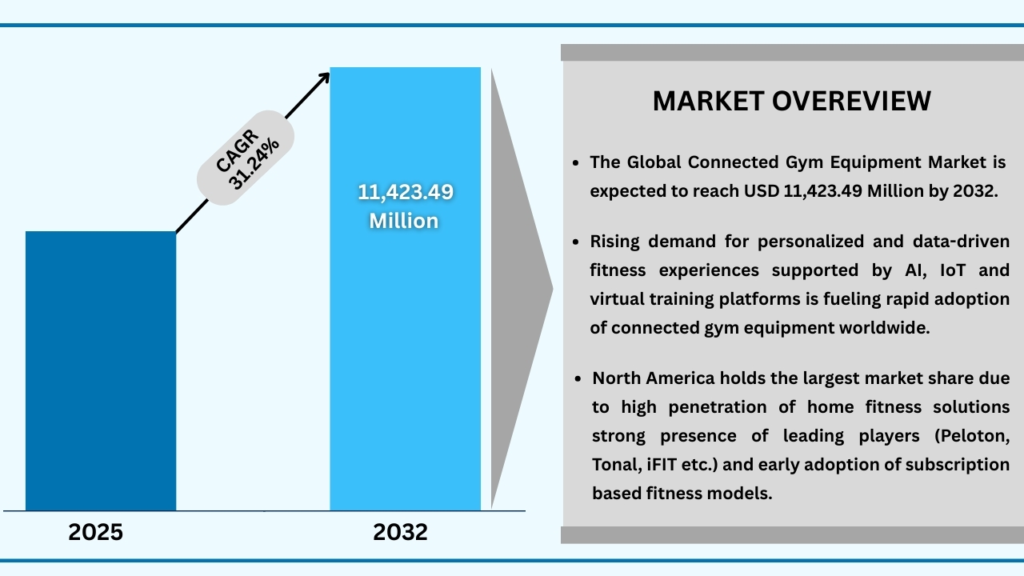

Market Synopsis

The global Connected Gym Equipment market was valued at USD 1,310.17 million in 2024 and is projected to reach USD 11,423.49 million by 2032, growing at a strong CAGR of 31.24%. The Connected Gym Equipment market is expanding rapidly, driven by the increasing consumer demand for personalized, tech-enabled fitness experiences. The integration of artificial intelligence, IoT, and advanced data analytics into fitness machines is enabling users to track progress, receive real-time feedback, and access interactive workout sessions. This shift toward digital fitness ecosystems is further supported by the growing popularity of virtual training platforms and subscription-based models, which deliver flexibility, motivation, and convenience to users across both home and commercial fitness settings. Rising health awareness, busy lifestyles, and the need for preventive healthcare are also pushing consumers to invest in smart fitness solutions that combine innovation with performance tracking.

North America leads the market due to its early adoption of digital technologies, strong presence of major connected fitness brands, and higher consumer willingness to pay for subscription-based training services. In parallel, Asia-Pacific is emerging as a high-growth region as urbanization, digital penetration, and rising disposable incomes drive demand for connected fitness equipment. Across regions, the blending of in-gym solutions with at-home connected fitness ecosystems is creating a hybrid fitness culture, shaping the industry’s future trajectory. With technology increasingly becoming central to how individuals manage their wellness, connected gym equipment is positioned as a cornerstone of the global fitness transformation.

Global Connected Gym Equipment Market (USD Million)

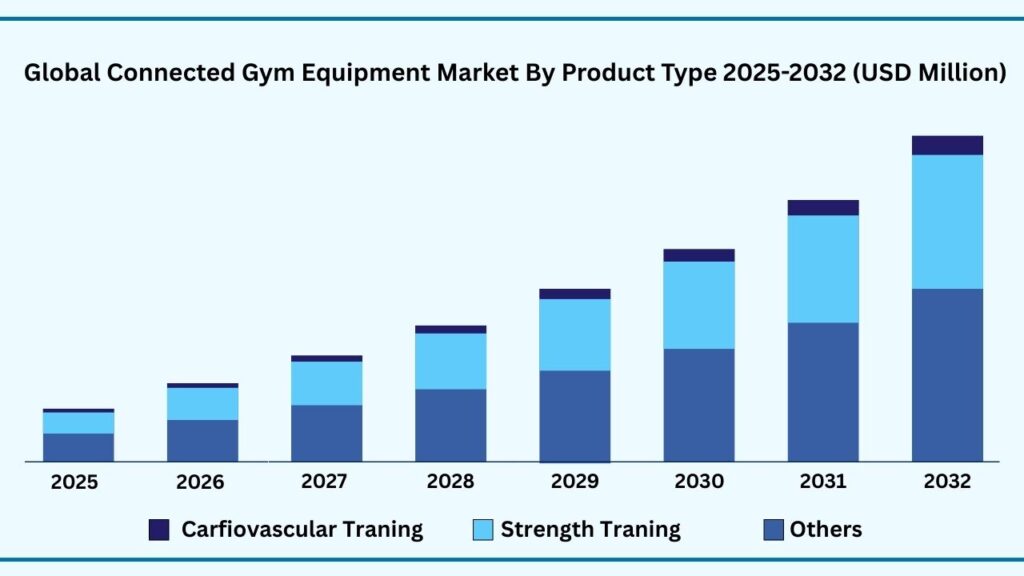

Global Connected Gym Equipment Market by Product Type Insights:

Cardiovascular Training segment accounted for market share of share 50.11% in 2024 in the global Connected Gym Equipment market.

The Cardiovascular Training segment accounted for the largest share of the global Connected Gym Equipment market in 2024, representing 50.11% of total revenues. Cardiovascular Training segment is expected to register a CAGR of 31.61 % during the forecast year from 2025 to 2032 and expected to reach USD 5,838.55 million in 2032. The Cardiovascular Training segment dominates the global Connected Gym Equipment market, driven by the rising consumer preference for equipment that supports weight management, endurance building, and overall heart health. Smart treadmills, stationary bikes, rowing machines, and elliptical trainers are increasingly equipped with connected features such as real-time performance tracking, AI-enabled coaching, and immersive virtual training sessions. The appeal of cardio equipment lies in its ability to deliver comprehensive health benefits while integrating seamlessly with fitness apps and wearable devices, offering users a holistic and connected fitness experience. Growing awareness about lifestyle-related diseases and the global trend toward preventive healthcare are further fueling demand for connected cardiovascular equipment across gyms, corporate wellness programs, and home setups.

