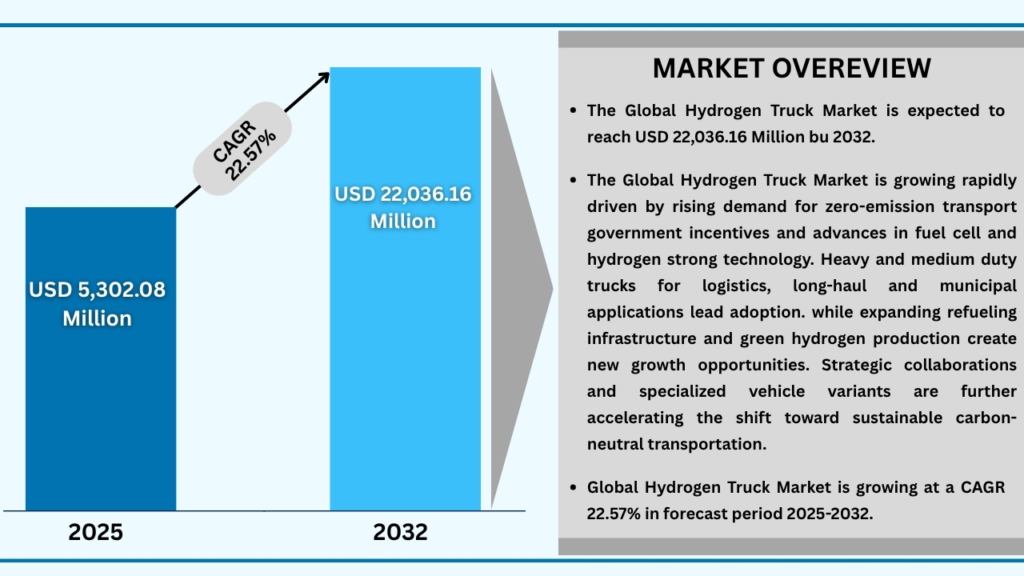

Market Synopsis

The global hydrogen truck market size was USD 4,325.76 million in 2024 and is expected to reach USD 22,036.16 million at a CAGR of 22.57% during the forecast period from 2025 to 2032. The global hydrogen truck market is witnessing steady growth as the push for sustainable and zero-emission transportation intensifies. Hydrogen-powered trucks are gaining traction in heavy-duty and long-haul applications due to their long driving ranges, quick refuelling, and ability to reduce carbon emissions compared to diesel and even battery-electric alternatives. Adoption is being strongly supported in North America and Europe through decarbonization policies and hydrogen infrastructure development, while Asia-Pacific, led by China, Japan, and South Korea, is emerging as a high-growth region driven by government roadmaps and industrial expansion. Although challenges such as high production costs, limited refuelling infrastructure, and reliance on affordable green hydrogen remain, advancements in fuel cell technology, hydrogen storage, and large-scale production are rapidly addressing these barriers. With increasing global commitments to net-zero targets, hydrogen trucks are set to become a critical driver of sustainable logistics and the future of heavy-duty mobility.

Global Hydrogen Truck Market (USD million)

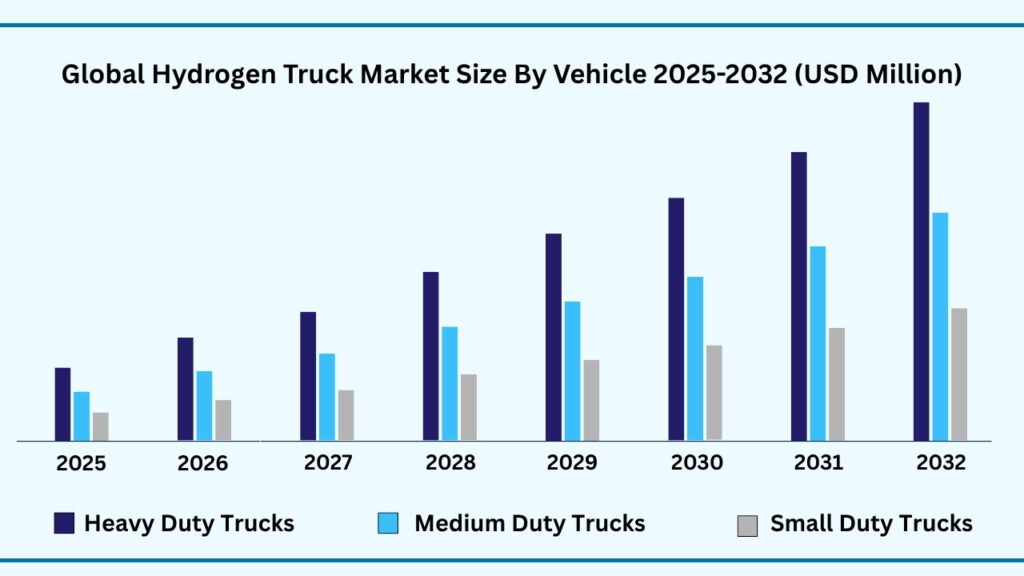

Global Hydrogen Truck Market by Vehicle Insights:

Heavy-duty trucks segment accounted for market share of share 52.21% in 2024 in the global hydrogen truck market.

The heavy-duty truck segment holds the dominant share of 52.21% in the global hydrogen truck market in 2024, with revenues expected to reach USD 11,518.70 million and a strong CAGR of 22.59% through 2032. This leadership is driven by the segment’s suitability for long-haul freight, logistics, and industrial transport, where hydrogen fuel cells offer the dual advantages of extended driving ranges and quick refuelling, while maintaining high payload efficiency. Global players such as Daimler Truck, Volvo, Hyundai, and Toyota are spearheading innovation in this category, with pilot projects already showcasing commercial viability. Hyundai’s XCIENT fuel cell trucks, for example, are actively operating in Switzerland and South Korea, proving hydrogen’s real-world potential to decarbonize large-scale logistics. Governments and fleet operators are increasingly collaborating to expand hydrogen corridors and refuelling networks, which further reinforces the growth momentum of heavy-duty applications.

In comparison, medium- and small-duty hydrogen trucks, though smaller in current market share, are emerging as vital growth engines for urban and regional transport. Medium-duty trucks are finding traction in city logistics, municipal services, and regional distribution, offering a sustainable solution where emissions regulations are tightening and battery-electric vehicles face operational constraints like charging downtime. Small-duty trucks, on the other hand, are becoming attractive for last-mile delivery and e-commerce logistics, where quick refuelling and longer operational hours provide an edge over conventional electric vans. Startups and niche manufacturers are increasingly exploring compact hydrogen truck designs, positioning them to capture future demand as green hydrogen production scales up. Together, these segments highlight the versatility of hydrogen across different freight needs, paving the way for a cleaner, more resilient global transport ecosystem.

Global Hydrogen Truck Market, By Vehicle (USD million)

Global Hydrogen Truck Market by Motor Power Insights:

200-400 KW segment accounted for market share of share 45.40% in 2024 in the global hydrogen truck market.

