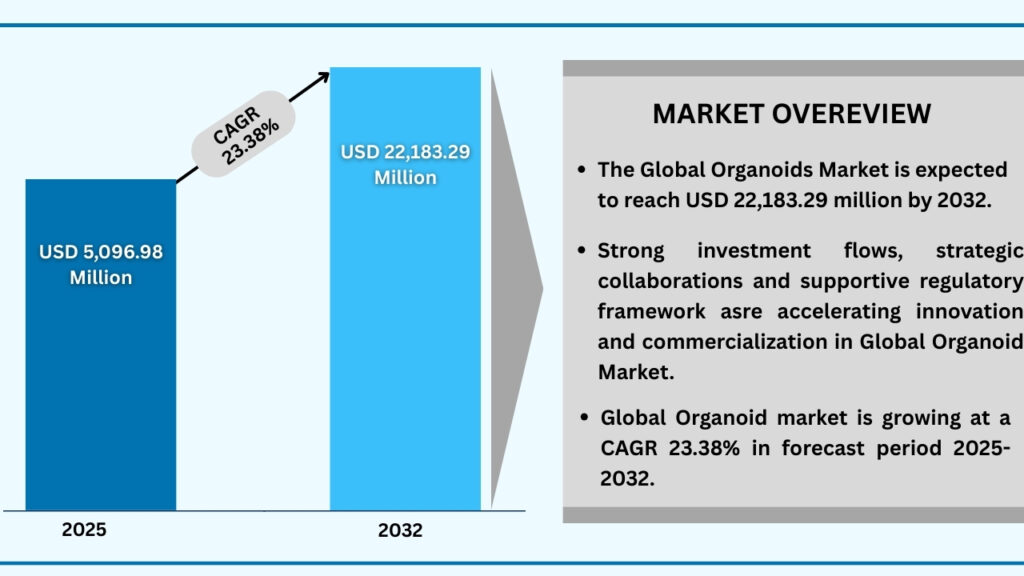

Market Synopsis

The global organoid market size was USD 4,131.12 million in 2024 and is expected to reach USD 22,183.29 million at a CAGR of 23.38% during the forecast period from 2025 to 2032. The global organoid market is experiencing rapid expansion, driven by the growing demand for physiologically relevant 3D models that closely replicate human organ systems. Increasing emphasis on precision medicine, regenerative therapies, and advanced drug discovery is fuelling adoption across pharmaceutical, biotechnology, and academic research sectors. Rising concerns over the limitations of traditional 2D cell cultures and animal models are further boosting the shift toward organoid-based systems, which offer higher accuracy, scalability, and predictive value. Market growth is also supported by advancements in stem cell research, genome editing technologies, and bioengineering methods that are enhancing the development and application of organoids in disease modelling, toxicology, and personalized treatment testing. Strong investment flows, strategic collaborations, and supportive regulatory frameworks are accelerating innovation and commercialization in this field. With global R&D expenditure in life sciences increasing steadily, organoid technologies are emerging as a transformative tool, poised to reshape drug discovery, cancer research, and regenerative medicine, particularly in regions fostering innovation and translational research.

Global Organoid Market (USD million)

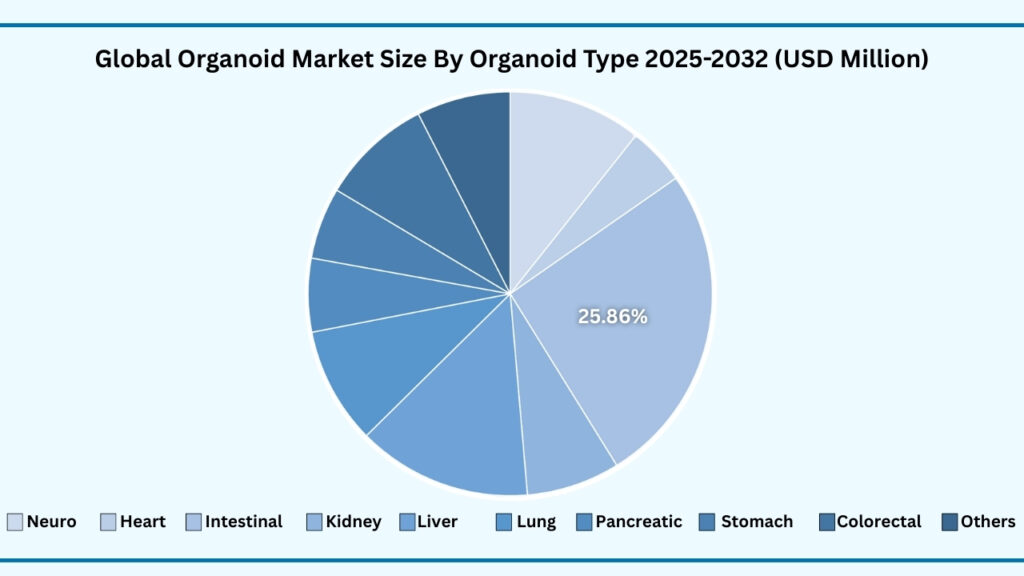

Global Organoid Market by Organoid Type Insights:

Intestinal organoids segment accounted for market share of share 25.86% in 2024 in the global organoid market.

The organoid type segment showcases a diverse range of applications, with intestinal organoids leading the market at 25.86% of revenues in 2024. This sub-segment alone is projected to grow at a CAGR of 23.40%, reaching USD 5,751.53 million during the forecast period from 2025 to 2032. The strong adoption of intestinal organoids is driven by their unmatched ability to replicate gut physiology, offering valuable insights into nutrient absorption, microbiome interactions, and gastrointestinal diseases such as Crohn’s disease and colorectal cancer. Beyond intestinal models, neuro, liver, kidney, and heart organoids are increasingly recognized as powerful tools for studying neurodegeneration, metabolic disorders, nephrotoxicity, and cardiomyopathies, respectively. Each organoid type brings unique advantages by mirroring human tissue complexity in ways that traditional 2D cell cultures or animal models cannot achieve.

Market players and research institutes are actively advancing this segment by refining protocols, developing standardized culture systems, and expanding disease-specific models. For instance, STEMCELL Technologies has developed a wide range of organoid culture kits and media that streamline workflows for intestinal, liver, and brain organoids, making them more accessible for both academic and industrial researchers. Similarly, HUB Organoids, in collaboration with Hubrecht Organoid Technology, has pioneered patient-derived organoid models that are now being applied in personalized oncology to guide treatment strategies and accelerate clinical decision-making.

Alongside these innovations, lung, pancreatic, and stomach organoids are finding applications in conditions such as pulmonary fibrosis, diabetes, and gastric cancers, while “others” like prostate, retina, skin, and breast organoids are enabling specialized research across oncology, ophthalmology, and dermatology. Collectively, these advances are transforming organoid platforms into indispensable assets for drug discovery, regenerative medicine, and personalized healthcare, while strategic collaborations between biotech firms, pharmaceutical companies, and academic consortia continue to expand accessibility and accelerate their clinical translation.

Global Organoid Market, By Organoid Type (USD million)

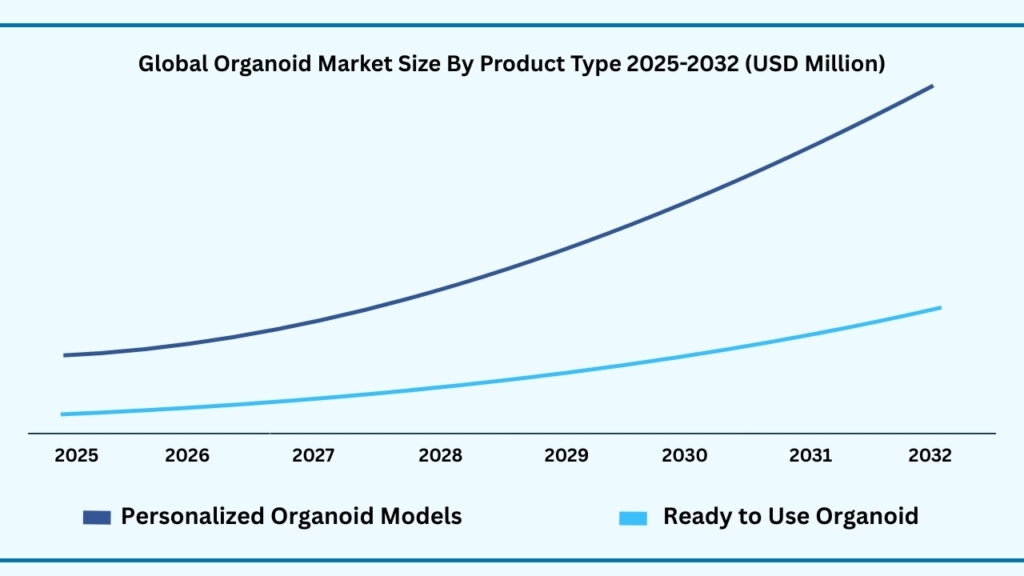

Global Organoid Market by Product Type Insights:

Ready-to-Use organoid products segment accounted for market share of share 61.91% in 2024 in the global organoid market.

The Ready-to-Use Organoid Products segment leads the global organoid market, accounting for 65.02% of the share in 2024. Revenues in this category are expected to reach USD 14,481.89 million during the forecast period from 2025 to 2032, growing at a CAGR of 23.44%. This dominance stems from the increasing adoption of prevalidated organoid cultures, expansion kits, and off-the-shelf models that enable researchers to accelerate their studies without the need for labour-intensive stem cell derivation or culture optimization. Ready-to-use products are being widely employed in applications ranging from cancer drug screening to toxicity assays and infectious disease research, as they offer consistency, scalability, and reproducibility across experiments. Academic institutions and pharmaceutical companies alike benefit from these solutions, as they provide standardized models that reduce variability and shorten project timelines. For example, STEMCELL Technologies has scaled its catalogue of intestinal, brain, and liver organoid kits, making it easier for labs worldwide to implement complex organoid systems in routine workflows.

Alongside this, the Personalized Organoid Models sub-segment is emerging as a transformative area, reflecting the shift toward precision medicine. Derived from patient-specific stem cells, these models allow researchers and clinicians to replicate individual disease profiles and evaluate tailored treatment strategies. Personalized organoids are proving especially valuable in oncology, where patient-derived tumour organoids are being used to guide therapy selection and improve clinical outcomes. Initiatives led by groups such as HUB Organoids, in collaboration with healthcare providers, have demonstrated the potential of these models to bring personalized insights directly into clinical decision-making. While this sub-segment currently represents a smaller share compared to ready-to-use products, it is gaining momentum as healthcare systems explore individualized approaches to drug testing and regenerative therapies.

Looking ahead, the organoid product landscape is expected to evolve further with the integration of advanced technologies such as AI-driven analytics, high-throughput screening platforms, and hybrid organoid–organ-on-a-chip systems. These innovations will not only enhance the predictive power of organoid models but also expand their role in translational research and clinical applications. As pharmaceutical pipelines become more focused on precision therapies and rare diseases, demand for both standardized and patient-specific organoid models will intensify. This dual track of innovation ensures that ready-to-use products will continue to anchor large-scale research, while personalized organoids redefine the future of patient-centered healthcare.