This segment’s growth is also strongly supported by the popularity of subscription-based workout platforms that pair with cardio machines to deliver engaging, on-demand training. North America has been a frontrunner, with companies like Peloton and iFIT revolutionizing connected cycling and treadmill experiences, while Asia-Pacific is seeing rapid adoption due to urbanization and rising digital fitness penetration. Moreover, the integration of gamification, live leaderboards, and virtual community participation has made connected cardio training more interactive, motivating, and sustainable for users. With these innovations, cardiovascular equipment is expected to remain the largest revenue contributor in the connected fitness ecosystem, shaping the future of both home and commercial fitness markets.

Global Connected Gym Equipment Market by Product Type (USD Million)

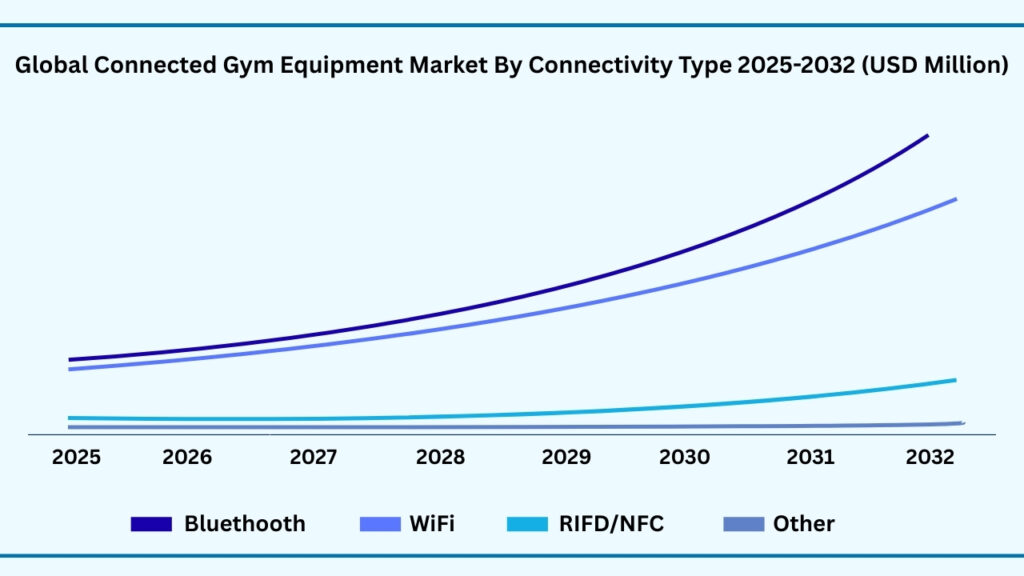

Global Connected Gym Equipment Maret by Connectivity Type Insights:

Bluetooth segment accounted for the largest market share of share 39.10% in 2024 in the global Connected Gym Equipment market.

Based on the connectivity type, Bluetooth segment held the largest revenue share of 39.10% in 2024, and expected to register a CAGR of 31.49% between 2025 to 2032 and the market is expected to reach USD 5,709.46 million by 2032. The Bluetooth segment holds the largest share of the Connected Gym Equipment market due to its widespread compatibility, cost-effectiveness, and ease of integration across fitness devices. Most smart fitness machines, including treadmills, bikes, and strength training equipment, rely on Bluetooth technology to sync seamlessly with smartphones, tablets, and wearables. This allows users to track real-time performance metrics such as heart rate, calories burned, and workout intensity while connecting to popular fitness apps. The simplicity of Bluetooth setup, combined with its low energy consumption and ability to provide stable short-range connectivity, has made it the preferred choice for manufacturers as well as consumers.

Growth in this segment is also being fueled by the rising demand for at-home fitness solutions and the popularity of hybrid training models where Bluetooth-enabled devices connect users to digital platforms and subscription-based content. The technology’s adaptability across both residential and commercial gyms ensures that it remains the standard choice for entry- to mid-range connected equipment, while complementing advanced IoT ecosystems. As consumer expectations evolve toward personalized and interactive workouts, Bluetooth’s role as the backbone of data sharing and device interoperability will continue to strengthen, maintaining its position as the largest connectivity type in the connected gym equipment industry.

Global Connected Gym Equipment Market by Connectivity Type (USD Million)

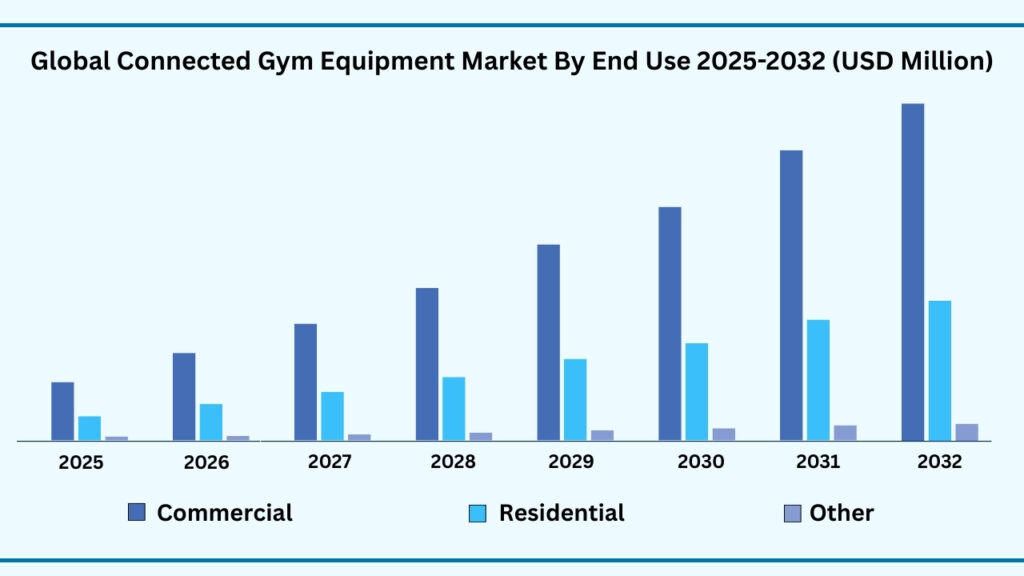

Global Connected Gym Equipment Maret by End Use Insights:

Commercial segment accounted for the largest market share of share 79.21% in 2024 in the global Connected Gym Equipment market.

