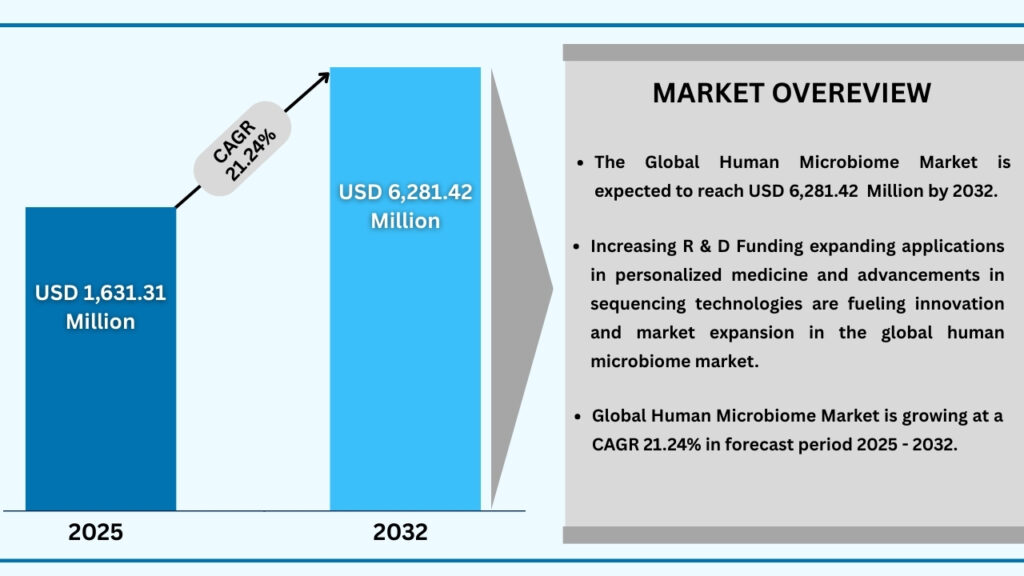

Market Synopsis

The global human microbiome market size was USD 1,345.52 million in 2024 and is expected to reach USD 6,281.42 million at a CAGR of 21.24% during the forecast period from 2025 to 2032. The global human microbiome market is witnessing strong growth, fuelled by increasing awareness of the role of gut and other microbial communities in maintaining health, rising prevalence of chronic and lifestyle-related diseases, and the growing demand for personalized and preventive healthcare solutions. The market encompasses probiotics, prebiotics, live biotherapeutics, diagnostics, and microbiome-based therapeutics that target a wide range of conditions including gastrointestinal, metabolic, autoimmune, and neurological disorders. North America currently leads the market due to advanced research and supportive regulatory frameworks, while Asia-Pacific is emerging as the fastest-growing region driven by expanding healthcare infrastructure and consumer interest in wellness products. Although challenges such as regulatory uncertainties, high development costs, and limited large-scale clinical evidence persist, advancements in sequencing technologies, bioinformatics, and microbiome modulation strategies are expected to accelerate innovation and open new opportunities in both therapeutic and consumer health applications.

Global Human Microbiome Market (USD million)

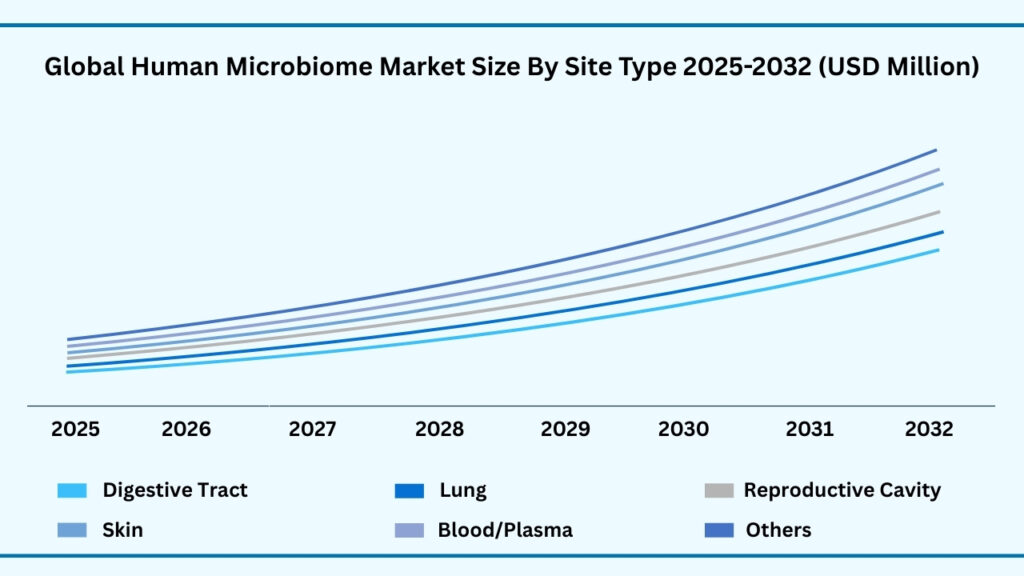

Global Human Microbiome Market by Site Insights:

Digestive tract segment accounted for market share of share 63.80% in 2024 in the global human microbiome market.

The Digestive tract segment leads the global human microbiome market, accounting for 63.80% of the share in 2024. Revenues in this category are expected to reach USD 4,014.20 million during the forecast period from 2025 to 2032, growing at a CAGR of 21.26%The digestive tract dominates the site segment, reflecting its central role in nutrient absorption, immunity, and gut health. Its leadership is driven by the strong clinical focus on gastrointestinal disorders such as irritable bowel syndrome, Crohn’s disease, and colorectal cancer, as well as the widespread adoption of probiotics, prebiotics, and live biotherapeutics. Companies like Enterome, Vedanta Biosciences, and Seres Therapeutics are spearheading therapeutic innovations in this space, while Yakult Honsha and Nestlé Health Science continue to strengthen the consumer wellness side with microbiome-based nutritional solutions.

Beyond the gut, the lung and reproductive cavity sub-segments are steadily gaining importance as research highlights the role of microbial communities in respiratory and reproductive health. Lung microbiome studies are uncovering new approaches to asthma, COPD, and pulmonary fibrosis, with biotech firms such as Synlogic and research centres like the National Jewish Health Center taking the lead. In parallel, reproductive tract microbiome research is advancing solutions for fertility, maternal health, and bacterial vaginosis, where companies like Osel Inc. and Ferring Pharmaceuticals are developing live biotherapeutics and diagnostic tools to address these needs.

Other emerging areas, including the skin, blood/plasma, musculoskeletal, and ENT microbiomes, are expanding the scope of applications in more specialized domains. The skin microbiome is attracting investments from companies such as AOBiome and L’Oréal, which are developing products for dermatological and cosmetic use, ranging from acne and eczema therapies to anti-aging solutions. In blood and plasma research, Microba Life Sciences is working on biomarker discovery to improve early detection and precision medicine. Musculoskeletal and ENT microbiomes, though still early in research, are being investigated for their links to arthritis, sinusitis, and ear infections, supported by academic collaborations. Collectively, these diverse site-specific applications are broadening the human microbiome market and driving innovation across therapeutics, diagnostics, and consumer health.

