Market Synopsis

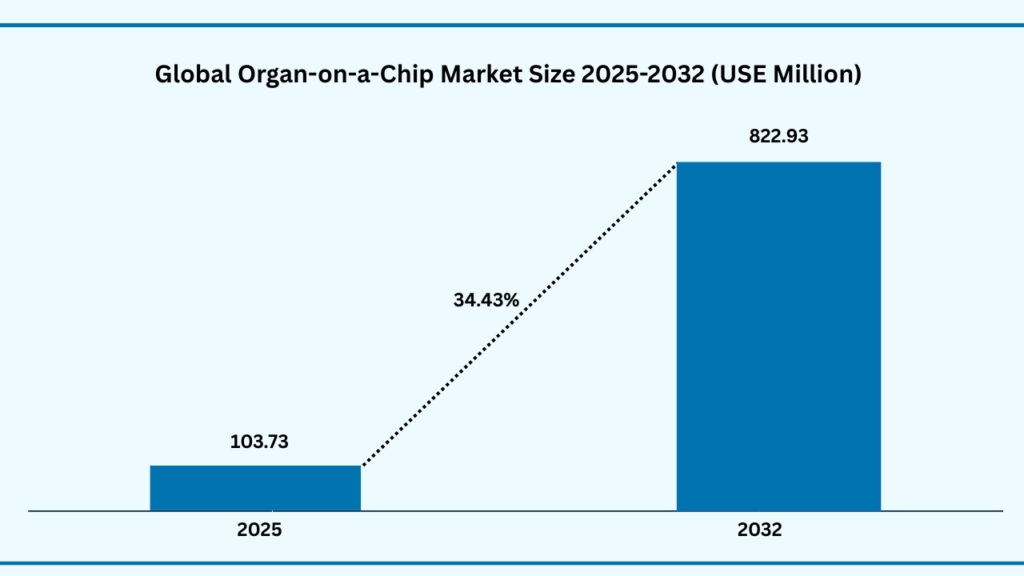

The global organ-on-a-chip market size was USD 77.16 million in 2024 and is expected to reach USD 822.93 million at a CAGR of 34.43% during the forecast period from 2025 to 2032. Market expansion is being fueled by rising demand for more accurate and cost-effective drug testing models, the growing need to reduce reliance on animal testing, and increasing adoption of micro physiological systems in pharmaceutical and biotechnology research. Further momentum is coming from advancements in microfluidics, tissue engineering, and stem cell technologies, along with greater regulatory support for alternatives to traditional preclinical models. The market is also witnessing strong investment flows and strategic partnerships aimed at accelerating product development and commercialization. With global R&D spending in life sciences continuing to rise, organ-on-a-chip technologies are gaining traction as a breakthrough solution for predicting human responses more effectively. As pharmaceutical companies seek faster, safer, and more reliable platforms for drug discovery, the adoption of organ-on-a-chip systems is expected to see significant long-term growth, particularly in regions with strong innovation ecosystems and growing emphasis on precision medicine.

Global Organ-on-a-Chip Market (USD million)

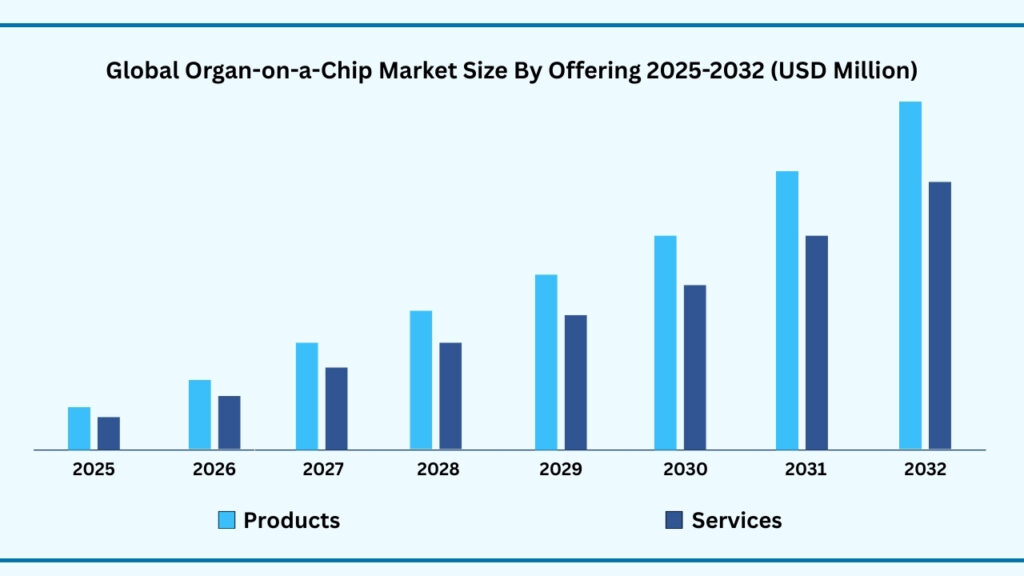

Global Organ-on-a-Chip Market by Offering Insights:

Products segment accounted for market share of share 56.27% in 2024 in the global organ-on-a-chip market.

The products segment accounted for the largest share of the global organ-on-a-chip market in 2024, representing 56.27% of total revenues. Products are projected to grow at a CAGR of 34.44% between 2025 and 2032, reaching USD 463.42 million by the end of the forecast period. This dominance is driven by the rising adoption of organ-mimicking chips, instruments, and consumables that enable researchers to replicate human biology with high precision. Single-organ chips, such as liver-, lung-, and heart-on-a-chip, are widely used for drug toxicity and disease modelling, while multi-organ and body-on-a-chip systems are gaining momentum for studying systemic responses and complex drug interactions. Instruments and integrated platforms provide researchers with scalable and automated workflows, and consumables, reagents, and ready-to-use kits ensure reliable and repeatable outcomes. Meanwhile, software and data tools are increasingly vital for interpreting results, offering advanced analytics and AI-driven insights that enhance the value of chip-based studies. Together, these innovations are making organ-on-a-chip products an indispensable part of modern drug discovery and biomedical research.

Leading players are investing heavily to expand their positions within this segment. Emulate Inc. has advanced its lung- and liver-on-a-chip systems and partnered with pharmaceutical companies in the U.S. to accelerate safety testing, while CN Bio has launched multi-organ models in Europe to study metabolism and systemic drug effects. TissUse GmbH is pioneering multi-organ platforms that link up to four tissues on a single chip, meeting demand for whole-body simulations. Mimetas has scaled its OrganoPlate platform, enabling high-throughput drug screening and improving compatibility with pharmaceutical pipelines, and Nortis has focused on developing kidney-on-a-chip solutions to model renal diseases and drug-induced nephrotoxicity. On the consumables and reagents front, providers are expanding reagent kits and panels to simplify workflows for academic labs and contract research organizations. Companies are also integrating software and analytics into their offerings, with collaborations aimed at developing AI-driven platforms to interpret chip-generated data more effectively.

Alongside products, the services sub-segment is also emerging as an important component of the offering landscape. Custom services, which include tailored chip design and contract research programs, are gaining popularity among pharmaceutical companies that seek organ-specific solutions without heavy investment in in-house infrastructure. Standardized services, such as prevalidated toxicity assays and disease models, are being offered to academic institutions and biotech firms that need reliable and scalable research tools. Players like TissUse and CN Bio have already built service-oriented models that complement their hardware offerings, helping clients conduct specialized studies and validate results. These service initiatives not only expand accessibility to organ-on-a-chip technologies but also accelerate their adoption in global drug development pipelines.