Global Organoid Market, By Product Type (USD million)

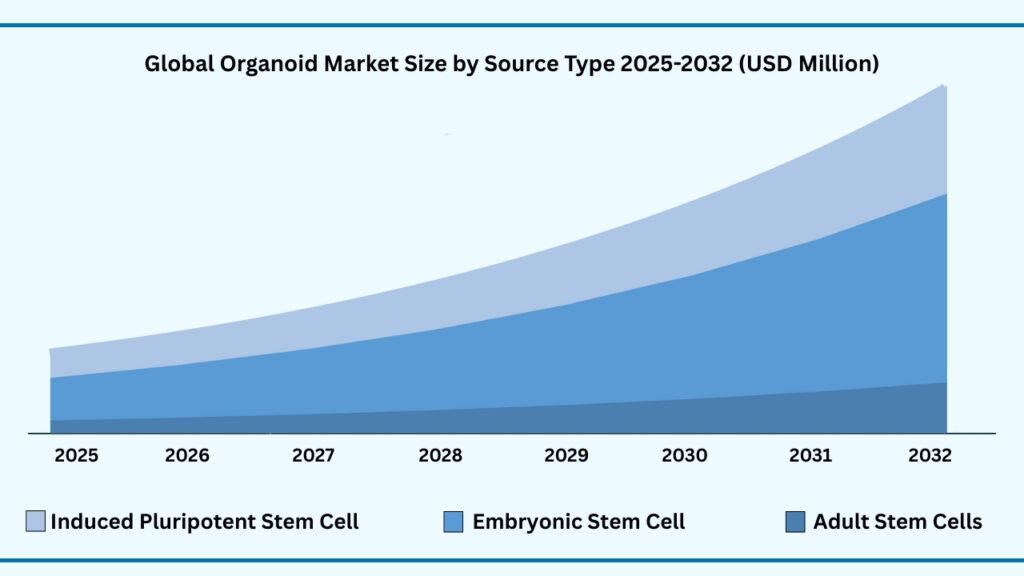

Global Organoid Market by Source Type Insights:

Induced Pluripotent Stem Cells (iPSCs) segment accounted for market share of share 54% in 2024 in the global organoid market.

The Induced Pluripotent Stem Cells (iPSCs) segment leads the global organoid market, capturing 54% of the share in 2024. Revenues from this category are expected to reach USD 12,066.02 million by the end of the forecast period from 2025 to 2032, growing at a CAGR of 23.49%. The strong position of iPSCs is attributed to their versatility, as they can be reprogrammed from adult somatic cells and differentiated into virtually any cell type. This makes them an ideal source for organoid development across multiple organ systems, including brain, liver, kidney, and heart. Researchers value iPSC-derived organoids for their ability to model patient-specific conditions and for their potential in regenerative medicine. They also offer ethical advantages over embryonic stem cells, driving their adoption across both academia and industry. For instance, FUJIFILM Cellular Dynamics has made significant strides in developing iPSC-derived cell lines and organoid models that are increasingly being integrated into pharmaceutical research and toxicity testing.

Alongside iPSCs, Embryonic Stem Cells (ESCs) continue to play a vital role in organoid research due to their inherent pluripotency and ability to form highly complex tissue structures. ESC-derived organoids are widely used in developmental biology studies and in modelling genetic diseases, offering insights into early-stage organogenesis that other cell sources cannot replicate. Meanwhile, Adult Stem Cells, particularly tissue-specific stem cells such as intestinal or hepatic progenitors, are gaining attention for their clinical relevance. These cells are directly harvested from tissues and expanded into organoids that closely resemble the native organ environment, making them valuable in disease modelling, personalized medicine, and regenerative therapies. Efforts by academic consortia and biotech companies are pushing forward the use of adult stem cell–derived organoids in translational applications, including gut microbiome studies and liver disease models.

In comparison, iPSCs currently dominate because they combine the scalability of cell reprogramming with the flexibility to generate a wide variety of organoid types, positioning them ahead of ESCs and adult stem cells. While ESCs remain important for fundamental biology and adult stem cells are well-suited for tissue-specific applications, iPSCs strike a balance between ethical acceptability, versatility, and clinical potential. This unique positioning ensures that iPSCs will continue to lead the market while ESCs and adult stem cells strengthen niche areas of organoid research.

Global Organoid Market, By Source Type (USD million)

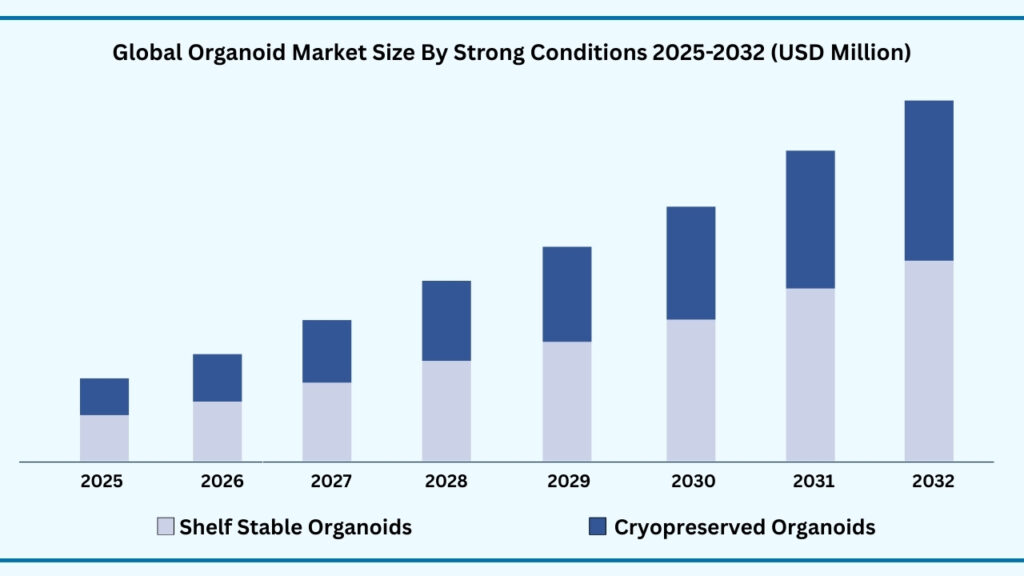

Global Organoid Market by Storage Conditions Insights:

Shelf-stable Organoids segment accounted for market share of share 61.91% in 2024 in the global organoid market.

The Shelf-stable Organoids segment leads the global organoid market, capturing 61.91% of the share in 2024. Revenues from this category are projected to reach USD 13,193.59 million by the end of the forecast period from 2025 to 2032, growing at a CAGR of 22.76%. The segment’s leadership is driven by the rising demand for organoid models that can be stored, transported, and readily applied without complex thawing or culture processes. Shelf-stable formats are particularly attractive to pharmaceutical companies, contract research organizations, and academic labs as they ensure reproducibility, reduce handling errors, and make large-scale studies more practical. These organoids are increasingly being used in applications such as high-throughput drug screening, toxicology testing, and disease modelling, where ease of use and reliability are critical. For example, companies are introducing ready-to-plate organoids that can be shipped globally, enabling research teams to begin experiments immediately upon delivery.

In contrast, the Cryopreserved Organoids sub-segment plays a complementary role, offering long-term storage solutions that retain cellular integrity and functionality. Cryopreservation allows researchers to build biobanks of patient-derived organoids, supporting personalized medicine initiatives and retrospective studies. This approach is especially valuable in oncology, where patient tumour organoids can be preserved for future drug response testing and therapeutic development. Several academic centres and biotech firms are actively expanding cryopreserved organoid libraries to facilitate collaborative research and clinical validation. While cryopreserved models require more specialized handling compared to shelf-stable counterparts, they are indispensable for ensuring genetic diversity and long-term accessibility in translational research.

In comparison, shelf-stable organoids currently dominate due to their convenience, scalability, and readiness for immediate application across diverse research settings. Cryopreserved organoids, on the other hand, remain critical for biobanking and patient-specific research that demands long-term preservation. Together, these storage innovations provide a balanced framework—shelf-stable formats driving everyday usability and scalability, while cryopreservation ensures depth, diversity, and clinical relevance in organoid research. This dual strategy is expected to shape the way organoids are distributed, applied, and integrated into global biomedical pipelines.

Global Organoid Market, By Storage conditions (USD million)

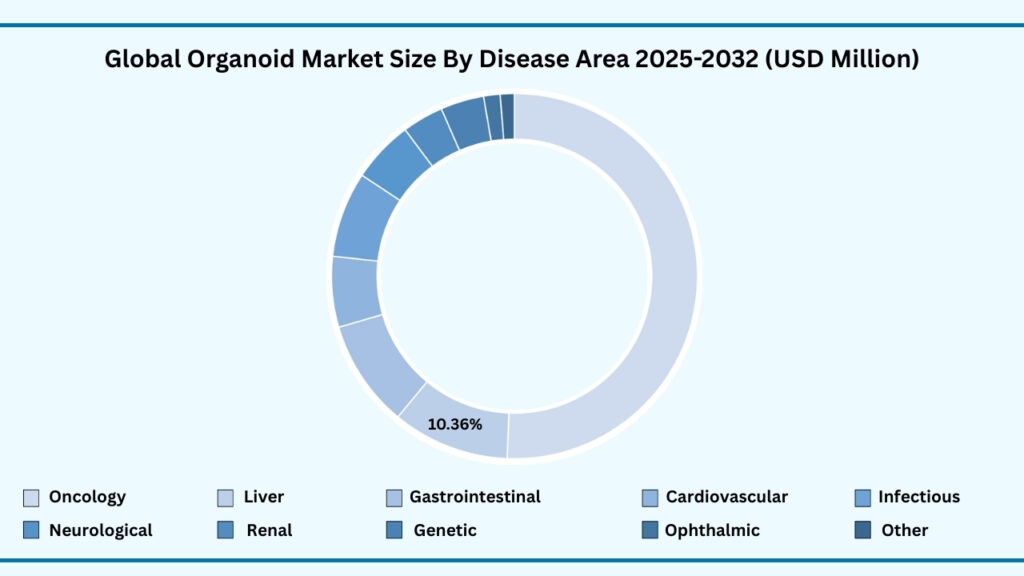

Global Organoid Market by Disease Area Insights:

Oncology segment accounted for market share of share 50.69% in 2024 in the global organoid market.

The Oncology segment leads the global organoid market, accounting for 50.69% of the share in 2024. Revenues in this category are projected to reach USD 11,262.86 million during the forecast period from 2025 to 2032, growing at a CAGR of 23.40%. This dominance is driven by the expanding use of tumour-derived organoids to study cancer biology, test drug responses, and design personalized treatment strategies. Organoids derived from patient tumour samples replicate the heterogeneity of cancers more accurately than traditional models, allowing researchers to evaluate chemotherapy, immunotherapy, and targeted therapies in a patient-specific manner. They are increasingly used by pharmaceutical companies for preclinical drug screening and by clinicians in precision oncology programs. For example, HUB Organoids has pioneered patient-derived tumour organoids for colorectal and breast cancers, helping translate lab findings into treatment guidance in clinical settings.

Beyond oncology, organoids are making a strong impact across other disease areas. Liver disease organoids are being applied in hepatotoxicity studies and in modelling viral hepatitis and fatty liver disease, while gastrointestinal organoids are enabling breakthroughs in inflammatory bowel disease, Crohn’s, and ulcerative colitis research. Neurological organoids derived from iPSCs are gaining traction for studying Alzheimer’s, Parkinson’s, and rare neurodevelopmental disorders, offering insights that animal models often fail to capture. In parallel, renal organoids are being explored for nephrotoxicity testing and kidney regeneration, while cardiovascular and infectious disease models are increasingly valuable for simulating cardiac dysfunctions or respiratory infections such as influenza and COVID-19. Emerging applications also include ophthalmic organoids to study retinal degeneration and genetic disease models to decode inherited conditions using CRISPR-edited lines.