The 200–400 kW motor power segment leads the global hydrogen truck market, holding the largest share of 45.40% in 2024. Revenues in this category are projected to reach USD 10,013.02 million during the forecast period from 2025 to 2032, growing at a strong CAGR of 22.58%. Trucks in this power range dominate due to their balance of performance, efficiency, and adaptability for medium- to long-haul transport. They are particularly well-suited for logistics companies seeking reliable alternatives to diesel vehicles without compromising on payload capacity or driving range. Global manufacturers such as Daimler Truck, Volvo, and Hyundai are actively focusing on this segment, integrating fuel cell stacks optimized for consistent power delivery. Pilot projects in Europe and North America have already demonstrated that 200–400 kW hydrogen trucks can seamlessly handle regional freight distribution, setting the stage for large-scale adoption.

The up to 200 kW category, while smaller in market share, plays a significant role in lighter-duty applications such as city logistics, last-mile delivery, and municipal services. Trucks in this power range are increasingly used in urban environments where shorter routes, frequent stops, and strict emissions regulations drive demand for cleaner and more flexible solutions. Their lower power requirements make them more cost-effective, and combined with hydrogen’s quick refuelling advantage, they provide fleet operators with higher daily utilization rates compared to battery-electric vans. Several startups and regional manufacturers are designing compact hydrogen trucks under this category to serve e-commerce logistics and urban freight networks, particularly in densely populated regions of Asia-Pacific.

The above 400 kW segment, though still in its early stages, represents a critical frontier for the future of heavy-duty hydrogen trucking. These high-power models are tailored for demanding applications such as long-haul freight, cross-border transport, and specialized industrial uses where higher torque and endurance are essential. Early prototypes and demonstration projects in the U.S. and Europe are showcasing how above 400 kW hydrogen trucks can achieve performance levels comparable to conventional diesel-powered heavy-duty vehicles, but with zero tailpipe emissions. As infrastructure and fuel supply chains mature, this segment is expected to gain traction among logistics operators handling energy-intensive routes. Together, the growth across all three sub-segments highlights the flexibility of hydrogen fuel cell technology in addressing diverse power needs, reinforcing its role as a cornerstone in the decarbonization of global transport.

Global Hydrogen Truck Market, By Motor Power (USD million)

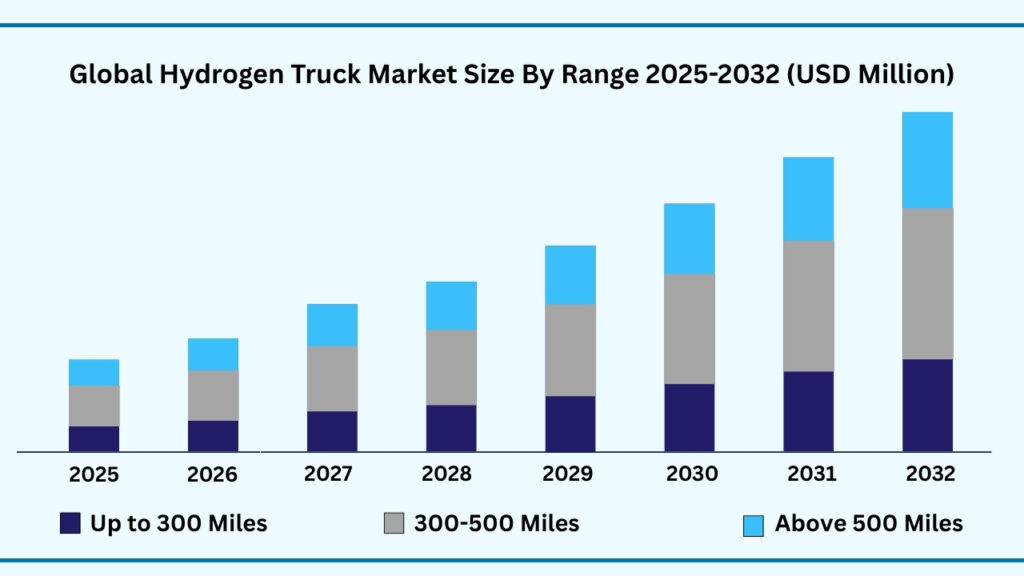

Global Hydrogen Truck Market by Range Insights:

300-500 Miles segment accounted for market share of share 45.58% in 2024 in the global hydrogen truck market.

The 300–500 miles range segment leads the global hydrogen truck market, capturing the largest share of 45.58% in 2024. Revenues in this category are projected to reach USD 10,067.84 million during the forecast period from 2025 to 2032, expanding at a CAGR of 22.61%. Trucks in this range dominate the segment as they strike the right balance between long-haul efficiency and operational flexibility, making them ideal for regional logistics and intercity transport. Fleet operators are increasingly adopting trucks in this category because they combine extended driving capability with relatively quick refueling, addressing one of the key barriers faced by electric alternatives. Companies such as Daimler Truck, Volvo, and Hyundai are advancing vehicle platforms in this range, with several demonstration projects already underway in Europe, North America, and Asia to showcase their commercial viability for logistics and freight distribution.

The up to 300 miles category continues to play an important role, particularly in short-haul and urban delivery operations where range requirements are lower but efficiency and sustainability remain priorities. These trucks are especially suitable for last-mile delivery, municipal services, and regional supply chains that operate on fixed, predictable routes. Hydrogen’s advantage of fast refuelling ensures these vehicles can complete multiple trips per day, providing higher operational uptime compared to battery-electric trucks. Startups and specialized manufacturers are increasingly targeting this category to meet the needs of e-commerce growth and city logistics, particularly in regions like Asia-Pacific where demand for compact, efficient transport solutions is rising.

The above 500 miles segment, while still developing, is poised to play a crucial role in transforming long-haul freight and cross-border transportation. These high-range hydrogen trucks are designed to replicate and eventually replace the performance of traditional diesel-powered heavy-duty vehicles, making them suitable for routes that demand high endurance and minimal downtime. Early trials in the U.S. and Europe are exploring above-500-mile trucks for logistics corridors, with companies collaborating on hydrogen fuelling hubs along major highways. As green hydrogen production and refuelling infrastructure expand, this segment is expected to see greater adoption, unlocking opportunities for truly long-distance, zero-emission trucking. Together, the growing adoption across all three range categories highlights the adaptability of hydrogen technology, with the 300–500 miles segment anchoring today’s market while shorter- and longer-range models pave the way for a diversified and sustainable transport future.

Global Hydrogen Truck Market, By Range (USD million)

Global Hydrogen Truck Market by Hydrogen Tank Size Insights:

30-60 KG segment accounted for market share of share 54.20% in 2024 in the global hydrogen truck market.

The 30–60 kg hydrogen tank size segment dominates the global hydrogen truck market, capturing the largest share of 54.20% in 2024. Revenues from this category are expected to reach USD 11,964.54 million by the end of the forecast period, growing at a CAGR of 22.60%. This leadership is largely due to the optimal balance these tanks provide between storage capacity and vehicle performance, making them well-suited for medium- to long-haul operations. Trucks equipped with 30–60 kg tanks offer extended driving ranges while maintaining manageable weight and space requirements, ensuring practical integration into existing logistics systems. Major manufacturers, including Hyundai, Volvo, and Daimler Truck, are actively deploying vehicles with this tank size for regional freight corridors, supported by government-backed hydrogen fuelling infrastructure in regions such as Europe and North America.

