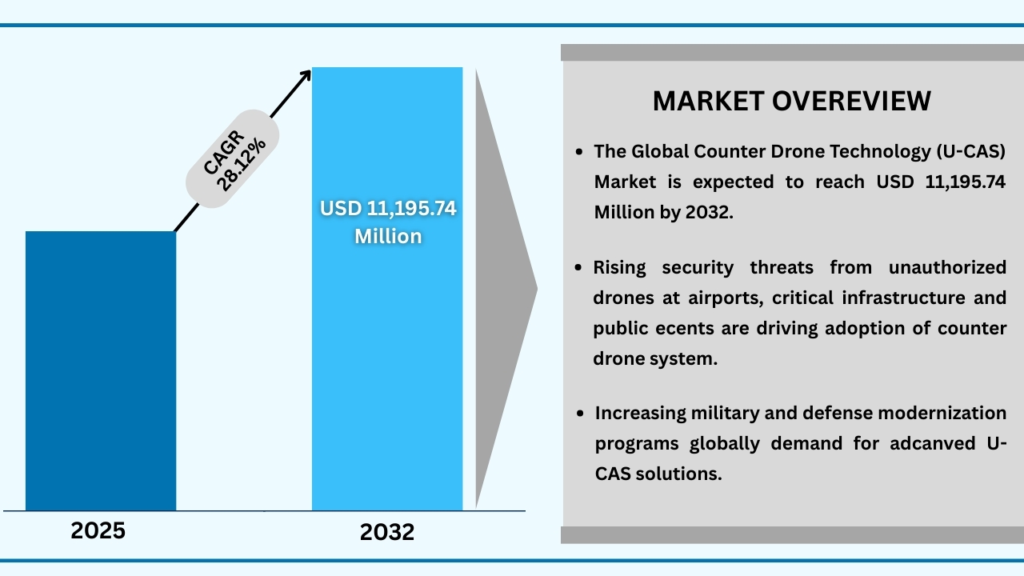

Market Synopsis

The Global Counter Drone Technology (U-CAS) market was valued at USD 1,555.20 million in 2024 and is projected to reach USD 11,195.74 million by 2032, growing at a strong CAGR of 28.12%. The rapid growth of the Global Counter Drone Technology (U-CAS) market is primarily driven by the escalating security threats posed by unauthorized and hostile drones across defense, commercial, and critical infrastructure sectors. Airports, government facilities, military bases, and high-profile public events face increasing risks from espionage, smuggling, and drone-enabled attacks. Rising incidents of drone misuse have accelerated the adoption of detection, tracking, and neutralization systems, creating strong demand for advanced U-CAS solutions. Additionally, the integration of artificial intelligence, machine learning, and multi-sensor technologies has enhanced system precision and operational efficiency, further fueling market growth.

Another significant factor driving the market is the surge in defense modernization programs and proactive regulatory support in regions such as North America, Europe, and Asia-Pacific. Governments and private organizations are investing heavily in research, development, and deployment of sophisticated counter-drone solutions, including radar, RF sensors, directed-energy systems, and integrated command platforms. This investment, combined with increasing awareness of drone-related security vulnerabilities and the need for rapid-response systems, is encouraging both established players and emerging startups to innovate, expand product portfolios, and capture new market opportunities, supporting the market’s strong projected CAGR of 28.12%.

The growing commercialization of drones across logistics, agriculture, energy, and urban surveillance is also contributing to the expansion of the U-CAS market. As drones become more accessible and widely used, the potential for accidental or intentional airspace violations increases, prompting industries and governments to adopt counter-drone measures proactively. Furthermore, advancements in miniaturized sensors, autonomous detection systems, and cost-effective neutralization technologies are enabling broader deployment across both urban and remote areas. This convergence of rising drone adoption and technological innovation is creating a robust ecosystem for U-CAS solutions, further reinforcing long-term market growth.

Global Counter Drone Technology (U-CAS) Market (USD Million), 2025-2032

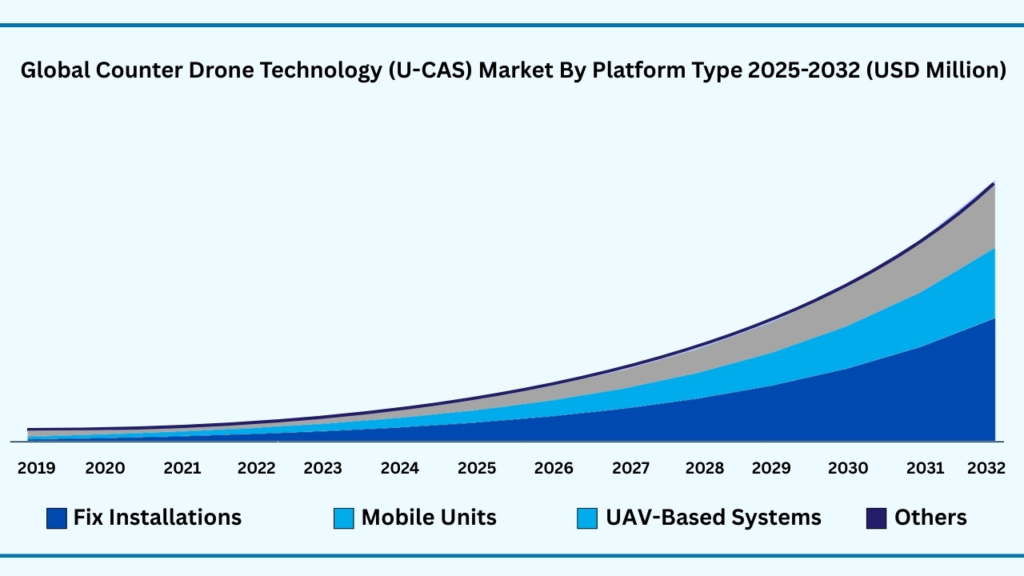

Global Counter Drone Technology (U-CAS) Market By Platform Type Insights:

Fix installations segment accounted for market share of share 47.88% in 2024 in the Global Counter Drone Technology (U-CAS) market.