Based on end use, Commercial segment held the largest revenue share of 79.21% in the global Connected Gym Equipment market in 2024 and expected to register a CAGR of 31.48% from 2025 to 2032 and expected to reach USD 9,162.78 million. The Commercial segment dominates the global Connected Gym Equipment market, largely due to the rapid digital transformation of gyms, health clubs, fitness studios, and corporate wellness centers. With the rising demand for personalized fitness experiences, commercial facilities are investing heavily in connected machines such as treadmills, bikes, and strength systems that integrate with apps, wearables, and subscription-based platforms. These solutions not only enhance the member experience through real-time performance tracking and interactive virtual training but also allow operators to improve client engagement, retention, and overall service value. Moreover, the growing emphasis on preventive healthcare and workplace wellness programs is pushing institutions and corporations to deploy advanced connected fitness equipment on a larger scale.

This segment’s growth is further supported by the strong presence of international gym chains and boutique fitness studios that differentiate themselves through premium digital fitness offerings. The ability of connected equipment to provide data-driven insights, gamification features, and remote monitoring has become a key driver in attracting tech-savvy consumers who seek immersive and motivating workout environments. Additionally, commercial adoption benefits from scalable subscription and service models, where gyms can bundle digital content with memberships to create recurring revenue streams. As the hybrid fitness culture evolves, combining in-person training with digital integration, the commercial sector is expected to remain the largest contributor to connected gym equipment revenues, shaping the global fitness landscape.

Global Connected Gym Equipment Market by End Use (USD Million)

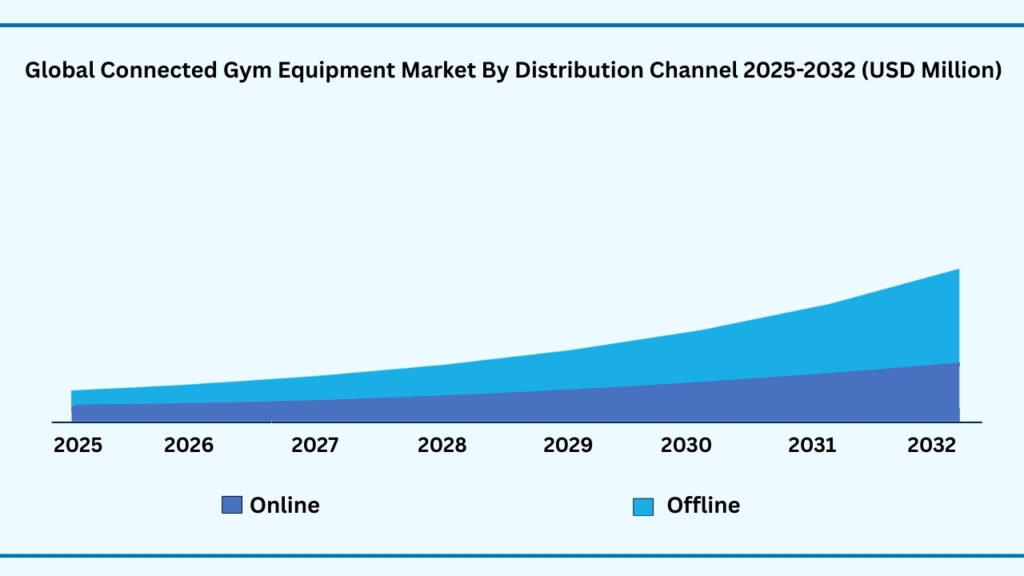

Global Connected Gym Equipment Market by Distribution Channel Insights:

Offline segment accounted for the largest market share of share of 65.78% in 2024 in the global Connected Gym Equipment market.

Based on distribution channel, offline segment held the largest revenue share of 65.78% in the global Connected Gym Equipment market in 2024 and expected to register a CAGR of 30.90% from 2024 to 2032 and expected to reach USD 7,427.55 million in 2032. The Offline segment continues to hold the largest share of the global Connected Gym Equipment market, supported by the strong presence of specialty fitness stores, sporting goods retailers, and large-format retail chains. Consumers often prefer purchasing high-value connected fitness machines such as treadmills, bikes, and strength equipment in person, where they can test functionality, evaluate features, and receive expert guidance before making an investment. Offline channels also provide immediate after-sales support, installation services, and financing options, which play a crucial role in influencing purchase decisions, particularly for commercial buyers such as gyms and wellness centers. This hands-on experience and trust factor have made offline sales the dominant channel despite the growth of e-commerce.

In addition, the offline segment benefits from the strategies of leading fitness equipment manufacturers who partner with distributors and authorized retailers to expand market presence and brand visibility. Many commercial facilities rely on direct dealership networks to procure equipment in bulk, ensuring service reliability and long-term maintenance contracts. The presence of demo zones, product showcases, and exclusive offline promotions further enhances customer engagement. While online channels are growing rapidly, the offline channel’s ability to deliver personalized consultation, bundled service packages, and real-time product trials ensures it remains the preferred choice for a large segment of consumers and enterprises in the connected gym equipment market.

Global Connected Gym Equipment by Distribution Channel (USD Million)

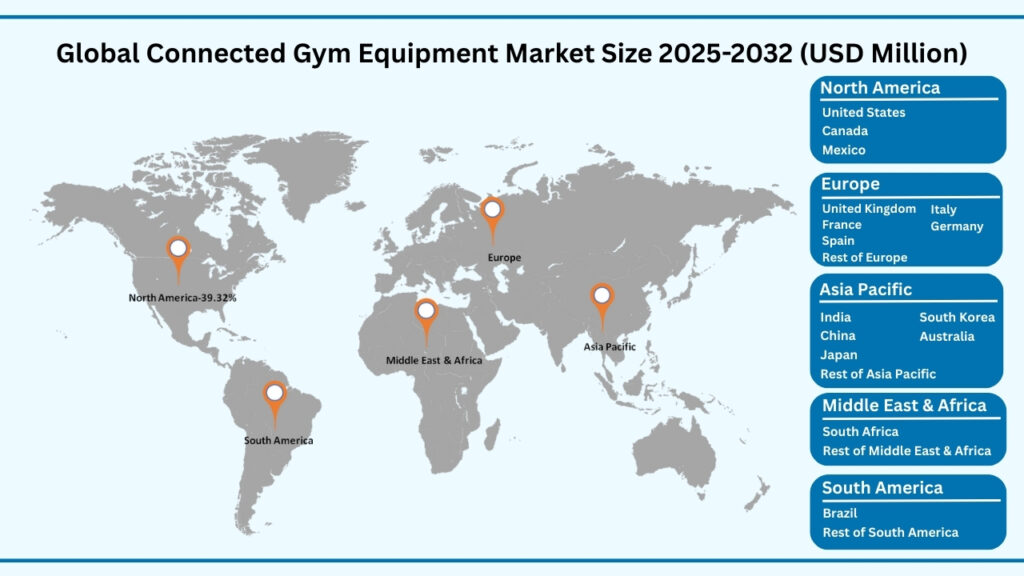

Global Connected Gym Equipment Market by Region Insights:

North America segment accounted for the largest market share of share of 39.32% in 2024 in the global Connected Gym Equipment market.