In comparison, below 30 kg tanks cater to lighter-duty applications, particularly in urban transport and short-haul delivery services. These smaller tanks are easier to integrate into compact vehicle designs, making them ideal for municipal fleets, last-mile logistics, and e-commerce delivery where frequent stops and shorter ranges dominate operations. Hydrogen’s fast refuelling capability provides a strong advantage in this segment, enabling higher vehicle utilization rates compared to battery-electric alternatives. Startups and specialized manufacturers are increasingly targeting this category to address the growing demand for zero-emission vehicles in densely populated cities, especially in Asia-Pacific, where strict emissions norms and rapid urbanization are driving innovation in compact hydrogen mobility solutions.

The above 60 kg segment, while still developing, is positioned to play a critical role in heavy-duty and long-haul freight transport. These larger tanks are designed for trucks covering extensive routes with minimal downtime, offering the endurance needed for cross-border logistics and energy-intensive industrial applications. Early demonstrations in the U.S. and Europe are already showcasing hydrogen trucks with high-capacity tanks performing on par with conventional diesel vehicles, but without emissions. As advancements in lightweight tank materials and refuelling infrastructure expand, the adoption of above 60 kg hydrogen storage systems is expected to accelerate, particularly among fleet operators managing high-mileage transport routes. Together, the three sub-segments reflect how hydrogen tank sizes are tailored to diverse operational needs, with the 30–60 kg category leading today’s market while smaller and larger tanks carve specialized roles in the evolving ecosystem of zero-emission trucking.

Global Hydrogen Truck Market, By Hydrogen Tank Size (USD million)

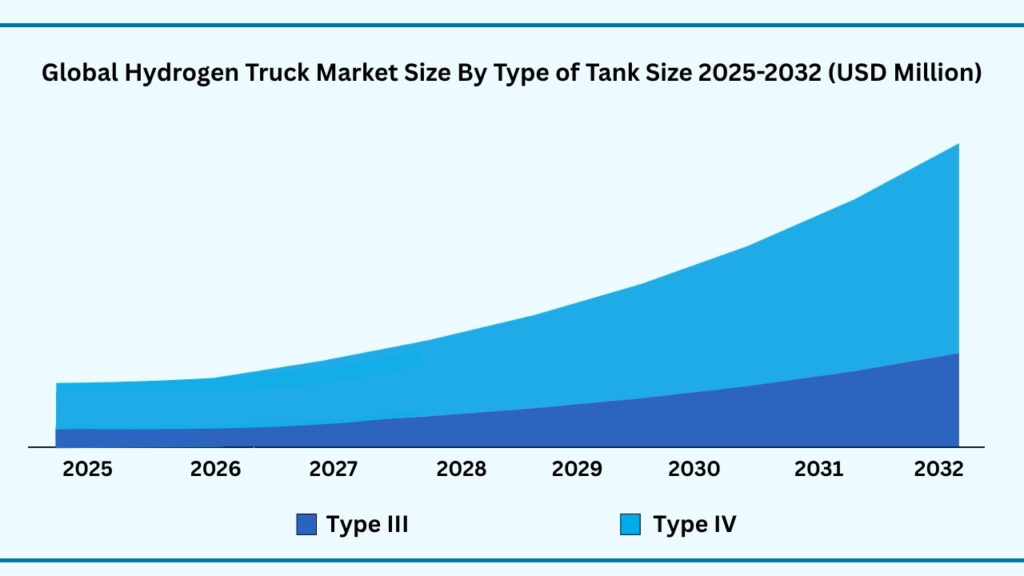

Global Hydrogen Truck Market by Type of Tank Insights:

Type IV segment accounted for market share of share 67.88% in 2024 in the global hydrogen truck market.

The Type IV tank segment leads the global hydrogen truck market, capturing the largest share of 67.88% in 2024. Revenues from this category are expected to reach USD 14,962.94 million during the forecast period, growing at a CAGR of 22.58%. Type IV tanks dominate due to their lightweight composite construction, which combines a polymer liner with a full carbon fiber wrap, significantly reducing vehicle weight while maximizing hydrogen storage capacity. This makes them especially suitable for medium- and long-haul trucks, where efficiency, payload, and range are critical. Global leaders such as Toyota, Daimler Truck, and Hyundai are increasingly adopting Type IV tanks in their hydrogen truck platforms, recognizing their ability to deliver both safety and high performance. The rising number of demonstration fleets in Europe, North America, and Asia highlights the growing confidence in Type IV tanks as the backbone of commercial hydrogen mobility.

Type III tanks, while representing a smaller market share, remain important in the hydrogen truck ecosystem. Constructed with a metallic liner wrapped in carbon fiber composites, these tanks offer high strength and durability, making them attractive for applications where mechanical robustness is a priority. Their slightly higher weight compared to Type IV tanks can limit efficiency in long-haul operations, but they are well-suited for shorter-range applications or where cost considerations play a bigger role. Several regional manufacturers and pilot projects continue to deploy Type III tanks for urban and medium-duty hydrogen trucks, ensuring their ongoing relevance in the market.

Looking ahead, the interplay between Type III and Type IV technologies reflects the industry’s focus on balancing performance, cost, and safety. While Type IV tanks are expected to anchor the majority of future growth due to their efficiency and ability to extend driving ranges, Type III tanks will continue to serve niche applications and provide transitional solutions where infrastructure or cost constraints exist. Together, these tank types highlight the innovation and adaptability shaping the hydrogen truck market, ensuring that vehicles can meet diverse operational needs while driving forward the global shift to zero-emission freight transport.

Global Hydrogen Truck Market, By Type of Tank (USD million)

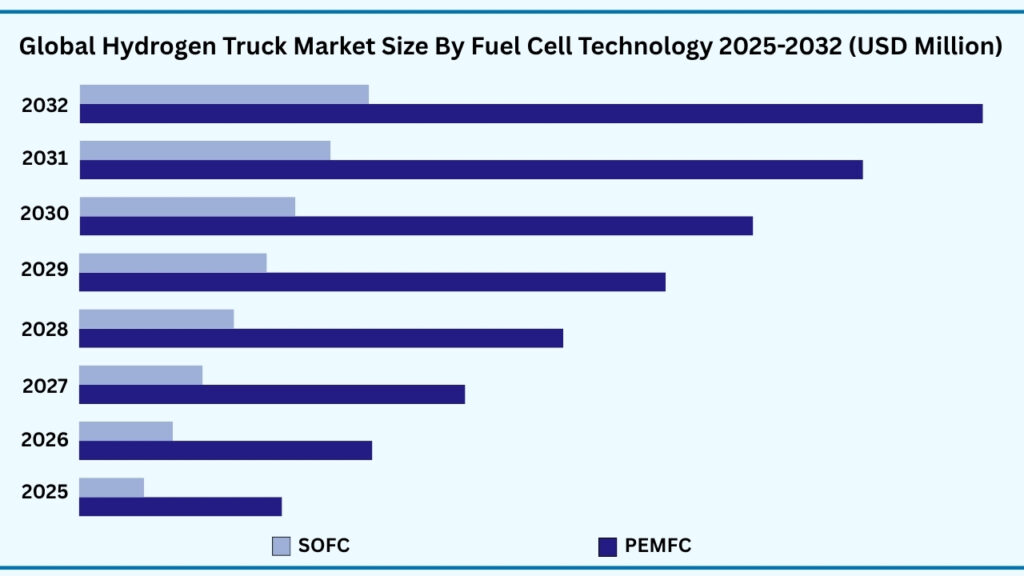

Global Hydrogen Truck Market by Fuel Cell Technology Insights:

PEMFC segment accounted for market share of share 83.25% in 2024 in the global hydrogen truck market.