The fix installations segment accounted for the largest share of the Global Counter Drone Technology (U-CAS) market in 2024, representing 47.88% of total revenues. fix installations segment is expected to register a CAGR of 28.12 % during the forecast year from 2025 to 2032 and expected to reach USD 11,195.74 million in 2032. The Fixed Installations segment dominates the U-CAS market due to its ability to provide continuous, high-precision protection for critical infrastructure and high-security zones. Airports, military bases, government buildings, and energy facilities require permanent, reliable systems that can detect, track, and neutralize unauthorized drones in real time. The segment’s high adoption is driven by the need for round-the-clock monitoring and integrated response capabilities, which standalone mobile or ad-hoc systems often cannot provide. Fixed installations also allow the deployment of multi-sensor setups, combining radar, RF sensors, EO/IR cameras, and acoustic systems to enhance detection accuracy and reduce false alarms.

The growth of this segment is further supported by government and defense investments in infrastructure security and the increasing number of drone-related security incidents worldwide. Fixed installations offer a scalable and long-term solution, reducing operational risks and ensuring compliance with regulatory requirements for airspace safety. Additionally, technological advancements, such as AI-driven analytics, automated threat assessment, and integrated neutralization capabilities, are enhancing system efficiency and reliability. These factors make fixed installations the preferred choice for high-value and high-risk sites, contributing to their significant share and strong projected CAGR of 28.12% from 2025 to 2032.

Global Counter Drone Technology (U-CAS) Market by Platform (USD Million)

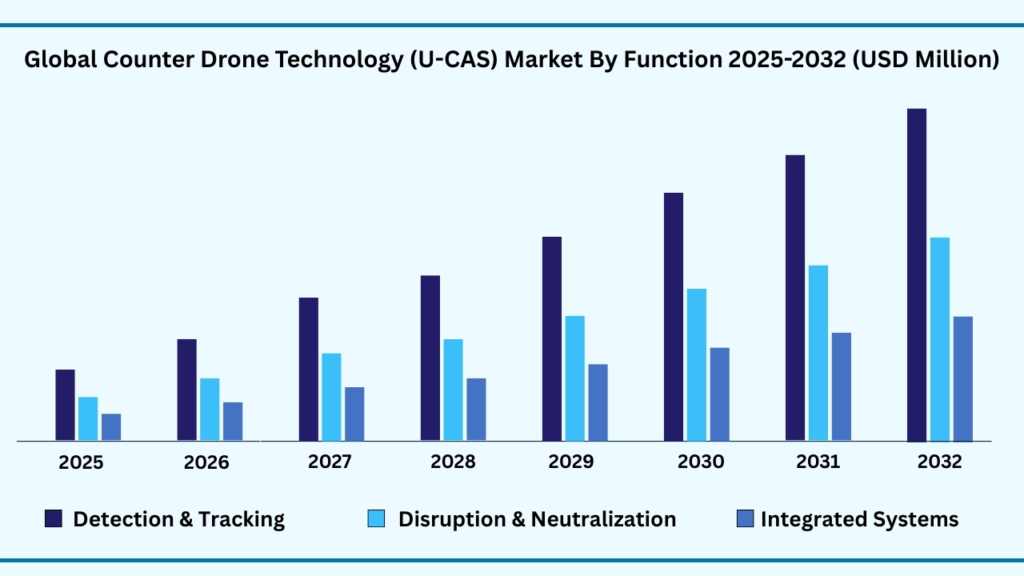

Global Counter Drone Technology (U-CAS) Maret by Function Insights:

Detection & Tracking segment accounted for the largest market share of share 55.45% in 2024 in the Global Counter Drone Technology (U-CAS) market.

Based on the function, Detection & Tracking segment held the largest revenue share of 55.45% in 2024, and expected to register a CAGR of 28.25% between 2025 to 2032 and the market is expected to reach USD 6,252.82 million by 2032. The Detection & Tracking segment leads the U-CAS market due to its critical role in identifying, monitoring, and assessing unauthorized drone activity across military, commercial, and civil applications. Airports, government facilities, border areas, and critical infrastructure rely heavily on advanced detection systems—such as radar, RF sensors, EO/IR cameras, and acoustic sensors—to provide real-time situational awareness. By delivering early warning and precise tracking data, these systems enable timely and effective neutralization of potential threats, making them indispensable in comprehensive counter-drone strategies.