In comparison, oncology currently dominates because cancer organoids directly address one of the largest unmet needs in global healthcare—effective, personalized cancer treatment. However, the rapid uptake of organoids in liver, gastrointestinal, neurological, and infectious disease research highlights how their application scope is broadening beyond oncology. This balance ensures that while cancer research anchors current demand, other therapeutic areas will continue to expand the market’s reach, making organoids a cornerstone technology for both biomedical research and future clinical practice.

Global Organoid Market, By Disease Area (USD million)

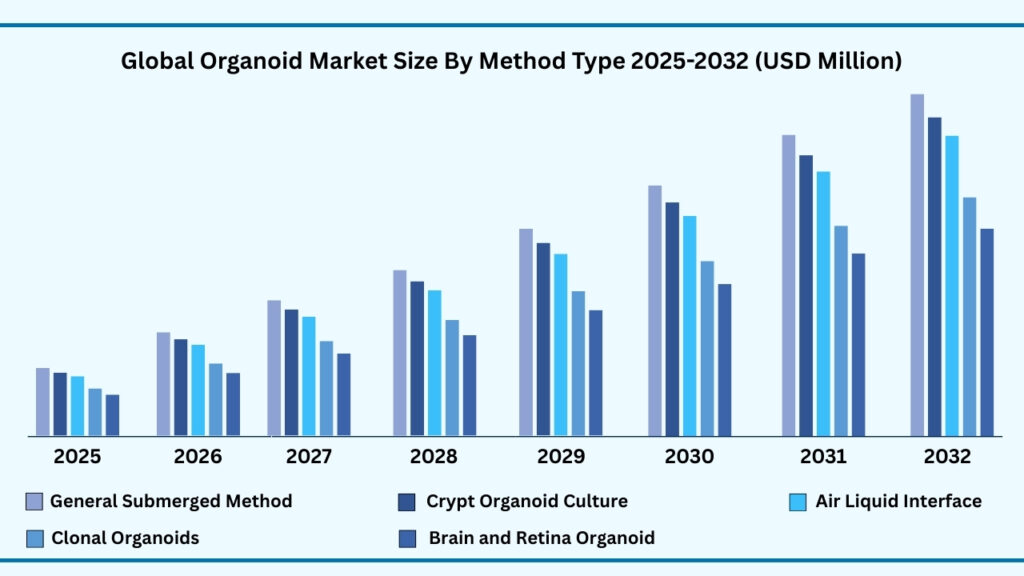

Global Organoid Market by Method Insights:

General Submerged Method for Organoid Culture segment accounted for market share of share 23.73% in 2024 in the global organoid market.

The General Submerged Method for Organoid Culture leads the global organoid market, capturing 23.73% of the share in 2024. Revenues from this segment are projected to reach USD 5,301.33 million during the forecast period from 2025 to 2032, growing at a CAGR of 23.49%. This method remains the most widely adopted because of its relative simplicity, cost-effectiveness, and adaptability across multiple tissue types. In this approach, organoids are embedded in an extracellular matrix scaffold, such as Matrigel, and cultured in nutrient-rich media under submerged conditions. The technique has become a gold standard for laboratories worldwide due to its reproducibility and compatibility with high-throughput applications. For instance, intestinal and hepatic organoids grown through this method are increasingly being used in drug screening and toxicity testing pipelines, giving researchers a reliable and scalable foundation for experimentation.

Alongside the submerged method, advanced techniques such as crypt organoid culture and the air-liquid interface (ALI) method are gaining momentum for enabling more physiologically relevant tissue environments. Crypt-based approaches, often applied to intestinal organoids, allow for better preservation of stem cell niches, while ALI methods are particularly valuable for modelling respiratory and gastrointestinal systems with enhanced epithelial organization. Similarly, clonal organoids derived from Lgr5+ cells are pushing the boundaries of precision research by isolating and expanding single stem cells into complex 3D structures, offering unique opportunities for developmental biology and cancer research. On another front, specialized brain and retina organoid protocols are opening new avenues in neuroscience and ophthalmology, helping researchers mimic cortical development or retinal degeneration with remarkable accuracy.

In comparison, while the general submerged method dominates today due to its ease of use and scalability, other specialized methods are carving strong niches by addressing the need for higher physiological relevance and disease-specific modelling. This combination ensures that while submerged cultures anchor the majority of current research activity, advanced culture techniques will continue to expand the toolkit available to scientists, accelerating the integration of organoids into translational research and clinical innovation.

Global Organoid Market, By Method (USD million)

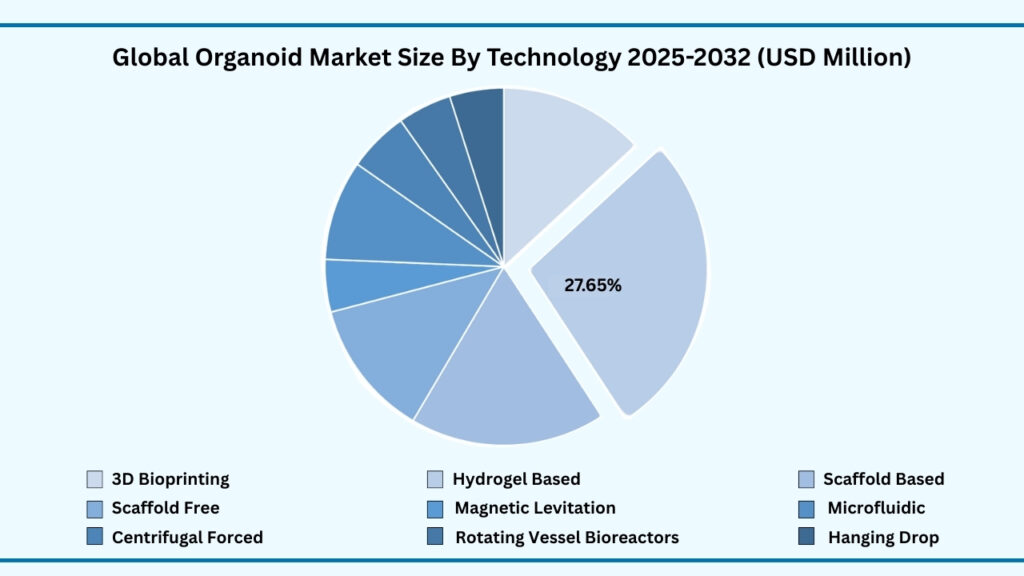

Global Organoid Market by Technology Insights:

Hydrogel-Based Technology segment accounted for market share of share 27.65% in 2024 in the global organoid market.

The Hydrogel-Based Technology segment dominates the global organoid market, holding 27.65% of the share in 2024. Revenues from this segment are projected to reach USD 6,133.68 million during forecast period from 2025 to 2032, expanding at a CAGR of 23.38%. Hydrogels have become the most widely used platform because they provide a supportive three-dimensional structure that closely mirrors the natural extracellular matrix (ECM). Their customizable properties—such as stiffness, porosity, and biochemical cues—enable researchers to culture organoids representing diverse tissues, including the liver, intestine, brain, and kidney. Both academic laboratories and pharmaceutical companies rely heavily on hydrogel systems because they deliver reproducibility and can be scaled for high-throughput applications. Increasingly, hydrogel formulations are being designed to mimic specific disease environments, which is driving progress in oncology research, regenerative therapies, and precision medicine.

At the same time, a wide range of alternative technologies are advancing organoid science. 3D bioprinting offers precise control over the placement of cells and biomaterials, creating highly customized organoid models for complex disease studies. Scaffold-based methods provide essential architectural support, whereas scaffold-free self-assembly techniques utilize the natural ability of cells to organize into tissue-like structures without external frameworks. Newer tools such as magnetic levitation and centrifugal forced aggregation are helping researchers generate consistent spheroids more efficiently. Systems like the rotating wall vessel bioreactor and hanging drop culture are improving nutrient and oxygen exchange during growth. In parallel, microfluidic technologies (organ-on-chip platforms) are bridging the gap between organoids and in vivo physiology by introducing fluid flow and mechanical cues that replicate organ-level functions.

In comparison, hydrogel-based approaches currently lead the market because they offer the best mix of scalability, flexibility, and physiological relevance. While bioprinting, microfluidics, and other next-generation methods are carving out strong niches for advanced research, hydrogels remain the cornerstone for most organoid applications. Together, these complementary technologies are creating a robust ecosystem—hydrogels providing the foundation for widespread adoption, while emerging tools expand the possibilities for more complex, clinically relevant organoid models.

Global Organoid Market, By Technology (USD million)

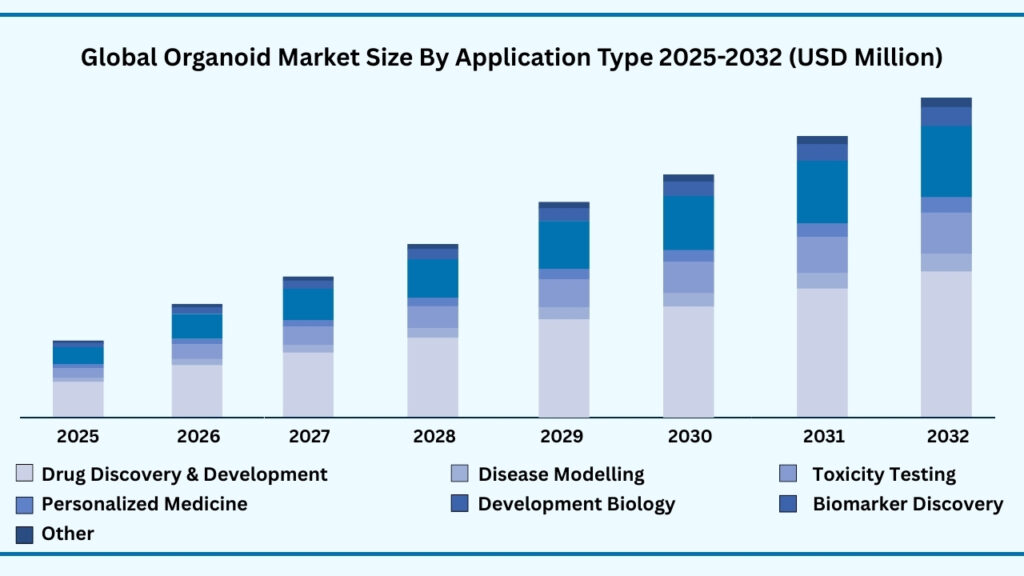

Global Organoid Market by Application Type Insights:

Drug Discovery and Development segment accounted for market share of share 40.27% in 2024 in the global organoid market.

The Drug Discovery and Development segment leads the global organoid market, capturing 40.27% of the share in 2024. Revenues from this category are projected to reach USD 8,976.31 million during the forecast period from 2025 to 2032, growing at a CAGR of 23.45%. The dominance of this segment is fuelled by the increasing use of organoids as predictive preclinical models that more accurately replicate human physiology compared to traditional 2D cultures or animal testing. Pharmaceutical companies are adopting organoid platforms to evaluate drug efficacy, optimize dosing, and reduce attrition rates during clinical trials. By offering insights into complex biological responses at an early stage, organoid-based drug discovery helps shorten development timelines and reduce costs. For instance, patient-derived tumour organoids are now being integrated into oncology pipelines, enabling the identification of responsive and resistant cancer subtypes before progressing into expensive trials.