The Proton Exchange Membrane Fuel Cell (PEMFC) segment holds the dominant position in the global hydrogen truck market, accounting for the largest share of 83.25% in 2024. Revenues from this category are projected to reach USD 18,367.66 million by the end of the forecast period, growing at a CAGR of 22.59%. This leadership is primarily attributed to PEMFC’s high efficiency, compact design, and quick start-up capability, which make it particularly suitable for heavy-duty and commercial transport applications. Their ability to operate at relatively low temperatures while delivering consistent power output ensures reliable performance in real-world trucking conditions. Global automotive leaders such as Toyota, Hyundai, and Daimler Truck are prioritizing PEMFC technology in their hydrogen vehicle platforms, with commercial deployments like Hyundai’s XCIENT fuel cell trucks and Toyota’s partnerships in logistics networks demonstrating its strong market potential.

In comparison, the Solid Oxide Fuel Cell (SOFC) segment, though smaller in current adoption, is emerging as an area of interest due to its ability to operate at very high efficiencies and its versatility in using different types of fuels, including hydrogen and biofuels. SOFCs are particularly valued for their durability and long operating life, which make them attractive for stationary power generation and, increasingly, for potential heavy-duty transport applications. However, challenges such as high operating temperatures and longer start-up times have so far limited their widespread use in trucks. Nonetheless, several pilot projects and research initiatives in Europe and North America are exploring SOFC integration into transport systems, signalling a gradual but important role for this technology in the future hydrogen mobility landscape.

Together, the dominance of PEMFC and the emerging opportunities for SOFC illustrate the diverse technological foundations shaping the hydrogen truck market. While PEMFC continues to anchor large-scale commercialization thanks to its proven adaptability and performance, SOFC represents a longer-term innovation pathway with the potential to complement or enhance next-generation hydrogen solutions. This combination ensures that the industry can balance immediate deployment needs with future advancements, reinforcing fuel cell technology as a central pillar in the global transition toward zero-emission heavy-duty transport.

Global Hydrogen Truck Market, By Fuel Cell Technology (USD million)

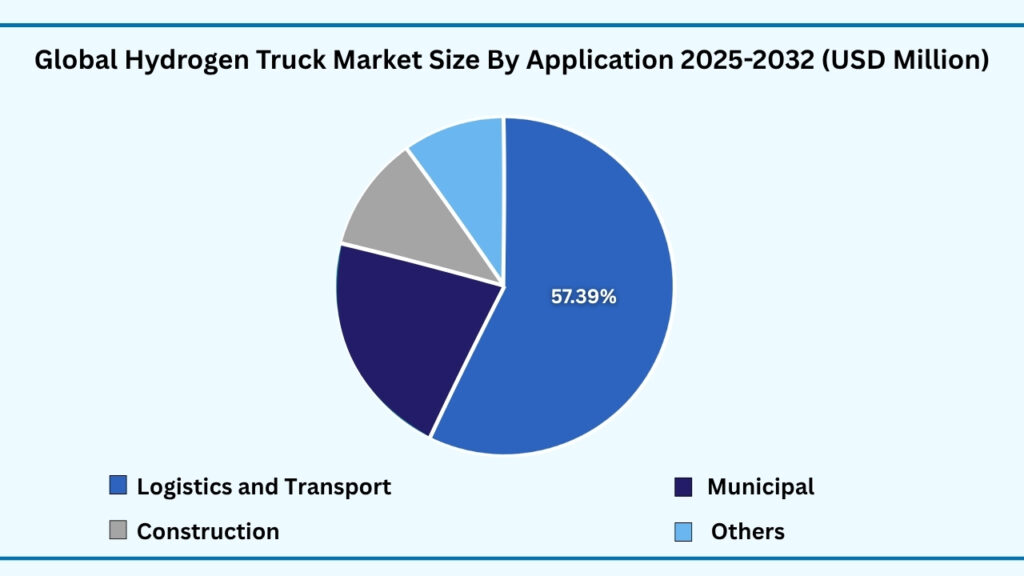

Global Hydrogen Truck Market by Application Insights:

Logistics segment accounted for market share of share 57.46% in 2024 in the global hydrogen truck market.

The Logistics and Transport segment holds the largest share in the global hydrogen truck market, accounting for 57.46% in 2024. Revenues from this segment are projected to reach USD 12,687.71 million during the forecast period, growing at a strong CAGR of 22.60%. Logistics companies and long-haul transport operators are increasingly turning to hydrogen-powered trucks as a sustainable alternative to diesel fleets, driven by the need to cut emissions and comply with stricter environmental regulations. Hydrogen trucks offer long driving ranges, fast refuelling times, and strong payload capacity features that are critical for supply chain efficiency. For example, companies like DHL and DB Schenker have started piloting hydrogen trucks for regional and cross-border freight operations, underlining how this technology is becoming central to green logistics strategies.

Beyond logistics, the Municipal segment is emerging as another important adopter, with city authorities investing in hydrogen-powered refuse collection vehicles, buses, and utility trucks to improve urban air quality. Municipal fleets often follow fixed routes and require high uptime, making hydrogen an ideal solution to replace diesel in reducing noise and emissions in densely populated areas. Similarly, the Construction segment is gradually exploring hydrogen trucks and machinery to decarbonize heavy-duty operations at worksites. Construction projects, which often demand robust performance under harsh conditions, are beginning to test hydrogen trucks for transporting raw materials and equipment, supporting the sector’s transition toward more sustainable infrastructure development.

Meanwhile, the others category, which includes sectors such as mining, agriculture, and port operations, highlights the versatility of hydrogen trucks in specialized industrial environments. Mining companies, for instance, are experimenting with hydrogen-powered haul trucks to reduce reliance on diesel in remote locations, while port authorities are testing hydrogen vehicles to cut emissions in freight handling. Together, these application areas form a dynamic ecosystem, where logistics leads large-scale adoption, municipalities and construction drive sustainability in public services and infrastructure, and niche sectors expand the scope of hydrogen mobility into high-value, specialized use cases. This breadth of adoption reinforces hydrogen trucks as a critical enabler of the global shift toward cleaner and more efficient transport solutions.

Global Hydrogen Truck Market, By Application (USD million)

Global Hydrogen Truck Market by Region Insights:

Asia-Pacific segment accounted for market share of share 37.34% in 2024 in the global hydrogen truck market.