Growth in this segment is driven by rising drone-related security incidents and increasing adoption of advanced detection technologies. Innovations in AI-driven analytics, multi-sensor integration, and automated alert systems have improved accuracy and reduced false alarms, encouraging wider deployment in high-risk zones. Additionally, regulatory requirements for airspace safety and proactive surveillance needs across defense and commercial sectors continue to support strong adoption of detection and tracking solutions.

Global Counter Drone Technology (U-CAS) Market by Function (USD Million)

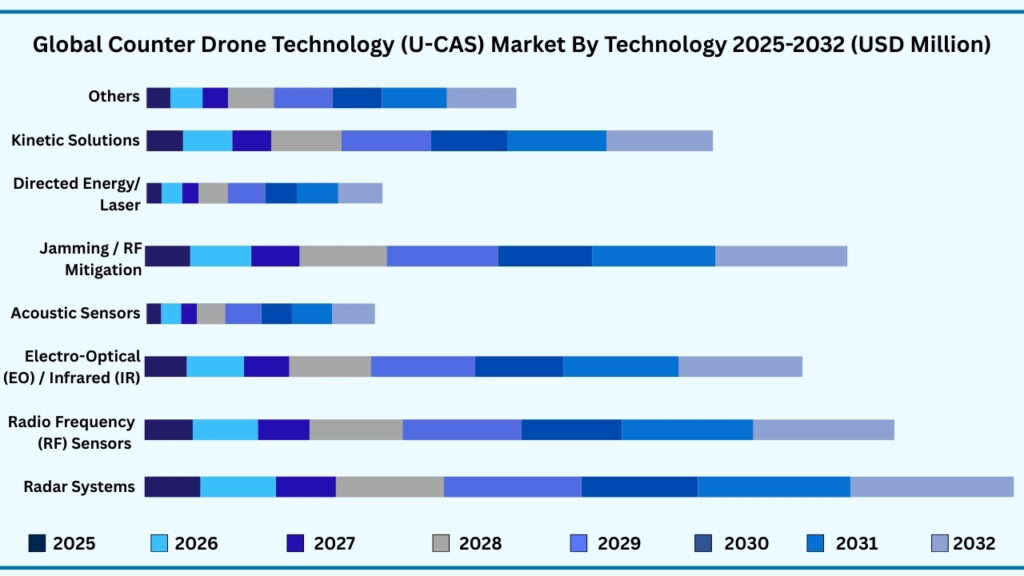

Global Counter Drone Technology (U-CAS) Maret by Technology Insights:

Radar systems segment accounted for the largest market share of share 25.32% in 2024 in the Global Counter Drone Technology (U-CAS) market.

Based on effect, heat-activated segment held the largest revenue share of 25.32% in the Global Counter Drone Technology (U-CAS) market in 2024 and expected to register a CAGR of 28.59% from 2025 to 2032 and expected to reach USD 2,908.65 million. The Heat-Activated segment dominates the U-CAS market due to its ability to respond reliably to thermal triggers, enabling precise and automated counter-drone operations. These systems are widely used in critical infrastructure, defense, and high-security environments where rapid response to unauthorized drone activity is essential. By activating only under specific conditions, heat-sensitive mechanisms enhance operational efficiency, reduce false activations, and provide targeted neutralization capabilities, making them a preferred choice for permanent installations and integrated security setups.

The growth of the Heat-Activated segment is driven by advancements in thermal detection technologies and integration with multi-sensor platforms. Combining heat activation with radar, RF sensors, and AI-based analytics improves detection accuracy and system responsiveness, particularly in challenging environmental conditions. Additionally, increasing emphasis on automation, reliability, and precision in counter-drone solutions encourages adoption of heat-activated technologies across both defense and commercial sectors, reinforcing their importance in the evolving U-CAS market.

Global Counter Drone Technology (U-CAS) Market by Technology (USD Million)

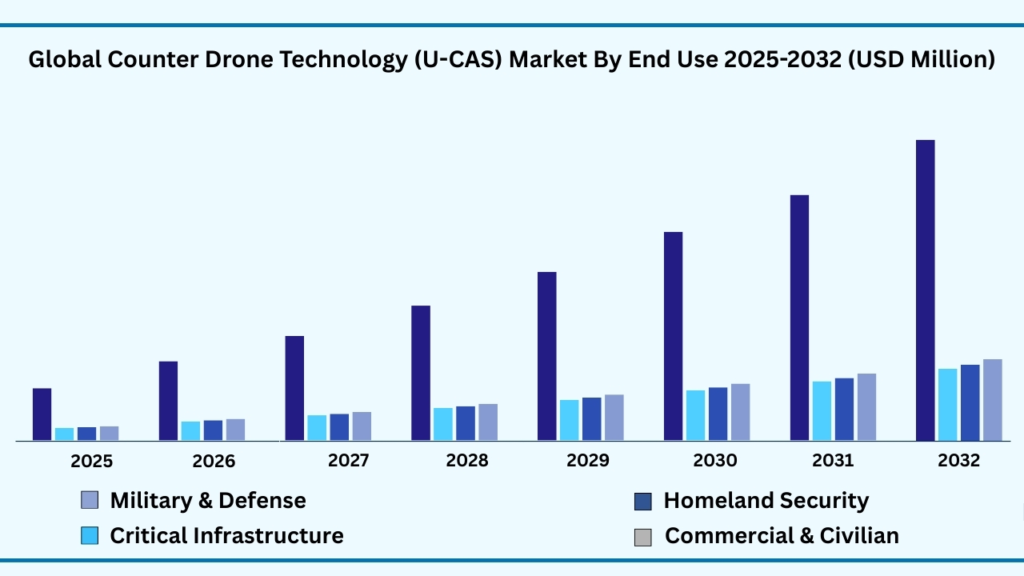

Global Counter Drone Technology (U-CAS) Market by End Use Insights:

Military & Defense segment accounted for the largest market share of share of 45.21% in 2024 in the Global Counter Drone Technology (U-CAS) market.