Beyond drug discovery, organoids are proving valuable in a broad range of biomedical applications. Disease modelling has emerged as a transformative area, where organoids are used to recreate the pathophysiology of conditions such as cystic fibrosis, Alzheimer’s, and inflammatory bowel disease. This approach allows researchers to study disease mechanisms in a controlled environment and test new interventions with greater accuracy. Similarly, toxicity testing using liver, kidney, or cardiac organoids provides a safer and more reliable method for screening drug-induced side effects compared to animal studies. In parallel, personalized medicine and precision neurology are rapidly growing, with patient-derived brain organoids being applied to tailor treatments for neurodegenerative and rare neurological disorders. Applications also extend to developmental biology, where organoids are being used to study organ formation, and biomarker discovery, which is helping accelerate early detection of diseases. Other areas, including infectious disease research and regenerative medicine, are also gaining traction as organoids become more versatile and accessible.

In comparison, while drug discovery currently anchors the largest share due to its immediate commercial relevance, applications such as disease modelling, toxicity testing, and personalized medicine are expanding the horizon for organoid use. Together, these application areas illustrate how organoids are not just transforming pharmaceutical R&D but are also laying the groundwork for breakthroughs across biomedical research and clinical practice. This balanced growth ensures that organoids will remain central to both innovation pipelines and patient-focused healthcare strategies in the years ahead.

Global Organoid Market, By Application Type (USD million)

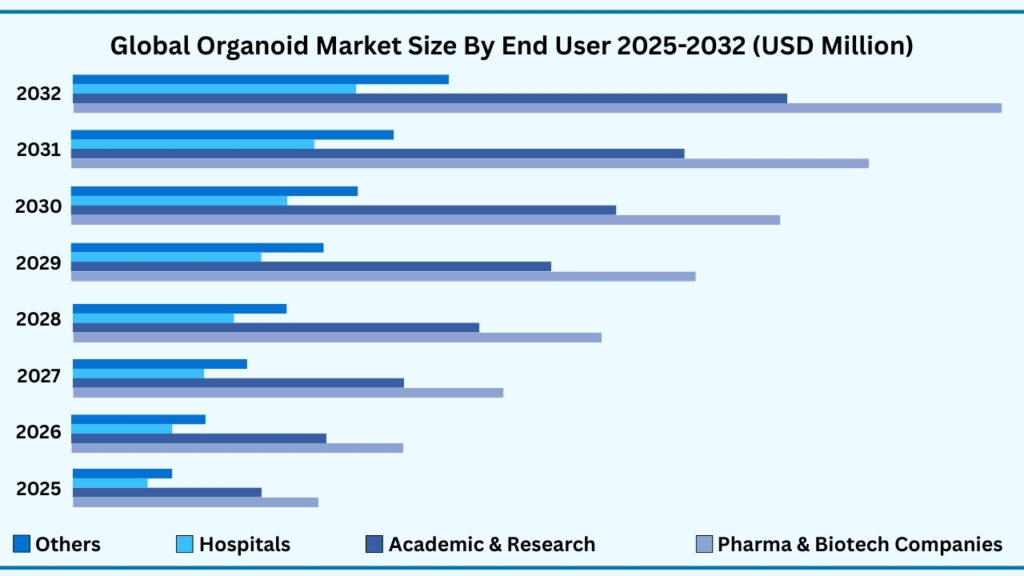

Global Organoid Market by End User Insights:

Pharmaceutical and Biotechnology Companies segment accounted for market share of share 45.69% in 2024 in the global organoid market.

The Pharmaceutical and Biotechnology Companies segment leads the global organoid market, accounting for 45.69% of the share in 2024. Revenues from this category are projected to reach USD 10,177.06 million during the forecast period from 2025 to 2032, growing at a CAGR of 23.44%. The segment’s dominance stems from the rapid adoption of organoid platforms in drug discovery, preclinical testing, and personalized therapy development. Pharma and biotech firms are increasingly using patient-derived organoids to evaluate drug efficacy and toxicity in disease-relevant models, significantly reducing the risks of late-stage trial failures. These companies also benefit from the scalability and reproducibility of organoid systems, which align well with high-throughput screening pipelines. For example, leading biotech players are leveraging cancer organoids to identify biomarkers and accelerate oncology drug development, while liver and kidney organoids are being integrated into toxicity studies to enhance drug safety assessments.

Beyond pharma and biotech, academic and research institutions represent another strong end-user group, using organoids to unravel disease mechanisms, study genetic disorders, and advance regenerative medicine. Universities and research consortia have been at the forefront of innovation, pioneering protocols for brain, intestinal, and retinal organoids that are now widely adopted across the industry. Meanwhile, hospitals and clinical centres are beginning to apply organoid technology for personalized medicine—particularly in oncology, where patient-derived tumour organoids are used to predict treatment responses and guide therapy decisions. The Others category, which includes contract research organizations (CROs), government bodies, and regulatory agencies, is also expanding as stakeholders seek standardized platforms for safety validation, quality assurance, and policy development.

In comparison, pharmaceutical and biotechnology companies dominate today because of their immediate need for predictive and scalable models in R&D pipelines. However, the growing contributions from academia, hospitals, and regulatory stakeholders highlight the collaborative ecosystem forming around organoid technologies. Together, these end users are ensuring that organoids not only accelerate drug development but also extend into clinical care and public health, reinforcing their role as a cornerstone of modern biomedical research and innovation.

Global Organoid Market, By End USer (USD million)

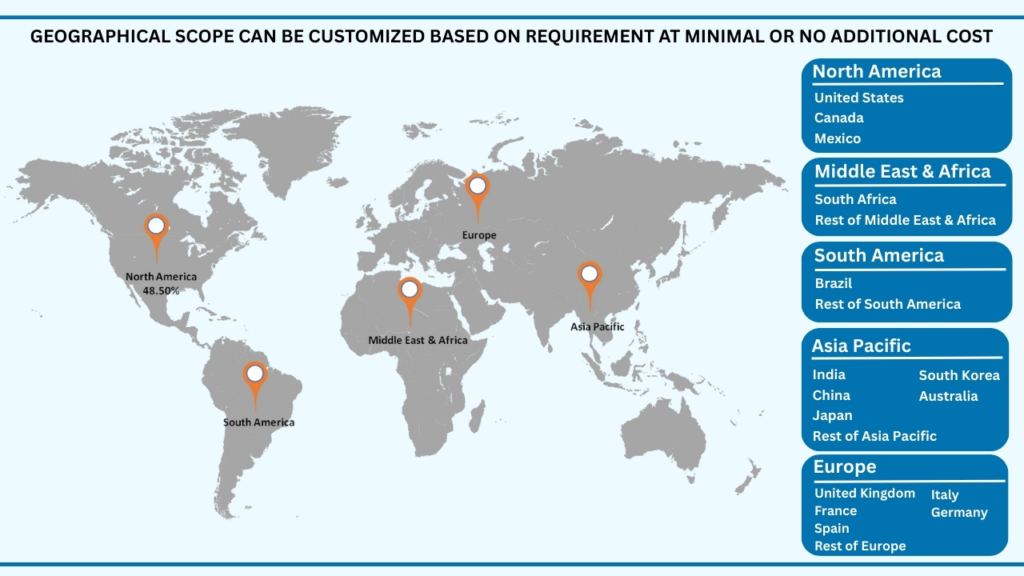

Global Organoid Market by Region Insights:

North America segment accounted for market share of share 48.50% in 2024 in the global organoid market.

The North America region leads the global organoid market, accounting for 48.50% of the share in 2024. Revenues from this region are projected to reach USD 10,809.58 million during the forecast period from 2025 to 2032, expanding at a CAGR of 23.45%. North America’s leadership is supported by strong investments in biomedical research, a well-established pharmaceutical and biotechnology sector, and extensive adoption of advanced preclinical testing models. The U.S. in particular has seen rapid uptake of organoid platforms, with both academic centres and private companies leveraging them for oncology, neurology, and regenerative medicine research. Federal funding initiatives, combined with collaborations between universities and industry players, are further driving innovation. For example, several U.S.-based consortia are actively building patient-derived organoid biobanks to accelerate precision medicine programs, while biotech firms are using organoids to refine drug discovery pipelines and reduce reliance on animal testing.

Beyond North America, Europe represents another major hub for organoid research, benefiting from strong regulatory support for animal-free testing models and collaborative networks across academic and industry institutions. Countries like Germany, the Netherlands, and the U.K. are leading the charge, with specialized centres focusing on intestinal, liver, and brain organoids for both fundamental research and translational applications. Meanwhile, the Asia Pacific region is emerging as the fastest-growing market, fuelled by rising R&D spending, expanding biotech industries, and increasing government initiatives in countries such as Japan, China, and South Korea. In contrast, Latin America (LATAM) and the Middle East & Africa (MEA) currently hold smaller shares but are showing steady progress as research infrastructure develops and international collaborations expand.

In comparison, North America dominates today because of its advanced research ecosystem, strong financial backing, and robust pharmaceutical pipelines. However, the rapid acceleration of organoid adoption in Europe and Asia Pacific signals a broader global shift toward integrating organoids in drug discovery, disease modelling, and clinical care. Together, these regions are shaping a dynamic and interconnected market landscape, ensuring that organoid technologies continue to expand their role in advancing biomedical research and patient-cantered innovation worldwide.

Global Organoid Market, By Region (USD million)

Major Companies and Competitive Landscape

The global organoid market is evolving rapidly, marked by intense competition and continuous innovation from both established biotechnology leaders and emerging players. Companies in this space are actively engaging in strategic collaborations, licensing agreements, research partnerships, and mergers & acquisitions to expand their market presence and technological capabilities. A major focus lies on enhancing organoid development protocols, standardizing culture conditions, improving reproducibility, and scaling up production for clinical and commercial applications. These initiatives aim to accelerate drug discovery, optimize toxicology screening, reduce reliance on animal testing, and support personalized medicine solutions. Key players profiled in the global organoid market report include:

- Thermo Fisher Scientific Inc.

- Corning Incorporated

- Merck KGaA

- STEMCELL Technologies Inc.

- Lonza Group AG

- Sartorius AG

- Greiner Bio-One International GmbH

- Charles River Laboratories International Inc.

- Bio-Techne

- Molecular Devices (Danaher)

- Hubrecht Organoid Technology (HUB)

- Crown Bioscience Inc. (JSR)

- DefiniGEN Ltd.

- Cellesce Ltd.

- InSphero AG

- MIMETAS BV

- BioIVT LLC

- 3Dnamics Inc.

- Organoid Therapeutics

- QGel SA

- 3D Biotek LLC

- OcellO B.V.

- Emulate Inc.

- TissUse GmbH

- AIVITA Biomedical, Inc.