Global Organ-on-a-Chip Market, By Offering (USD million)

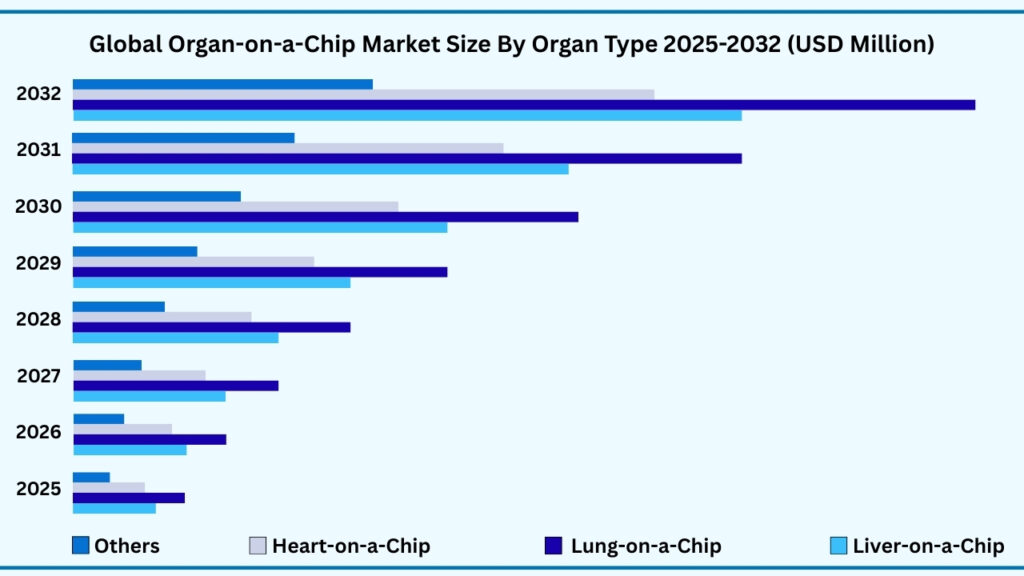

Global Organ-on-a-Chip Market by Organ Type Insights:

Lung-on-a-Chip segment accounted for market share of share 35.01% in 2024 in the global organ-on-a-chip market.

The lung-on-a-chip segment leads the global organ-on-a-chip market, capturing 35.01% of the share in 2024, with revenues projected to reach USD 289.03 million by 2032 at a CAGR of 34.48% during the forecast period from 2025 to 2032. Its dominance is driven by the rising demand for accurate models that replicate the lung’s microenvironment to study respiratory diseases, drug inhalation, and toxicity caused by airborne pollutants. Pharmaceutical companies are increasingly using lung-on-a-chip devices for preclinical testing of inhalable therapies and vaccines, while academic researchers rely on them to study chronic conditions such as asthma, COPD, and pulmonary fibrosis. The segment’s strength also comes from global attention to respiratory health following the COVID-19 pandemic, which accelerated investment in lung-specific organ chips to model viral infections and evaluate antiviral drugs more effectively.

Alongside lungs, liver-on-a-chip platforms are emerging as a critical segment, owing to the liver’s central role in metabolism and drug toxicity. These chips are widely used to evaluate hepatotoxicity in new drug candidates, offering predictive insights that are difficult to achieve with animal models. Heart-on-a-chip systems are also gaining momentum, particularly for studying cardiac arrhythmias, drug-induced cardiotoxicity, and personalized medicine approaches. These chips allow researchers to simulate human cardiac function in a laboratory setting, supporting the safe development of cardiovascular drugs.

The Others category, which includes brain-on-a-chip, kidney-on-a-chip, gut-on-a-chip, and multi-organ systems, represents the cutting edge of innovation. These platforms are being designed to replicate highly complex biological environments, offering opportunities to study neurological diseases, renal disorders, and systemic interactions across organs. Multi-organ chips, in particular, are attracting strong interest for their ability to simulate whole-body responses, providing a bridge between cell cultures and clinical trials. Together, these organ-type segments highlight how lung-on-a-chip maintains market leadership, while liver, heart, and other advanced models continue to broaden the scope of applications, driving the market’s rapid growth trajectory.

Global Organ-on-a-Chip Market, By Organ Type (USD million)

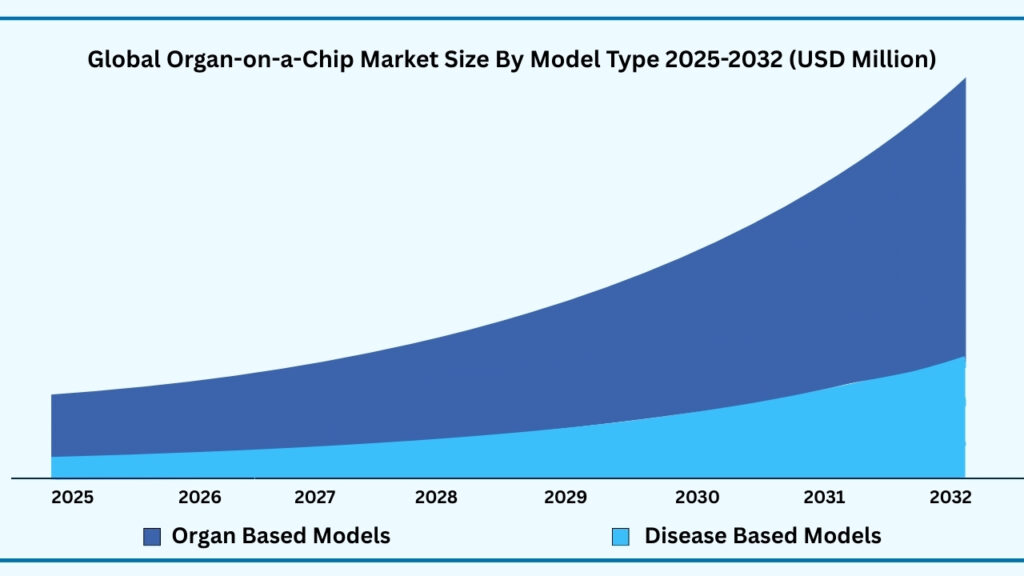

Global Organ-on-a-Chip Market by Model Type Insights:

Organ-Based Models segment accounted for market share of share 75.73% in 2024 in the global organ-on-a-chip market.

The organ-based models segment leads the global organ-on-a-chip market, accounting for 75.73% of the share in 2024. This segment is projected to grow at a CAGR of 34.46% during the forecast period from 2025 to 2032, reaching USD 624.17 million by the end of the period. Its strong position is supported by the extensive use of liver, lung, heart, and kidney chips in pharmaceutical research, drug toxicity studies, and preclinical testing. Organ-based models replicate human organ microenvironments with high fidelity, allowing researchers to evaluate safety and efficacy before advancing to costly clinical trials. Their scalability, ability to deliver reproducible results, and suitability for regulatory discussions make them the most widely adopted model type and the foundation of this market’s expansion.

In comparison, disease-based models are gaining prominence for their ability to simulate complex human pathologies such as cancer, neurodegenerative disorders, diabetes, and infectious diseases. These models provide a dynamic platform to study disease progression, drug resistance, and patient-specific responses in ways that conventional methods cannot match. Pharmaceutical companies are using them to develop targeted therapies and personalized medicine strategies, while academic researchers rely on them to explore the molecular basis of disease in real time. Though currently smaller in share compared to organ-based systems, disease-focused chips are expected to become increasingly important as precision medicine and rare disease research gather momentum.

Together, these segments highlight a balanced growth path where organ-based models act as the primary driver of adoption, while disease-based systems push innovation boundaries and open new opportunities for translational research. With growing demand for predictive, human-relevant models, this segmentation reflects how organ-on-a-chip technology is evolving to serve both standardized safety testing and cutting-edge therapeutic development.