The Asia-Pacific region holds the largest share of the global hydrogen truck market, accounting for 37.34% in 2024. Revenues from this region are projected to reach USD 8,247.18 million during the forecast period, expanding at a CAGR of 22.61%. Rapid industrialization, growing logistics demand, and strong government support for green transportation are driving the adoption of hydrogen trucks in countries such as China, Japan, and South Korea. Investments in hydrogen infrastructure, including refueling stations and green hydrogen production facilities, are enabling fleet operators to deploy hydrogen trucks at scale. For instance, South Korea’s ambitious hydrogen roadmap and China’s pilot programs for heavy-duty hydrogen trucks are setting benchmarks for the region, demonstrating the viability of hydrogen mobility in densely populated and industrially active areas.

Europe is emerging as another key market, fuelled by stringent emissions regulations, decarbonization goals, and government incentives for clean mobility. Countries such as Germany, France, and the Netherlands are actively integrating hydrogen trucks into logistics networks, public transport, and long-haul freight operations. Hydrogen corridors across major highways and industrial zones are accelerating commercial adoption, with companies like Daimler Truck and Volvo piloting fuel cell trucks in collaboration with logistics partners. North America, particularly the U.S. and Canada, is also witnessing growth as federal and state policies support zero-emission freight and infrastructure development, while pilot deployments in California and along cross-country freight routes highlight the region’s potential.

Meanwhile, Latin America (LATAM) and the Middle East & Africa (MEA) segments are gradually entering the hydrogen truck ecosystem, representing emerging markets with significant long-term growth opportunities. LATAM countries are exploring hydrogen trucks to modernize logistics, reduce emissions in urban centres, and support sustainable mining and industrial operations. Similarly, MEA nations, led by the UAE and Saudi Arabia, are investing in hydrogen production and testing fuel cell vehicles for logistics and industrial applications. Together, these regional sub-segments illustrate a diverse adoption landscape, with Asia-Pacific leading the market through industrial and policy support, Europe and North America driving regulatory-led deployment, and LATAM and MEA poised for future growth as infrastructure and investments mature.

Global Hydrogen Truck Market, By Region (USD million)

Major Companies and Competitive Landscape

The global hydrogen truck market is expanding rapidly, driven by increasing demand for zero-emission, sustainable transportation solutions across logistics, municipal services, construction, and industrial sectors. Companies are focusing on strategic partnerships, joint ventures, and technological collaborations to advance fuel cell technology, optimize truck performance, and develop high-efficiency, long-range hydrogen vehicles. Efforts are also directed toward expanding hydrogen refuelling infrastructure, improving fuel cell durability and energy efficiency, and exploring emerging applications in long-haul freight, urban delivery, and specialized industrial transport. Key companies active in the global hydrogen truck market include:

- Hyundai Motor Company

- Nikola Corporation

- Daimler Truck AG

- Volvo Group

- TRATON GROUP

- Scania

- PACCAR Holding

- Dongfeng Motor Corporation

- Foton International

- Yutong International Holding Co., Ltd.

- IVECO

- Cummins Inc.

- Ballard Power Systems

- Toyota Motor Corporation

- Hino Motors, Ltd.

- Tevva

- Hyzon Motors

- Landi Renzo S.p.A.

- First Mode Holdings, Inc.

- Nel ASA

- Solaris Bus & Coach sp. z o.o.

- US Hybrid

- Great Wall Motor Company Ltd.

- Grove Hydrogen Automotive

- Esoro AG

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 5,302.08 Million |

| CAGR (2024–2032) | 22.57% |

| Revenue forecast to 2033 | USD 22,036.16 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million, Volume Kiloton and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | Global Hydrogen Truck Market, By Vehicle, By Motor Power, By Range, By Hydrogen Tank Size, By Type of Tank, By Fuel Cell Technology, By Application and By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, Rest of MEA |

| Key companies profiled | Hyundai Motor Company, Nikola Corporation, Daimler Truck AG, Volvo Group, TRATON Group, Scania, PACCAR Holding, Dongfeng Motor Corporation, Foton International, Yutong International, IVECO, Cummins Inc., Ballard Power Systems, Toyota Motor Corporation, Hino Motors, Tevva, Hyzon Motors, Landi Renzo, First Mode Holdings, Nel ASA, Solaris Bus & Coach, US Hybrid, Great Wall Motor Company, Grove Hydrogen Automotive, and Esoro AG. |

| Customization scope | 10 hours of free customization and expert consultation |

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of Hydrogen Truck Market

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1.Primary

2.1.2.Secondary

2.1.3.Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1.Market value

2.3.2.Market volume

2.3.3.Exchange rate

2.3.4.Price

2.3.5.Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2025–2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10. Formulation & manufacturing

4.11. Distribution & retail

4.12. Import-export analysis

4.13. Brand comparative analysis

4.14. Technological advancements

4.15. Porter’s five force

4.15.1. Threat of new entrants

4.15.1.1. Capital requirment

4.15.1.2. Product knowledge

4.15.1.3. Technical knowledge

4.15.1.4. Customer relation

4.15.1.5. Access to appliation and technology

4.15.2. Threat of substitutes

4.15.2.1. Cost

4.15.2.2. Performance

4.15.2.3. Availability

4.15.2.4. Technical knowledge

4.15.2.5. Durability

4.15.3. Bargainning power of buyers

4.15.3.1. Numbers of buyers relative to suppliers

4.15.3.2. Product differentiation

4.15.3.3. Threat of forward integration

4.15.3.4. Buyers volume

4.15.4. Bargainning power of suppliers

4.15.4.1. Suppliers concentration

4.15.4.2. Buyers switching cost to other suppliers

4.15.4.3. Threat of backward integration

4.15.5. Bargainning power of suppliers

4.15.5.1. Industry concentration

4.15.5.2. Industry growth rate

4.15.5.3. Product differentiation

4.16. Patent analysis

4.17. Regulation coverage

4.18. Pricing analysis

4.19. Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1.Rising Focus on Zero-Emission Transportation

5.1.2.Advancements in Hydrogen Fuel Cell Technology

5.1.3.Supportive Government Policies & Incentives

5.2. Restraints

5.2.1.High Vehicle & Infrastructure Costs

5.2.2.Limited Hydrogen Refueling Network

5.3. Opportunities

5.3.1.Growing Demand for Long-Haul & Heavy-Duty Applications

5.3.2.Expansion of Green Hydrogen Production

5.3.3.Strategic Collaborations & Investments

5.4. Challenges

5.4.1.Scaling Production & Commercial Viability

5.4.2.Safety & Regulatory Concerns

Chapter 6. Global Hydrogen Truck Market By Vehicle Insights & Trends, Revenue (USD Million)

6.1. Vehicle Dynamics & Market Share, 2019–2032

6.1.1. Heavy-duty trucks

6.1.2. Medium-duty trucks

6.1.3. Small-duty trucks

Chapter 7. Global Hydrogen Truck Market By Motor Power Insights & Trends, Revenue (USD Million)

7.1. Motor Power Dynamics & Market Share, 2019–2032

7.1.1. Up to 200 KW

7.1.2. 200-400 KW

7.1.3. Above 400 KW

Chapter 8. Global Hydrogen Truck Market By Range Insights & Trends, Revenue (USD Million)

8.1. Range Dynamics & Market Share, 2019–2032

8.1.1. Up to 300 Miles

8.1.2. 300-500 Miles

8.1.3. Above 500 Miles

Chapter 9. Global Hydrogen Truck Market By Hydrogen Tank Size Insights & Trends, Revenue (USD Million)