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 5,096.98 Million |

| CAGR (2024–2032) | 23.38% |

| Revenue forecast to 2033 | USD 22,183.29 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Organoid Type, By Product Type, By Source Type, By Storage Conditions, By Disease Area, By Method, By Technology, By Application Type, By End User and By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, UAE, South Africa, Turkey, Rest of MEA |

| Key companies profiled | Thermo Fisher Scientific Inc., Corning Incorporated, Merck KGaA, STEMCELL Technologies Inc., Lonza Group AG, Sartorius AG, Greiner Bio-One International GmbH, Charles River Laboratories International Inc., Bio-Techne, Molecular Devices (Danaher), Hubrecht Organoid Technology (HUB), Crown Bioscience Inc. (JSR), DefiniGEN Ltd., Cellesce Ltd., InSphero AG, MIMETAS BV, BioIVT LLC, 3Dnamics Inc., Organoid Therapeutics, QGel SA, 3D Biotek LLC, OcellO B.V., Emulate Inc., TissUse GmbH, and AIVITA Biomedical, Inc. |

| Customization scope | 10 hours of free customization and expert consultation |

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of global organoids market

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1.Primary

2.1.2.Secondary

2.1.3.Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1.Market value

2.3.2.Market volume

2.3.3.Exchange rate

2.3.4.Price

2.3.5.Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2025-2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10. Formulation & manufacturing

4.11. Distribution & retail

4.12. Import-export analysis

4.13. Brand comparative analysis

4.14. Technological advancements

4.15. Porter’s five force

4.15.1. Threat of new entrants

4.15.1.1. Capital requirment

4.15.1.2. Product knowledge

4.15.1.3. Technical knowledge

4.15.1.4. Customer relation

4.15.1.5. Access to appliation and technology

4.15.2. Threat of substitutes

4.15.2.1. Cost

4.15.2.2. Performance

4.15.2.3. Availability

4.15.2.4. Technical knowledge

4.15.2.5. Durability

4.15.3. Bargainning power of buyers

4.15.3.1. Numbers of buyers relative to suppliers

4.15.3.2. Product differentiation

4.15.3.3. Threat of forward integration

4.15.3.4. Buyers volume

4.15.4. Bargainning power of suppliers

4.15.4.1. Suppliers concentration

4.15.4.2. Buyers switching cost to other suppliers

4.15.4.3. Threat of backward integration

4.15.5. Bargainning power of suppliers

4.15.5.1. Industry concentration

4.15.5.2. Industry growth rate

4.15.5.3. Product differentiation

4.15.6. Patent analysis

4.16. Patent quality and strength

4.17. Regulation coverage

4.18. Pricing analysis

4.19. Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1.Rising use of patient-derived organoids (PDOs) for translational cancer research and

precision oncology

5.1.2.Improved 3D culture media, ECM substitutes, and bioreactors boosting viability and

throughput

5.1.3.Pharma/biotech partnerships to replace or triage animal models in efficacy and

toxicology screens

5.2. Restraints

5.2.1.Batch-to-batch variability and lack of reproducibility across labs and vendors

5.2.2.High costs for specialized media, matrices, and long culture cycles

5.3. Opportunities

5.3.1.High-throughput screening with automated handling, miniaturization, and image-based

analytics

5.3.2.Co-culture and immune-organoid platforms for immuno-oncology and infectious disease

studies

5.3.3.Personalized medicine workflows—patient stratification, companion diagnostics, and

therapy selection

5.4. Threat

5.4.1.Regulatory uncertainty on validation, data requirements, and acceptance in decision-

making

5.4.2.Intellectual Property constraints on media, matrices, and Patient-Derived Organoids

derivation methods limiting broad adoption

5.4.3.Supply chain risks for critical reagents and reliance on animal-derived Extracellular

Matrix during transition to synthetics

Chapter 6. Global Organoids Market By Organoid Type Insights & Trends, Revenue

(USD Million)

6.1. Organoid Type Dynamics & Market Share, 2025–2032

6.1.1.Brain Organoids

6.1.2.Heart Organoids

6.1.3.Intestinal Organoids

6.1.4.Kidney Organoids

6.1.5.Liver Organoids

6.1.6.Lung Organoids

6.1.7.Pancreatic Organoids

6.1.8.Stomach Organoids

6.1.9.Neuro Organoids

6.1.10. Colorectal Organoids

6.1.11. Others(Prostrate, Retina, Skin, Breast)

Chapter 7. Global Organoids Market By Product Type Insights & Trends, Revenue (USD

Million)

7.1. Product Type Dynamics & Market Share, 2025-2032

7.1.1.Ready-to-Use Organoid Products

7.1.2.Personalized Organoid Models

Chapter 8. Global Organoids Market By Source Type Insights & Trends, Revenue (USD

Million)

8.1. Source Type Dynamics & Market Share, 2025-2032

8.1.1.Induced Pluripotent Stem Cells (iPSCs)

8.1.2.Embryonic Stem Cells (ESCs)

8.1.3.Adult Stem Cells

Chapter 9. Global Organoids Market By Storage Conditions Insights & Trends, Revenue (USD

Million)

9.1. Storage Conditions Dynamics & Market Share, 2025-2032

9.1.1.Shelf-stable Organoids

9.1.2.Cryopreserved Organoids

Chapter 10. Global Organoids Market By Disease Area Insights & Trends, Revenue (USD Million)

10.1. Disease Area Dynamics & Market Share, 2025-2032

10.1.1. Oncology

10.1.2. Liver Diseases

10.1.3. Gastrointestinal Diseases

10.1.4. Cardiovascular Diseases

10.1.5. Infectious Diseases

10.1.6. Neurological Disorders

10.1.7. Renal Diseases

10.1.8. Genetic Diseases

10.1.9. Ophthalmic Diseases

10.1.10. Other (endocrine diseases)

Chapter 11. Global Organoids Market By Method Insights & Trends, Revenue (USD Million)

11.1. Method Dynamics & Market Share, 2025-2032

11.1.1. General Submerged Method

11.1.2. Crypt Organoid Culture Techniques

11.1.3. Air Liquid Interface (ALI) Method

11.1.4. Clonal Organoids from Lgr5+ Cells

11.1.5. Brain and Retina Organoid Formation Protocol

Chapter 12. Global Organoids Market By Technology Insights & Trends, Revenue (USD

Million)

12.1. Technology Dynamics & Market Share, 2025-2032

12.1.1. 3D Bioprinting

12.1.2. Hydrogel-Based Technology

12.1.3. Scaffold-Based Technology

12.1.4. Scaffold-Free (Self-Assembly) Techniques

12.1.5. Magnetic Levitation

12.1.6. Microfluidic Technology (Organ-on-Chip)

12.1.7. Centrifugal Forced Aggregation

12.1.8. Rotating Wall Vessel Bioreactors

12.1.9. Hanging Drop Culture

Chapter 13. Global Organoids Market By Application Type Insights & Trends, Revenue

(USD Million)

13.1. Application Type Dynamics & Market Share, 2025-2032

13.1.1. Drug Discovery & Development

13.1.2. Disease Modelling

13.1.3. Toxicity Testing

13.1.4. Personalized Medicine & Precision neurology

13.1.5. Development Biology

13.1.6. Biomarker Discovery

13.1.7. Other (biomedical research)

Chapter 14. Global Organoids Market By End User Insights & Trends, Revenue (USD

Million)

14.1.1. Pharmaceutical & Biotechnology Companies

14.1.2. Academic & Research Institutions

14.1.3. Hospitals

14.1.4. Others (CROs, government, regulators)

Chapter 15. Global Enzymatic DNA Synthesis Market Regional Outlook

15.1. Global Enzymatic DNA Synthesis Market Share By Region, 2025-2032

15.2. North America

15.2.1. Market By Organoid Type, Market Estimates and Forecast, USD Million

15.2.1.1. Brain Organoids

15.2.1.2. Heart Organoids

15.2.1.3. Intestinal Organoids

15.2.1.4. Kidney Organoids

15.2.1.5. Liver Organoids

15.2.1.6. Lung Organoids

15.2.1.7. Pancreatic Organoids

15.2.1.8. Stomach Organoids

15.2.1.9. Neuro Organoids

15.2.1.10.Colorectal Organoids

15.2.1.11.Others(Prostrate, Retina, Skin, Breast)

15.2.2.Market By Product Type, Market Estimates and Forecast, USD Million

15.2.2.1. Ready-to-Use Organoid Products

15.2.2.2. Personalized Organoid Models

15.2.3.Market By Source Type, Market Estimates and Forecast, USD Million

15.2.3.1. Induced Pluripotent Stem Cells (iPSCs)

15.2.3.2. Embryonic Stem Cells (ESCs)

15.2.3.3. Adult Stem Cells

15.2.4.Market By Storage Conditions, Market Estimates and Forecast, USD Million

15.2.4.1. Shelf-stable Organoids

15.2.4.2. Cryopreserved Organoids

15.2.5.Market By Disease Area, Market Estimates and Forecast, USD Million

15.2.5.1. Oncology

15.2.5.2. Liver Diseases

15.2.5.3. Gastrointestinal Diseases

15.2.5.4. Cardiovascular Diseases

15.2.5.5. Infectious Diseases

15.2.5.6. Neurological Disorders

15.2.5.7. Renal Diseases

15.2.5.8. Genetic Diseases

15.2.5.9. Ophthalmic Diseases

15.2.5.10. Other (endocrine diseases)

15.2.6.Market By Method, Market Estimates and Forecast, USD Million

15.2.6.1. General Submerged Method

15.2.6.2. Crypt Organoid Culture Techniques

15.2.6.3. Air Liquid Interface (ALI) Method

15.2.6.4. Clonal Organoids from Lgr5+ Cells

15.2.6.5. Brain and Retina Organoid Formation Protocol

15.2.7.Market By Technology, Market Estimates and Forecast, USD Million

15.2.7.1. 3D Bioprinting

15.2.7.2. Hydrogel-Based Technology

15.2.7.3. Scaffold-Based Technology

15.2.7.4. Scaffold-Free (Self-Assembly) Techniques

15.2.7.5. Magnetic Levitation

15.2.7.6. Microfluidic Technology (Organ-on-Chip)

15.2.7.7. Centrifugal Forced Aggregation

15.2.7.8. Rotating Wall Vessel Bioreactors

15.2.7.9. Hanging Drop Culture

15.2.8.Market By Application Type, Market Estimates and Forecast, USD Million

15.2.8.1. Drug Discovery & Development

15.2.8.2. Disease Modelling

15.2.8.3. Toxicity Testing

15.2.8.4. Personalized Medicine & Precision neurology

15.2.8.5. Development Biology

15.2.8.6. Biomarker Discovery

15.2.8.7. Other (biomedical research))

15.2.9.Market By End User, Market Estimates and Forecast, USD Million

15.2.9.1. Pharmaceutical & Biotechnology Companies

15.2.9.2. Academic & Research Institutions

15.2.9.3. Hospitals

15.2.9.4. Others (CROs, government, regulators)

15.2.10. Market By Country, Market Estimates and Forecast, USD Million

15.2.10.1.US

15.2.10.2.Canada

15.2.10.3.Mexico

15.3. Europe

15.3.1.Market By Organiod Type, Market Estimates and Forecast, USD Million

15.3.1.1. Brain Organoids

15.3.1.2. Heart Organoids

15.3.1.3. Intestinal Organoids

15.3.1.4. Kidney Organoids

15.3.1.5. Liver Organoids

15.3.1.6. Lung Organoids

15.3.1.7. Pancreatic Organoids

15.3.1.8. Stomach Organoids

15.3.1.9. Neuro Organoids

15.3.1.10.Colorectal Organoids

15.3.1.11.Others(Prostrate, Retina, Skin, Breast)

15.3.2.Market By Product Type, Market Estimates and Forecast, USD Million

15.3.2.1. Ready-to-Use Organoid Products

15.3.2.2. Personalized Organoid Models

15.3.3.Market By Source Type, Market Estimates and Forecast, USD Million,

15.3.3.1. Induced Pluripotent Stem Cells (iPSCs)

15.3.3.2. Embryonic Stem Cells (ESCs)

15.3.3.3. Adult Stem Cells

15.3.4.Market By Storage Conditions, Market Estimates and Forecast, USD Million

15.3.4.1. Shelf-stable Organoids

15.3.4.2. Cryopreserved Organoids

15.3.5.Market By Disease Area, Market Estimates and Forecast, USD Million,

15.3.5.1. Oncology

15.3.5.2. Liver Diseases

15.3.5.3. Gastrointestinal Diseases

15.3.5.4. Cardiovascular Diseases

15.3.5.5. Infectious Diseases

15.3.5.6. Neurological Disorders

15.3.5.7. Renal Diseases

15.3.5.8. Genetic Diseases

15.3.5.9. Ophthalmic Diseases

15.3.5.10.Other (endocrine diseases)