Based on by form, wire segment held the largest revenue share of 45.21% in the Global Counter Drone Technology (U-CAS) market in 2024 and expected to register a CAGR of 28.10% from 2024 to 2032 and expected to reach USD 5,099.66 million in 2032. The Wire segment leads the U-CAS market due to its versatility and reliability in delivering high-performance counter-drone solutions. Wire-based components are widely used in detection, tracking, and neutralization systems, providing precise connectivity, robust signal transmission, and durability under demanding operational conditions. Their adaptability allows integration into fixed installations, mobile units, and UAV-based systems, making them essential for applications across defense, homeland security, critical infrastructure, and commercial sectors.

The growth of the Wire segment is driven by increasing demand for durable and scalable counter-drone infrastructure. Technological advancements in wire materials, insulation, and conductivity have enhanced system efficiency, reduced maintenance requirements, and improved overall performance. Additionally, as organizations prioritize reliable, long-term solutions for drone detection and mitigation, wire-based systems continue to be preferred for their consistent performance, operational safety, and compatibility with advanced multi-sensor platforms, reinforcing their dominant position in the U-CAS market.

Global Counter Drone Technology (U-CAS) by End Use (USD Million)

Global Counter Drone Technology (U-CAS) Market by Region Insights:

North America segment accounted for the largest market share of share of 43.46% in 2024 in the Global Counter Drone Technology (U-CAS) market.

Based on region, the Global Counter Drone Technology (U-CAS) market is segmented into Europe, Asia-Pacific, North America, Latin America and Middle East & Africa. Among these, North America region held the largest revenue share of 28.21% in the Global Counter Drone Technology (U-CAS) market in 2024 and expected to register a CAGR of 9.13% from 2024 to 2032 and expected to reach USD 11,740.88 million in 2032. North America dominates the U-CAS market due to strong defense and security initiatives, advanced technological infrastructure, and high adoption of innovative counter-drone solutions. The U.S., Canada, and Mexico are leading the deployment of radar systems, RF sensors, jamming technologies, and integrated platforms across military bases, airports, government facilities, and critical infrastructure. The presence of major defense contractors and technology providers, coupled with substantial R&D investments, has created a robust ecosystem for the development and implementation of advanced counter-drone technologies.

The growth in North America is further supported by rising security concerns, proactive government regulations, and increasing incidents of drone-related threats. Organizations across defense, homeland security, and commercial sectors are prioritizing the adoption of automated detection, tracking, and neutralization systems to ensure airspace safety. Additionally, technological advancements in AI, multi-sensor integration, and automated threat response have accelerated the deployment of sophisticated U-CAS solutions, reinforcing North America’s position as a leading and high-growth market in the global counter-drone landscape.

Global Counter Drone Technology (U-CAS) Market By Region (USD Million)

Major Companies and Competitive Landscape

The global Counter Drone Technology (U-CAS) market is highly fragmented, comprising a mix of multinational defense contractors, specialized solution providers, and innovative startups. Leading companies are actively pursuing strategies such as mergers and acquisitions, joint ventures, and strategic collaborations with technology partners, system integrators, and end-use industries to strengthen their market presence. Significant investments are being made in expanding production capacities, enhancing system performance, and developing advanced detection, tracking, and neutralization technologies to meet growing demand across defense, homeland security, critical infrastructure, and commercial sectors. These initiatives focus on improving operational efficiency, ensuring reliability, and scaling deployment while maintaining strict quality and regulatory compliance.

In addition, market leaders are increasingly emphasizing sustainability and operational efficiency. Companies are optimizing power usage, improving system lifecycle management, and ensuring compliance with global regulatory standards governing airspace safety and RF emissions. Research and development efforts are concentrated on producing high-accuracy detection systems, AI-driven analytics, integrated neutralization platforms, and modular solutions that reduce operational costs while improving responsiveness. By combining technological innovation, sustainability, and strategic market expansion, key players are strengthening their competitive positioning and driving broader adoption of Counter Drone Technology across diverse sectors worldwide.

Some of the leading companies profiled in the Global Counter Drone Technology (U-CAS) market report include:

- Lockheed Martin

- Raytheon Technologies (RTX)

- Thales Group

- Israel Aerospace Industries (IAI)

- Saab AB

- General Dynamics

- Northrop Grumman

- BAE Systems

- Elbit Systems

- DroneShield Ltd

- Dedrone

- QinetiQ Group plc

- Rafael Advanced Defense Systems

- Leonardo S.p.A.

- SAES Getters S.p.A

Strategic Development

Expansion in China:

In early 2025, Dedrone inaugurated a new office in Beijing, China, reinforcing its commitment to the rapidly growing Asia-Pacific market. This strategic expansion aims to strengthen local partnerships, enhance customer support, and address the increasing demand for advanced counter-drone solutions across commercial, defense, and critical infrastructure sectors.