Based on region, the global Connected Gym Equipment market is segmented into Europe, Asia-Pacific, North America, Latin America and Middle East & Africa. Among these, North America region held the largest revenue share of 39.32% in the global Connected Gym Equipment market in 2024 and expected to register a CAGR of 31.62% from 2024 to 2032 and expected to reach USD 4,583.10 million in 2032. North America held the largest share of the global Connected Gym Equipment market, driven by the region’s early adoption of digital fitness technologies and the strong presence of leading players such as Peloton, Tonal, and iFIT. Consumers in the U.S. and Canada have shown a high willingness to invest in smart fitness machines that offer personalized training, data-driven insights, and seamless connectivity with apps and wearables. The popularity of subscription-based fitness platforms, coupled with the rise of home gyms, has further accelerated adoption across residential users, while commercial gyms and wellness centers are increasingly integrating connected equipment to attract and retain members. Additionally, rising health awareness, increasing rates of obesity, and a shift toward preventive healthcare are creating strong demand for connected cardiovascular and strength-training solutions across the region.

The market in North America is also supported by well-developed infrastructure, higher disposable incomes, and a tech-savvy population that embraces innovations such as AI-driven coaching, gamification, and immersive virtual training. The region’s fitness ecosystem benefits from strategic partnerships between fitness equipment manufacturers, digital platforms, and wellness apps, creating an integrated and engaging user experience. Moreover, corporate wellness initiatives and institutional investments in advanced gym facilities are boosting commercial adoption. With the blending of at-home and in-gym digital fitness experiences becoming a long-term trend, North America is expected to remain the leading regional market, setting benchmarks for innovation and shaping the global connected fitness industry.

Global Connected Gym Equipment Market by Region (USD Million)

Major Companies and Competitive Landscape

The global Connected Gym Equipment market is highly fragmented, featuring a mix of established multinational corporations and emerging startups competing for market share. Major players are actively pursuing strategies such as mergers and acquisitions, partnerships with technology providers, collaborations with fitness platforms, and alliances with commercial gyms and wellness chains to expand their reach. Companies are also investing heavily in product innovation, developing smart treadmills, stationary bikes, ellipticals, rowing machines, and strength-training systems with advanced AI, IoT, AR/VR integration, and personalized digital content to meet evolving consumer expectations. These innovations focus on enhancing user engagement, performance tracking, and seamless connectivity across both home and commercial fitness environments.

In addition, leading players are increasingly emphasizing sustainability, energy efficiency, and user-centric design to strengthen brand loyalty and appeal to health-conscious, tech-savvy consumers. The growing demand for hybrid fitness models that combine in-gym experiences with connected at-home workouts is pushing companies to refine their offerings with interactive features, subscription-based platforms, and gamification elements. Strategic investments in digital ecosystems, premiumization, and regional expansion are enabling broader accessibility, while ongoing regulatory compliance and service support initiatives are ensuring reliability and user trust. This focus on innovation, connectivity, and experience-driven solutions is driving growth and shaping the future of the global Connected Gym Equipment market.

Some of the leading companies profiled in the global Connected Gym Equipment market report include:

- Peloton Interactive

- Tonal Systems

- FIT / NordicTrack (ICON Health & Fitness)

- Technogym

- Echelon Fitness

- Hydrow

- Temp

- AXJOX

- Aviron

- Concept2

- Bowflex

- Life Fitness.

- Precor

- Johnson Health Tech

- EGYM

- OxeFit

- Ergatta

Strategic Development

Resale Platform Launch: In September 2025, Peloton introduced “Repowered,” a resale marketplace for used Peloton bikes and accessories, initially available in select U.S. cities. Sellers receive 70% of the sale price in cash, and buyers benefit from product history access and optional delivery services.

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 1,310.17 Million |

| CAGR (2024–2032) | 31.24% |

| Revenue forecast to 2033 | USD 11,423.49 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Product Type, By Connectivity Type, By Distribution Channel By End Use and By region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, Rest of MEA |

| Key companies profiled | “Peloton Interactive, Tonal Systems, FIT / NordicTrack (ICON Health & Fitness), Technogym, Echelon Fitness, Hydrow, Temp, AXJOX, Aviron, Concept2, Bowflex, Life Fitness., Precor, Johnson Health Tech, EGYM, OxeFit, Ergatta, FightCamp, TRUE Fitness, Matrix Fitness, Keiser, Cybex, Rogue Fitness, Core Health & Fitness, ICON Health & Fitness |

| Customization scope | 10 hours of free customization and expert consultation |

Some Key Questions the Report Will Answer

- What is the expected revenue Compound Annual Growth Rate (CAGR) of the global Connected Gym Equipment market over the forecast period (2025–2032)?

- The global Connected Gym Equipment market revenue is expected to register a Compound Annual Growth Rate (CAGR) of 31.24% during the forecast period.

- What was the size of the global Connected Gym Equipment in 2024?

- The global alkyl amines market size was USD 1,310.17 Million in 2024.

- Which factors are expected to drive the global Connected Gym Equipment market growth?

- Technological Advancements: The integration of Artificial Intelligence (AI), Internet of Things (IoT), and virtual reality into gym equipment has revolutionized the fitness experience. These technologies enable real-time performance tracking, personalized workout plans, and immersive training environments, enhancing user engagement and satisfaction.

- Which was the leading segment in the global Connected Gym Equipment market in terms of product type in 2024?

- Cardiovascular Training segment was leading in the Connected Gym Equipment market on the basis of product form in 2024.