15.3.6.Market By Method, Market Estimates and Forecast, USD Million

15.3.6.1. General Submerged Method

15.3.6.2. Crypt Organoid Culture Techniques

15.3.6.3. Air Liquid Interface (ALI) Method

15.3.6.4. Clonal Organoids from Lgr5+ Cells

15.3.6.5. Brain and Retina Organoid Formation Protocol

15.3.7.Market By Technology, Market Estimates and Forecast, USD Million

15.3.7.1. 3D Bioprinting

15.3.7.2. Hydrogel-Based Technology

15.3.7.3. Scaffold-Based Technology

15.3.7.4. Scaffold-Free (Self-Assembly) Techniques

15.3.7.5. Magnetic Levitation

15.3.7.6. Microfluidic Technology (Organ-on-Chip)

15.3.7.7. Centrifugal Forced Aggregation

15.3.7.8. Rotating Wall Vessel Bioreactors

15.3.7.9. Hanging Drop Culture

15.3.8.Market By Application Type, Market Estimates and Forecast, USD Million

15.3.8.1. Drug Discovery & Development

15.3.8.2. Disease Modelling

15.3.8.3. Toxicity Testing

15.3.8.4. Personalized Medicine & Precision neurology

15.3.8.5. Development Biology

15.3.8.6. Biomarker Discovery

15.3.8.7. Other (biomedical research)

15.3.9.Market By End User, Market Estimates and Forecast, USD Million

15.3.9.1. Pharmaceutical & Biotechnology Companies

15.3.9.2. Academic & Research Institutions

15.3.9.3. Hospitals

15.3.9.4. Others (CROs, government, regulators)

15.3.10. Market By Country, Market Estimates and Forecast, USD Million

15.3.10.1.Germany

15.3.10.2.France

15.3.10.3.U.K

15.3.10.4.Italy

15.3.10.5.Spain

15.3.10.6.Benelux

15.3.10.7.Russia

15.3.10.8.Finland

15.3.10.9.Sweden

15.3.10.10. Rest Of Europe

15.4. Asia-Pacific

15.4.1.Market By ProductType, Market Estimates and Forecast, USD Million

15.4.1.1. Brain Organoids

15.4.1.2. Heart Organoids

15.4.1.3. Intestinal Organoids

15.4.1.4. Kidney Organoids

15.4.1.5. Liver Organoids

15.4.1.6. Lung Organoids

15.4.1.7. Pancreatic Organoids

15.4.1.8. Stomach Organoids

15.4.1.9. Neuro Organoids

15.4.1.10.Colorectal Organoids

15.4.1.11.Others(Prostrate, Retina, Skin, Breast)

15.4.2.Market By Product Type, Market Estimates and Forecast, USD Million

15.4.2.1. Ready-to-Use Organoid Products

15.4.2.2. Personalized Organoid Models

15.4.3.Market By Source Type, Market Estimates and Forecast, USD Million

15.4.3.1. Induced Pluripotent Stem Cells (iPSCs)

15.4.3.2. Embryonic Stem Cells (ESCs)

15.4.3.3. Adult Stem Cells

15.4.4.Market By Storage Conditions, Market Estimates and Forecast, USD Million

15.4.4.1. Shelf-stable Organoids

15.4.4.2. Cryopreserved Organoids

15.4.5.Market By Disease Area, Market Estimates and Forecast, USD Million

15.4.5.1. Oncology

15.4.5.2. Liver Diseases

15.4.5.3. Gastrointestinal Diseases

15.4.5.4. Cardiovascular Diseases

15.4.5.5. Infectious Diseases

15.4.5.6. Neurological Disorders

15.4.5.7. Renal Diseases

15.4.5.8. Genetic Diseases

15.4.5.9. Ophthalmic Diseases

15.4.5.10.Other (endocrine diseases)

15.4.6.Market By Method, Market Estimates and Forecast, USD Million

15.4.6.1. General Submerged Method

15.4.6.2. Crypt Organoid Culture Techniques

15.4.6.3. Air Liquid Interface (ALI) Method

15.4.6.4. Clonal Organoids from Lgr5+ Cells

15.4.6.5. Brain and Retina Organoid Formation Protocol

15.4.7.Market By Technology, Market Estimates and Forecast, USD Million

15.4.7.1. 3D Bioprinting

15.4.7.2. Hydrogel-Based Technology

15.4.7.3. Scaffold-Based Technology

15.4.7.4. Scaffold-Free (Self-Assembly) Techniques

15.4.7.5. Magnetic Levitation

15.4.7.6. Microfluidic Technology (Organ-on-Chip)

15.4.7.7. Centrifugal Forced Aggregation

15.4.7.8. Rotating Wall Vessel Bioreactors

15.4.7.9. Hanging Drop Culture

15.4.8.Market By Application Type, Market Estimates and Forecast, USD Million

15.4.8.1. Drug Discovery & Development

15.4.8.2. Disease Modelling

15.4.8.3. Toxicity Testing

15.4.8.4. Personalized Medicine & Precision neurology

15.4.8.5. Development Biology

15.4.8.6. Biomarker Discovery

15.4.8.7. Other (biomedical research)

15.4.9.Market By End User, Market Estimates and Forecast, USD Million

15.4.9.1. Pharmaceutical & Biotechnology Companies

15.4.9.2. Academic & Research Institutions

15.4.9.3. Hospitals

15.4.9.4. Others (CROs, government, regulators)

15.4.10. Market By Country, Market Estimates and Forecast, USD Million

15.4.10.1.China

15.4.10.2.India

15.4.10.3.Japan

15.4.10.4.South Korea

15.4.10.5.Indonesia

15.4.10.6.Thailand

15.4.10.7.Vietnam

15.4.10.8.Australia

15.4.10.9.New Zeland

15.4.10.10. Rest of APAC

15.5. Latin America

15.5.1.Market By Organoid Type, Market Estimates and Forecast, USD Million

15.5.1.1. Brain Organoids

15.5.1.2. Heart Organoids

15.5.1.3. Intestinal Organoids

15.5.1.4. Kidney Organoids

15.5.1.5. Liver Organoids

15.5.1.6. Lung Organoids

15.5.1.7. Pancreatic Organoids

15.5.1.8. Stomach Organoids

15.5.1.9. Neuro Organoids

15.5.1.10.Colorectal Organoids

15.5.1.11.Others(Prostrate, Retina, Skin, Breast)

15.5.2.Market By Product Type, Market Estimates and Forecast, USD Million

15.5.2.1. Ready-to-Use Organoid Products

15.5.2.2. Personalized Organoid Models

15.5.3.Market By Source Type, Market Estimates and Forecast, USD Million

15.5.3.1. Induced Pluripotent Stem Cells (iPSCs)

15.5.3.2. Embryonic Stem Cells (ESCs)

15.5.3.3. Adult Stem Cells

15.5.4.Market By Storage Conditions, Market Estimates and Forecast, USD Million

15.5.4.1. Shelf-stable Organoids

15.5.4.2. Cryopreserved Organoids

15.5.5.Market By Disease Area, Market Estimates and Forecast, USD Million

15.5.5.1. Oncology

15.5.5.2. Liver Diseases

15.5.5.3. Gastrointestinal Diseases

15.5.5.4. Cardiovascular Diseases

15.5.5.5. Infectious Diseases

15.5.5.6. Neurological Disorders

15.5.5.7. Renal Diseases

15.5.5.8. Genetic Diseases

15.5.5.9. Ophthalmic Diseases

15.5.5.10.Other (endocrine diseases)

15.5.6.Market By Method, Market Estimates and Forecast, USD Million

15.5.6.1. General Submerged Method

15.5.6.2. Crypt Organoid Culture Techniques

15.5.6.3. Air Liquid Interface (ALI) Method

15.5.6.4. Clonal Organoids from Lgr5+ Cells

15.5.6.5.Brain and Retina Organoid Formation Protocol

15.5.7.Market By Technology, Market Estimates and Forecast, USD Million

15.5.7.1. 3D Bioprinting

15.5.7.2. Hydrogel-Based Technology

15.5.7.3. Scaffold-Based Technology

15.5.7.4. Scaffold-Free (Self-Assembly) Techniques

15.5.7.5. Magnetic Levitation

15.5.7.6. Microfluidic Technology (Organ-on-Chip)

15.5.7.7. Centrifugal Forced Aggregation

15.5.7.8. Rotating Wall Vessel Bioreactors

15.5.7.9. Hanging Drop Culture

15.5.8.Market By Application Type, Market Estimates and Forecast, USD Million

15.5.8.1. Drug Discovery & Development

15.5.8.2. Disease Modelling

15.5.8.3. Toxicity Testing

15.5.8.4. Personalized Medicine & Precision neurology

15.5.8.5. Development Biology

15.5.8.6. Biomarker Discovery

15.5.8.7. Other (biomedical research)

15.5.9.Market By End User, Market Estimates and Forecast, USD Million

15.5.9.1. Pharmaceutical & Biotechnology Companies

15.5.9.2. Academic & Research Institutions

15.5.9.3. Hospitals

15.5.9.4. Others (CROs, government, regulators)

15.5.10.Market By Country, Market Estimates and Forecast, USD Million

15.5.10.1. Brazil

15.5.10.2. Rest of LATAM

15.6. Middle East & Africa

15.6.1.Market By Organoid Type, Market Estimates and Forecast, USD Million

15.6.1.1. Brain Organoids

15.6.1.2. Heart Organoids

15.6.1.3. Intestinal Organoids

15.6.1.4. Kidney Organoids

15.6.1.5. Liver Organoids

15.6.1.6. Lung Organoids

15.6.1.7. Pancreatic Organoids

15.6.1.8. Stomach Organoids

15.6.1.9. Neuro Organoids

15.6.1.10.Colorectal Organoids

15.6.1.11.Others(Prostrate, Retina, Skin, Breast)

15.6.2.Market By Product Type, Market Estimates and Forecast, USD Million

15.6.2.1. Ready-to-Use Organoid Products

15.6.2.2. Personalized Organoid Models

15.6.3.Market By Source Type, Market Estimates and Forecast, USD Million

15.6.3.1. Induced Pluripotent Stem Cells (iPSCs)

15.6.3.2. Embryonic Stem Cells (ESCs)

15.6.3.3. Adult Stem Cells

15.6.4.Market By Storage Conditions, Market Estimates and Forecast, USD Million

15.6.4.1. Shelf-stable Organoids

15.6.4.2. Cryopreserved Organoids

15.6.5.Market By Disease Area, Market Estimates and Forecast, USD Million

15.6.5.1. Oncology

15.6.5.2. Liver Diseases

15.6.5.3. Gastrointestinal Diseases

15.6.5.4. Cardiovascular Diseases

15.6.5.5. Infectious Diseases

15.6.5.6. Neurological Disorders

15.6.5.7. Renal Diseases

15.6.5.8. Genetic Diseases

15.6.5.9. Ophthalmic Diseases

15.6.5.10.Other (endocrine diseases)