Global Organ-on-a-Chip Market, By Model Type (USD million)

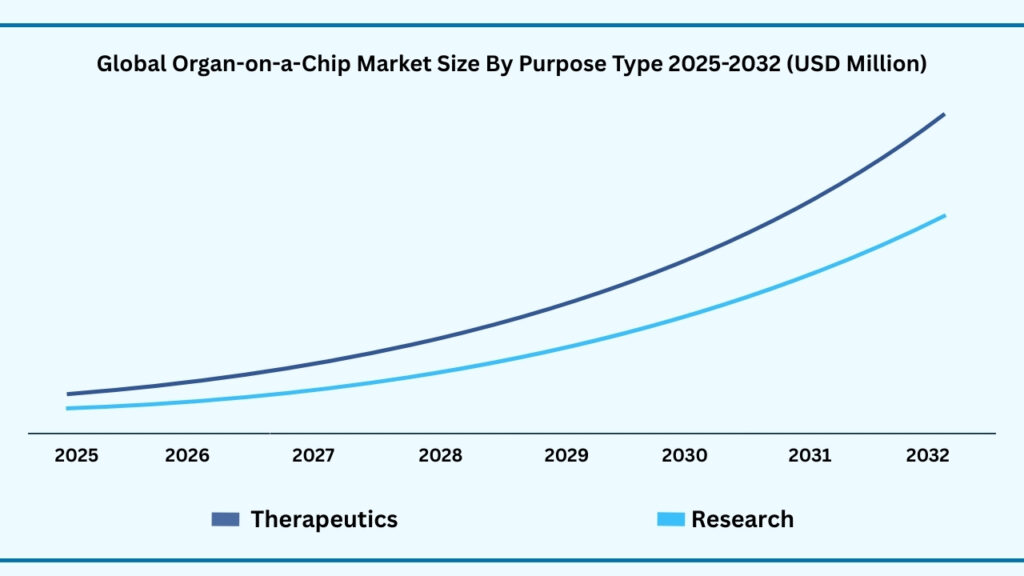

Global Organ-on-a-Chip Market by Purpose Type Insights:

Therapeutics segment accounted for market share of share 59.70% in 2024 in the global organ-on-a-chip market.

The global organ-on-a-chip market, based on purpose type, is segmented into Therapeutics and Research. Among these, Therapeutics leads with the largest share of 59.70% in 2024 and is projected to expand at a CAGR of 34.44% during the forecast period from 2025 to 2032, reaching USD 491.68 million by the end of the period. This dominance is driven by the increasing adoption of organ-on-a-chip platforms in drug discovery, toxicity testing, and preclinical validation, where the ability to mimic human organ physiology offers a more reliable alternative to animal models. Pharmaceutical companies leverage these models to streamline development pipelines, reduce costs, and improve success rates of clinical trials. The growing focus on personalized medicine further accelerates uptake, as organ chips can be tailored to patient-specific cells, enabling more predictive insights into therapeutic responses.

Meanwhile, the Research segment continues to expand as academic institutions, biotech startups, and government-funded initiatives utilize organ-on-a-chip systems to explore fundamental biology and disease mechanisms. From studying cancer metastasis to unraveling complex interactions in neurodegenerative disorders, research applications highlight the versatility of these models in bridging the gap between in vitro studies and clinical realities. Although smaller in current market share compared to therapeutics, this segment is critical in pushing the frontiers of innovation by generating new knowledge that fuels translational applications.

Collectively, these segments showcase a market that balances commercial application with scientific exploration. Therapeutics serves as the primary growth driver by directly addressing industry needs for safer, faster, and more cost-efficient drug development, while research-oriented adoption ensures continuous innovation and refinement of the technology. Together, they reflect how organ-on-a-chip systems are not only transforming the drug development landscape but also reshaping the way we understand and model human biology.

Global Organ-on-a-Chip Market, By Purpose Type (USD million)

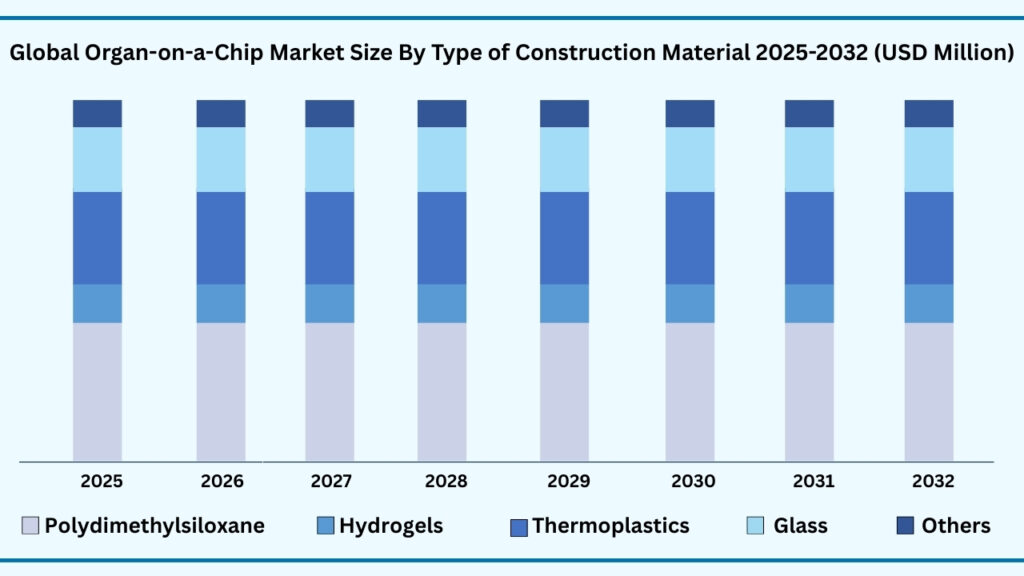

Global Organ-on-a-Chip Market by Type of Construction Material Insights:

Polydimethylsiloxane segment accounted for market share of share 42.03% in 2024 in the global organ-on-a-chip market.

Based on type of construction material, the global organ-on-a-chip market is segmented into Polydimethylsiloxane (PDMS), Glass, Hydrogels, Thermoplastics, and Others (such as Silicon). Among these, Polydimethylsiloxane (PDMS) dominates the segment with the largest share of 42.03% in 2024 and is projected to grow at a CAGR of 34.48% during the forecast period from 2025 to 2032, reaching USD 347.02 million by the end of the period. PDMS remains the material of choice due to its unique combination of biocompatibility, optical transparency, and flexibility, which makes it ideal for fabricating microfluidic channels and replicating the dynamic physiological environment of human organs. Its gas permeability is particularly valuable for simulating oxygen and nutrient exchange in lung- or liver-on-chip models, making it highly suitable for drug screening and disease modelling.

The dominance of PDMS is further reinforced by its wide adoption in academic research and prototype development, where cost-effectiveness and ease of molding are crucial. Continuous advancements in microfabrication techniques, such as soft lithography and 3D printing, have improved the scalability of PDMS-based chips, bridging the gap between laboratory models and commercial-ready platforms. While alternatives like glass offer superior chemical resistance and hydrogels provide better tissue-like environments for cellular studies, PDMS remains the backbone material due to its versatility across multiple applications. For example, companies like Emulate Inc. and Kirkstall leverage PDMS-based designs to create organ chips widely used in pharmaceutical testing and toxicology studies.

Collectively, this segment highlights how material choice directly impacts performance, scalability, and adoption of organ-on-a-chip systems. PDMS continues to be the primary growth driver, offering a balance of functionality and cost-effectiveness, while emerging materials like hydrogels and thermoplastics are paving the way for more specialized applications in advanced disease modelling and regenerative medicine. This mix of established reliability and ongoing innovation ensures that construction material trends will remain central to shaping the next phase of the organ-on-a-chip market.