Global Human Microbiome Market, By Site Type (USD million)

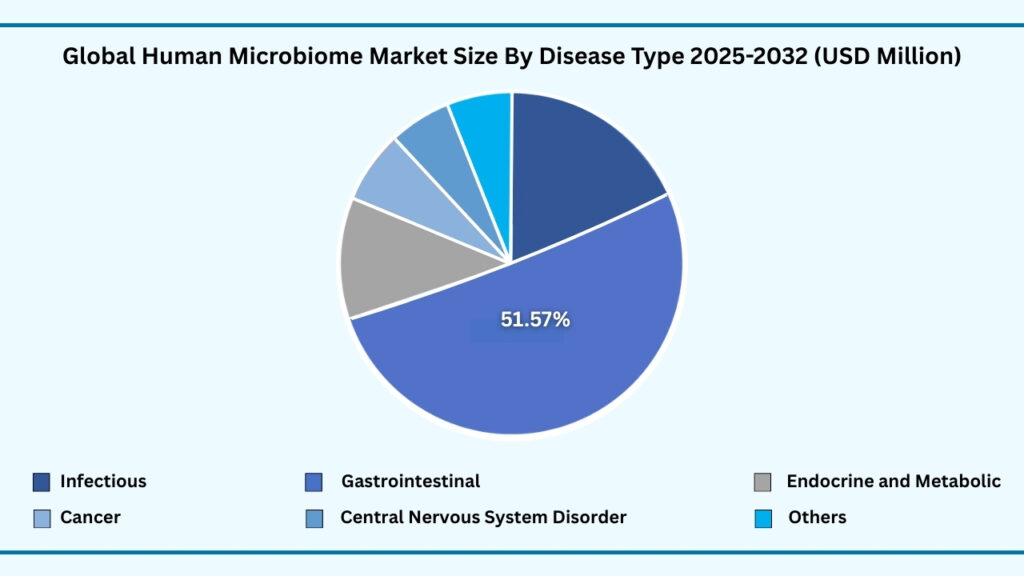

Global Human Microbiome Market by Disease Insights:

Gastrointestinal diseases segment accounted for market share of share 51.61% in 2024 in the global human microbiome market.

The Gastrointestinal Diseases segment leads the global human microbiome market, holding the largest share of 51.61% in 2024, with revenues projected to reach USD 3,247.11 million during the forecast period from 2025 to 2032 at a CAGR of 21.26%. This dominance stems from the strong link between gut microbiota and digestive health, where imbalances are associated with conditions such as inflammatory bowel disease (IBD), irritable bowel syndrome (IBS), and colorectal cancer. Advances in microbiome-based therapeutics and probiotics have accelerated the adoption of targeted solutions to restore gut microbial balance and improve patient outcomes. Companies such as Seres Therapeutics and Vedanta Biosciences are pioneering microbiome therapeutics, while Nestlé Health Science and Yakult are expanding their probiotic portfolios, ensuring broad adoption across both clinical and consumer health markets. The rising prevalence of gastrointestinal disorders globally, coupled with growing awareness of gut health, continues to drive this segment’s leadership.

Alongside this, Infectious Diseases, Cancer, Endocrine & Metabolic Disorders, and Central Nervous System (CNS) Disorders are emerging as high-potential sub-segments within the microbiome landscape. Infectious diseases are seeing promising research in fecal microbiota transplantation (FMT) and microbial therapies for recurrent Clostridioides difficile infections, supported by FDA-approved treatments such as Rebyota. Cancer-focused studies are leveraging microbiome modulation to enhance immunotherapy responses, with early-stage clinical trials showing encouraging results. Similarly, microbiome interventions in endocrine and metabolic disorders, such as obesity and type 2 diabetes, are gaining traction as researchers uncover the gut microbiota’s role in regulating metabolism and insulin sensitivity. In the CNS domain, companies like Axial Therapeutics are exploring the gut–brain axis to develop therapies for autism spectrum disorder and Parkinson’s disease, underscoring the expanding clinical applications of microbiome science.

Looking ahead, the others category, which includes autoimmune, inflammatory, and dermatological disorders, represents a promising frontier for microbiome innovation. Start-ups and established players alike are investigating the role of skin and systemic microbiota in conditions such as atopic dermatitis, psoriasis, and rheumatoid arthritis. For instance, AOBiome is developing topical microbiome-based products for skin health, while partnerships between biotech firms and academic research centres are advancing trials in autoimmune and inflammatory diseases. As microbiome science matures, the disease segment is expected to evolve into a diversified landscape, with gastrointestinal diseases anchoring current revenues while emerging sub-segments redefine the future of personalized, microbiome-driven healthcare solutions.

Global Human Mircobiome Market, By Disease (USD million)

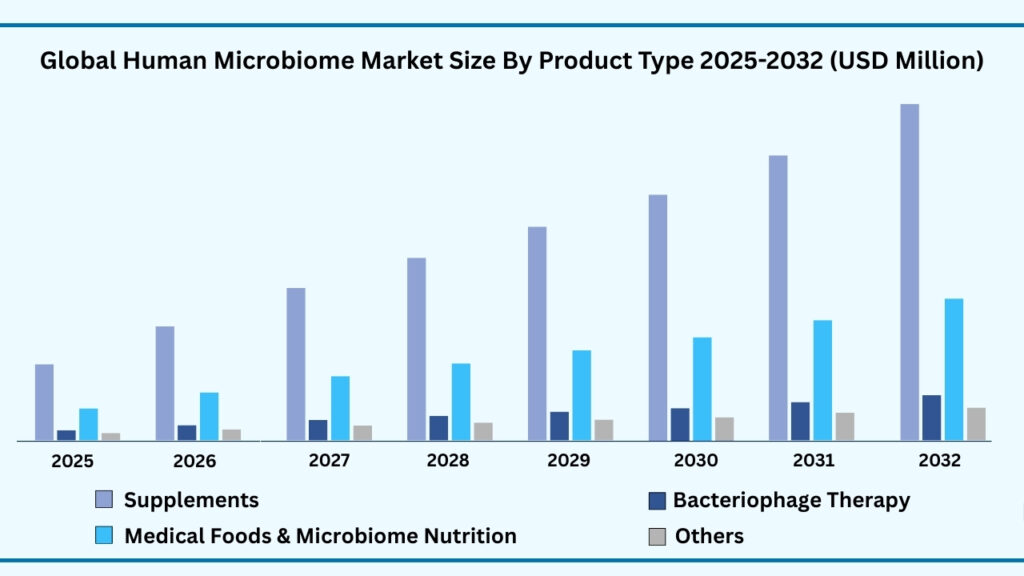

Global Human Microbiome Market by Product Type Insights:

Supplements segment accounted for market share of share 73.41% in 2024 in the global human microbiome market.

The Supplements segment leads the global human microbiome market, holding the largest share of 73.41% in 2024, with revenues projected to reach USD 4,618.78 million during the forecast period from 2025 to 2032 at a CAGR of 21.26%. This dominance is fuelled by rising consumer awareness about gut health and the widespread adoption of probiotic and prebiotic formulations to support digestive balance, immunity, and overall wellness. The ease of accessibility through pharmacies, online channels, and retail outlets has further strengthened this segment’s reach. Companies such as Nestlé Health Science, Yakult Honsha, and DSM-Firmenich are leading the way with diversified probiotic portfolios and novel supplement formulations, while start-ups are innovating with personalized solutions and Synbiotics. With increasing lifestyle-related disorders and a growing preference for preventive healthcare, supplements remain the anchor of the human microbiome product landscape.

Beyond supplements, Bacteriophage Therapy and Medical Foods & Microbiome Nutrition are rapidly emerging as high-potential sub-segments. Bacteriophage therapy is attracting renewed interest as an alternative to antibiotics in addressing antimicrobial resistance, with biotech innovators exploring targeted phage cocktails to treat bacterial infections. Meanwhile, medical foods and microbiome nutrition products are gaining traction in managing chronic conditions such as IBD, metabolic syndrome, and lactose intolerance, offering clinically validated solutions tailored to specific patient needs. Companies like Kaleido Biosciences and Enterome are developing microbiome-focused nutritional interventions, signalling a shift toward integrating therapeutic and dietary approaches. These sub-segments, though smaller today, are positioned to transform the treatment and prevention landscape in the coming years.

Looking ahead, the others category, encompassing drugs, diagnostics, and postbiotics, represents a promising frontier of microbiome innovation. The development of microbiome-based drugs is progressing through clinical pipelines, with several candidates under investigation for gastrointestinal, metabolic, and neurological conditions. Diagnostics are also gaining relevance, with companies such as uBiome (before its closure) and emerging players working to profile gut microbiota for personalized health insights. Postbiotics—non-viable microbial products that confer health benefits—are also drawing interest as stable, safe alternatives to traditional probiotics. Together, these innovations reflect the market’s transition from conventional supplements to advanced, science-driven solutions, ensuring that while supplements continue to dominate revenues, emerging product types will redefine the future scope and clinical utility of microbiome-based products.