15.6.6.Market By Method, Market Estimates and Forecast, USD Million

15.6.6.1. General Submerged Method

15.6.6.2. Crypt Organoid Culture Techniques

15.6.6.3. Air Liquid Interface (ALI) Method

15.6.6.4. Clonal Organoids from Lgr5+ Cells

15.6.6.5. Brain and Retina Organoid Formation Protocol

15.6.7.Market By Technology, Market Estimates and Forecast, USD Million

15.6.7.1. 3D Bioprinting

15.6.7.2. Hydrogel-Based Technology

15.6.7.3. Scaffold-Based Technology

15.6.7.4. Scaffold-Free (Self-Assembly) Techniques

15.6.7.5. Magnetic Levitation

15.6.7.6. Microfluidic Technology (Organ-on-Chip)

15.6.7.7. Centrifugal Forced Aggregation

15.6.7.8. Rotating Wall Vessel Bioreactors

15.6.7.9. Hanging Drop Culture

15.6.8.Market By Application Type, Market Estimates and Forecast, USD Million

15.6.8.1. Drug Discovery & Development

15.6.8.2. Disease Modelling

15.6.8.3. Toxicity Testing

15.6.8.4. Personalized Medicine & Precision neurology

15.6.8.5. Development Biology

15.6.8.6. Biomarker Discovery

15.6.8.7. Other (biomedical research)

15.6.9.Market By End User, Market Estimates and Forecast, USD Million

15.6.9.1. Pharmaceutical & Biotechnology Companies

15.6.9.2. Academic & Research Institutions

15.6.9.3. Hospitals

15.6.9.4. Others (CROs, government, regulators)

15.6.10. Market By Country, Market Estimates and Forecast, USD Million

15.6.10.1.Saudi Arabia

15.6.10.2.UAE

15.6.10.3.South Africa

15.6.10.4.Turkey

15.6.10.5.Rest of MEA

Chapter 16. Competitive Landscape

16.1. Market Revenue Share By Manufacturers

16.2. Mergers & Acquisitions

16.3. Competitor’s Positioning

16.4. Strategy Benchmarking

16.5. Vendor Landscape

16.6. Distributors

16.6.1.North America

16.6.2.Europe

16.6.3.Asia Pacific

16.6.4.Middle East & Africa

16.6.5.Latin America

16.7. Others

Chapter 17. Company Profiles

17.1. Thermo Fisher Scientific Inc.

17.1.1. Company Overview

17.1.2. Product & Service Offerings

17.1.3. Strategic Initiatives

17.1.4. Financials

17.1.5. Research Insights

17.2. Corning Incorporated

17.2.1. Company Overview

17.2.2. Product & Service Offerings

17.2.3. Strategic Initiatives

17.2.4. Financials

17.2.5. Research Insights

17.3. Merck KGaA

17.3.1. Company Overview

17.3.2. Product & Service Offerings

17.3.3. Strategic Initiatives

17.3.4. Financials

17.3.5. Research Insights

17.4. BioIVT

17.4.1. Company Overview

17.4.2. Product & Service Offerings

17.4.3. Strategic Initiatives

17.4.4. Financials

17.4.5. Research Insights

17.5. HUB Organoids BV

17.5.1. Company Overview

17.5.2. Product & Service Offerings

17.5.3. Strategic Initiatives

17.5.4. Financials

17.5.5. Research Insights

17.6. STEMCELL Technologies

17.6.1. Company Overview

17.6.2. Product & Service Offerings

17.6.3. Strategic Initiatives

17.6.4. Financials

17.6.5. Research Insights

17.7. InSphero

17.7.1. Company Overview

17.7.2. Product & Service Offerings

17.7.3. Strategic Initiatives

17.7.4. Financials

17.7.5. Research Insights

17.8. BICO

17.8.1. Company Overview

17.8.2. Product & Service Offerings

17.8.3. Strategic Initiatives

17.8.4. Financials

17.8.5. Conclusion

17.9. BeCytes Biotechnologies SL

17.9.1. Company Overview

17.9.2. Product & Service Offerings

17.9.3. Strategic Initiatives

17.9.4. Financials

17.9.5. Conclusion

17.10. GBA Group

17.10.1. Company Overview

17.10.2. Product & Service Offerings

17.10.3. Strategic Initiatives

17.10.4. Financials

17.10.5. Conclusion

17.11. Kirstall Ltd.

17.11.1. Company Overview

17.11.2. Product & Service Offerings

17.11.3. Strategic Initiatives

17.11.4. Financials

17.11.5. Conclusion

17.12. MIMETAS BV

17.12.1. Company Overview

17.12.2. Product & Service Offerings

17.12.3. Strategic Initiatives

17.12.4. Financials

17.12.5. Conclusion

17.13. Neuromics

17.13.1. Company Overview

17.13.2. Product & Service Offerings

17.13.3. Strategic Initiatives

17.13.4. Financials

17.13.5. Conclusion

17.14. ACROBiosystems

17.14.1. Company Overview

17.14.2. Product & Service Offerings

17.14.3. Strategic Initiatives

17.14.4. Financials

17.14.5. Conclusion

17.15. BioPredic International

17.15.1. Company Overview

17.15.2. Product & Service Offerings

17.15.3. Strategic Initiatives

17.15.4. Financials

17.15.5. Conclusion

17.16. CN Bio Innovations Ltd.

17.16.1. Company Overview

17.16.2. Product & Service Offerings

17.16.3. Strategic Initiatives

17.16.4. Financials

17.16.5. Conclusion

17.17. Emulate, Inc.

17.17.1. Company Overview

17.17.2. Product & Service Offerings

17.17.3. Strategic Initiatives

17.17.4. Financials

17.17.5. Conclusion

17.18. Pandorum Technologies Pvt. Ltd.

17.18.1. Company Overview

17.18.2. Product & Service Offerings

17.18.3. Strategic Initiatives

17.18.4. Financials

17.18.5. Conclusion

17.19. DefiniGEN Limited

17.19.1. Company Overview

17.19.2. Product & Service Offerings

17.19.3. Strategic Initiatives

17.19.4. Financials

17.19.5. Conclusion

17.20. 3Dnamics Inc.

17.20.1. Company Overview

17.20.2. Product & Service Offerings

17.20.3. Strategic Initiatives

17.20.4. Financials

17.20.5. Conclusion

17.21. Organovo Holdings, Inc.

17.21.1. Company Overview

17.21.2. Product & Service Offerings

17.21.3. Strategic Initiatives

17.21.4. Financials

17.21.5. Conclusion

17.22. Newcells Biotech

17.22.1. Company Overview

17.22.2. Product & Service Offerings

17.22.3. Strategic Initiatives

17.22.4. Financials

17.22.5. Conclusion

17.23. Cellesce Ltd.

17.23.1. Company Overview

17.23.2. Product & Service Offerings

17.23.3. Strategic Initiatives

17.23.4. Financials

17.23.5. Conclusion

17.24. CelVivo ApS

17.24.1. Company Overview

17.24.2. Product & Service Offerings

17.24.3. Strategic Initiatives

17.24.4. Financials

17.24.5. Conclusion

17.25. ATCC (American Type Culture Collection)

17.25.1. Company Overview

17.25.2. Product & Service Offerings

17.25.3. Strategic Initiatives

17.25.4. Financials

17.25.5. Conclusion

Global Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP. has segmented global Organoid market on the basis of By Organoid Type, By Product Type, Source Type, By Storage Conditions, By Disease Area, By Method, By Technology, By Application Type, By End User and by region for 2019 to 2032.

- Global Organoid Type Outlook (Revenue, USD Million; 2025-2032)

-

- Brain Organoids

-

- Heart Organoids

-

- Intestinal Organoids

-

- Kidney Organoids

-

- Liver Organoids

-

- Lung Organoids

-

- Pancreatic Organoids

-

- Stomach organoids

-

- Neuro organoids

-

- Colorectal organoids

-

- Others (Prostrate, Retina, Skin, Breast)

- Global Product Type Outlook (Revenue, USD Million; 2025-2032)

-

- Ready-to-Use Organoid Products

-

- Personalized Organoid Models

- Global Source Type Outlook (Revenue, USD Million; 2025-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Global Storage Conditions Outlook (Revenue, USD Million; 2025-2032)

-

- Shelf-stable Organoids

-

- Cryopreserved Organoids

- Global Disease Area Outlook (Revenue, USD Million; 2025-2032)

-

- Oncology

-

- Liver Diseases

-

- Gastrointestinal Diseases

-

- Cardiovascular Diseases

-

- Infectious Diseases

-

- Neurological Disorders

-

- Renal Diseases

-

- Genetic Diseases

-

- Ophthalmic Diseases

-

- Other (endocrine diseases)

- Global Method Outlook (Revenue, USD Million; 2025-2032)

-

- General Submerged Method

-

- Crypt Organoid Culture Techniques

-

- Air Liquid Interface (ALI) Method

-

- Clonal Organoids from Lgr5+ Cells

-

- Brain and Retina Organoid Formation Protocol

- Global Technology Outlook (Revenue, USD Million; 2025-2032)

-

- 3D Bioprinting

-

- Hydrogel-Based Technology

-

- Scaffold-Based Technology

-

- Scaffold-Free (Self-Assembly) Techniques

-

- Magnetic Levitation

-

- Microfluidic Technology (Organ-on-Chip)

-

- Centrifugal Forced Aggregation

-

- Rotating Wall Vessel Bioreactors

-

- Hanging Drop Culture

- Global Application Type Outlook (Revenue, USD Million; 2025-2032)

-

- Drug Discovery & Development

-

- Disease Modelling

-

- Toxicity Testing

-

- Personalized Medicine & Precision neurology

-

- Development Biology

-

- Biomarker Discovery

-

- Other (biomedical research)

- Global Application Type Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical & Biotechnology Companies

-

- Academic & Research Institutions

-

- Hospitals

-

- Others (CROs, government, regulators)

- North America

- North America Organoid Type Outlook (Revenue, USD Million; 2025-2032)

-

- Brain Organoids

-

- Heart Organoids

-

- Intestinal Organoids

-

- Kidney Organoids

-

- Liver Organoids

-

- Lung Organoids

-

- Pancreatic Organoids

-

- Stomach organoids

-

- Neuro organoids

-

- Colorectal organoids

-

- Others (Prostrate, Retina, Skin, Breast)

- North America Product Type Outlook (Revenue, USD Million; 2025-2032)

-

- Ready-to-Use Organoid Products

-

- Personalized Organoid Models

- North America Source Type Outlook (Revenue, USD Million; 2025-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- North America Storage Conditions Outlook (Revenue, USD Million; 2025-2032)

-

- Shelf-stable Organoids

-

- Cryopreserved Organoids

- North America Disease Area Outlook (Revenue, USD Million; 2025-2032)

-

- Oncology

-

- Liver Diseases

-

- Gastrointestinal Diseases

-

- Cardiovascular Diseases

-

- Infectious Diseases

-

- Neurological Disorders

-

- Renal Diseases

-

- Genetic Diseases

-

- Ophthalmic Diseases

-

- Other (endocrine diseases)

- North America Method Outlook (Revenue, USD Million; 2025-2032)

-

- General Submerged Method

-

- Crypt Organoid Culture Techniques

-

- Air Liquid Interface (ALI) Method

-

- Clonal Organoids from Lgr5+ Cells

-

- Brain and Retina Organoid Formation Protocol

- North America Technology Outlook (Revenue, USD Million; 2025-2032)