Global Organ-on-a-Chip Market, By Type Of Construction Material (USD million)

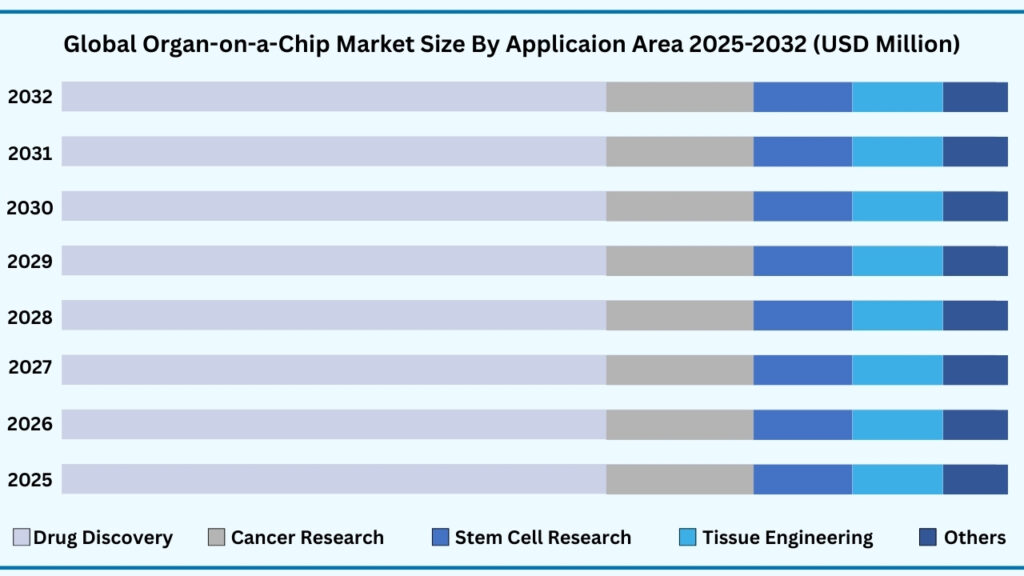

Global Organ-on-a-Chip Market by Application Area Insights:

Drug Discovery segment accounted for market share of share 57.42% in 2024 in the global organ-on-a-chip market.

Drug discovery represents the largest application area of the global organ-on-a-chip market, accounting for 57.42% of revenues in 2025 and projected to reach USD 474.08 million, growing at a CAGR of 34.48% during the forecast period. This leadership is fuelled by the pressing need for more predictive preclinical models that can bridge the gap between laboratory research and human clinical outcomes. Traditional methods, such as animal testing and 2D cell cultures, often fall short in replicating human physiology, leading to high drug attrition rates. Organ-on-a-chip platforms address this challenge by mimicking the structural and functional characteristics of human organs in a microfluidic environment, enabling researchers to test drug efficacy, absorption, and toxicity with greater accuracy and efficiency. For instance, liver- and kidney-on-chip models are increasingly being used to evaluate drug metabolism and nephrotoxicity, reducing the reliance on animal studies and accelerating decision-making in pharmaceutical pipelines.

The strong adoption of organ-on-a-chip systems in drug discovery is further reinforced by growing collaborations between chip developers and pharmaceutical companies, who see these models as essential tools for de-risking costly late-stage failures. Advances in multi-organ chips, which allow the testing of systemic interactions such as liver–heart or gut–liver crosstalk, are expanding their role in evaluating drug safety across complex biological systems. Beyond small molecules, these platforms are also proving valuable in biologics and advanced therapies, where immune-on-chip models are being applied to assess responses to immunotherapies and cell-based treatments. Such versatility makes them indispensable in modern R&D pipelines, providing not only more reliable safety data but also helping shorten timelines for bringing new drugs to market.

Recent momentum highlights the transformative impact of these systems. Regulatory agencies, including the U.S. FDA, have initiated partnerships and pilot programs to explore the integration of organ-on-chip data into drug evaluation frameworks, signalling growing recognition of their translational value. At the same time, biotech startups and academic labs are leveraging innovations in 3D cell culture and microfluidics to refine chip designs, creating more physiologically relevant and cost-effective solutions. Collectively, these developments underscore why drug discovery and toxicity testing remain the cornerstone application of the organ-on-a-chip market, anchoring its growth while paving the way for safer, faster, and more efficient drug development worldwide.

Global Organ-on-a-Chip Market, By Application Area (USD million)

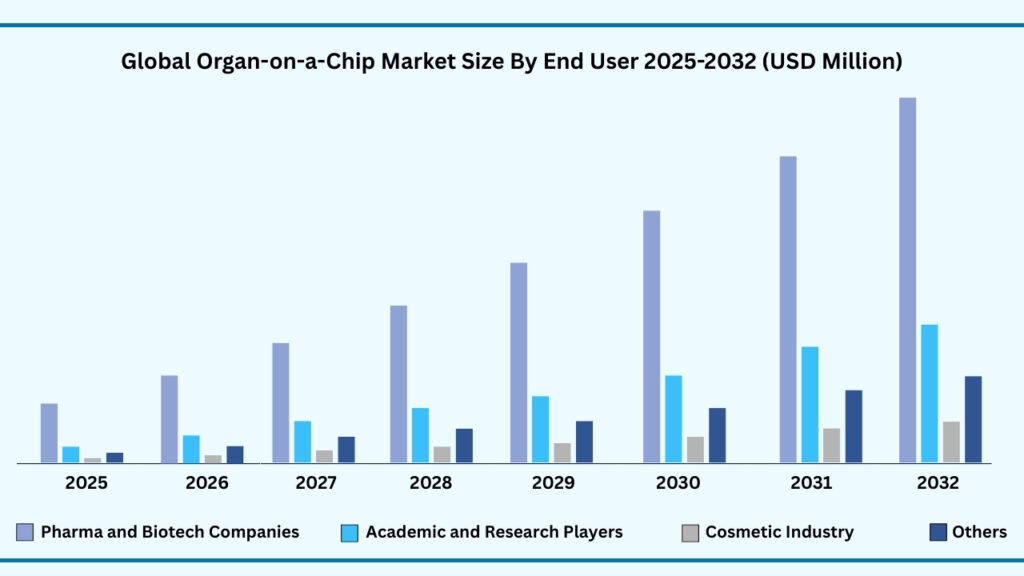

Global Organ-on-a-Chip Market by End User Insights:

Pharmaceutical and biotech companies segment accounted for market share of share 66.57% in 2024 in the global organ-on-a-chip market.

Pharmaceutical and biotechnology companies represent the largest end-user segment in the global organ-on-a-chip market, holding 66.57% of the share in 2025 and projected to grow at a CAGR of 34.52% during the forecast period, reaching USD 550.92 million by the end of the period. Their dominance stems from the critical role these companies play in developing and commercializing novel therapeutics, where organ-on-a-chip systems are increasingly used to enhance preclinical testing and drug discovery processes. By replicating human organ physiology in a controlled microenvironment, these platforms enable pharma and biotech firms to better predict drug responses, reduce failure rates in clinical trials, and accelerate timelines for bringing new therapies to market. For instance, liver- and heart-on-a-chip models are being widely adopted to evaluate toxicity and cardiotoxicity of drug candidates before advancing them to costly human trials.

The growth of this segment is further driven by rising investments in advanced drug development technologies and the shift toward precision medicine. Pharmaceutical companies are leveraging organ-on-a-chip models not only for small-molecule drugs but also for biologics and cell-based therapies, where traditional animal models often fall short. Biotech startups are also at the forefront of adopting these technologies to rapidly screen compounds, optimize dosing strategies, and de-risk R&D programs. Strategic collaborations between chip technology providers and large pharma players are expanding access to multi-organ and disease-specific chips, supporting more complex studies such as oncology, immunology, and rare disease research.