Global Human Microbiome Market, By Product Type (USD million)

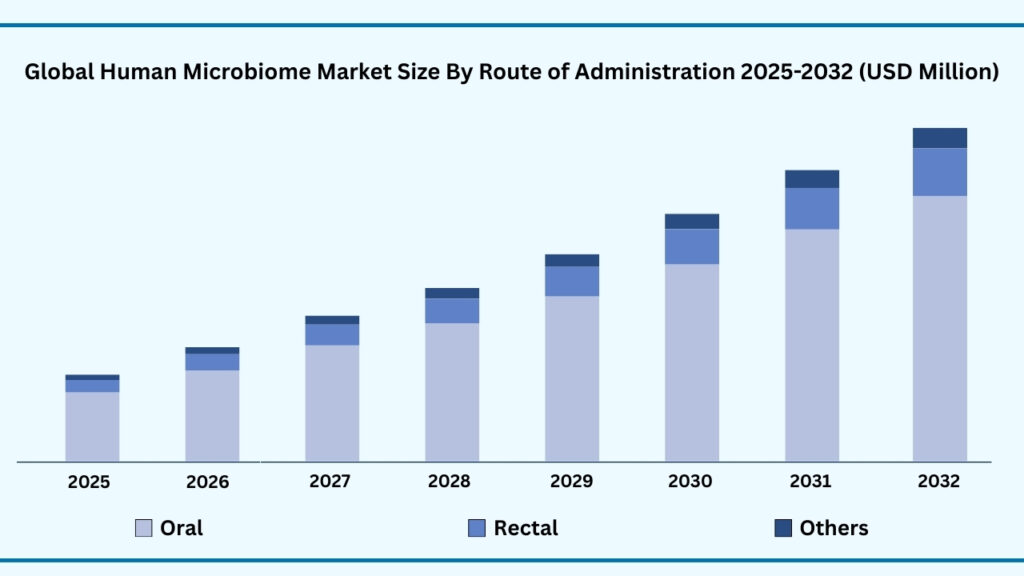

Global Human Microbiome Market by Route of Administration Insights:

Oral segment accounted for market share of share 88.05% in 2024 in the global human microbiome market.

The Oral route of administration leads the global human microbiome market, capturing the largest share of 88.05% in 2024, with revenues projected to reach USD 5,535.47 million by the end of the forecast period from 2025 to 2032 at a CAGR of 21.25%. This dominance is largely due to the convenience, safety, and wide acceptance of oral formulations such as probiotics, prebiotics, and microbiome-targeted drugs. Oral delivery directly influences the gut microbiota, which plays a central role in digestion, metabolism, immunity, and overall health. The market has witnessed rapid growth in easy-to-consume products like capsules, powders, and functional foods, which are increasingly integrated into both clinical use and consumer wellness routines. Companies like Yakult, Nestlé Health Science, and Seres Therapeutics are leading innovation in this space, driving global adoption through a mix of nutraceuticals and prescription-grade microbiome therapies.

In comparison, the Rectal route of administration serves as a critical niche, particularly in therapeutic approaches such as fecal microbiota transplantation (FMT) for recurrent Clostridioides difficile infections (CDI) and other gastrointestinal conditions. Rectal delivery enables direct targeting of the lower gastrointestinal tract, offering higher efficacy in certain disease states where oral formulations may have limited reach. FDA-approved products like Rebyota highlight the clinical potential of this route, while ongoing trials are evaluating its broader applications in inflammatory bowel disease (IBD) and ulcerative colitis. Although less widely adopted due to procedural complexities and patient acceptance, the rectal route plays an indispensable role in specific therapeutic contexts where precision and localized impact are essential.

The Others category, which includes injectable, nasal, and vaginal routes, is gradually gaining recognition as research expands into systemic and localized microbiome interventions. Injectable microbiome therapies are being explored for conditions requiring rapid systemic impact, while nasal delivery is under investigation for targeting the gut–brain axis in neurological disorders such as autism and Parkinson’s disease. Vaginal microbiome therapies are another emerging frontier, with companies like Osel Inc. developing products aimed at restoring balance and preventing infections. Though currently representing a smaller market share, these alternative routes demonstrate the versatility of microbiome-based interventions and are expected to grow steadily as scientific understanding and delivery technologies advance. Together, oral formulations anchor accessibility and mass adoption, rectal therapies secure targeted GI outcomes, and alternative routes open new possibilities for systemic and specialized applications, shaping a balanced and evolving route of administration landscape.

Global Human Microbiome Market, By Route of Administration (USD million)

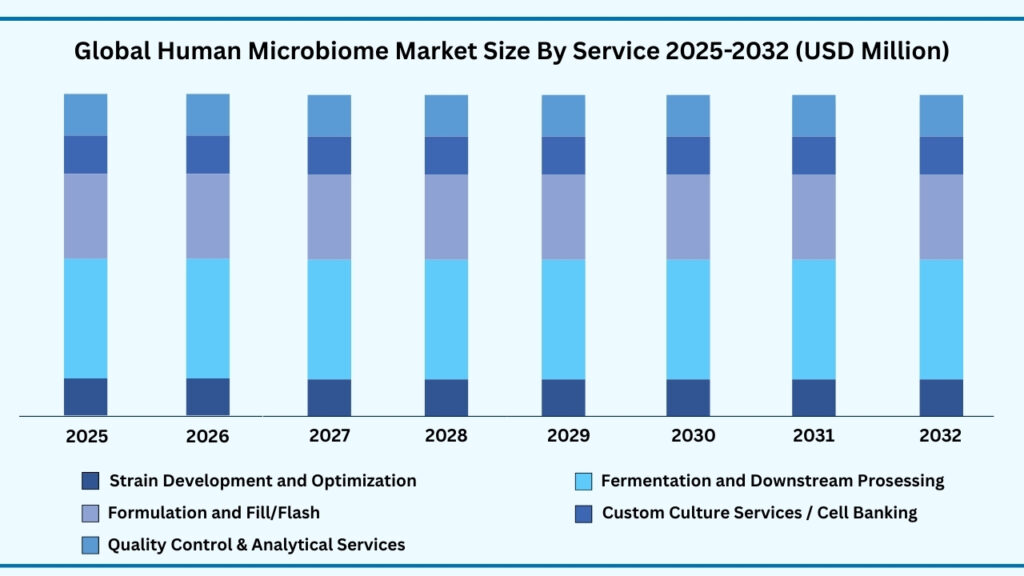

Global Human Microbiome Market by Services Insights:

Fermentation and Downstream Processing segment accounted for market share of share 36.14% in 2024 in the global human microbiome market.

The Fermentation and Downstream Processing segment leads the global human microbiome services market, capturing the largest share of 36.14% in 2024, with revenues projected to reach USD 2,273.49 million during the forecast period from 2025 to 2032 at a CAGR of 21.26%. This leadership stems from the central role of fermentation in cultivating microbial strains at scale and downstream processing in ensuring purity, stability, and functionality of microbiome-based products. These services are essential for producing probiotics, live biotherapeutics, and microbiome-derived metabolites under strict quality and regulatory standards. Contract research and manufacturing organizations (CROs and CDMOs) are increasingly relied upon by biotech and pharmaceutical companies to provide scalable, GMP-compliant fermentation solutions. For example, firms such as Lonza and WuXi Biologics are advancing capabilities in microbial fermentation and purification, enabling faster development and commercialization of microbiome therapies and supplements.

Beyond fermentation, other service areas are witnessing strong demand as the microbiome industry matures. Strain Development and Optimization is key to identifying and engineering microbial strains with enhanced therapeutic efficacy, stability, or metabolic function, often using synthetic biology approaches. Formulation and Fill/Finish services ensure that microbial products retain viability and consistency across diverse delivery formats such as capsules, powders, or liquid suspensions. Custom Culture Services and Cell Banking are also gaining traction, supporting long-term preservation of proprietary strains and patient-derived samples for future R&D applications. Together, these services provide the technical backbone for companies ranging from early-stage biotech start-ups to established nutraceutical players, accelerating the path from discovery to market launch.