Strategic Divestment:

In mid-2025, Drone Shield Ltd. divested a portion of its non-core security solutions business to focus on its U-CAS portfolio, including AI-driven detection, RF-based neutralization, and integrated systems. This decision aligns with the company’s strategy to streamline operations, concentrate on high-growth counter-drone technologies, and expand its market presence across North America, Europe, and Asia-Pacific.

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 1,555.20 Million |

| CAGR (2024–2032) | 28.12% |

| Revenue forecast to 2033 | USD 32,228.60 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million, Volume Kiloton and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Platform Type, By Function, By Technology, By End Use and By region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, Rest of MEA |

| Key companies profiled | Lockheed Martin, Raytheon Technologies (RTX), Thales Group, Israel Aerospace Industries (IAI), Saab AB, General Dynamics, Northrop Grumman, BAE Systems, Elbit Systems, Drone Shield Ltd, Dedrone, QinetiQ Group plc, Rafael Advanced Defense Systems, Leonardo S.p.A. |

| Customization scope | 10 hours of free customization and expert consultation |

Some Key Questions the Report Will Answer

- What is the expected revenue Compound Annual Growth Rate (CAGR) of the Global Counter Drone Technology (U-CAS) market over the forecast period (2025–2032)?

- The Global Counter Drone Technology (U-CAS) market revenue is expected to register a Compound Annual Growth Rate (CAGR) of 28.12% during the forecast period.

- What was the size of the Global Counter Drone Technology (U-CAS) in 2024?

- The global Counter Drone Technology (U-CAS) market size was USD 1,555.20 Million in 2024.

- Which factors are expected to drive the Global Counter Drone Technology (U-CAS) market growth?

- The growth of the Global Counter Drone Technology (U-CAS) market is expected to be driven by rising security threats from unauthorized and hostile drones, increasing adoption of advanced detection and neutralization technologies, and significant investments in defense modernization and homeland security programs. Airports, military bases, critical infrastructure, and public venues are increasingly deploying multi-sensor systems, AI-driven analytics, and integrated response platforms to safeguard airspace and prevent espionage, smuggling, or attacks. Additionally, rapid technological advancements, such as radar, RF sensors, directed-energy solutions, and autonomous neutralization systems, are enhancing operational efficiency and reliability, further fueling market adoption across both defense and commercial sectors worldwide.

- Which was the leading segment in the Global Counter Drone Technology (U-CAS) market in platform type in 2024?

- In 2024, Fix installations segment accounted for the largest market share with a market share of 43.46% in terms of USD million.

- What are some restraints for revenue growth of the Global Counter Drone Technology (U-CAS) market?

- Revenue growth in the Global Counter Drone Technology (U-CAS) market is restrained by high implementation and operational costs, complex regulatory frameworks, and legal restrictions on certain counter-drone measures. Advanced systems such as radar, RF jamming, and directed-energy solutions require significant capital investment, ongoing maintenance, and skilled personnel, which can limit adoption, particularly among smaller organizations or cost-sensitive regions. Additionally, stringent aviation, communication, and safety regulations in many countries restrict the deployment of certain technologies, slowing large-scale market penetration and creating challenges for companies seeking to expand their global footprint.

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of Counter Drone Technology (U-CAS) Market

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1.Primary

2.1.2.Secondary

2.1.3.Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1.Market value

2.3.2.Market volume

2.3.3.Exchange rate

2.3.4.Price

2.3.5.Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2019–2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10. Formulation & manufacturing

4.11. Distribution & retail

4.12. Import-export analysis

4.13. Brand comparative analysis

4.14. Technological advancements

4.15. Porter’s five force

4.16. Threat of new entrants

4.16.1.1. Capital requirment

4.16.1.2. Product knowledge

4.16.1.3. Technical knowledge

4.16.1.4. Customer relation

4.16.1.5. Access to appliation and technology

4.16.2. Threat of substitutes

4.16.2.1. Cost

4.16.2.2. Performance

4.16.2.3. Availability

4.16.2.4. Technical knowledge

4.16.2.5. Durability

4.16.3. Bargainning power of buyers

4.16.3.1. Numbers of buyers relative to suppliers

4.16.3.2. Product differentiation

4.16.3.3. Threat of forward integration

4.16.3.4. Buyers volume

4.16.4. Bargainning power of suppliers

4.16.4.1. Suppliers concentration

4.16.4.2. Buyers switching cost to other suppliers

4.16.4.3. Threat of backward integration

4.16.5. Bargainning power of suppliers

4.16.5.1. Industry concentration

4.16.5.2. Industry growth rate

4.16.5.3. Product differentiation

4.17. Patent analysis

4.18. Regulation coverage

4.19. Pricing analysis

4.20. Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1. Rising Security Threats from Unauthorized Drones

5.1.2. Growing Adoption in Military & Defense

5.1.3. Expansion of Civil & Commercial Applications

5.2. Restraints

5.2.1. High Development & Deployment Costs

5.2.2. Regulatory & Legal Complexities

5.3. Opportunities

5.3.1. Integration of AI & Machine Learning

5.3.2. Emerging Demand in Smart Cities & Critical Infrastructure

5.3.3. Commercial Partnerships & Dual-Use Tech

5.4. Challenges

5.4.1. Adapting to Rapidly Evolving Drone Technology

5.4.2. Risk of Collateral Damage

Chapter 6. Global Counter Drone Technology (U-CAS) Market By Platform Type Insights & Trends, Revenue (USD Million)