- What are some restraints for revenue growth of the global Connected Gym Equipment market?

- High Initial Investment: The premium pricing of connected gym equipment, often exceeding USD 1,000 per unit, may deter budget-conscious consumers. This high upfront cost can limit accessibility, particularly in emerging markets where disposable income is lower.

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of Connected Fitness Equipment Market

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1.Primary

2.1.2.Secondary

2.1.3.Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1.Market value

2.3.2.Market volume

2.3.3.Exchange rate

2.3.4.Price

2.3.5.Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2019–2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10. Formulation & manufacturing

4.11. Distribution & retail

4.12. Import-export analysis

4.13. Brand comparative analysis

4.14. Technological advancements

4.15. Porter’s five force

4.15.1. Threat of new entrants

4.15.1.1. Capital requirment

4.15.1.2. Product knowledge

4.15.1.3. Technical knowledge

4.15.1.4. Customer relation

4.15.1.5. Access to appliation and technology

4.15.2. Threat of substitutes

4.15.2.1. Cost

4.15.2.2. Performance

4.15.2.3. Availability

4.15.2.4. Technical knowledge

4.15.2.5. Durability

4.15.3. Bargainning power of buyers

4.15.3.1. Numbers of buyers relative to suppliers

4.15.3.2. Product differentiation

4.15.3.3. Threat of forward integration

4.15.3.4. Buyers volume

4.15.4. Bargainning power of suppliers

4.15.4.1. Suppliers concentration

4.15.4.2. Buyers switching cost to other suppliers

4.15.4.3. Threat of backward integration

4.15.5. Bargainning power of suppliers

4.15.5.1. Industry concentration

4.15.5.2. Industry growth rate

4.15.5.3. Product differentiation

4.16. Patent analysis

4.17. Regulation coverage

4.18. Pricing analysis

4.19. Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1. Rising Health & Wellness Awareness

5.1.2. Growth of Home Fitness & Hybrid Models

5.1.3. Technology Integration & Personalization

5.2. Restraints

5.2.1. High Initial Cost & Subscription Dependency

5.2.2. Data Privacy & Security Concerns

5.3. Opportunities

5.3.1. Emerging Markets Adoption

5.3.2. Corporate Wellness & Institutional Demand

5.3.3. Integration with Wearables & Health Ecosystems

5.3.4. Expansion in minimally invasive surgery

5.4. Challenges

5.4.1. Intense Competition & Rapid Tech Evolution

5.4.2. Low Equipment Utilization & Customer Retention

Chapter 6. Global Connected Fitness Equipment Market By Product Type Insights & Trends,

Revenue (USD Million)

6.1. Product Type Dynamics & Market Share, 2019–2032

6.1.1.1. Cardiovascular training

6.1.1.1.1. Treadmills

6.1.1.1.2. Stationary Bikes

6.1.1.1.3. Ellipticals / Cross Trainers

6.1.1.1.4. Rowing Machines

6.1.1.1.5. Stair Climbers / Steppers

6.1.1.1.6. Spin & Air Bikes

6.1.1.1.7. Other

6.1.1.2. Strength training

6.1.1.2.1. Smart Resistance Machines

6.1.1.2.2. Free Weights & Dumbbells

6.1.1.2.3. Cables & Racks

6.1.1.2.4. Suspension & Bodyweight

6.1.1.2.5. AI-Based Smart Mirrors

6.1.1.2.6. Other

6.1.1.3. Other

Chapter 7. Global Connected Fitness Equipment Market By Connectivity Type Insights & Trends,

Revenue (USD Million)

7.1. Connectivity Type Dynamics & Market Share, 2019–2032

7.1.1. Bluetooth

7.1.2. WiFi

7.1.3. RFID / NFC

7.1.4. Other

Chapter 8. Global Connected Fitness Equipment Market By End Use Insights & Trends, Revenue

(USD Million)

8.1. End Use Dynamics & Market Share, 2019–2032

8.1.1.Residential

8.1.2.Commercial

8.1.3.Other

Chapter 9. Global Connected Fitness Equipment Market By Distribution Channel Insights &

Trends, Revenue (USD Million)