Complementing these, Quality Control and Analytical Services are becoming indispensable in safeguarding product integrity and regulatory compliance. With increasing scrutiny from agencies like the FDA and EMA, robust analytical methods are required to assess strain identity, potency, contamination, and clinical safety. Companies such as Eurofins Scientific and Charles River Laboratories are expanding their microbiome-focused testing portfolios to support global clients in clinical trials and commercial manufacturing. While fermentation and downstream processing currently dominate due to their critical role in large-scale production, the growth of complementary services highlights a broader trend: the move toward fully integrated service ecosystems. This balanced service landscape ensures scalability, safety, and innovation, making it possible for microbiome products to progress from the lab bench to patients and consumers worldwide.

Global Human Microbiome Market, By Services (USD million)

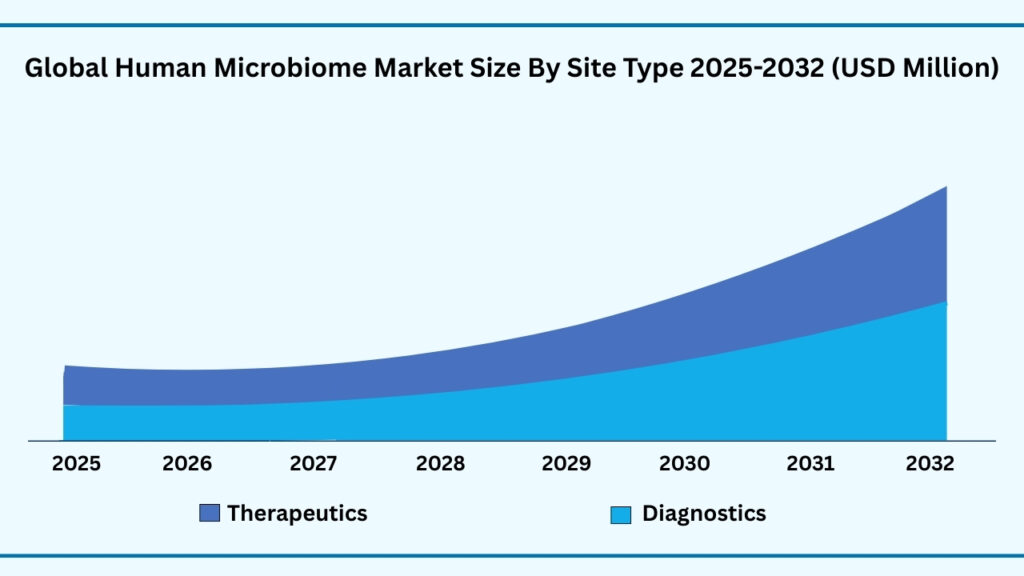

Global Human Microbiome Market by Application Insights:

Therapeutics segment accounted for market share of share 64.98% in 2024 in the global human microbiome market.

The Therapeutics segment leads the global human microbiome market, accounting for the largest share of 64.98% in 2024, with revenues projected to reach USD 4,085.09 million by the end of the forecast period from 2025 to 2032, growing at a CAGR of 21.25%. This dominance is fuelled by the rapid advancement of microbiome-based therapies targeting gastrointestinal, metabolic, and infectious diseases, alongside growing interest in immuno-oncology. Live biotherapeutic products, fecal microbiota transplantation (FMT), and next-generation probiotics are increasingly being adopted to restore microbial balance and improve patient outcomes. For example, Seres Therapeutics’ Vowst, an FDA-approved oral microbiome therapeutic for recurrent Clostridioides difficile infection, underscores how microbiome interventions are transitioning from experimental concepts into mainstream clinical solutions. Pharmaceutical companies and biotech innovators alike are investing heavily in this space, establishing therapeutics as the anchor of microbiome applications.

Alongside therapeutics, the Diagnostics sub-segment is emerging as a vital area, leveraging microbiome profiling and advanced sequencing technologies to detect disease signatures and monitor treatment responses. Microbiome diagnostics are being explored in a wide range of conditions, from colorectal cancer and inflammatory bowel disease (IBD) to metabolic and neurological disorders, by identifying microbial biomarkers that correlate with disease progression. Companies such as BiomeDx and Microba Life Sciences are pioneering diagnostic platforms that use gut microbiome analysis to deliver actionable health insights. With rising adoption of precision medicine, these diagnostic tools are expected to play a crucial role in enabling earlier disease detection, risk stratification, and individualized care strategies.

In comparison, while therapeutics currently dominate due to their direct clinical impact and commercial traction, diagnostics are carving out a complementary and fast-growing role by supporting preventive healthcare and personalized treatment planning. This dual growth trajectory reflects the market’s evolution toward an integrated model, where therapeutics drive disease modification and diagnostics provide guidance for optimized outcomes. Together, these applications are not only shaping the way microbiome science is translated into healthcare but also ensuring that both treatment and detection advance in tandem to improve patient care on a global scale.

Global Human Microbiome Market, By Application (USD million)

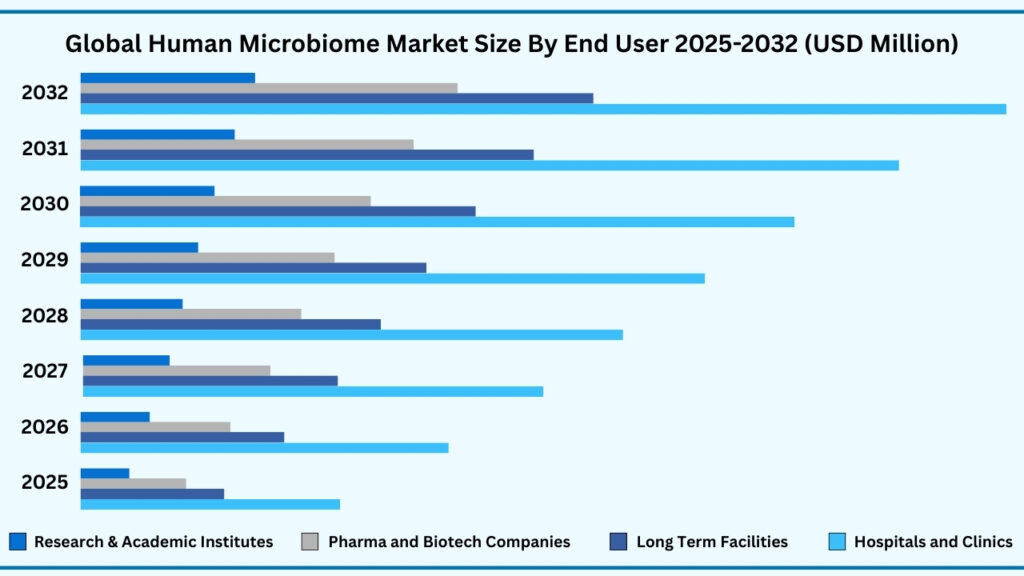

Global Human Microbiome Market by End User Insights:

Hospitals and Clinics segment accounted for market share of share 64.98% in 2024 in the global human microbiome market.

The Hospitals and Clinics segment represents the largest share of the organoid market, accounting for 48.87% in 2024. Revenues from this segment are projected to reach USD 3,074.57 million during the forecast period from 2025 to 2032, expanding at a CAGR of 21.26%. Hospitals and clinics have become central to the adoption of organoid technologies because they directly connect cutting-edge science to patient care. Organoids are increasingly used in personalized medicine, where miniature patient-derived models allow clinicians to predict drug responses before prescribing treatments. For example, in oncology, hospitals are beginning to integrate organoid testing into decision-making for chemotherapy, ensuring therapies are more effective and reducing unnecessary side effects. With the rising demand for precision diagnostics and tailored treatment strategies, healthcare providers are investing in organoid platforms as practical tools for improving clinical outcomes.