9.1. Hydrogen Tank Size Dynamics & Market Share, 2019–2032

9.1.1. Below 30 KG

9.1.2. 30-60 KG

9.1.3. Above 60 KG

Chapter 10. Global Hydrogen Truck Market By Type of Tank Insights & Trends, Revenue (USD Million)

10.1. Type of Tank Dynamics & Market Share, 2019–2032

10.1.1.Type III

10.1.2.Type IV

Chapter 11. Global Hydrogen Truck Market By Fuel Cell Technology Insights & Trends, Revenue (USD Million)

11.1. Fuel Cell Technology Dynamics & Market Share, 2019–2032

11.1.1.PEMFC(Proton Exchange Membrane Fuel Cell)

11.1.2.SOFC(Solid Oxide Fuel Cell)

Chapter 12. Global Hydrogen Truck Market By Application Insights & Trends, Revenue (USD Million)

12.1. Application Dynamics & Market Share, 2019–2032

12.1.1.Logistics and Transport

12.1.2.Municipal

12.1.3.Construction

12.1.4.Others

Chapter 13. Global Hydrogen Truck Market Regional Outlook

13.1. Hydrogen Truck Share By Region, 2019–2032

13.2. North America

13.2.1. Market By Vehicle Estimates and Forecast, USD Million, 2019-2032

13.2.1.1. Heavy-duty trucks

13.2.1.2. Medium-duty trucks

13.2.1.3. Small-duty trucks

13.2.2. Market By Motor Power, Market Estimates and Forecast, USD Million, 2019-2032

13.2.2.1. Up to 200 KW

13.2.2.2. 200-400 KW

13.2.2.3. Above 400 KW

13.2.3. Market By Range, Market Estimates and Forecast, USD Million, 2019-2032

13.2.3.1. Up to 300 Miles

13.2.3.2. 300-500 Miles

13.2.3.3. Above 500 Miles

13.2.4. Market By Hydrogen Tank Size, Market Estimates and Forecast, USD Million, 2019-2032

13.2.4.1. Below 30 KG

13.2.4.2. 30-60 KG

13.2.4.3. Above 60 KG

13.2.5. Market By Type of Tank, Market Estimates and Forecast, USD Million, 2019-2032

13.2.5.1. Type III

13.2.5.2. Type IV

13.2.6. Market By Fuel Cell Technology, Market Estimates and Forecast, USD Million, 2019-2032

13.2.6.1. PEMFC(Proton Exchange Membrane Fuel Cell)

13.2.6.2. SOFC(Solid Oxide Fuel Cell)

13.2.7. Market By Application, Market Estimates and Forecast, USD Million, 2019-2032

13.2.7.1. Logistics and Transport

13.2.7.2. Municipal

13.2.7.3. Construction

13.2.7.4. Others

13.2.8. Market By Country, Market Estimates and Forecast, USD Million, 2019-2032

13.2.8.1. US

13.2.8.2. Canada

13.2.8.3. Mexico

13.3. Europe

13.3.1. Market By Vehicle Estimates and Forecast, USD Million, 2019-2032

13.3.1.1. Heavy-duty trucks

13.3.1.2. Medium-duty trucks

13.3.1.3. Small-duty trucks

13.3.2. Market By Motor Power, Market Estimates and Forecast, USD Million, 2019-2032

13.3.2.1. Up to 200 KW

13.3.2.2. 200-400 KW

13.3.2.3. Above 400 KW

13.3.3. Market By Range, Market Estimates and Forecast, USD Million, 2019-2032

13.3.3.1. Up to 300 Miles

13.3.3.2. 300-500 Miles

13.3.3.3. Above 500 Miles

13.3.4. Market By Hydrogen Tank Size, Market Estimates and Forecast, USD Million, 2019-2032

13.3.4.1. Below 30 KG

13.3.4.2. 30-60 KG

13.3.4.3. Above 60 KG

13.3.5. Market By Type of Tank, Market Estimates and Forecast, USD Million, 2019-2032

13.3.5.1. Type III

13.3.5.2. Type IV

13.3.6. Market By Fuel Cell Technology, Market Estimates and Forecast, USD Million, 2019-2032

13.3.6.1. PEMFC(Proton Exchange Membrane Fuel Cell)

13.3.6.2. SOFC(Solid Oxide Fuel Cell)

13.3.7. Market By Application, Market Estimates and Forecast, USD Million, 2019-2032

13.3.7.1. Logistics and Transport

13.3.7.2. Municipal

13.3.7.3. Construction

13.3.7.4. Others

13.3.8. Market By Country, Market Estimates and Forecast, USD Million, 2019-2032

13.3.8.1. Germany

13.3.8.2. France

13.3.8.3. U.K

13.3.8.4. Italy

13.3.8.5. Spain

13.3.8.6. Benelux

13.3.8.7. Russia

13.3.8.8. Finland

13.3.8.9. Sweden

13.3.8.10. Rest Of Europe

13.4. Asia-Pacific

13.4.1. Market By Vehicle Estimates and Forecast, USD Million, 2019-2032

13.4.1.1. Heavy-duty trucks

13.4.1.2. Medium-duty trucks

13.4.1.3. Small-duty trucks

13.4.2. Market By Motor Power, Market Estimates and Forecast, USD Million, 2019-2032

13.4.2.1. Up to 200 KW

13.4.2.2. 200-400 KW

13.4.2.3. Above 400 KW

13.4.3. Market By Range, Market Estimates and Forecast, USD Million, 2019-2032

13.4.3.1. Up to 300 Miles

13.4.3.2. 300-500 Miles

13.4.3.3. Above 500 Miles

13.4.4. Market By Hydrogen Tank Size, Market Estimates and Forecast, USD Million, 2019-2032

13.4.4.1. Below 30 KG

13.4.4.2. 30-60 KG

13.4.4.3. Above 60 KG

13.4.5. Market By Type of Tank, Market Estimates and Forecast, USD Million, 2019-2032

13.4.5.1. Type III

13.4.5.2. Type IV

13.4.6. Market By Fuel Cell Technology, Market Estimates and Forecast, USD Million, 2019-2032

13.4.6.1. PEMFC(Proton Exchange Membrane Fuel Cell)

13.4.6.2. SOFC(Solid Oxide Fuel Cell)

13.4.7. Market By Application, Market Estimates and Forecast, USD Million, 2019-2032

13.4.7.1. Logistics and Transport

13.4.7.2. Municipal

13.4.7.3. Construction

13.4.7.4. Others

13.4.8. Market By Country, Market Estimates and Forecast, USD Million, 2019-2032

13.4.8.1.1. China

13.4.8.1.2. India

13.4.8.1.3. Japan

13.4.8.1.4. South Korea

13.4.8.1.5. Indonesia

13.4.8.1.6. Thailand

13.4.8.1.7. Vietnam

13.4.8.1.8. Australia

13.4.8.1.9. New Zeland

13.4.8.1.10. Rest of APAC

13.5. Latin America

13.5.1. Market By Vehicle Estimates and Forecast, USD Million, 2019-2032

13.5.1.1. Heavy-duty trucks

13.5.1.2. Medium-duty trucks

13.5.1.3. Small-duty trucks

13.5.2. Market By Motor Power, Market Estimates and Forecast, USD Million, 2019-2032

13.5.2.1. Up to 200 KW

13.5.2.2. 200-400 KW

13.5.2.3. Above 400 KW

13.5.3. Market By Range, Market Estimates and Forecast, USD Million, 2019-2032

13.5.3.1. Up to 300 Miles

13.5.3.2. 300-500 Miles

13.5.3.3. Above 500 Miles

13.5.4. Market By Hydrogen Tank Size, Market Estimates and Forecast, USD Million, 2019-2032

13.5.4.1. Below 30 KG

13.5.4.2. 30-60 KG

13.5.4.3. Above 60 KG

13.5.5. Market By Type of Tank, Market Estimates and Forecast, USD Million, 2019-2032

13.5.5.1. Type III

13.5.5.2. Type IV

13.5.6. Market By Fuel Cell Technology, Market Estimates and Forecast, USD Million, 2019-2032

13.5.6.1. PEMFC(Proton Exchange Membrane Fuel Cell)

13.5.6.2. SOFC(Solid Oxide Fuel Cell)

13.5.7. Market By Application, Market Estimates and Forecast, USD Million, 2019-2032

13.5.7.1. Logistics and Transport

13.5.7.2. Municipal

13.5.7.3. Construction

13.5.7.4. Others

13.5.8. Market By Country, Market Estimates and Forecast, USD Million, 2019-2032

13.5.8.1. Brazil

13.5.8.2. Rest of LATAM

13.6. Middle East & Africa

13.6.1. Market By Vehicle Estimates and Forecast, USD Million, 2019-2032

13.6.1.1. Heavy-duty trucks

13.6.1.2. Medium-duty trucks

13.6.1.3. Small-duty trucks

13.6.2. Market By Motor Power, Market Estimates and Forecast, USD Million, 2019-2032

13.6.2.1. Up to 200 KW

13.6.2.2. 200-400 KW

13.6.2.3. Above 400 KW

13.6.3. Market By Range, Market Estimates and Forecast, USD Million, 2019-2032

13.6.3.1. Up to 300 Miles

13.6.3.2. 300-500 Miles

13.6.3.3. Above 500 Miles

13.6.4. Market By Hydrogen Tank Size, Market Estimates and Forecast, USD Million, 2019-2032

13.6.4.1. Below 30 KG

13.6.4.2. 30-60 KG

13.6.4.3. Above 60 KG

13.6.5. Market By Type of Tank, Market Estimates and Forecast, USD Million, 2019-2032

13.6.5.1. Type III

13.6.5.2. Type IV

13.6.6. Market By Fuel Cell Technology, Market Estimates and Forecast, USD Million, 2019-2032

13.6.6.1. PEMFC(Proton Exchange Membrane Fuel Cell)

13.6.6.2. SOFC(Solid Oxide Fuel Cell)

13.6.7. Market By Application, Market Estimates and Forecast, USD Million, 2019-2032

13.6.7.1. Logistics and Transport

13.6.7.2. Municipal

13.6.7.3. Construction

13.6.7.4. Others

13.6.8. Market By Country, Market Estimates and Forecast, USD Million, 2019-2032

13.6.8.1. Saudi Arabia

13.6.8.2. Rest of MEA

Chapter 14. Competitive Landscape

14.1. Market Revenue Share By Manufacturers

14.2. Mergers & Acquisitions

14.3. Competitor’s Positioning

14.4. Strategy Benchmarking

14.5. Vendor Landscape

14.5.1. Distributors

14.5.1.1. North America

14.5.1.2. Europe

14.5.1.3. Asia Pacific

14.5.1.4. Middle East & Africa

14.5.1.5. Latin America

Chapter 15. Company Profiles

15.1. Hyundai Motor Company

15.1.1. Company Overview

15.1.2. Product & Service Offerings

15.1.3. Strategic Initiatives

15.1.4. Financials

15.1.5. Conclusion

15.2. Nikola Corporation

15.2.1. Company Overview

15.2.2. Product & Service Offerings

15.2.3. Strategic Initiatives

15.2.4. Financials

15.2.5. Conclusion

15.3. Daimler Truck AG

15.3.1. Company Overview

15.3.2. Product & Service Offerings

15.3.3. Strategic Initiatives

15.3.4. Financials

15.3.5. Conclusion

15.4. Volvo Group

15.4.1. Company Overview

15.4.2. Product & Service Offerings

15.4.3. Strategic Initiatives

15.4.4. Financials

15.5. TRATON GROUP

15.5.1. Company Overview

15.5.2. Product & Service Offerings

15.5.3. Strategic Initiatives

15.5.4. Financials

15.5.5. Conclusion

15.6. Scania

15.6.1. Company Overview

15.6.2. Product & Service Offerings

15.6.3. Strategic Initiatives

15.6.4. Financials

15.6.5. Conclusion

15.7. PACCAR Holding

15.7.1. Company Overview

15.7.2. Product & Service Offerings

15.7.3. Strategic Initiatives

15.7.4. Financials

15.7.5. Conclusion

15.8. Dongfeng Motor Corporation

15.8.1. Company Overview

15.8.2. Product & Service Offerings

15.8.3. Strategic Initiatives

15.8.4. Financials

15.8.5. Conclusion

15.9. Foton International

15.9.1. Company Overview

15.9.2. Product & Service Offerings

15.9.3. Strategic Initiatives

15.9.4. Financials

15.9.5. Conclusion

15.10. Yutong International Holding Co., Ltd.

15.10.1. Company Overview

15.10.2. Product & Service Offerings

15.10.3. Strategic Initiatives

15.10.4. Financials

