietnam Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Vietnam Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Vietnam Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Vietnam Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Vietnam Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Vietnam End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Australia

- Australia Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Australia Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Australia Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Australia Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Australia Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Australia Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Australia End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- New Zeeland

- New Zeeland Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- New Zeeland Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- New Zeeland Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- New Zeeland Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- New Zeeland Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- New Zeeland Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- New Zeeland End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Rest of APAC

- Rest of APAC Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Rest of APAC Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Rest of APAC Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Rest of APAC Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Rest of APAC Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Rest of APAC Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Rest of APAC End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Latin America

- Latin America Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Latin America Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Latin America Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Latin America Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Latin America Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Latin America Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Latin America End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Brazil

- Brazil Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Brazil Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Brazil Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Brazil Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Brazil Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Brazil Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Brazil End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Rest of LATAM

- Rest of LATAM Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Rest of LATAM Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Rest of LATAM Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Rest of LATAM Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Rest of LATAM Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Rest of LATAM Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Rest of LATAM End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Middle East & Africa

- Middle East & Africa Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Middle East & Africa Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Middle East & Africa Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Middle East & Africa Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Middle East & Africa Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Middle East & Africa Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Middle East & Africa End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- Saudi Arabia

- Saudi Arabia Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Saudi Arabia Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- Saudi Arabia Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- Saudi Arabia Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- Saudi Arabia Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- Saudi Arabia Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh

- Saudi Arabia End Use Outlook (Revenue, USD Million; 2019-2032)

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Passenger Vehicles

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- Commercial Vehicles

- UAE

- UAE Vehicle Type Outlook (Revenue, USD Million; 2019-2032)

- Two-Wheelers

- Three-Wheelers

- Four-Wheelers

- UAE Battery Type Outlook (Revenue, USD Million; 2019-2032)

- Lithium-Ion

- Lead-Acid

- Other

- UAE Service Type Outlook (Revenue, USD Million; 2019-2032)

- Subscription-Based

- Pay-Per-Use

- Hybrid model

- UAE Station Category Outlook (Revenue, USD Million; 2019-2032)

- Manual stations

- Automated stations

- Other

- UAE Ownership Outlook (Revenue, USD Million; 2019-2032)

- Public swap station

- Private swap station

- UAE Capacity Outlook (Revenue, USD Million; 2019-2032)

- Less than 30 kWh

- More than 30 kWh