Beyond frontline hospitals, long-term care facilities are slowly integrating organoid-based insights into their care pathways, particularly for managing age-related conditions like neurodegenerative disorders. Although adoption here is at an early stage, organoids are helping researchers understand disease progression in Alzheimer’s and Parkinson’s, which can eventually guide better long-term treatment protocols. Meanwhile, pharma and biotech companies are major accelerators of organoid technology, leveraging them to streamline preclinical drug discovery, toxicity screening, and clinical trial design. By reducing reliance on animal models and offering human-relevant data, organoids are helping companies cut costs, lower attrition rates, and bring therapies to market faster. Their use in regenerative medicine pipelines also highlights their growing value in translating research breakthroughs into tangible therapies.

The role of research and academic institutes is equally critical, as these institutions remain the innovation engines of organoid science. Universities and dedicated research centres are pioneering new techniques such as gene-edited organoids for rare disease modelling and microfluidic integration for more physiologically relevant systems. Collaborations between academic labs and healthcare providers are expanding, ensuring that novel organoid methods move quickly from the bench to the bedside. In this way, hospitals and clinics serve as the primary adopters and largest end-user group, while long-term care, pharma/biotech, and academic institutions create a complementary ecosystem that drives innovation, scales applications, and extends the clinical impact of organoids worldwide.

Global Human Microbiome Market, By End User (USD million)

Global Human Microbiome Market by Region Insights:

North America segment accounted for market share of share 42.51% in 2024 in the global human microbiome market.

The North America region dominates the global organoid market, holding 42.51% of the share in 2024. Revenues from this region are projected to reach USD 2,676.88 million during the forecast period, expanding at a CAGR of 21.28%. The leadership of North America is largely attributed to strong investments in biotechnology and advanced healthcare infrastructure, which foster the rapid adoption of organoid platforms. Academic centres, hospitals, and pharmaceutical companies across the U.S. and Canada are actively using organoids for drug discovery, precision medicine, and disease modelling. For instance, patient-derived tumour organoid programs supported by institutions like the National Cancer Institute are helping to accelerate oncology research and clinical trial design. With regulatory bodies such as the FDA increasingly encouraging alternatives to animal testing, North America continues to provide a fertile environment for organoid innovation and commercialization.

In Europe, organoid research is thriving due to strong public funding, cross-border collaborations, and an emphasis on ethical standards in biomedical research. Countries such as Germany, the Netherlands, and the U.K. are leading hubs, with academic institutions and biopharma companies actively developing organoid models for gastrointestinal, neurological, and infectious diseases. Europe’s supportive regulatory environment, combined with initiatives like Horizon Europe, has accelerated organoid adoption for both research and clinical translation. Meanwhile, the Asia Pacific region is witnessing the fastest growth, propelled by expanding biotech industries in China, Japan, South Korea, and India. Rising healthcare investments and increasing focus on precision medicine are encouraging widespread organoid applications across oncology, infectious disease studies, and regenerative medicine. Governments and private investors in the region are also prioritizing cutting-edge research, making Asia Pacific a hotspot for future expansion.

In comparison, Latin America (LATAM) and the Middle East & Africa (MEA) represent emerging markets that are gradually integrating organoid technologies into their biomedical ecosystems. While adoption is at an earlier stage, countries like Brazil and South Africa are beginning to establish partnerships with international research institutions to leverage organoids in infectious disease research and regenerative therapies. These regions face infrastructure and funding limitations, but growing awareness, medical tourism, and increasing investment in advanced healthcare systems are creating pathways for future growth. Overall, North America continues to anchor the market with its mature ecosystem, Europe sustains momentum with strong collaborations, Asia Pacific fuels rapid expansion, and LATAM and MEA provide new opportunities that will shape the long-term global outlook for organoid applications.

Global Human Microbiome Market, By Region (USD million)

Major Companies and Competitive Landscape

The global human microbiome market is advancing at a remarkable pace, shaped by strong competition and rapid scientific progress from both leading life sciences companies and innovative startups. Industry players are increasingly focusing on partnerships, acquisitions, and cross-sector collaborations to expand their portfolios and strengthen their technological capabilities. A central priority is improving methods for microbiome profiling, developing standardized analytical tools, and enhancing reproducibility in clinical research. At the same time, efforts are being directed toward translating microbiome discoveries into scalable therapeutics, diagnostics, and nutrition-based applications. These strategies aim to accelerate the commercialization of microbiome-based interventions, reduce development risks, and broaden access to personalized healthcare solutions. Key companies active in the global human microbiome market include:

- Baseclear B.V.

- Beijing Genomics Institute (BGI) Genomics Co., Ltd

- Charles River Laboratories International Inc.

- Clinical Microbiomics A/S

- Eurofins Scientific SE

- GENEWIZ, Inc.

- Illumina, Inc.

- Novogene Corporation

- OraSure Technologies, Inc.

- Oxford Nanopore Technologies, Inc.

- Pacific Biosciences of California, Inc.

- QIAGEN N.V.

- Second Genome, Inc.

- Thermo Fisher Scientific Inc.

- Viome, Inc.

- CosmosID

- Leucine Rich Bio Pvt. Ltd.

- Microba

- Microbiome Insights Inc.

- Molzym GmbH & Co. KG.

- AOBiome

- Synlogic

- Evelo Biosciences

- Pendulum Therapeutics

- Enterome

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 1,631.31 Million |

| CAGR (2024–2032) | 21.24% |

| Revenue forecast to 2033 | USD 6,281.42 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Site, By Disease, By Product Type, By Route of Administration, By Services, By Application, By End User and By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, Rest of MEA |

| Key companies profiled | Baseclear B.V., BGI Genomics Co., Ltd, Charles River Laboratories International Inc., Clinical Microbiomics A/S, Eurofins Scientific SE, GENEWIZ Inc., Illumina Inc., Novogene Corporation, OraSure Technologies Inc., Oxford Nanopore Technologies Inc., Pacific Biosciences of California Inc., QIAGEN N.V., Second Genome Inc., Thermo Fisher Scientific Inc., Viome Inc., CosmosID, Leucine Rich Bio Pvt. Ltd., Microba, Microbiome Insights Inc., Molzym GmbH & Co. KG., AOBiome, Synlogic, Evelo Biosciences, Pendulum Therapeutics, and Enterome |

| Customization scope | 10 hours of free customization and expert consultation |

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of global Human microbiome market

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1.Primary

2.1.2.Secondary

2.1.3.Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1.Market value

2.3.2.Market volume

2.3.3.Exchange rate

2.3.4.Price

2.3.5.Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2019-2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10. Formulation & manufacturing

4.11. Distribution & retail

4.12. Import-export analysis

4.13. Brand comparative analysis

4.14. Technological advancements

4.15. Porter’s five force

4.15.1. Threat of new entrants

4.15.1.1. Capital requirment

4.15.1.2. Product knowledge

4.15.1.3. Technical knowledge

4.15.1.4. Customer relation

4.15.1.5. Access to appliation and technology

4.15.2. Threat of substitutes

4.15.2.1. Cost

4.15.2.2. Performance

4.15.2.3. Availability

4.15.2.4. Technical knowledge

4.15.2.5. Durability

4.15.3. Bargainning power of buyers

4.15.3.1. Numbers of buyers relative to suppliers

4.15.3.2. Product differentiation

4.15.3.3. Threat of forward integration

4.15.3.4. Buyers volume

4.15.4. Bargainning power of suppliers

4.15.4.1. Suppliers concentration

4.15.4.2. Buyers switching cost to other suppliers

4.15.4.3. Threat of backward integration

4.15.5. Bargainning power of suppliers

4.15.5.1. Industry concentration

4.15.5.2. Industry growth rate

4.15.5.3. Product differentiation

4.15.6. Patent analysis

4.16. Patent quality and strength

4.17. Regulation coverage

4.18. Pricing analysis

4.19. Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1.Rising prevalence of lifestyle-related diseases, gastrointestinal disorders, and metabolic

syndromes boosting demand for microbiome-based solutions

5.1.2.Advances in metagenomics, next-generation sequencing (NGS), and bioinformatics

accelerating microbiome research and applications

5.1.3.Increasing collaborations among pharma, biotech, and academic institutions to develop

microbiome-based therapeutics, probiotics, and diagnostics

5.2. Restraints

5.2.1.Lack of standardization in microbiome analysis, characterization, and clinical validation