15.10.5. Conclusion

15.11. IVECO

15.11.1. Company Overview

15.11.2. Product & Service Offerings

15.11.3. Strategic Initiatives

15.11.4. Financials

15.11.5. Conclusion

15.12. Cummins Inc.

15.12.1. Company Overview

15.12.2. Product & Service Offerings

15.12.3. Strategic Initiatives

15.12.4. Financials

15.12.5. Conclusion

15.13. Ballard Power Systems

15.13.1. Company Overview

15.13.2. Product & Service Offerings

15.13.3. Strategic Initiatives

15.13.4. Financials

15.13.5. Conclusion

15.14. Toyota Motor Corporation

15.14.1. Company Overview

15.14.2. Product & Service Offerings

15.14.3. Strategic Initiatives

15.14.4. Financials

15.14.5. Conclusion

15.15. Hino Motors, Ltd.

15.15.1. Company Overview

15.15.2. Product & Service Offerings

15.15.3. Strategic Initiatives

15.15.4. Financials

15.15.5. Conclusion

15.16. Tevva

15.16.1. Company Overview

15.16.2. Product & Service Offerings

15.16.3. Strategic Initiatives

15.16.4. Financials

15.16.5. Conclusion

15.17. Hyzon Motors

15.17.1. Company Overview

15.17.2. Product & Service Offerings

15.17.3. Strategic Initiatives

15.17.4. Financials

15.17.5. Conclusion

15.18. Landi Renzo S.p.A.

15.18.1. Company Overview

15.18.2. Product & Service Offerings

15.18.3. Strategic Initiatives

15.18.4. Financials

15.18.5. Conclusion

15.19. First Mode Holdings, Inc.

15.19.1. Company Overview

15.19.2. Product & Service Offerings

15.19.3. Strategic Initiatives

15.19.4. Financials

15.19.5. Conclusion

15.20. Nel ASA

15.20.1. Company Overview

15.20.2. Product & Service Offerings

15.20.3. Strategic Initiatives

15.20.4. Financials

15.20.5. Conclusion

15.21. Solaris Bus & Coach sp. z o.o.

15.21.1. Company Overview

15.21.2. Product & Service Offerings

15.21.3. Strategic Initiatives

15.21.4. Financials

15.21.5. Conclusion

15.22. Ballard

15.22.1. Company Overview

15.22.2. Product & Service Offerings

15.22.3. Strategic Initiatives

15.22.4. Financials

15.22.5. Conclusion

15.23. Great Wall Motor Company Ltd.

15.23.1. Company Overview

15.23.2. Product & Service Offerings

15.23.3. Strategic Initiatives

15.23.4. Financials

15.23.5. Conclusion

15.24. Grove Hydrogen Automotive

15.24.1. Company Overview

15.24.2. Product & Service Offerings

15.24.3. Strategic Initiatives

15.24.4. Financials

15.24.5. Conclusion

15.25. Esoro AG

15.25.1. Company Overview

15.25.2. Product & Service Offerings

15.25.3. Strategic Initiatives

15.25.4. Financials

15.25.5. Conclusion

Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP. has segmented global hydrogen truck market on the basis of By Vehicle, By Motor Power, By Range, By Hydrogen Tank Size, By Type of Tank, By Fuel Cell Technology, By Application and by region for 2019 to 2032.

- Global Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Global Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Global Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Global Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Global Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Global Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Global Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- North America

- North America Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- North America Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- North America Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- North America Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- North America Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- North America Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- North America Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- U.S

- U.S Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- U.S Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- U.S Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- U.S Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- U.S Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- U.S Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- U.S Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Canada

- Canada Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Canada Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Canada Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Canada Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Canada Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Canada Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Canada Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Mexico

- Mexico Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Mexico Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Mexico Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Mexico Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Mexico Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Mexico Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Mexico Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Europe

- Europe Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Europe Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Europe Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Europe Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Europe Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Europe Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Europe Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Germany

- Germany Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Germany Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Germany Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Germany Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Germany Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Germany Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Germany Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- France

- France Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- France Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- France Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- France Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- France Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- France Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- France Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- U.K

- U.K Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- U.K Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- U.K Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- U.K Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- U.K Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- U.K Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- U.K Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Italy

- Italy Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Italy Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Italy Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Italy Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Italy Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Italy Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Italy Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Spain

- Spain Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Spain Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Spain Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Spain Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Spain Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Spain Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Spain Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Benelux

- Benelux Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Benelux Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Benelux Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Benelux Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Benelux Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Benelux Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Benelux Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Russia

- Russia Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Russia Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Russia Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Russia Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Russia Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Russia Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Russia Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Finland

- Finland Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Finland Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Finland Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Finland Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Finland Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Finland Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Finland Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Sweden

- Sweden Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Sweden Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Sweden Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Sweden Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Sweden Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Sweden Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Sweden Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Rest of Europe

- Rest of Europe Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Rest of Europe Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Rest of Europe Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Rest of Europe Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Rest of Europe Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Rest of Europe Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Rest of Europe Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Asia-Pacific