Moreover, regulatory interest is beginning to align with industry adoption. The U.S. FDA and European agencies have initiated pilot programs that consider data from organ-on-a-chip studies in preclinical safety assessments, signalling a potential paradigm shift in drug approval pathways. As the pressure to cut costs and improve R&D productivity intensifies, pharmaceutical and biotech companies are positioned as the leading force driving demand for organ-on-a-chip technologies. Their focus on innovation, efficiency, and translational relevance ensures this segment will remain the anchor of market growth in the years ahead.

Global Organ-on-a-Chip Market, By End User (USD million)

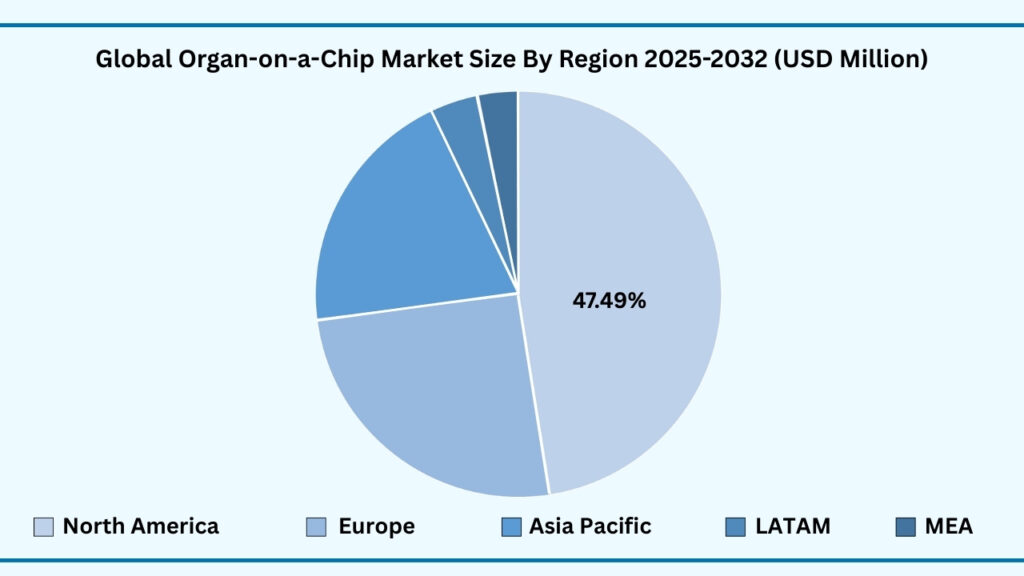

Global Organ-on-a-Chip Market by Region Insights:

North America segment accounted for market share of share 47.61% in 2024 in the global organ-on-a-chip market.

North America holds the largest share of the global organ-on-a-chip market, accounting for 47.61% in 2025, and is projected to expand at a CAGR of 34.50% during the forecast period, reaching USD 393.36 million by the end of the period. This leadership is underpinned by the region’s strong biotechnology and pharmaceutical ecosystem, with major industry players actively investing in advanced preclinical testing solutions. The presence of world-leading research institutions, cutting-edge laboratories, and a well-established healthcare innovation framework makes North America the hub for early adoption of organ-on-a-chip technologies. Applications such as drug toxicity testing, disease modelling, and personalized medicine are gaining momentum in the U.S. and Canada, where demand for more predictive, human-relevant models is steadily replacing reliance on traditional animal studies. For example, companies like Emulate Inc. and CN Bio have established strong research partnerships in the region to advance organ-chip applications for drug discovery and regulatory science.

The region also benefits from favourable government initiatives and regulatory engagement that encourage the adoption of alternative preclinical models. The U.S. FDA has launched pilot programs to evaluate the integration of organ-on-a-chip data into regulatory submissions, signalling a shift toward greater acceptance of these technologies in drug approval processes. At the same time, funding from the National Institutes of Health (NIH) and other agencies continues to accelerate innovation and commercialization of organ-chip platforms across therapeutic areas, from oncology to rare diseases.

Adding to this strength is North America’s vibrant network of biotech startups, academic spin-offs, and contract research organizations (CROs) that work closely with pharma companies to translate breakthrough research into real-world applications. The combination of industry leadership, academic excellence, and a supportive policy environment ensures North America’s dominance in the global organ-on-a-chip market. While Europe and Asia Pacific are quickly emerging as high-growth regions, North America maintains its edge through its early mover advantage, integrated innovation ecosystem, and strong focus on transforming drug development with human-relevant models.

Global Organ-on-a-Chip Market, By Region (USD million)

Major Companies and Competitive Landscape

The global organ-on-a-chip market is highly dynamic and fragmented, with both established life sciences leaders and emerging startups driving innovation and revenue growth. Companies in this sector are actively pursuing strategies such as strategic collaborations, research partnerships, licensing agreements, and targeted acquisitions to strengthen their competitive position. A key emphasis is placed on advancing chip design, integrating microfluidics with tissue engineering, improving scalability, and developing cost-efficient platforms that can reliably mimic human organ functions. These efforts are aimed at accelerating drug discovery, enhancing toxicology studies, reducing dependence on animal models, and enabling personalized medicine approaches. Some of the leading companies profiled in the global organ-on-a-chip market report include:

-

-

-

-

- 4DCell

- Aim biotech

- Beonchip

- CN BIO

- Emulate

- InSphero

- Jiksak Bioengineering

- Kirkstall

- Lena Biosciences

- Merck Millipore

- MesoBio Tech

- MicroBrain Biotech

- Mimetas

- Numa Biosciences

- Qureator

- SynVivo

- TissUse

- Visikol

- Xona microfluidics

- Hesperos

- TARA Biosystems

- Cherry Biotech

- BiomimX

- AlveoliX

- Nortis

-

-

-

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 103.73 Million |

| CAGR (2024–2032) | 34.43% |

| Revenue forecast to 2033 | USD 822.93 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million, and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Offering, By Organ Type, By Model Type, By Purpose Type, By Type of Construction Material, By Application Area, By End User and By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, UAE, South Africa, Turkey, Rest of MEA |

| Key companies profiled | 4DCell, Aim biotech, Beonchip, CN BIO, Emulate, InSphero, Jiksak Bioengineering, Kirkstall, Lena Biosciences, Merck Millipore, MesoBio Tech, MicroBrain Biotech, Mimetas, Numa Biosciences, Qureator, SynVivo, TissUse, Visikol, Xona microfluidics, Hesperos, TARA Biosystems, Cherry Biotech, BiomimX, AlveoliX, Nortis |

| Customization scope | 10 hours of free customization and expert consultation |

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of global organ-on-a-chip market

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1.Primary

2.1.2.Secondary

2.1.3.Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1.Market value

2.3.2.Market volume

2.3.3.Exchange rate

2.3.4.Price

2.3.5.Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2025-2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10. Formulation & manufacturing

4.11. Distribution & retail

4.12. Import-export analysis4.13.Brand comparative analysis

4.14. Technological advancements

4.15. Porter’s five force

4.15.1. Threat of new entrants

4.15.1.1. Capital requirment

4.15.1.2. Product knowledge

4.15.1.3. Technical knowledge

4.15.1.4. Customer relation

4.15.1.5. Access to appliation and technology

4.15.2. Threat of substitutes

4.15.2.1. Cost

4.15.2.2. Performance

4.15.2.3. Availability

4.15.2.4. Technical knowledge

4.15.2.5. Durability

4.15.3. Bargainning power of buyers

4.15.3.1. Numbers of buyers relative to suppliers

4.15.3.2. Product differentiation

4.15.3.3. Threat of forward integration

4.15.3.4. Buyers volume

4.15.4. Bargainning power of suppliers

4.15.4.1. Suppliers concentration

4.15.4.2. Buyers switching cost to other suppliers

4.15.4.3. Threat of backward integration

4.15.5. Bargainning power of suppliers

4.15.5.1. Industry concentration

4.15.5.2. Industry growth rate

4.15.5.3. Product differentiation

4.15.6. Patent analysis

4.16. Patent quality and strength

4.17. Regulation coverage

4.18. Pricing analysis

4.19. Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1.Rising demand for predictive, animal-free drug testing models