5.2.2.Limited awareness among healthcare providers and patients about microbiome-based

interventions

5.3. Opportunities

5.3.1.Growing potential of microbiome-based personalized nutrition, precision medicine, and

targeted therapies

5.3.2.Expansion in applications across oncology, neurology (gut-brain axis), dermatology, and

immunology

5.3.3.Increasing investment in microbiome-derived drug discovery, fecal microbiota

transplantation (FMT), and live biotherapeutic products (LBPs)

5.4. Threat

5.4.1.Stringent and evolving regulatory frameworks for safety, efficacy, and clinical trial

approval of microbiome-based products

5.4.2.Intellectual property challenges in proprietary microbial strains, data ownership, and

formulation methods

5.4.3.Supply chain vulnerabilities in sourcing probiotics, live cultures, and advanced

sequencing technologies

Chapter 6. Global Human Microbiome Market By SIte Insights & Trends, Revenue (USD Million)

6.1. Site Dynamics & Market Share, 2019–2032

6.1.1.Digestive Tract

6.1.2.Lung

6.1.3.Reproductive Cavity

6.1.4.Skin

6.1.5.Blood/Plasma

6.1.6.Others (Musculoskeletal, ENT)

Chapter 7. Global Human Microbiome Market By Disease Insights & Trends, Revenue (USD

Million)

7.1. Disease Dynamics & Market Share, 2019-2032

7.2. Infectious Diseases

7.3. Gastrointestinal diseases

7.4. Endocrine and metabolic diseases

7.5. Cancer

7.6. Central Nervous System (CNS) disorder

7.6.1.Others (Autoimmune & Inflammatory, Dermatological Disorders)

Chapter 8. Global Human Microbiome Market By Product Type Insights & Trends, Revenue

(USD Million)

8.1. Product Type Dynamics & Market Share, 2019-2032

8.1.1.Drugs

8.1.2.Supplements

8.1.2.1. Probiotics

8.1.2.2. Prebiotics

8.1.2.3. Synbiotics

8.1.3.Bacteriophage Therapy

8.1.4.Medical Foods & Microbiome Nutrition

8.1.5.Others (Postbiotics, Diagnostics)

Chapter 9. Global Human Microbiome Market By Route of Administration Insights & Trends,

Revenue (USD Million)

9.1. Route of Administration Dynamics & Market Share, 2019-2032

9.1.1.Oral route of administration

9.1.2.Rectal route of administration

9.1.3.Others (injectable, nasal, vaginal)

Chapter 10. Global Human Microbiome Market By Services Insights & Trends, Revenue (USD

Million)

10.1. Services Dynamics & Market Share, 2019-2032

10.1.1. Strain Development and Optimization

10.1.2. Fermentation and Downstream Processing

10.1.3. Formulation and Fill/Flash

10.1.4. Quality Control & Analytical Services

10.1.5. Custom Culture Services / Cell Banking

Chapter 11. Global Human Microbiome Market By Application Insights & Trends, Revenue (USD

Million)

11.1. Application Dynamics & Market Share, 2019-2032

11.1.1. Therapeutics

11.1.2. Diagnostics

Chapter 12. Global Human Microbiome Market By End User Insights & Trends, Revenue (USD

Million)

12.1. End User Dynamics & Market Share, 2019-2032

12.1.1. Hospitals and Clinics

12.1.2. Long-Term Care Facilities

12.1.3. Pharma and Biotech Companies

12.1.4. Research & Academic Institutes

Chapter 13. Global Human Microbiome Market By Services Insights & Trends, Revenue (USD

Million)

13.1. Dynamics & Market Share, 2019-2032

Chapter 14. Global Human MicrobiomeMarket Regional Outlook

14.1. Global Human Microbiome Market Share By Region, 2019-2032

14.2. North America

14.3. Market By Site, Market Estimates and Forecast, USD Million

14.3.1.Digestive Tract

14.3.2.Lung

14.3.3.Reproductive Cavity

14.3.4.Skin

14.3.5.Blood/Plasma

14.3.6.Others (Musculoskeletal, ENT)

14.4. Market By Disease, Market Estimates and Forecast, USD Million

14.4.1.Infectious Diseases

14.4.2.Gastrointestinal diseases

14.4.3.Endocrine and metabolic diseases

14.4.4.Cancer

14.4.5.Central Nervous System (CNS) disorder

14.4.6.Others (Autoimmune & Inflammatory, Dermatological Disorders)

14.5. Market By Product Type, Market Estimates and Forecast, USD Million

14.5.1.Drugs

14.5.2.Supplements

14.5.2.1. Probiotics

14.5.2.2. Prebiotics

14.5.2.3. Synbiotics

14.5.3. Bacteriophage Therapy

14.5.4. Medical Foods & Microbiome Nutrition

14.5.5. Others (Postbiotics, Diagnostics)

14.6. Market By Route of Administration, Market Estimates and Forecast, USD Million

14.6.1. Oral route of administration

14.6.2. Rectal route of administration

14.6.3. Others (injectable, nasal, vaginal)

14.7. Market Services, Market Estimates and Forecast, USD Million

14.7.1. Strain Development and Optimization

14.7.2. Fermentation and Downstream Processing

14.7.3. Formulation and Fill/Flash

14.7.4. Quality Control & Analytical Services

14.7.5. Custom Culture Services / Cell Banking

14.8. Market Application, Market Estimates and Forecast, USD Million

14.8.1. Therapeutics

14.8.2. Diagnostics

14.9. Market End User, Market Estimates and Forecast, USD Million

14.9.1. Hospitals and Clinics

14.9.2. Long-Term Care Facilities

14.9.3. Pharma and Biotech Companies

14.9.4. Research & Academic Institutes

14.10. Market By Country, Market Estimates and Forecast, USD Million

14.10.1. US

14.10.2. Canada

14.10.3. Mexico

14.11. Europe

14.11.1. Market By Site, Market Estimates and Forecast, USD Million

14.11.1.1. Digestive Tract

14.11.1.2. Lung

14.11.1.3. Reproductive Cavity

14.11.1.4. Skin

14.11.1.5. Blood/Plasma

14.11.1.6. Others (Musculoskeletal, ENT)

14.11.2.Market By Disease, Market Estimates and Forecast, USD Million

14.11.2.1. Infectious Diseases

14.11.2.2. Gastrointestinal diseases

14.11.2.3. Endocrine and metabolic diseases

14.11.2.4. Cancer

14.11.2.5. Central Nervous System (CNS) disorder

14.11.2.6. Others (Autoimmune & Inflammatory, Dermatological Disorders)

14.11.3.Market By Product Type, Market Estimates and Forecast, USD Million

14.11.3.1. Drugs

14.11.3.2. Supplements

14.11.3.2.1. Probiotics

14.11.3.2.2. Prebiotics

14.11.3.2.3. Synbiotics

14.11.3.3. Bacteriophage Therapy

14.11.3.4. Medical Foods & Microbiome Nutrition

14.11.3.5. Others (Postbiotics, Diagnostics)

14.11.4.Market By Route of Admisnistration, Market Estimates and Forecast, USD Million