6.1. Platform Type Dynamics & Market Share, 2019–2032

6.1.1. Fix installations

6.1.2. Mobile Units

6.1.3. UAV-Based Systems

6.1.4. Others

Chapter 7. Global Counter Drone Technology (U-CAS) Market By Function Insights & Trends, Revenue (USD Million)

7.1. Technology Dynamics & Market Share, 2019–2032

7.1.1. Detection & Tracking

7.1.2. Disruption & Neutralization

7.1.3. Integrated Systems

Chapter 8. Global Counter Drone Technology (U-CAS) Market By Technology Insights & Trends, Revenue (USD Million)

8.1. Technology Dynamics & Market Share, 2019–2032

8.1.1. Radar systems

8.1.2. Radio Frequency (RF) sensors

8.1.3. Electro-optical (EO) / Infrared (IR)

8.1.4. Acoustic sensors

8.1.5. Jamming / RF mitigation

8.1.6. Directed Energy / Laser

8.1.7. Kinetic solutions

8.1.8. Other

Chapter 9. Global Counter Drone Technology (U-CAS) Market By End Use Insights & Trends, Revenue (USD Million)

9.1. End Use Use Dynamics & Market Share, 2019–2032

9.1.1. Military & Defense

9.1.2. Homeland Security

9.1.3. Critical Infrastructure

9.1.4. Commercial & Civilian

Chapter 10. Global Counter Drone Technology (U-CAS) Market Regional Outlook

10.1.Counter Drone Technology (U-CAS) Share By Region, 2019–2032

10.2.North America

10.2.1. Market By Platform Type Estimates and Forecast, USD Million, 2019-2032

10.2.1.1. Fix installations

10.2.1.2. Mobile Units

10.2.1.3. UAV-Based Systems

10.2.1.4. Others

10.2.2. Market By Function, Market Estimates and Forecast, USD Million, 2019 2032

10.2.2.1. Detection & Tracking

10.2.2.2. Disruption & Neutralization

10.2.2.3. Integrated Systems

10.2.3. Market By Technology, Market Estimates and Forecast, USD Million, 2019-2032

10.2.3.1. Radar systems

10.2.3.2. Radio Frequency (RF) sensors

10.2.3.3. Electro-optical (EO) / Infrared (IR)

10.2.3.4. Acoustic sensors

10.2.3.5. Jamming / RF mitigation

10.2.3.6. Directed Energy / Laser

10.2.3.7. Kinetic solutions

10.2.3.8. Other

10.2.4. Market By End Use Estimates and Forecast, USD Million, 2019-2032

10.2.4.1. Military & Defense

10.2.4.2. Homeland Security

10.2.4.3. Critical Infrastructure

10.2.4.4. Commercial & Civilian

10.2.5. Market By Country, Market Estimates and Forecast, USD Million, 2025-2032

10.2.5.1. US

10.2.5.2. Canada

10.2.5.3. Mexico

10.3. Europe

10.3.1. Market By Platform Type Estimates and Forecast, USD Million, 2019-2032

10.3.1.1. Fix installations

10.3.1.2. Mobile Units

10.3.1.3. UAV-Based Systems

10.3.1.4. Others

10.3.2. Market By Function, Market Estimates and Forecast, USD Million, 2019-2032

10.3.2.1. Detection & Tracking

10.3.2.2. Disruption & Neutralization

10.3.2.3. Integrated Systems

10.3.3. Market By Technology, Market Estimates and Forecast, USD Million, 2019-2032

10.3.3.1. Radar systems

10.3.3.2. Radio Frequency (RF) sensors

10.3.3.3. Electro-optical (EO) / Infrared (IR)

10.3.3.4. Acoustic sensors

10.3.3.5. Jamming / RF mitigation

10.3.3.6. Directed Energy / Laser

10.3.3.7. Kinetic solutions

10.3.3.8. Other

10.3.4. Market By End Use Estimates and Forecast, USD Million, 2019-2032

10.3.4.1. Military & Defense

10.3.4.2. Homeland Security

10.3.4.3. Critical Infrastructure

10.3.4.4. Commercial & Civilian

10.3.5. Market By Country, Market Estimates and Forecast, USD Million,

10.3.5.1. Germany

10.3.5.2. France

10.3.5.3. U.K

10.3.5.4. Italy

10.3.5.5. Spain

10.3.5.6. Benelux

10.3.5.7. Russia

10.3.5.8. Finland

10.3.5.9. Sweden

10.3.5.10. Rest Of Europe

10.4. Asia-Pacific

10.4.1. Market By Platform Type Estimates and Forecast, USD Million, 2019-2032

10.4.1.1. Fix installations

10.4.1.2. Mobile Units

10.4.1.3. UAV-Based Systems

10.4.1.4. Others

10.4.2. Market By Function, Market Estimates and Forecast, USD Million, 2019-2032

10.4.2.1. Detection & Tracking

10.4.2.2. Disruption & Neutralization

10.4.2.3. Integrated Systems

10.4.3. Market By Technology, Market Estimates and Forecast, USD Million, 2019-2032

10.4.3.1. Radar systems

10.4.3.2. Radio Frequency (RF) sensors

10.4.3.3. Electro-optical (EO) / Infrared (IR)

10.4.3.4. Acoustic sensors

10.4.3.5. Jamming / RF mitigation

10.4.3.6. Directed Energy / Laser

10.4.3.7. Kinetic solutions

10.4.3.8. Other

10.4.4. Market By End Use Estimates and Forecast, USD Million, 2019-2032

10.4.4.1. Military & Defense

10.4.4.2. Homeland Security

10.4.4.3. Critical Infrastructure

10.4.4.4. Commercial & Civilian

10.4.5. Market By Country, Market Estimates and Forecast, USD Million,

10.4.5.1.1. China

10.4.5.1.2. India

10.4.5.1.3. Japan

10.4.5.1.4. South Korea

10.4.5.1.5. Indonesia

10.4.5.1.6. Thailand

10.4.5.1.7. Vietnam

10.4.5.1.8. Australia

10.4.5.1.9. New Zeland

10.4.5.1.10. Rest of APAC

10.5. Latin America

10.5.1. Market By Platform Type Estimates and Forecast, USD Million, 2019-2032

10.5.1.1. Fix installations

10.5.1.2. Mobile Units

10.5.1.3. UAV-Based Systems

10.5.1.4. Others

10.5.2. Market By Function, Market Estimates and Forecast, USD Million, 2019-2032

10.5.2.1. Detection & Tracking

10.5.2.2. Disruption & Neutralization

10.5.2.3. Integrated Systems

10.5.3. Market By Technology, Market Estimates and Forecast, USD Million, 2019-2032

10.5.3.1. Radar systems

10.5.3.2. Radio Frequency (RF) sensors

10.5.3.3. Electro-optical (EO) / Infrared (IR)

10.5.3.4. Acoustic sensors

10.5.3.5. Jamming / RF mitigation

10.5.3.6. Directed Energy / Laser

10.5.3.7. Kinetic solutions

10.5.3.8. Other

10.5.4. Market By End Use Estimates and Forecast, USD Million, 2019-2032

10.5.4.1. Military & Defense

10.5.4.2. Homeland Security

10.5.4.3. Critical Infrastructure

10.5.4.4. Commercial & Civilian

10.5.5. Market By Country, Market Estimates and Forecast, USD Million,

10.5.5.1. Brazil

10.5.5.2. Rest of LATAM

10.6. Middle East & Africa

10.6.1. Market By Platform Type Estimates and Forecast, USD Million, 2019-2032

10.6.1.1. Fix installations

10.6.1.2. Mobile Units

10.6.1.3. UAV-Based Systems

10.6.1.4. Others

10.6.2. Market By Function, Market Estimates and Forecast, USD Million, 2019-2032

10.6.2.1. Detection & Tracking

10.6.2.2. Disruption & Neutralization

10.6.2.3. Integrated Systems

10.6.3. Market By Technology, Market Estimates and Forecast, USD Million, 2019-2032

10.6.3.1. Radar systems

10.6.3.2. Radio Frequency (RF) sensors

10.6.3.3. Electro-optical (EO) / Infrared (IR)