9.1. Distribution Channel & Market Share, 2019–2032

9.1.1. Offline

9.1.1.1. Specialty Fitness Equipment Stores

9.1.1.2. Sporting Goods Retailers

9.1.1.3. Electronics & Lifestyle Stores

9.1.1.4. Commercial Sales (B2B)

9.1.1.5. Dealer/Distributor Networks

9.1.2. Online

9.1.2.1. Brand-Owned E-commerce Platforms

9.1.2.2. E-commerce Marketplaces

9.1.2.3. Fitness Apps + Hardware Bundles

9.1.2.4. Flash Sale / Discount Portals

Chapter 10. Global Connected Fitness Equipment Market Regional Outlook

10.1. Connected Fitness Equipment Share By Region, 2019–2032

10.2. North America

10.2.1. Market By Product Type Estimates and Forecast, USD Million, 2019-2032

10.2.1.1. Cardiovascular training

10.2.1.1.1. Treadmills

10.2.1.1.2. Stationary Bikes

10.2.1.1.3. Ellipticals / Cross Trainers

10.2.1.1.4. Rowing Machines

10.2.1.1.5. Stair Climbers / Steppers

10.2.1.1.6. Spin & Air Bikes

10.2.1.1.7. Other

10.2.1.2. Strength training

10.2.1.2.1. Smart Resistance Machines

10.2.1.2.2. Free Weights & Dumbbells

10.2.1.2.3. Cables & Racks

10.2.1.2.4. Suspension & Bodyweight

10.2.1.2.5. AI-Based Smart Mirrors

10.2.1.2.6. Other

10.2.1.3. Other

10.2.2. Market By Connectivity Type, Market Estimates and Forecast, USD Million,

2019-2032

10.2.2.1. Bluetooth

10.2.2.2. WiFi

10.2.2.3. RFID / NFC

10.2.2.4. Other

10.2.3. Market By End Use, Market Estimates and Forecast, USD Million, 2019-2032

10.2.3.1. Residential

10.2.3.2. Commercial

10.2.3.3. Other

10.2.4. Market By Distribution Channel, Market Estimates and Forecast, USD Million,

2019-2032

10.2.4.1. Offline

10.2.4.1.1. Specialty Fitness Equipment Stores

10.2.4.1.2. Sporting Goods Retailers

10.2.4.1.3. Electronics & Lifestyle Stores

10.2.4.1.4. Commercial Sales (B2B)

10.2.4.1.5. Dealer/Distributor Networks

10.2.4.2. Online

10.2.4.2.1. Brand-Owned E-commerce Platforms

10.2.4.2.2. E-commerce Marketplaces

10.2.4.2.3. Fitness Apps + Hardware Bundles

10.2.4.2.4. Flash Sale / Discount Portals

10.2.5. Market By Country, Market Estimates and Forecast, USD Million, 2025-2032

10.2.5.1. US

10.2.5.2. Canada

10.2.5.3. Mexico

10.3. Europe

10.3.1. Market By Product Type Estimates and Forecast, USD Million, 2019-2032

10.3.1.1. Cardiovascular training

10.3.1.1.1. Treadmills

10.3.1.1.2. Stationary Bikes

10.3.1.1.3. Ellipticals / Cross Trainers

10.3.1.1.4. Rowing Machines

10.3.1.1.5. Stair Climbers / Steppers

10.3.1.1.6. Spin & Air Bikes

10.3.1.1.7. Other

10.3.1.2. Strength training

10.3.1.2.1. Smart Resistance Machines

10.3.1.2.2. Free Weights & Dumbbells

10.3.1.2.3. Cables & Racks

10.3.1.2.4. Suspension & Bodyweight

10.3.1.2.5. AI-Based Smart Mirrors

10.3.1.2.6. Other

10.3.1.3. Other

10.3.2. Market By Connectivity Type, Market Estimates and Forecast, USD Million,

2019-2032

10.3.2.1. Bluetooth

10.3.2.2. WiFi

10.3.2.3. RFID / NFC

10.3.2.4. Other

10.3.3. Market By End Use, Market Estimates and Forecast, USD Million, 2019-2032

10.3.3.1. Residential

10.3.3.2. Commercial

10.3.3.3. Other

10.3.4. Market By Distribution Channel, Market Estimates and Forecast, USD Million,

2019-2032

10.3.4.1. Offline

10.3.4.1.1. Specialty Fitness Equipment Stores

10.3.4.1.2. Sporting Goods Retailers

10.3.4.1.3. Electronics & Lifestyle Stores

10.3.4.1.4. Commercial Sales (B2B)

10.3.4.1.5. Dealer/Distributor Networks

10.3.4.2. Online

10.3.4.2.1. Brand-Owned E-commerce Platforms

10.3.4.2.2. E-commerce Marketplaces

10.3.4.2.3. Fitness Apps + Hardware Bundles

10.3.4.2.4. Flash Sale / Discount Portals

10.3.5. Market By Country, Market Estimates and Forecast, USD Million,

10.3.5.1. Germany

10.3.5.2. France

10.3.5.3. U.K

10.3.5.4. Italy

10.3.5.5. Spain

10.3.5.6. Benelux

10.3.5.7. Russia

10.3.5.8. Finland

10.3.5.9. Sweden

10.3.5.10. Rest Of Europe

10.4. Asia-Pacific

10.4.1. Market By Product Type Estimates and Forecast, USD Million, 2019-2032

10.4.1.1. Cardiovascular training

10.4.1.1.1. Treadmills

10.4.1.1.2. Stationary Bikes

10.4.1.1.3. Ellipticals / Cross Trainers

10.4.1.1.4. Rowing Machines

10.4.1.1.5. Stair Climbers / Steppers

10.4.1.1.6. Spin & Air Bikes

10.4.1.1.7. Other

10.4.1.2. Strength training

10.4.1.2.1. Smart Resistance Machines

10.4.1.2.2. Free Weights & Dumbbells

10.4.1.2.3. Cables & Racks

10.4.1.2.4. Suspension & Bodyweight

10.4.1.2.5. AI-Based Smart Mirrors

10.4.1.2.6. Other

10.4.1.3. Other

10.4.2. Market By Connectivity Type, Market Estimates and Forecast, USD Million,

2019-2032

10.4.2.1. Bluetooth

10.4.2.2. WiFi

10.4.2.3. RFID / NFC

10.4.2.4. Other

10.4.3. Market By End Use, Market Estimates and Forecast, USD Million, 2019-2032

10.4.3.1. Residential

10.4.3.2. Commercial

10.4.3.3. Other

10.4.4. Market By Distribution Channel, Market Estimates and Forecast, USD Million,

2019-2032

10.4.4.1. Offline

10.4.4.1.1. Specialty Fitness Equipment Stores

10.4.4.1.2. Sporting Goods Retailers

10.4.4.1.3. Electronics & Lifestyle Stores

10.4.4.1.4. Commercial Sales (B2B)

10.4.4.1.5. Dealer/Distributor Networks

10.4.4.2. Online

10.4.4.2.1. Brand-Owned E-commerce Platforms

10.4.4.2.2. E-commerce Marketplaces

10.4.4.2.3. Fitness Apps + Hardware Bundles

10.4.4.2.4. Flash Sale / Discount Portals

10.4.5. Market By Country, Market Estimates and Forecast, USD Million,

10.4.5.1.1. China

10.4.5.1.2. India

10.4.5.1.3. Japan

10.4.5.1.4. South Korea

10.4.5.1.5. Indonesia

10.4.5.1.6. Thailand

10.4.5.1.7. Vietnam

10.4.5.1.8. Australia

10.4.5.1.9. New Zeland

10.4.5.1.10. Rest of APAC

10.5. Latin America

10.5.1. Market By Product Type Estimates and Forecast, USD Million, 2019-2032

10.5.1.1. Cardiovascular training

10.5.1.1.1. Treadmills

10.5.1.1.2. Stationary Bikes

10.5.1.1.3. Ellipticals / Cross Trainers

10.5.1.1.4. Rowing Machines

10.5.1.1.5. Stair Climbers / Steppers

10.5.1.1.6. Spin & Air Bikes

10.5.1.1.7. Other

10.5.1.2. Strength training

10.5.1.2.1. Smart Resistance Machines

10.5.1.2.2. Free Weights & Dumbbells

10.5.1.2.3. Cables & Racks

10.5.1.2.4. Suspension & Bodyweight

10.5.1.2.5. AI-Based Smart Mirrors

10.5.1.2.6. Other

10.5.1.3. Other

10.5.2. Market By Connectivity Type, Market Estimates and Forecast, USD Million,

2019-2032

10.5.2.1. Bluetooth

10.5.2.2. WiFi

10.5.2.3. RFID / NFC

10.5.2.4. Other

10.5.3. Market By End Use, Market Estimates and Forecast, USD Million, 2019-2032

10.5.3.1. Residential

10.5.3.2. Commercial

10.5.3.3. Other

10.5.4. Market By Distribution Channel, Market Estimates and Forecast, USD Million,

2019-2032

10.5.4.1. Offline

10.5.4.1.1. Specialty Fitness Equipment Stores

10.5.4.1.2. Sporting Goods Retailers

10.5.4.1.3. Electronics & Lifestyle Stores

10.5.4.1.4. Commercial Sales (B2B)

10.5.4.1.5. Dealer/Distributor Networks

10.5.4.2. Online

10.5.4.2.1. Brand-Owned E-commerce Platforms

10.5.4.2.2. E-commerce Marketplaces

10.5.4.2.3. Fitness Apps + Hardware Bundles

10.5.4.2.4. Flash Sale / Discount Portals

10.5.5. Market By Country, Market Estimates and Forecast, USD Million,

10.5.5.1. Brazil

10.5.5.2. Rest of LATAM

10.6. Middle East & Africa

10.6.1. Market By Product Type Estimates and Forecast, USD Million, 2019-2032

10.6.1.1. Cardiovascular training

10.6.1.1.1. Treadmills

10.6.1.1.2. Stationary Bikes

10.6.1.1.3. Ellipticals / Cross Trainers

10.6.1.1.4. Rowing Machines

10.6.1.1.5. Stair Climbers / Steppers

10.6.1.1.6. Spin & Air Bikes

10.6.1.1.7. Other

10.6.1.2. Strength training

10.6.1.2.1. Smart Resistance Machines

10.6.1.2.2. Free Weights & Dumbbells

10.6.1.2.3. Cables & Racks

10.6.1.2.4. Suspension & Bodyweight

10.6.1.2.5. AI-Based Smart Mirrors

10.6.1.2.6. Other

10.6.1.3. Other

10.6.2. Market By Connectivity Type, Market Estimates and Forecast, USD Million,

2019-2032

10.6.2.1. Bluetooth