14.11.4.1. Oral route of administration

14.11.4.2. Rectal route of administration

14.11.4.3. Others (injectable, nasal, vaginal)

14.11.5.Market By Services, Market Estimates and Forecast, USD Million

14.11.5.1. Strain Development and Optimization

14.11.5.2. Fermentation and Downstream Processing

14.11.5.3. Formulation and Fill/Flash

14.11.5.4. Quality Control & Analytical Services

14.11.5.5. Custom Culture Services / Cell Banking

14.11.6.Market Application, Market Estimates and Forecast, USD Million

14.11.6.1. Therapeutics

14.11.6.2. Diagnostics

14.11.7.Market End User, Market Estimates and Forecast, USD Million

14.11.7.1. Hospitals and Clinics

14.11.7.2. Long-Term Care Facilities

14.11.7.3. Pharma and Biotech Companies

14.11.7.4. Research & Academic Institutes

14.11.8.Market By Country, Market Estimates and Forecast, USD Million

14.11.8.1. Germany

14.11.8.2. France

14.11.8.3. U.K

14.11.8.4. Italy

14.11.8.5. Spain

14.11.8.6. Benelux

14.11.8.7. Russia

14.11.8.8. Finland

14.11.8.9. Sweden

14.11.8.10. Rest Of Europe

14.12. Asia-Pacific

14.13. Market By Site, Market Estimates and Forecast, USD Million

14.13.1. Digestive Tract

14.13.2. Lung

14.13.3. Reproductive Cavity

14.13.4. Skin

14.13.5. Blood/Plasma

14.13.6. Others (Musculoskeletal, ENT)

14.14. Market By Disease, Market Estimates and Forecast, USD Million

14.14.1. Infectious Diseases

14.14.2. Gastrointestinal diseases

14.14.3. Endocrine and metabolic diseases

14.14.4. Cancer

14.14.5. Central Nervous System (CNS) disorder

14.14.6. Others (Autoimmune & Inflammatory, Dermatological Disorders)

14.15. Market By Product Type, Market Estimates and Forecast, USD Million

14.15.1. Drugs

14.15.2. Supplements

14.15.2.1.Probiotics

14.15.2.2.Prebiotics

14.15.2.3.Synbiotics

14.15.3. Bacteriophage Therapy

14.15.4. Medical Foods & Microbiome Nutrition

14.15.5. Others (Postbiotics, Diagnostics)

14.16. Market By Route of Administration, Market Estimates and Forecast, USD Million

14.16.1. Oral route of administration

14.16.2. Rectal route of administration

14.16.3. Others (injectable, nasal, vaginal)

14.17. Market By Services, Market Estimates and Forecast, USD Million

14.17.1. Strain Development and Optimization

14.17.2. Fermentation and Downstream Processing

14.17.3. Formulation and Fill/Flash

14.17.4. Quality Control & Analytical Services

14.17.5. Custom Culture Services / Cell Banking

14.18. Market Application, Market Estimates and Forecast, USD Million

14.18.1. Therapeutics

14.18.2. Diagnostics

14.19. Market End User, Market Estimates and Forecast, USD Million

14.19.1. Hospitals and Clinics

14.19.2. Long-Term Care Facilities

14.19.3. Pharma and Biotech Companies

14.19.4. Research & Academic Institutes

14.20. Market By Country, Market Estimates and Forecast, USD Million

14.20.1. China

14.20.2. India

14.20.3. Japan

14.20.4. South Korea

14.20.5. Indonesia

14.20.6. Thailand

14.20.7. Vietnam

14.20.8. Australia

14.20.9. New Zeland

14.20.10. Rest of APAC

14.21. Latin America

14.22. Market By Site, Market Estimates and Forecast, USD Million

14.22.1. Digestive Tract

14.22.2. Lung

14.22.3. Reproductive Cavity

14.22.4. Skin

14.22.5. Blood/Plasma

14.22.6. Others (Musculoskeletal, ENT)

14.23. Market By Disease, Market Estimates and Forecast, USD Million

14.23.1. Infectious Diseases

14.23.2. Gastrointestinal diseases

14.23.3. Endocrine and metabolic diseases

14.23.4. Cancer

14.23.5. Central Nervous System (CNS) disorder

14.23.6. Others (Autoimmune & Inflammatory, Dermatological Disorders)

14.24. Market By Product Type, Market Estimates and Forecast, USD Million

14.24.1. Drugs

14.24.2. Supplements

14.24.2.1.Probiotics

14.24.2.2.Prebiotics

14.24.2.3.Synbiotics

14.24.3. Bacteriophage Therapy

14.24.4. Medical Foods & Microbiome Nutrition

14.24.5. Others (Postbiotics, Diagnostics)

14.25. Market By Route of Administration, Market Estimates and Forecast, USD Million

14.25.1. Oral route of administration

14.25.2. Rectal route of administration

14.25.3. Others (injectable, nasal, vaginal)

14.26. Market By Services, Market Estimates and Forecast, USD Million

14.26.1. Strain Development and Optimization

14.26.2. Fermentation and Downstream Processing

14.26.3. Formulation and Fill/Flash

14.26.4. Quality Control & Analytical Services

14.26.5. Custom Culture Services / Cell Banking

14.27. Market Application, Market Estimates and Forecast, USD Million

14.27.1. Therapeutics

14.27.2. Diagnostics

14.28. Market End User, Market Estimates and Forecast, USD Million

14.28.1. Hospitals and Clinics

14.28.2. Long-Term Care Facilities

14.28.3. Pharma and Biotech Companies

14.28.4. Research & Academic Institutes

14.29. Market By Country, Market Estimates and Forecast, USD Million

14.29.1. Brazil

14.29.2. Rest of LATAM

14.30. Middle East & Africa

14.31. Market By Site, Market Estimates and Forecast, USD Million

14.31.1. Digestive Tract

14.31.2. Lung

14.31.3. Reproductive Cavity

14.31.4. Skin

14.31.5. Blood/Plasma

14.31.6. Others (Musculoskeletal, ENT)

14.32. Market By DIsease, Market Estimates and Forecast, USD Million

14.32.1. Infectious Diseases

14.32.2. Gastrointestinal diseases

14.32.3. Endocrine and metabolic diseases

14.32.4. Cancer

14.32.5. Central Nervous System (CNS) disorder

14.32.6. Others (Autoimmune & Inflammatory, Dermatological Disorders)

14.33. Market By Product Type, Market Estimates and Forecast, USD Million

14.33.1. Drugs

14.33.2. Supplements

14.33.2.1.Probiotics

14.33.2.2.Prebiotics

14.33.2.3.Synbiotics

14.33.3. Bacteriophage Therapy

14.33.4. Medical Foods & Microbiome Nutrition

14.33.5. Others (Postbiotics, Diagnostics)

14.34. Market By Route of Administration, Market Estimates and Forecast, USD Million

14.34.1. Oral route of administration

14.34.2. Rectal route of administration

14.34.3. Others (injectable, nasal, vaginal)

14.35. Market By Services, Market Estimates and Forecast, USD Million

14.35.1. Strain Development and Optimization

14.35.2. Fermentation and Downstream Processing

14.35.3. Formulation and Fill/Flash

14.35.4. Quality Control & Analytical Services

14.35.5. Custom Culture Services / Cell Banking

14.36. Market Application, Market Estimates and Forecast, USD Million

14.36.1. Therapeutics

14.36.2. Diagnostics

14.37. Market End User, Market Estimates and Forecast, USD Million

14.37.1. Hospitals and Clinics

14.37.2. Long-Term Care Facilities

14.37.3. Pharma and Biotech Companies

14.37.4. Research & Academic Institutes

14.38. Market By Country, Market Estimates and Forecast, USD Million

14.38.1. Saudi Arabia

14.38.2. UAE

14.38.3. South Africa

14.38.4. Turkey

14.38.5. Rest of MEA

Chapter 15. Competitive Landscape

15.1. Market Revenue Share By Manufacturers

15.2. Mergers & Acquisitions

15.3. Competitor’s Positioning

15.4. Strategy Benchmarking

15.5. Vendor Landscape

15.6. Distributors

15.6.1.North America

15.6.2.Europe

15.6.3.Asia Pacific

15.6.4.Middle East & Africa

15.6.5.Latin America

15.7. Others

Chapter 16. Company Profiles

16.1. Baseclear B.V.

16.1.1. Company Overview

16.1.2. Product & Service Offerings

16.1.3. Strategic Initiatives

16.1.4. Financials

16.1.5. Conclusion

16.2. Beijing Genomics Institute (BGI) Genomics Co., Ltd

16.2.1. Company Overview

16.2.2. Product & Service Offerings

16.2.3. Strategic Initiatives

16.2.4. Financials

16.2.5. Conclusion

16.3. Charles River Laboratories International Inc.

16.3.1. Company Overview

16.3.2. Product & Service Offerings

16.3.3. Strategic Initiatives

16.3.4. Financials

16.3.5. Conclusion

16.4. Clinical Microbiomics A/S

16.4.1. Company Overview

16.4.2. Product & Service Offerings

16.4.3. Strategic Initiatives

16.4.4. Financials

16.4.5. Conclusion

16.5. Eurofins Scientific SE

16.5.1. Company Overview

16.5.2. Product & Service Offerings

16.5.3. Strategic Initiatives

16.5.4. Financials

16.5.5. Conclusion

16.6. GENEWIZ, Inc.

16.6.1. Company Overview

16.6.2. Product & Service Offerings

16.6.3. Strategic Initiatives

16.6.4. Financials

16.6.5. Conclusion

16.7. Illumina, Inc.

16.7.1. Company Overview

16.7.2. Product & Service Offerings

16.7.3. Strategic Initiatives

16.7.4. Financials

16.7.5. Conclusion

16.8. Novogene Corporation

16.8.1. Company Overview

16.8.2. Product & Service Offerings

16.8.3. Strategic Initiatives

16.8.4. Financials

16.8.5. Conclusion

16.9. OraSure Technologies, Inc.

16.9.1. Company Overview

16.9.2. Product & Service Offerings

16.9.3. Strategic Initiatives

16.9.4. Financials

16.9.5. Conclusion

16.10. Oxford Nanopore Technologies, Inc.

16.10.1. Company Overview

16.10.2. Product & Service Offerings

16.10.3. Strategic Initiatives

16.10.4. Financials

16.10.5. Conclusion

16.11. Pacific Biosciences of California, Inc.

16.11.1. Company Overview

16.11.2. Product & Service Offerings

16.11.3. Strategic Initiatives

16.11.4. Financials

16.11.5. Conclusion

16.12. QIAGEN N.V.

16.12.1. Company Overview

16.12.2. Product & Service Offerings

16.12.3. Strategic Initiatives

16.12.4. Financials

16.12.5. Conclusion

16.13. Second Genome, Inc.

16.13.1. Company Overview

16.13.2. Product & Service Offerings

16.13.3. Strategic Initiatives

16.13.4. Financials

16.13.5. Conclusion

16.14. Thermo Fisher Scientific Inc.

16.14.1. Company Overview

16.14.2. Product & Service Offerings

16.14.3. Strategic Initiatives

16.14.4. Financials

16.14.5. Conclusion

16.15. Viome, Inc.

16.15.1. Company Overview

16.15.2. Product & Service Offerings

16.15.3. Strategic Initiatives

16.15.4. Financials

16.15.5. Conclusion

16.16. CosmosID

16.16.1. Company Overview

16.16.2. Product & Service Offerings

16.16.3. Strategic Initiatives

16.16.4. Financials

16.16.5. Conclusion

16.17. Leucine Rich Bio Pvt. Ltd.

16.17.1. Company Overview

16.17.2. Product & Service Offerings

16.17.3. Strategic Initiatives

16.17.4. Financials

16.17.5. Conclusion

16.18. Microba

16.18.1. Company Overview

16.18.2. Product & Service Offerings