5.1.2.Advances in microfluidics, multi-organ integration, and tissue engineering

5.1.3.Increasing industry R&D investments and collaborations

5.2. Restraints

5.2.1.Lack of standardized protocols and validation frameworks

5.2.2.Limited scalability and technical expertise requirements

5.3. Opportunities

5.3.1.Growing adoption in drug discovery, personalized medicine, and toxicology

5.3.2.Expansion of body-on-a-chip platforms for complex disease modeling

5.3.3.Strong growth potential in developing nations with supportive funding

5.4. Threat

5.4.1.Competition from organoids and 3D culture systems

5.4.2.Uncertain regulatory pathways and validation challenges

Chapter 6. Global Organ-on-a-Chip Market By Offering Insights & Trends, Revenue

(USD Million)

6.1. Offering Dynamics & Market Share, 2025–2032

6.1.1.Products

6.1.1.1. Organ Chips

6.1.1.1.1. Single-organ chips

6.1.1.1.2. Multi-organ/body-on-a-chip systems

6.1.1.2. Instruments & Platforms

6.1.1.3. Consumables & Reagents

6.1.1.4. Software & Data Tools

6.1.1.5. Kits & Ready-to-use Panels

6.1.2.Services

6.1.2.1. Customs Services

6.1.2.2. Standard Services

Chapter 7. Global Organ-on-a-Chip Market By Organ Type Insights & Trends, Revenue

(USD Million)

7.1. Organ Type Dynamics & Market Share, 2025-2032

7.1.1.Liver-on-a-Chip

7.1.2.Lung-on-a-Chip

7.1.3.Heart-on-a-Chip

7.1.4.Others

Chapter 8. Global Organ-on-a-Chip Market By Model Type Insights & Trends, Revenue

(USD Million)

8.1. Model Type Dynamics & Market Share, 2025-2032

8.1.1.Organ-Based models

8.1.2.Disease-Based models

Chapter 9. Global Organ-on-a-Chip Market By Purpose Type Insights & Trends,

Revenue (USD Million)

9.1. Purpose Level Dynamics & Market Share, 2025-2032

9.1.1.Therapeutics

9.1.2.Research

Chapter 10. Global Organ-on-a-Chip Market By Type of Construction Material Insights &

Trends, Revenue (USD Million)

10.1. Type of Construction Material Dynamics & Market Share, 2025-2032

10.1.1. Polydimethylsiloxane

10.1.2. Glass

10.1.3. Hydrogels

10.1.4. Thermoplastics

10.1.5. Others (Silicon)

Chapter 11. Global Organ-on-a-Chip Market By Application Area Insights & Trends,

Revenue (USD Million)

11.1. Application Area Dynamics & Market Share, 2025-2032

11.1.1. Drug discovery/Toxicity testing

11.1.2. Cancer research

11.1.3. Stem cell research

11.1.4. Tissue engineering/Regenerative medicine

11.1.5. Others (Personalized medicine)

Chapter 12. Global Organ-on-a-Chip Market By End User Insights & Trends, Revenue

(USD Million)