- Asia-Pacific Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Asia-Pacific Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Asia-Pacific Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Asia-Pacific Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Asia-Pacific Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Asia-Pacific Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Asia-Pacific Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- China

- China Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- China Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- China Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- China Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- China Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- China Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- China Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- India

- India Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- India Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- India Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- India Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- India Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- India Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- India Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Japan

- Japan Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Japan Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Japan Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Japan Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Japan Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Japan Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Japan Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- South Korea

- South Korea Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- South Korea Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- South Korea Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- South Korea Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- South Korea Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- South Korea Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- South Korea Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Indonesia

- Indonesia Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Indonesia Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Indonesia Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Indonesia Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Indonesia Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Indonesia Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Indonesia Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Vietnam

- Vietnam Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Vietnam Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Vietnam Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Vietnam Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Vietnam Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Vietnam Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Vietnam Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Australia

- Australia Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Australia Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Australia Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Australia Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Australia Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Australia Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Australia Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- New Zeeland

- New Zeeland Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- New Zeeland Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- New Zeeland Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- New Zeeland Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- New Zeeland Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- New Zeeland Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- New Zeeland Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Rest of APAC

- Rest of APAC Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Rest of APAC Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Rest of APAC Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Rest of APAC Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Rest of APAC Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Rest of APAC Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Rest of APAC Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Latin America

- Latin America Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Latin America Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Latin America Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Latin America Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Latin America Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Latin America Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Latin America Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Brazil

- Brazil Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Brazil Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Brazil Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Brazil Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Brazil Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Brazil Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Brazil Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Rest of LATAM

- Rest of LATAM Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Rest of LATAM Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Rest of LATAM Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Rest of LATAM Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Rest of LATAM Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Rest of LATAM Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Rest of LATAM Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Middle East & Africa

- Middle East & Africa Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Middle East & Africa Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Middle East & Africa Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Middle East & Africa Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Middle East & Africa Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Middle East & Africa Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Middle East & Africa Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Saudi Arabia

- Saudi Arabia Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Saudi Arabia Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Saudi Arabia Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Saudi Arabia Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Saudi Arabia Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Saudi Arabia Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Saudi Arabia Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- UAE

- UAE Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- UAE Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- UAE Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- UAE Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- UAE Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- UAE Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- UAE Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- South Africa

- South Africa Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- South Africa Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- South Africa Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- South Africa Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- South Africa Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- South Africa Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- South Africa Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Rest of MEA

- Rest of MEA Vehicle Outlook (Revenue, USD Million; 2019-2032)

- Heavy-duty trucks

- Medium-duty trucks

- Small-duty trucks

- Rest of MEA Motor Power Outlook (Revenue, USD Million; 2019-2032)

- Up to 200 KW

- 200-400 KW

- Above 400 KW

- Rest of MEA Range Outlook (Revenue, USD Million; 2019-2032)

- Up to 300 Miles

- 300-500 Miles

- Above 500 Miles

- Rest of MEA Hydrogen Tank Size Outlook (Revenue, USD Million; 2019-2032)

- Below 30 KG

- 30-60 KG

- Above 60 KG

- Rest of MEA Type of Tank Outlook (Revenue, USD Million; 2019-2032)

- Type III

- Type IV

- Rest of MEA Fuel Cell Technology Outlook (Revenue, USD Million; 2019-2032)

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Rest of MEA Application Outlook (Revenue, USD Million; 2019-2032)

- Logistics and Transport

- Municipal

- Construction

- Others

- Some Key Questions the Report Will Answer

- What is the expected revenue Compound Annual Growth Rate (CAGR) of the global hydrogen truck market over the forecast period (2025–2032)?

- The global hydrogen truck market revenue is expected to register a Compound Annual Growth Rate (CAGR) of 22.57% during the forecast period.

- Which factors are expected to drive the global hydrogen truck market growth?

- The global hydrogen truck market is driven by strict emission regulations, government incentives, and advancements in fuel cell and hydrogen storage technologies. Companies are adopting hydrogen trucks to meet sustainability goals while benefiting from long ranges, fast refueling, and high payload capacity. Growing demand for eco-friendly logistics solutions further supports market growth.

- What are main Challenges facing the Global hydrogen truck Market?