Market Synopsis

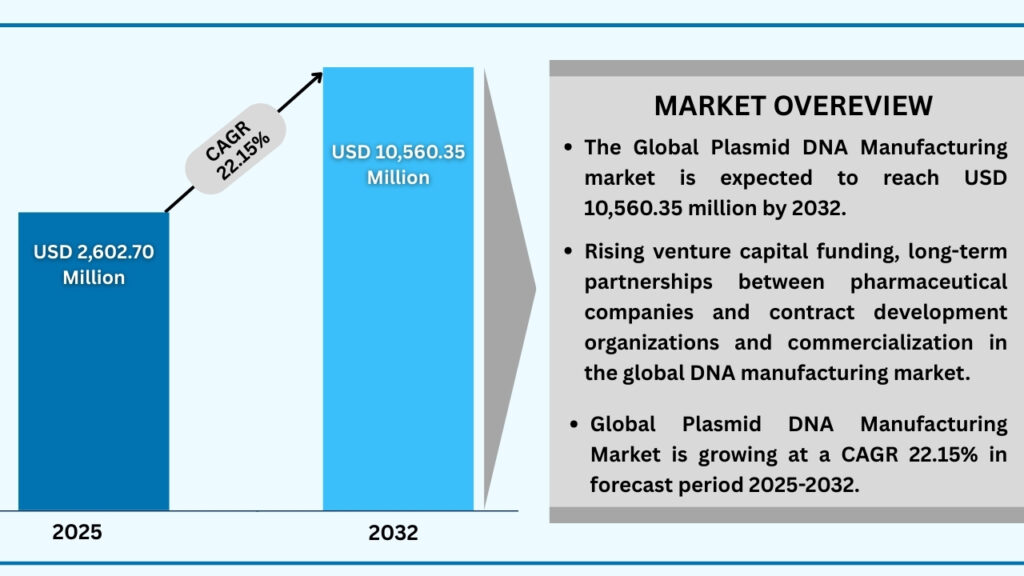

The global plasmid DNA manufacturing market size was USD 2,130.74 million in 2024 and is expected to reach USD 10,560.35 million at a CAGR of 22.15% during the forecast period from 2025 to 2032. The global plasmid DNA manufacturing market is growing rapidly as gene therapies, cell therapies, and DNA vaccines gain wider adoption. With traditional systems struggling to meet quality and scalability needs, advanced bioprocessing technologies and improved purification methods are being embraced to ensure consistent, large-scale production. Collaborations between biotech firms, pharma companies, and Contract Development and Manufacturing Organizations (CDMOs), along with rising investments and clearer Good Manufacturing Practice (GMP) regulations, are strengthening the industry’s foundation. As research in cell and gene therapies expands worldwide, plasmid DNA manufacturing is emerging as a crucial backbone for next-generation biopharmaceutical innovation.

Global Plasmid DNA Manufacturing Market (USD million)

Global Plasmid DNA Manufacturing Market by Grade Insights:

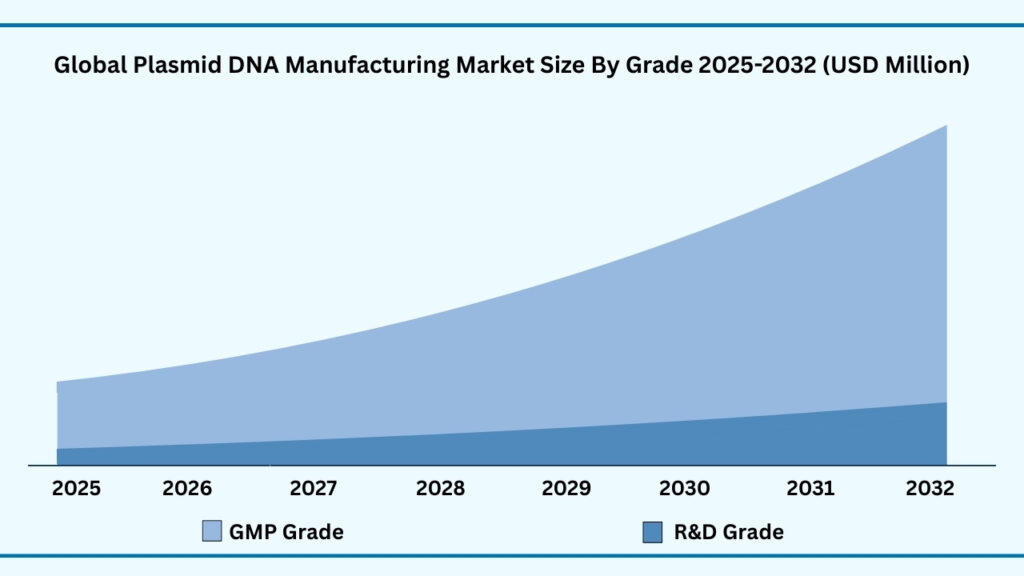

GMP Grade segment accounted for market share of share 87.43% in 2024 in the global plasmid DNA manufacturing market.

The grade-based segmentation of the plasmid DNA manufacturing market highlights a clear divide between Research & Development (R&D) applications and Good Manufacturing Practice (GMP) production, with GMP grade accounting for the dominant 87.43% share of revenues in 2024. This segment alone is projected to expand at a CAGR of 22.17%, reaching approximately USD 9,247.42 million during the forecast period from 2025 to 2032. The strong demand for GMP-grade plasmids stems from their critical role in producing clinical and commercial biologics, including viral vectors such as Adeno-Associated Virus (AAV), lentivirus, adenovirus, and retrovirus, all of which are foundational in advancing cell and gene therapies. Beyond viral vector manufacturing, GMP plasmids are integral to mRNA therapeutics, antibody-based medicines, DNA vaccine production, and gene and cell therapy pipelines, establishing them as a cornerstone of modern biopharmaceutical manufacturing.