12.1. End User Dynamics & Market Share, 2025-2032

12.1.1. Pharmaceutical and biotech companies

12.1.2. Academic and research players

12.1.3. Cosmetic industry players

12.1.4. Others (Contract Research Organizations)

Chapter 13. Global Organ-on-a-Chip Market Regional Outlook

13.1. Global Enzymatic DNA Synthesis Market Share By Region, 2025-2032

13.2. North America

13.2.1. Market By Offering, Market Estimates and Forecast, USD Million

13.2.1.1. Products

13.2.1.1.1. Organ Chips

13.2.1.1.1.1. Single-organ chips

13.2.1.1.1.2. Multi-organ/body-on-a-chip systems

13.2.1.1.2. Instruments & Platforms

13.2.1.1.3. Consumables & Reagents

13.2.1.1.4. Software & Data Tools

13.2.1.1.5. Kits & Ready-to-use Panels

13.2.1.2. Services

13.2.1.2.1. Customs Services

13.2.1.2.2. Standard Services

13.3. Market By Organ Type, Market Estimates and Forecast, USD Million

13.3.1. Liver-on-a-Chip

13.3.2. Lung-on-a-Chip

13.3.3. Heart-on-a-Chip

13.3.4. Others

13.4. Market By Model Type, Market Estimates and Forecast, USD Million

13.4.1. Organ-Based models

13.4.2. Disease-Based models

13.5. Market By Purpose Type, Market Estimates and Forecast, USD Million

13.5.1. Therapeutics

13.5.2. Research

13.6. Market By Type of Construction Material, Market Estimates and Forecast, USD Million

13.6.1. Polydimethylsiloxane

13.6.2. Glass

13.6.3. Hydrogels

13.6.4. Thermoplastics

13.6.5. Others (Silicon)

13.7. Market By Appliaction Area, Market Estimates and Forecast, USD Million

13.7.1. Drug discovery/Toxicity testing

13.7.2. Cancer research

13.7.3. Stem cell research

13.7.4. Tissue engineering/Regenerative medicine

13.7.5. Others (Personalized medicine)

13.8. Market By End User, Market Estimates and Forecast, USD Million

13.8.1. Pharmaceutical and biotech companies

13.8.2. Academic and research players

13.8.3. Cosmetic industry players

13.8.4. Others (Contract Research Organizations)

13.9. Market By Country, Market Estimates and Forecast, USD Million

13.9.1. US

13.9.2. Canada

13.9.3. Mexico

13.10. Europe

13.11. Market By Offering, Market Estimates and Forecast, USD Million

13.11.1. Products

13.11.1.1.Organ Chips

13.11.1.1.1. Single-organ chips

13.11.1.1.2. Multi-organ/body-on-a-chip systems

13.11.1.2.Instruments & Platforms

13.11.1.3.Consumables & Reagents

13.11.1.4.Software & Data Tools

13.11.1.5.Kits & Ready-to-use Panels

13.11.2. Services

13.11.2.1.Customs Services

13.11.2.2.Standard Services

13.12. Market By Organ Type, Market Estimates and Forecast, USD Million

13.12.1. Liver-on-a-Chip

13.12.2. Lung-on-a-Chip

13.12.3. Heart-on-a-Chip

13.12.4. Others

13.13. Market By Model Type, Market Estimates and Forecast, USD Million,

13.13.1. Organ-Based models

13.13.2. Disease-Based models

13.14. Market By Purpose Type, Market Estimates and Forecast, USD Million

13.14.1. Therapeutics

13.14.2. Research

13.15. Market By Type of Construction Material, Market Estimates and Forecast, USD Million,

13.15.1. Polydimethylsiloxane

13.15.2. Glass

13.15.3. Hydrogels

13.15.4. Thermoplastics

13.15.5. Others (Silicon)

13.16. Market By Application Area, Market Estimates and Forecast, USD Million

13.16.1. Drug discovery/Toxicity testing

13.16.2. Cancer research

13.16.3. Stem cell research

13.16.4. Tissue engineering/Regenerative medicine

13.16.5. Others (Personalized medicine)

13.17. Market By End User, Market Estimates and Forecast, USD Million

13.17.1. Pharmaceutical and biotech companies

13.17.2. Academic and research players

13.17.3. Cosmetic industry players

13.17.4. Others (Contract Research Organizations)

13.18. Market By Country, Market Estimates and Forecast, USD Million

13.18.1. Germany

13.18.2. France

13.18.3. U.K

13.18.4. Italy

13.18.5. Spain

13.18.6. Benelux

13.18.7. Russia

13.18.8. Finland

13.18.9. Sweden

13.18.10. Rest Of Europe

13.19. Asia-Pacific

13.20. Market By Offering, Market Estimates and Forecast, USD Million

13.20.1. Products

13.20.1.1.Organ Chips

13.20.1.1.1. Single-organ chips

13.20.1.1.2. Multi-organ/body-on-a-chip systems

13.20.1.2.Instruments & Platforms

13.20.1.3.Consumables & Reagents

13.20.1.4.Software & Data Tools

13.20.1.5.Kits & Ready-to-use Panels

13.20.2. Services

13.20.2.1.Customs Services

13.20.2.2.Standard Services

13.21. Market By Organ Type, Market Estimates and Forecast, USD Million

13.21.1. Liver-on-a-Chip

13.21.2. Lung-on-a-Chip

13.21.3. Heart-on-a-Chip

13.21.4. Others

13.22. Market By Model Type, Market Estimates and Forecast, USD Million

13.22.1. Organ-Based models

13.22.2. Disease-Based models

13.23. Market By Purpose Type, Market Estimates and Forecast, USD Million

13.23.1. Therapeutics

13.23.2. Research

13.24. Market By Type of Construction Material, Market Estimates and Forecast, USD Million

13.24.1. Polydimethylsiloxane

13.24.2. Glass

13.24.3. Hydrogels

13.24.4. Thermoplastics

13.24.5. Others (Silicon)

13.25. Market By Application Area, Market Estimates and Forecast, USD Million

13.25.1. Drug discovery/Toxicity testing

13.25.2. Cancer research

13.25.3. Stem cell research

13.25.4. Tissue engineering/Regenerative medicine

13.25.5. Others (Personalized medicine)

13.26. Market By End User, Market Estimates and Forecast, USD Million

13.26.1. Pharmaceutical and biotech companies

13.26.2. Academic and research players

13.26.3. Cosmetic industry players

13.26.4. Others (Contract Research Organizations)

13.27. Market By Country, Market Estimates and Forecast, USD Million

13.27.1. China

13.27.2. India

13.27.3. Japan

13.27.4. South Korea

13.27.5. Indonesia

13.27.6. Thailand

13.27.7. Vietnam

13.27.8. Australia

13.27.9. New Zeland

13.27.10. Rest of APAC

13.28. Latin America

13.29. Market By Offering, Market Estimates and Forecast, USD Million

13.29.1. Products

13.29.1.1.Organ Chips

13.29.1.1.1. Single-organ chips

13.29.1.1.2. Multi-organ/body-on-a-chip systems

13.29.1.2.Instruments & Platforms

13.29.1.3.Consumables & Reagents

13.29.1.4.Software & Data Tools

13.29.1.5.Kits & Ready-to-use Panels

13.29.2. Services

13.29.2.1.Customs Services

13.29.2.2.Standard Services

13.30. Market By Organ Type, Market Estimates and Forecast, USD Million

13.30.1. Liver-on-a-Chip

13.30.2. Lung-on-a-Chip

13.30.3. Heart-on-a-Chip

13.30.4. Others

13.31. Market By Model Type, Market Estimates and Forecast, USD Million

13.31.1. Organ-Based models

13.31.2. Disease-Based models

13.32. Market By Purpose Type, Market Estimates and Forecast, USD Million

13.32.1. Therapeutics

13.32.2. Research

13.33. Market By Type of Construction Material, Market Estimates and Forecast, USD Million

13.33.1. Polydimethylsiloxane

13.33.2. Glass

13.33.3. Hydrogels

13.33.4. Thermoplastics

13.33.5. Others (Silicon)

13.34. Market By Application Area, Market Estimates and Forecast, USD Million

13.34.1. Drug discovery/Toxicity testing

13.34.2. Cancer research

13.34.3. Stem cell research

13.34.4. Tissue engineering/Regenerative medicine

13.34.5. Others (Personalized medicine)

13.35. Market By End User, Market Estimates and Forecast, USD Million

13.35.1. Pharmaceutical and biotech companies

13.35.2. Academic and research players

13.35.3. Cosmetic industry players

13.35.4. Others (Contract Research Organizations)

13.36. Market By Country, Market Estimates and Forecast, USD Million

13.36.1. Brazil

13.36.2. Rest of LATAM

13.37. Middle East & Africa

13.38. Market By Offering, Market Estimates and Forecast, USD Million

13.38.1. Products

13.38.1.1.Organ Chips

13.38.1.1.1. Single-organ chips

13.38.1.1.2. Multi-organ/body-on-a-chip systems

13.38.1.2.Instruments & Platforms

13.38.1.3.Consumables & Reagents

13.38.1.4.Software & Data Tools

13.38.1.5.Kits & Ready-to-use Panels

13.38.2. Services

13.38.2.1.Customs Services

13.38.2.2.Standard Services

13.39. Market By Organ Type, Market Estimates and Forecast, USD Million

13.39.1. Liver-on-a-Chip

13.39.2. Lung-on-a-Chip

13.39.3. Heart-on-a-Chip

13.39.4. Others

13.40. Market By Model Type, Market Estimates and Forecast, USD Million

13.40.1. Organ-Based models

13.40.2. Disease-Based models

13.41. Market By Purpose Type, Market Estimates and Forecast, USD Million

13.41.1. Therapeutics

13.41.2. Research

13.42. Market By Type of Construction Material, Market Estimates and Forecast, USD Million

13.42.1. Polydimethylsiloxane

13.42.2. Glass

13.42.3. Hydrogels

13.42.4. Thermoplastics

13.42.5. Others (Silicon)

13.43. Market By Application Area, Market Estimates and Forecast, USD Million

13.43.1. Drug discovery/Toxicity testing

13.43.2. Cancer research

13.43.3. Stem cell research

13.43.4. Tissue engineering/Regenerative medicine

13.43.5. Others (Personalized medicine)

13.44. Market By End User, Market Estimates and Forecast, USD Million

13.44.1. Pharmaceutical and biotech companies

13.44.2. Academic and research players

13.44.3. Cosmetic industry players

13.44.4. Others (Contract Research Organizations)

13.45. Market By Country, Market Estimates and Forecast, USD Million

13.45.1. Saudi Arabia

13.45.2. UAE

13.45.3. South Africa

13.45.4. Turkey

13.45.5. Rest of MEA

Chapter 14. Competitive Landscape

14.1. Market Revenue Share By Manufacturers

14.2. Mergers & Acquisitions

14.3. Competitor’s Positioning

14.4. Strategy Benchmarking

14.5. Vendor Landscape

14.5.1. Distributors

14.5.1.1. North America

14.5.1.2. Europe

14.5.1.3. Asia Pacific

14.5.1.4. Middle East & Africa

14.5.1.5. Latin America

14.5.2. Others

Chapter 15. Company Profiles

15.1. 4DCell

15.1.1. Company Overview

15.1.2. Product & Service Offerings

15.1.3. Strategic Initiatives

15.1.4. Financials

15.1.5. Research Insights

15.2. Aim biotech

15.2.1. Company Overview

15.2.2. Product & Service Offerings

15.2.3. Strategic Initiatives

15.2.4. Financials

15.2.5. Research Insights

15.3. Beonchip

15.3.1. Company Overview

15.3.2. Product & Service Offerings

15.3.3. Strategic Initiatives

15.3.4. Financials

15.3.5. Research Insights

15.4. CN BIO

15.4.1. Company Overview

15.4.2. Product & Service Offerings

15.4.3. Strategic Initiatives

15.4.4. Financials

15.4.5. Research Insights

15.5. Emulate

15.5.1. Company Overview

15.5.2. Product & Service Offerings

15.5.3. Strategic Initiatives

15.5.4. Financials

15.5.5. Research Insights

15.6. InSphero

15.6.1. Company Overview

15.6.2. Product & Service Offerings

15.6.3. Strategic Initiatives

15.6.4. Financials

15.6.5. Research Insights

15.7. Molecular Assemblies

15.7.1. Company Overview

15.7.2. Product & Service Offerings

15.7.3. Strategic Initiatives

15.7.4. Financials

15.7.5. Conclusion

15.8. Kirkstall

15.8.1. Company Overview

15.8.2. Product & Service Offerings

15.8.3. Strategic Initiatives

15.8.4. Financials

15.8.5. Conclusion

15.9. Lena Biosciences

15.9.1. Company Overview

15.9.2. Product & Service Offerings

15.9.3. Strategic Initiatives

15.9.4. Financials

15.9.5. Conclusion

15.10. Merck Millipore

15.10.1. Company Overview

15.10.2. Product & Service Offerings

15.10.3. Strategic Initiatives

15.10.4. Financials

15.10.5. Conclusion

15.11. MesoBio Tech

15.11.1. Company Overview

15.11.2. Product & Service Offerings

15.11.3. Strategic Initiatives

15.11.4. Financials

15.11.5. Conclusion

15.12. MicroBrain Biotech

15.12.1. Company Overview

15.12.2. Product & Service Offerings

15.12.3. Strategic Initiatives

15.12.4. Financials

15.12.5. Conclusion

15.13. Mimetas

15.13.1. Company Overview

15.13.2. Product & Service Offerings

15.13.3. Strategic Initiatives

15.13.4. Financials

15.13.5. Conclusion

15.14. Numa Biosciences

15.14.1. Company Overview

15.14.2. Product & Service Offerings

15.14.3. Strategic Initiatives

15.14.4. Financials

15.14.5. Conclusion

15.15. Qureator

15.15.1. Company Overview

15.15.2. Product & Service Offerings

15.15.3. Strategic Initiatives

15.15.4. Financials

15.15.5. Conclusion

15.16. SynVivo

15.16.1. Company Overview

15.16.2. Product & Service Offerings

15.16.3. Strategic Initiatives

15.16.4. Financials

15.16.5. Conclusion

15.17. TissUse

15.17.1. Company Overview

15.17.2. Product & Service Offerings

15.17.3. Strategic Initiatives

15.17.4. Financials

15.17.5. Conclusion

15.18. Visikol

15.18.1. Company Overview

15.18.2. Product & Service Offerings

15.18.3. Strategic Initiatives

15.18.4. Financials

15.18.5. Conclusion

15.19. Xona microfluidics

15.19.1. Company Overview