10.6.2.2. WiFi

10.6.2.3. RFID / NFC

10.6.2.4. Other

10.6.3. Market By End Use, Market Estimates and Forecast, USD Million, 2019-2032

10.6.3.1. Residential

10.6.3.2. Commercial

10.6.3.3. Other

10.6.4. Market By Distribution Channel, Market Estimates and Forecast, USD Million,

2019-2032

10.6.4.1. Offline

10.6.4.1.1. Specialty Fitness Equipment Stores

10.6.4.1.2. Sporting Goods Retailers

10.6.4.1.3. Electronics & Lifestyle Stores

10.6.4.1.4. Commercial Sales (B2B)

10.6.4.1.5. Dealer/Distributor Networks

10.6.4.2. Online

10.6.4.2.1. Brand-Owned E-commerce Platforms

10.6.4.2.2. E-commerce Marketplaces

10.6.4.2.3. Fitness Apps + Hardware Bundles

10.6.4.2.4. Flash Sale / Discount Portals

10.6.5. Market By Country, Market Estimates and Forecast, USD Million,

10.6.5.1. Saudi Arabia

10.6.5.2. Rest of MEA

Chapter 11. Competitive Landscape

11.1. Market Revenue Share By Manufacturers

11.2. Mergers & Acquisitions

11.3. Competitor’s Positioning

11.4. Strategy Benchmarking

11.5. Vendor Landscape

11.5.1. Distributors

11.5.1.1. North America

11.5.1.2. Europe

11.5.1.3. Asia Pacific

11.5.1.4. Middle East & Africa

11.5.1.5. Latin America

Chapter 12. Company Profiles

12.1. Peloton Interactive

12.1.1. Company Overview

12.1.2. Product & Service Offerings

12.1.3. Strategic Initiatives

12.1.4. Financials

12.2. Tonal Systems

12.2.1. Company Overview

12.2.2. Product & Service Offerings

12.2.3. Strategic Initiatives

12.2.4. Financials

12.3. FIT / NordicTrack (ICON Health & Fitness)

12.3.1. Company Overview

12.3.2. Product & Service Offerings

12.3.3. Strategic Initiatives

12.3.4. Financials

12.4. Technogym

12.4.1. Company Overview

12.4.2. Product & Service Offerings

12.4.3. Strategic Initiatives

12.4.4. Financials

12.5. Echelon Fitness

12.5.1. Company Overview

12.5.2. Product & Service Offerings

12.5.3. Strategic Initiatives

12.5.4. Financials

12.6. Hydrow

12.6.1. Company Overview

12.6.2. Product & Service Offerings

12.6.3. Strategic Initiatives

12.6.4. Financials

12.7. Temp

12.7.1. Company Overview

12.7.2. Product & Service Offerings

12.7.3. Strategic Initiatives

12.7.4. Financials

12.7.5. Conclusion

12.8. AXJOX

12.8.1. Company Overview

12.8.2. Product & Service Offerings

12.8.3. Strategic Initiatives

12.8.4. Financials

12.8.5. Conclusion

12.9. Aviron

12.9.1. Company Overview

12.9.2. Product & Service Offerings

12.9.3. Strategic Initiatives

12.9.4. Financials

12.9.5. Conclusion

12.10. Concept2

12.10.1. Company Overview

12.10.2. Product & Service Offerings

12.10.3. Strategic Initiatives

12.10.4. Financials

12.10.5. Conclusion

12.11. Bowflex

12.11.1. Company Overview

12.11.2. Product & Service Offerings

12.11.3. Strategic Initiatives

12.11.4. Financials

12.11.5. Conclusion

12.12. Life Fitness.

12.12.1. Company Overview

12.12.2. Product & Service Offerings

12.12.3. Strategic Initiatives

12.12.4. Financials

12.12.5. Conclusion

12.13. Precor

12.13.1. Company Overview

12.13.2. Product & Service Offerings

12.13.3. Strategic Initiatives

12.13.4. Financials

12.13.5. Conclusion

12.14. Johnson Health Tech

12.14.1. Company Overview

12.14.2. Product & Service Offerings

12.14.3. Strategic Initiatives

12.14.4. Financials

12.14.5. Conclusion

12.15. EGYM

12.15.1. Company Overview

12.15.2. Product & Service Offerings

12.15.3. Strategic Initiatives

12.15.4. Financials

12.15.5. Conclusion

12.16. OxeFit

12.16.1. Company Overview

12.16.2. Product & Service Offerings

12.16.3. Strategic Initiatives

12.16.4. Financials

12.16.5. Conclusion

12.17. Ergatta

12.17.1. Company Overview

12.17.2. Product & Service Offerings

12.17.3. Strategic Initiatives

12.17.4. Financials

12.17.5. Conclusion

12.18. FightCamp

12.18.1. Company Overview

12.18.2. Product & Service Offerings

12.18.3. Strategic Initiatives

12.18.4. Financials

12.18.5. Conclusion

12.19. TRUE Fitness

12.19.1. Company Overview

12.19.2. Product & Service Offerings

12.19.3. Strategic Initiatives

12.19.4. Financials

12.19.5. Conclusion

12.20. Matrix Fitness

12.20.1. Company Overview

12.20.2. Product & Service Offerings

12.20.3. Strategic Initiatives

12.20.4. Financials

12.20.5. Conclusion

12.21. Keiser

12.21.1. Company Overview

12.21.2. Product & Service Offerings

12.21.3. Strategic Initiatives

12.21.4. Financials

12.21.5. Conclusion

12.22. Cybex

12.22.1. Company Overview

12.22.2. Product & Service Offerings

12.22.3. Strategic Initiatives

12.22.4. Financials

12.22.5. Conclusion

12.23. Rogue Fitness

12.23.1. Company Overview

12.23.2. Product & Service Offerings

12.23.3. Strategic Initiatives

12.23.4. Financials

12.23.5. Conclusion

12.24. Core Health & Fitness

12.24.1. Company Overview

12.24.2. Product & Service Offerings

12.24.3. Strategic Initiatives

12.24.4. Financials

12.24.5. Conclusion

12.25. ICON Health & Fitness

12.25.1. Company Overview

12.25.2. Product & Service Offerings

12.25.3. Strategic Initiatives

12.25.4. Financials

12.25.5. Conclusion

Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP. has segmented global Connected Fitness Equipment market on the basis of By Product Type, By Connectivity Type, By Distribution Channel By End Use and By region for 2019 to 2032

Global By Product Type Outlook (Revenue, USD Million 2019-2032)

-

- Natural & Organic Ingredients

-

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

-

- Strength Training

-

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

- Other

-

-

- Other

- Natural & Organic Ingredients

Global By Connectivity Type (Revenue, USD Million; 2019-2032)

-

- Bluetooth

- WiFi

- RFID / NFC

- Other

Global By End Use Outlook (Revenue, USD Million; 2019-2032)

-

- Residential

- Commercial

- Other

Global By Distribution Channel (Revenue, USD Million; 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- North America

- North America Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- North America Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- North America End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- North America Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- North America Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- U.S

- U.S Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- U.S Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- U.S End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- U.S Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- U.S Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Canada

- Canada Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Canada Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Canada End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Canada Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Canada Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Mexico

- Mexico Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Mexico Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Mexico End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Mexico Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Mexico Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Europe

- Europe Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Europe Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Europe End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Europe Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Europe Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Germany

- Germany Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Germany Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Germany End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Germany Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Germany Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- France