10.6.3.4. Acoustic sensors

10.6.3.5. Jamming / RF mitigation

10.6.3.6. Directed Energy / Laser

10.6.3.7. Kinetic solutions

10.6.3.8. Other

10.6.4. Market By End Use Estimates and Forecast, USD Million, 2019-2032

10.6.4.1. Military & Defense

10.6.4.2. Homeland Security

10.6.4.3. Critical Infrastructure

10.6.4.4. Commercial & Civilian

10.6.5. Market By Country, Market Estimates and Forecast, USD Million,

10.6.5.1. Saudi Arabia

10.6.5.2. Rest of MEA

Chapter 11. Competitive Landscape

11.1. Market Revenue Share By Manufacturers

11.2. Mergers & Acquisitions

11.3. Competitor’s Positioning

11.4. Strategy Benchmarking

11.5. Vendor Landscape

11.5.1. Distributors

11.5.1.1. North America

11.5.1.2. Europe

11.5.1.3. Asia Pacific

11.5.1.4. Middle East & Africa

11.5.1.5. Latin America

Chapter 12. Company Profiles

12.1. Lockheed Martin

12.1.1. Company Overview

12.1.2. Product & Service Offerings

12.1.3. Strategic Initiatives

12.1.4. Financials

12.2. Raytheon Technologies (RTX)

12.2.1. Company Overview

12.2.2. Product & Service Offerings

12.2.3. Strategic Initiatives

12.2.4. Financials

12.3. Thales Group

12.3.1. Company Overview

12.3.2. Product & Service Offerings

12.3.3. Strategic Initiatives

12.3.4. Financials

12.4. Israel Aerospace Industries (IAI)

12.4.1. Company Overview

12.4.2. Product & Service Offerings

12.4.3. Strategic Initiatives

12.4.4. Financials

12.5. Saab AB

12.5.1. Company Overview

12.5.2. Product & Service Offerings

12.5.3. Strategic Initiatives

12.5.4. Financials

12.6. General Dynamics

12.6.1. Company Overview

12.6.2. Product & Service Offerings

12.6.3. Strategic Initiatives

12.6.4. Financials

12.7. Northrop Grumman

12.7.1. Company Overview

12.7.2. Product & Service Offerings

12.7.3. Strategic Initiatives

12.7.4. Financials

12.7.5. Conclusion

12.8. BAE Systems

12.8.1. Company Overview

12.8.2. Product & Service Offerings

12.8.3. Strategic Initiatives

12.8.4. Financials

12.8.5. Conclusion

12.9. Elbit Systems

12.9.1. Company Overview

12.9.2. Product & Service Offerings

12.9.3. Strategic Initiatives

12.9.4. Financials

12.9.5. Conclusion

12.10. DroneShield Ltd

12.10.1. Company Overview

12.10.2. Product & Service Offerings

12.10.3. Strategic Initiatives

12.10.4. Financials

12.10.5. Conclusion

12.11. Dedrone

12.11.1. Company Overview

12.11.2. Product & Service Offerings

12.11.3. Strategic Initiatives

12.11.4. Financials

12.11.5. Conclusion

12.12. QinetiQ Group plc

12.12.1. Company Overview

12.12.2. Product & Service Offerings

12.12.3. Strategic Initiatives

12.12.4. Financials

12.12.5. Conclusion

12.13. Rafael Advanced Defense Systems

12.13.1. Company Overview

12.13.2. Product & Service Offerings

12.13.3. Strategic Initiatives

12.13.4. Financials

12.13.5. Conclusion

12.14. Leonardo S.p.A.

12.14.1. Company Overview

12.14.2. Product & Service Offerings

12.14.3. Strategic Initiatives

12.14.4. Financials

12.14.5. Conclusion

Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP has segmented global Counter Drone Technology (U-CAS) market on the basis of By Platform Type, By Function, By Technology, By region for 2019 to 2032

Global Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

Global Counter Drone Technology (U-CAS) By Function (Revenue, USD Million

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

Global Counter Drone Technology (U-CAS) By Technology Use Outlook (Revenue, USD Million

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

Global Counter Drone Technology (U-CAS) By End Use (Revenue, USD Million

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- North America

- North America Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- North America Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- North America Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- North America End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- U.S

- U.S Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- U.S Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- U.S Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- U.S End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Canada

- Canada Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Canada Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Canada Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Canada End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Mexico

- Canada Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Mexico Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Mexico Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Mexico End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Europe

- Europe Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Europe Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Europe Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Europe End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Germany

- Germany Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Germany Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Germany Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Germany End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- France

- France Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- France Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- France Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- France End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- U.K

- U.K Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- U.K Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- U.K Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- U.K End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Italy

- Italy Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Italy Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Italy Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Italy End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Spain

- Spain Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Spain Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Spain Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Spain End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Benelux