15.19.2. Product & Service Offerings

15.19.3. Strategic Initiatives

15.19.4. Financials

15.19.5. Conclusion

15.20. Hesperos

15.20.1. Company Overview

15.20.2. Product & Service Offerings

15.20.3. Strategic Initiatives

15.20.4. Financials

15.20.5. Conclusion

15.21. TARA Biosystems

15.21.1. Company Overview

15.21.2. Product & Service Offerings

15.21.3. Strategic Initiatives

15.21.4. Financials

15.21.5. Conclusion

15.22. Cherry Biotech

15.22.1. Company Overview

15.22.2. Product & Service Offerings

15.22.3. Strategic Initiatives

15.22.4. Financials

15.22.5. Conclusion

15.23. BiomimX

15.23.1. Company Overview

15.23.2. Product & Service Offerings

15.23.3. Strategic Initiatives

15.23.4. Financials

15.23.5. Conclusion

15.24. AlveoliX

15.24.1. Company Overview

15.24.2. Product & Service Offerings

15.24.3. Strategic Initiatives

15.24.4. Financials

15.24.5. Conclusion

15.25. Nortis

15.25.1. Company Overview

15.25.2. Product & Service Offerings

15.25.3. Strategic Initiatives

15.25.4. Financials

15.25.5. Conclusion

Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP. has segmented global Organ-on-a-Chip market on the basis of By Offering, By Organ Type, By Model Type, By Purpose Type, By Type of Construction Material, By Application Area, By End User and by region for 2019 to 2032.

- Global Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Global Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Global Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Global Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Global Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Global Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Global End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- North America

- North America Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- North America Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- North America Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- North America Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- North America Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- North America Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- North America End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- U.S

- U.S Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- U.S Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- U.S Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- U.S Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- U.S Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- U.S Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- U.S End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Canada

- Canada Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Canada Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Canada Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Canada Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Canada Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Canada Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Canada End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Mexico

- Mexico Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Mexico Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Mexico Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Mexico Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Mexico Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Mexico Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Mexico End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Europe

- Europe Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Europe Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Europe Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Europe Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Europe Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Europe Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Europe End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Germany

- Germany Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Germany Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Germany Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Germany Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Germany Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Germany Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Germany End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- France

- France Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- France Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- France Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- France Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- France Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- France Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- France End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- U.K

- U.K Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- U.K Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- U.K Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- U.K Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- U.K Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- U.K Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- U.K End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Italy

- Italy Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Italy Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Italy Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Italy Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Italy Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Italy Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Italy End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Spain

- Spain Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Spain Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Spain Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Spain Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Spain Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Spain Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Spain End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Benelux

- Benelux Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Benelux Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Benelux Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Benelux Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Benelux Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Benelux Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Benelux End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Russia

- Russia Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Russia Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Russia Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Russia Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Russia Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Russia Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Russia End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Finland

- Finland Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Finland Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Finland Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Finland Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Finland Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Finland Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Finland End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Sweden

- Sweden Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Sweden Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Sweden Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Sweden Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Sweden Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Sweden Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Sweden End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Rest of Europe

- Rest of Europe Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Rest of Europe Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Rest of Europe Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Rest of Europe Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Rest of Europe Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Rest of Europe Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Rest of Europe End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Asia-Pacific

- Asia-Pacific Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Asia-Pacific Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Asia-Pacific Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Asia-Pacific Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Asia-Pacific Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Asia-Pacific Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Asia-Pacific End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- China

- China Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- China Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- China Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- China Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- China Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- China Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- China End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- India

- India Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- India Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- India Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- India Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- India Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- India Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- India End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Japan

- Japan Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Japan Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Japan Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Japan Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Japan Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Japan Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Japan End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- South Korea

- South Korea Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- South Korea Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- South Korea Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- South Korea Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- South Korea Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- South Korea Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- South Korea End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Indonesia

- Indonesia Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Indonesia Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Indonesia Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Indonesia Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Indonesia Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Indonesia Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Indonesia End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Thailand

- Thailand Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Thailand Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Thailand Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Thailand Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Thailand Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Thailand Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others

- Thailand End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical and biotech companies

-

- Academic and research players

-

- Cosmetic industry players

-

- Others

- Vietnam

- Vietnam Offering Outlook (Revenue, USD Million; 2025-2032)

-

- Products

-

- Services

- Vietnam Organ Type Outlook (Revenue, USD Million; 2025-2032)

-

- Liver-on-a-Chip

-

- Lung-on-a-Chip

-

- Heart-on-a-Chip

-

- Others

- Vietnam Model Type Outlook (Revenue, USD Million; 2025-2032)

-

- Organ-Based models

-

- Disease-Based models

- Vietnam Purpose Type Outlook (Revenue, USD Million; 2025-2032)

-

- Therapeutics

-

- Research

- Vietnam Type of Construction Material Outlook (Revenue, USD Million; 2025-2032)

-

- Polydimethylsiloxane

-

- Glass

-

- Thermoplastics

-

- Hydrogels

-

- Others

- Vietnam Application Area Outlook (Revenue, USD Million; 2025-2032)

-

- Drug discovery

-

- Toxicity testing

-

- Cancer research

-

- Stem cell research

-

- Tissue engineering

-

- Regenerative medicine

-

- Others