-

- 3D Bioprinting

-

- Hydrogel-Based Technology

-

- Scaffold-Based Technology

-

- Scaffold-Free (Self-Assembly) Techniques

-

- Magnetic Levitation

-

- Microfluidic Technology (Organ-on-Chip)

-

- Centrifugal Forced Aggregation

-

- Rotating Wall Vessel Bioreactors

-

- Hanging Drop Culture

- North America Application Type Outlook (Revenue, USD Million; 2025-2032)

-

- Drug Discovery & Development

-

- Disease Modelling

-

- Toxicity Testing

-

- Personalized Medicine & Precision neurology

-

- Development Biology

-

- Biomarker Discovery

-

- Other (biomedical research)

- North America End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical & Biotechnology Companies

-

- Academic & Research Institutions

-

- Hospitals

-

- Others (CROs, government, regulators)

- U.S

- U.S Organoid Type Outlook (Revenue, USD Million; 2025-2032)

-

- Brain Organoids

-

- Heart Organoids

-

- Intestinal Organoids

-

- Kidney Organoids

-

- Liver Organoids

-

- Lung Organoids

-

- Pancreatic Organoids

-

- Stomach organoids

-

- Neuro organoids

-

- Colorectal organoids

-

- Others (Prostrate, Retina, Skin, Breast)

- U.S Product Type Outlook (Revenue, USD Million; 2025-2032)

-

- Ready-to-Use Organoid Products

-

- Personalized Organoid Models

- U.S Source Type Outlook (Revenue, USD Million; 2025-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- U.S Storage Conditions Outlook (Revenue, USD Million; 2025-2032)

-

- Shelf-stable Organoids

-

- Cryopreserved Organoids

- U.S Disease Area Outlook (Revenue, USD Million; 2025-2032)

-

- Oncology

-

- Liver Diseases

-

- Gastrointestinal Diseases

-

- Cardiovascular Diseases

-

- Infectious Diseases

-

- Neurological Disorders

-

- Renal Diseases

-

- Genetic Diseases

-

- Ophthalmic Diseases

-

- Other (endocrine diseases)

- U.S Method Outlook (Revenue, USD Million; 2025-2032)

-

- General Submerged Method

-

- Crypt Organoid Culture Techniques

-

- Air Liquid Interface (ALI) Method

-

- Clonal Organoids from Lgr5+ Cells

-

- Brain and Retina Organoid Formation Protocol

- U.S Technology Outlook (Revenue, USD Million; 2025-2032)

-

- 3D Bioprinting

-

- Hydrogel-Based Technology

-

- Scaffold-Based Technology

-

- Scaffold-Free (Self-Assembly) Techniques

-

- Magnetic Levitation

-

- Microfluidic Technology (Organ-on-Chip)

-

- Centrifugal Forced Aggregation

-

- Rotating Wall Vessel Bioreactors

-

- Hanging Drop Culture

- U.S Application Type Outlook (Revenue, USD Million; 2025-2032)

-

- Drug Discovery & Development

-

- Disease Modelling

-

- Toxicity Testing

-

- Personalized Medicine & Precision neurology

-

- Development Biology

-

- Biomarker Discovery

-

- Other (biomedical research)

- U.S End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical & Biotechnology Companies

-

- Academic & Research Institutions

-

- Hospitals

-

- Others (CROs, government, regulators)

- Canada

- Canada Organoid Type Outlook (Revenue, USD Million; 2025-2032)

-

- Brain Organoids

-

- Heart Organoids

-

- Intestinal Organoids

-

- Kidney Organoids

-

- Liver Organoids

-

- Lung Organoids

-

- Pancreatic Organoids

-

- Stomach organoids

-

- Neuro organoids

-

- Colorectal organoids

-

- Others (Prostrate, Retina, Skin, Breast)

- Canada Product Type Outlook (Revenue, USD Million; 2025-2032)

-

- Ready-to-Use Organoid Products

-

- Personalized Organoid Models

- Canada Source Type Outlook (Revenue, USD Million; 2025-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Canada Storage Conditions Outlook (Revenue, USD Million; 2025-2032)

-

- Shelf-stable Organoids

-

- Cryopreserved Organoids

- Canada Disease Area Outlook (Revenue, USD Million; 2025-2032)

-

- Oncology

-

- Liver Diseases

-

- Gastrointestinal Diseases

-

- Cardiovascular Diseases

-

- Infectious Diseases

-

- Neurological Disorders

-

- Renal Diseases

-

- Genetic Diseases

-

- Ophthalmic Diseases

-

- Other (endocrine diseases)

- Canada Method Outlook (Revenue, USD Million; 2025-2032)

-

- General Submerged Method

-

- Crypt Organoid Culture Techniques

-

- Air Liquid Interface (ALI) Method

-

- Clonal Organoids from Lgr5+ Cells

-

- Brain and Retina Organoid Formation Protocol

- Canada Technology Outlook (Revenue, USD Million; 2025-2032)

-

- 3D Bioprinting

-

- Hydrogel-Based Technology

-

- Scaffold-Based Technology

-

- Scaffold-Free (Self-Assembly) Techniques

-

- Magnetic Levitation

-

- Microfluidic Technology (Organ-on-Chip)

-

- Centrifugal Forced Aggregation

-

- Rotating Wall Vessel Bioreactors

-

- Hanging Drop Culture

- Canada Application Type Outlook (Revenue, USD Million; 2025-2032)

-

- Drug Discovery & Development

-

- Disease Modelling

-

- Toxicity Testing

-

- Personalized Medicine & Precision neurology

-

- Development Biology

-

- Biomarker Discovery

-

- Other (biomedical research)

- Canada End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical & Biotechnology Companies

-

- Academic & Research Institutions

-

- Hospitals

-

- Others (CROs, government, regulators)

- Mexico

- Mexico Organoid Type Outlook (Revenue, USD Million; 2025-2032)

-

- Brain Organoids

-

- Heart Organoids

-

- Intestinal Organoids

-

- Kidney Organoids

-

- Liver Organoids

-

- Lung Organoids

-

- Pancreatic Organoids

-

- Stomach organoids

-

- Neuro organoids

-

- Colorectal organoids

-

- Others (Prostrate, Retina, Skin, Breast)

- Mexico Product Type Outlook (Revenue, USD Million; 2025-2032)

-

- Ready-to-Use Organoid Products

-

- Personalized Organoid Models

- Mexico Source Type Outlook (Revenue, USD Million; 2025-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Mexico Storage Conditions Outlook (Revenue, USD Million; 2025-2032)

-

- Shelf-stable Organoids

-

- Cryopreserved Organoids

- Mexico Disease Area Outlook (Revenue, USD Million; 2025-2032)

-

- Oncology

-

- Liver Diseases

-

- Gastrointestinal Diseases

-

- Cardiovascular Diseases

-

- Infectious Diseases

-

- Neurological Disorders

-

- Renal Diseases

-

- Genetic Diseases

-

- Ophthalmic Diseases

-

- Other (endocrine diseases)

- Mexico Method Outlook (Revenue, USD Million; 2025-2032)

-

- General Submerged Method

-

- Crypt Organoid Culture Techniques

-

- Air Liquid Interface (ALI) Method

-

- Clonal Organoids from Lgr5+ Cells

-

- Brain and Retina Organoid Formation Protocol

- Mexico Technology Outlook (Revenue, USD Million; 2025-2032)

-

- 3D Bioprinting

-

- Hydrogel-Based Technology

-

- Scaffold-Based Technology

-

- Scaffold-Free (Self-Assembly) Techniques

-

- Magnetic Levitation

-

- Microfluidic Technology (Organ-on-Chip)

-

- Centrifugal Forced Aggregation

-

- Rotating Wall Vessel Bioreactors

-

- Hanging Drop Culture

- Mexico Application Type Outlook (Revenue, USD Million; 2025-2032)

-

- Drug Discovery & Development

-

- Disease Modelling

-

- Toxicity Testing

-

- Personalized Medicine & Precision neurology

-

- Development Biology

-

- Biomarker Discovery

-

- Other (biomedical research)

- Mexico End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical & Biotechnology Companies

-

- Academic & Research Institutions

-

- Hospitals

-

- Others (CROs, government, regulators)

- Europe

- Europe Organoid Type Outlook (Revenue, USD Million; 2025-2032)

-

- Brain Organoids

-

- Heart Organoids

-

- Intestinal Organoids

-

- Kidney Organoids

-

- Liver Organoids

-

- Lung Organoids

-

- Pancreatic Organoids

-

- Stomach organoids

-

- Neuro organoids

-

- Colorectal organoids

-

- Others (Prostrate, Retina, Skin, Breast)

- Europe Product Type Outlook (Revenue, USD Million; 2025-2032)

-

- Ready-to-Use Organoid Products

-

- Personalized Organoid Models

- Europe Source Type Outlook (Revenue, USD Million; 2025-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Europe Storage Conditions Outlook (Revenue, USD Million; 2025-2032)

-

- Shelf-stable Organoids

-

- Cryopreserved Organoids

- Europe Disease Area Outlook (Revenue, USD Million; 2025-2032)

-

- Oncology

-

- Liver Diseases

-

- Gastrointestinal Diseases

-

- Cardiovascular Diseases

-

- Infectious Diseases

-

- Neurological Disorders

-

- Renal Diseases

-

- Genetic Diseases

-

- Ophthalmic Diseases

-

- Other (endocrine diseases)

- Europe Method Outlook (Revenue, USD Million; 2025-2032)

-

- General Submerged Method

-

- Crypt Organoid Culture Techniques

-

- Air Liquid Interface (ALI) Method

-

- Clonal Organoids from Lgr5+ Cells

-

- Brain and Retina Organoid Formation Protocol

- Europe Technology Outlook (Revenue, USD Million; 2025-2032)

-

- 3D Bioprinting

-

- Hydrogel-Based Technology

-

- Scaffold-Based Technology

-

- Scaffold-Free (Self-Assembly) Techniques

-

- Magnetic Levitation

-

- Microfluidic Technology (Organ-on-Chip)

-

- Centrifugal Forced Aggregation

-

- Rotating Wall Vessel Bioreactors

-

- Hanging Drop Culture

- Europe Application Type Outlook (Revenue, USD Million; 2025-2032)

-

- Drug Discovery & Development

-

- Disease Modelling

-

- Toxicity Testing

-

- Personalized Medicine & Precision neurology

-

- Development Biology

-

- Biomarker Discovery

-

- Other (biomedical research)

- Europe End User Outlook (Revenue, USD Million; 2025-2032)

-

- Pharmaceutical & Biotechnology Companies

-

- Academic & Research Institutions

-

- Hospitals

-

- Others (CROs, government, regulators)

- Germany

- Germany Organoid Type Outlook (Revenue, USD Million; 2025-2032)

-

- Brain Organoids

-

- Heart Organoids

-

- Intestinal Organoids

-

- Kidney Organoids

-

- Liver Organoids

-

- Lung Organoids

-

- Pancreatic Organoids

-

- Stomach organoids

-

- Neuro organoids

-

- Colorectal organoids

-

- Others (Prostrate, Retina, Skin, Breast)

- Germany Product Type Outlook (Revenue, USD Million; 2025-2032)

-

- Ready-to-Use Organoid Products

-

- Personalized Organoid Models

- Germany Source Type Outlook (Revenue, USD Million; 2025-2032)

-

- Ready-to-Use Organoid Products

-

- Personalized Organoid Models

- Germany Storage Conditions Outlook (Revenue, USD Million; 2025-2032)

-

- Shelf-stable Organoids

-

- Cryopreserved Organoids