- Benelux Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Benelux Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Benelux Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Benelux End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Russia

- Russia Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Russia Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Russia Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Russia End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Finland

- Finland Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Finland Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Finland Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Finland End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Sweden

- Fin Sweden land Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Sweden Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Sweden Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Sweden End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Rest of Europe

- Rest of Europe land Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Rest of Europe Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Rest of Europe Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Rest of Europe End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Asia-Pacific

- Asia-Pacific land Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Asia-Pacific Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Asia-Pacific Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Asia-Pacific End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- China

- China land Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- China Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- China Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- China End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- India

- India land Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- India Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- India Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- India End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Japan

- Japan land Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Japan Counter Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Japan Counter Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Japan End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- South Korea

- South Korea land Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- South Korea Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- South Korea Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- South Korea End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Indonesia

- Indonesia Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Indonesia Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Indonesia Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Indonesia End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Thailand

- Thailand Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Thailand Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Thailand Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Thailand End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Vietnam

- Vietnam Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Vietnam Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Vietnam Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Vietnam End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Australia

- Australia Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Australia Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Australia Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Australia End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- New Zealand

- New Zealand Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- New Zealand Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- New Zealand Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- New Zealand End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Rest of Asia-Pacific

- Rest of Asia-Pacific Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Rest of Asia-Pacific Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Rest of Asia-Pacific Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Rest of Asia-Pacific End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Brazil

- Brazil Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Brazil Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Brazil Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Brazil End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Rest of Middle East & Africa

- Rest of Middle East & Africa Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Rest of Middle East & Africa Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Rest of Middle East & Africa Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Rest of Middle East & Africa End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Latin America

- Latin America Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Latin America Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Latin America Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Latin America End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Saudi Arabia

- Saudi Arabia Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Saudi Arabia Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Saudi Arabia Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Saudi Arabia End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian

- Rest of Middle East & Africa

- Rest of Middle East & Africa Counter Drone Technology (U-CAS) Market By Platform Type Outlook (Revenue, USD Million 2019-2032),

- Fix installations

- Mobile Units

- UAV-Based Systems

- Others

- Rest of Middle East & Africa Drone Technology (U-CAS) Market By Function Outlook (Revenue, USD Million 2019-2032),

- Detection & Tracking

- Disruption & Neutralization

- Integrated Systems

- Rest of Middle East & Africa Drone Technology (U-CAS) Market By Technology Outlook (Revenue, USD Million 2019-2032),

- Radar systems

- Radio Frequency (RF) sensors

- Electro-optical (EO) / Infrared (IR)

- Acoustic sensors

- Jamming / RF mitigation

- Directed Energy / Laser

- Kinetic solutions

- Other

- Rest of Middle East & Africa End Use Outlook (Revenue, USD Million2019-2032),

- Military & Defense

- Homeland Security

- Critical Infrastructure

- Commercial & Civilian