- France Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- France Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- France End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- France Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- France Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- U.K

- U.K Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- U.K Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- U.K End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- U.K Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- U.K Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Italy

- Italy Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Italy Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Italy End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Italy Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Italy Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Spain

- Spain Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Spain Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Spain End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Spain Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Spain Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Benelux

- Benelux Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Benelux Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Benelux End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Benelux Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Benelux Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Russia

- Russia Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Russia Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Russia End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Russia Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Russia Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Finland

- Finland Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Finland Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Finland End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Finland Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Finland Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Sweden

- Sweden Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Sweden Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Sweden End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Sweden Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Sweden Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Rest Of Europe

- Rest Of Europe Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Rest Of Europe Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Rest Of Europe End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Rest Of Europe Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Rest Of Europe Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Asia-Pacific

- Asia-Pacific Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Asia-Pacific Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Asia-Pacific End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Asia-Pacific Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Asia-Pacific Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- China

- China Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- China Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- China End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- China Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- China Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- India

- India Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- India Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- India End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- India Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- India Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Japan

- Japan Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Japan Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Japan End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Japan Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Japan Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Indonesia

- Indonesia Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Indonesia Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Indonesia End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Indonesia Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Indonesia Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Thailand

- Thailand Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Thailand Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Thailand End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Thailand Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Thailand Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Vietnam

- Vietnam Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Vietnam Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Vietnam End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Vietnam Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Vietnam Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Australia

- Australia Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Australia Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Australia End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Australia Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Australia Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- New Zealand

- New Zealand Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- New Zealand Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- New Zealand End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- New Zealand Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- New Zealand Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Rest of Asia-Pacific

- Rest of Asia-Pacific Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Rest of Asia-Pacific Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Rest of Asia-Pacific End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Rest of Asia-Pacific Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Rest of Asia-Pacific Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Latin-America

- Latin-America Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Latin-America Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Latin-America End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Latin-America Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Latin-America Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Brazil

- Brazil Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors

-

- Other

- Cardiovascular training

- Brazil Connectivity Type Outlook (Revenue, USD Million; 2019-2032)

- Bluetooth

- WiFi

- RFID / NFC

- Other

- Brazil End Use Outlook (Revenue, USD Million; 2019-2032)

- Residential

- Commercial

- Other

- Brazil Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Brazil Product Type Outlook (Revenue, USD Million 2019-2032)

Online

-

-

-

-

- Specialty Fitness Equipment Stores

- Sporting Goods Retailers

- Electronics & Lifestyle Stores

- Commercial Sales (B2B)

- Dealer/Distributor Networks

-

-

-

Offline

-

-

-

-

- Brand-Owned E-commerce Platforms

- E-commerce Marketplaces

- Fitness Apps + Hardware Bundles

- Flash Sale / Discount Portals

-

-

-

- Rest of Latam

- Rest of Latam Product Type Outlook (Revenue, USD Million 2019-2032)

- Cardiovascular training

-

- Treadmills

- Stationary Bikes

- Ellipticals / Cross Trainers

- Rowing Machines

- Stair Climbers / Steppers

- Spin & Air Bikes

- Other

-

- Strength training

-

- Smart Resistance Machines

- Free Weights & Dumbbells

- Cables & Racks

- Suspension & Bodyweight

- AI-Based Smart Mirrors