16.18.3. Strategic Initiatives

16.18.4. Financials

16.18.5. Conclusion

16.19. Microbiome Insights Inc.

16.19.1. Company Overview

16.19.2. Product & Service Offerings

16.19.3. Strategic Initiatives

16.19.4. Financials

16.19.5. Conclusion

16.20. Molzym GmbH & Co. KG.

16.20.1. Company Overview

16.20.2. Product & Service Offerings

16.20.3. Strategic Initiatives

16.20.4. Financials

16.20.5. Conclusion

16.21. AOBiome

16.21.1. Company Overview

16.21.2. Product & Service Offerings

16.21.3. Strategic Initiatives

16.21.4. Financials

16.21.5. Conclusion

16.22. Synlogic

16.22.1. Company Overview

16.22.2. Product & Service Offerings

16.22.3. Strategic Initiatives

16.22.4. Financials

16.22.5. Conclusion

16.23. Evelo Biosciences

16.23.1. Company Overview

16.23.2. Product & Service Offerings

16.23.3. Strategic Initiatives

16.23.4. Financials

16.23.5. Conclusion

16.24. Pendulum Therapeutics

16.24.1. Company Overview

16.24.2. Product & Service Offerings

16.24.3. Strategic Initiatives

16.24.4. Financials

16.24.5. Conclusion

16.25. Enterome

16.25.1. Company Overview

16.25.2. Product & Service Offerings

16.25.3. Strategic Initiatives

16.25.4. Financials

16.25.5. Conclusion

Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP. has segmented global human microbiome market on the basis of By Site, By Disease, Product Type, By Route of Administration, By Services, By Application, By End User and by region for 2019 to 2032.

- Global Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- Global Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- Global Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- Global Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- Global Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- Global Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- Global End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- North America

- North America Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- North America Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- North America Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- North America Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- North America Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- North America Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- North America End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- U.S

- U.S Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- U.S Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- U.S Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- U.S Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- U.S Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- U.S Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- U.S End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- Canada

- Canada Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- Canada Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- Canada Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- Canada Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- Canada Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- Canada Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- Canada End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- Mexico

- Mexico Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- Mexico Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- Mexico Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- Mexico Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- Mexico Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- Mexico Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- Mexico End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- Europe

- Europe Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- Europe Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- Europe Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- Europe Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- Europe Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- Europe Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- Europe End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- Germany

- Germany Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- Germany Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- Germany Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- Germany Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- Germany Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- Germany Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- Germany End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- France

- France Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- France Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- France Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- France Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- France Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- France Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- France End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- U.K

- U.K Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- U.K Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- U.K Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- U.K Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- U.K Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- U.K Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- U.K End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- Italy

- Italy Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- Italy Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- Italy Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- Italy Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- Italy Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- Italy Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- Italy End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- Spain

- Spain Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- Spain Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- Spain Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- Spain Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- Spain Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- Spain Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- Spain End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- Benelux

- Benelux Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- Benelux Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- Benelux Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- Benelux Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- Benelux Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- Benelux Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- Benelux End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- Russia

- Russia Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- Russia Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- Russia Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- Russia Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- Russia Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- Russia Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- Russia End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- Finland

- Finland Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- Finland Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- Finland Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- Finland Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- Finland Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- Finland Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- Finland End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- Sweden

- Sweden Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- Sweden Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- Sweden Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- Sweden Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- Sweden Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- Sweden Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- Sweden End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- Rest of Europe

- Rest of Europe Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- Rest of Europe Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- Rest of Europe Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- Rest of Europe Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- Rest of Europe Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- Rest of Europe Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- Rest of Europe End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes

- Asia-Pacific

- Asia-Pacific Site Outlook (Revenue, USD Million; 2019-2032)

- Digestive Tract

- Lung

- Reproductive Cavity

- Skin

- Blood/Plasma

- Others (Musculoskeletal, ENT)

- Asia-Pacific Disease Outlook (Revenue, USD Million; 2019-2032)

- Infectious Diseases

- Gastrointestinal diseases

- Endocrine and metabolic diseases

- Cancer

- Central Nervous System (CNS) disorder

- Others (Autoimmune & Inflammatory, Dermatological Disorders)

- Asia-Pacific Product Type Outlook (Revenue, USD Million; 2019-2032)

- Drugs

- Supplements

- Probiotics

- Prebiotics

- Synbiotics

- Bacteriophage Therapy

- Medical Foods & Microbiome Nutrition

- Others (Postbiotics, Diagnostics)

- Asia-Pacific Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Oral route of administration

- Rectal route of administration

- Others (injectable, nasal, vaginal)

- Asia-Pacific Route of Administration Outlook (Revenue, USD Million; 2019-2032)

- Strain Development and Optimization

- Fermentation and Downstream Processing

- Formulation and Fill/Flash

- Quality Control & Analytical Services

- Custom Culture Services / Cell Banking

- Asia-Pacific Application Outlook (Revenue, USD Million; 2019-2032)

- Therapeutics

- Diagnostics

- Asia-Pacific End User Outlook (Revenue, USD Million; 2019-2032)

- Hospitals and Clinics

- Long-Term Care Facilities

- Pharma and Biotech Companies

- Research & Academic Institutes