In parallel, the R&D-grade plasmid DNA segment continues to be an indispensable enabler of early-stage discovery, supporting preclinical work across viral vector design, messenger RNA (mRNA) development, antibody engineering, and DNA vaccine research. Applications also extend to cutting-edge areas like CRISPR-based gene editing and RNA therapeutics exploration, where academic labs and biotech startups are leveraging R&D-grade plasmids for proof-of-concept studies. Companies such as Aldevron (a Danaher company) and VGXI, Inc. provide both R&D- and GMP-grade plasmid services, allowing seamless progression from bench research to clinical production. Similarly, partnerships between contract development and manufacturing organizations (CDMOs) and pharmaceutical innovators are ensuring that advances made at the research level can be translated more efficiently into large-scale, regulatory-compliant manufacturing.

Collectively, the grade segment underscores how plasmid DNA manufacturing underpins the entire innovation spectrum—from basic research through clinical translation to commercial rollout. With GMP-grade plasmids driving revenue dominance due to their indispensability in advanced therapies, and R&D-grade plasmids fuelling scientific exploration, this dual structure is creating a robust ecosystem. The interplay between discovery-focused plasmid uses and large-scale GMP production is not only accelerating therapeutic pipelines but also fostering new opportunities in vaccines, precision medicine, and regenerative treatments.

Global Plasmid DNA Manufacturing Market, By Grade Type (USD million)

Global Plasmid DNA Manufacturing Market by Workflow Insights:

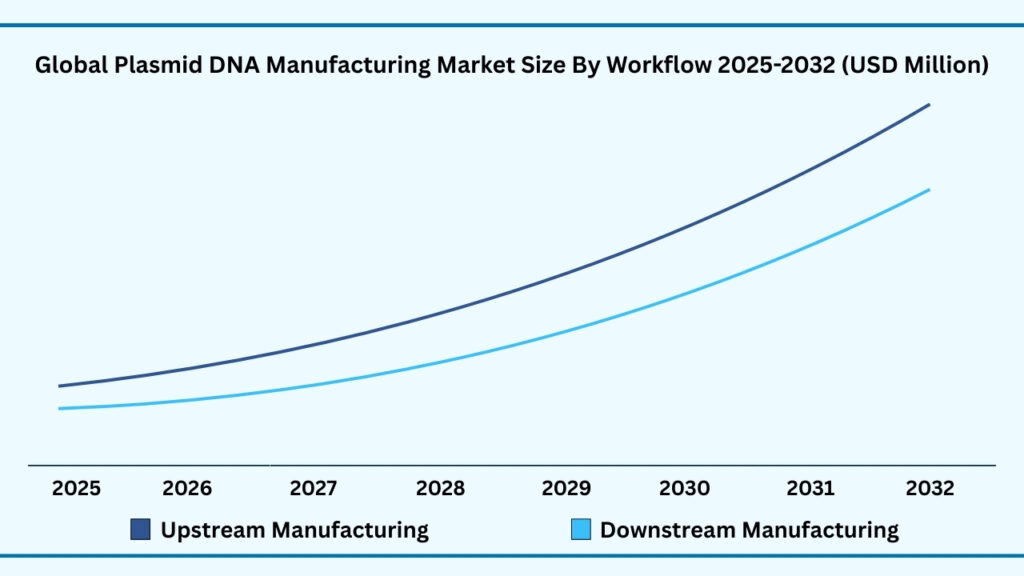

Upstream Manufacturing segment accounted for market share of share 53.97% in 2024 in the global Plasmid DNA Manufacturing market.

The workflow segmentation of the plasmid DNA manufacturing market is divided into upstream and downstream processes, with upstream manufacturing capturing the largest share at 53.97% of revenues in 2024. This segment is expected to grow at a CAGR of 22.16%, reaching nearly USD 5,703.66 million during forecast period from 2025 to 2032. Upstream activities such as vector amplification and expansion, followed by vector recovery and harvesting, form the foundation of plasmid DNA production. The efficiency and consistency of these early steps are critical in determining the overall yield and quality of plasmids, making them a priority for both research-oriented production and clinical-grade manufacturing. Companies and CDMOs are increasingly investing in advanced bioreactor systems, optimized host strains, and automated monitoring platforms to ensure higher productivity and scalability in upstream workflows.

Downstream manufacturing, which includes purification and fill–finish operations, plays an equally vital role by ensuring that plasmids meet stringent purity, safety, and stability requirements set by global regulatory agencies. Purification technologies such as chromatography and membrane-based systems are being refined to remove impurities and endotoxins while maintaining high recovery rates, enabling reliable supply for clinical applications. The fill–finish stage, where plasmids are aseptically formulated, packaged, and stored, has become an area of heightened focus given its impact on product integrity and shelf life. Providers like Lonza and Charles River have been working to enhance downstream platforms, introducing high-throughput purification solutions and flexible fill–finish capabilities to support both small-scale research needs and large commercial batches.

Together, upstream and downstream processes define the backbone of plasmid DNA manufacturing, ensuring that materials can progress smoothly from initial amplification to final delivery. With upstream manufacturing driving the majority of revenues due to its centrality in scaling production, and downstream innovations guaranteeing regulatory compliance and clinical readiness, the workflow segment is shaping the industry’s ability to meet the rising demand for DNA in vaccines, gene therapies, and advanced biologics.

Global Plasmid DNA Manufacturing Market, By workflow (USD million)

Global Plasmid DNA Manufacturing Market by Development Phase Insights:

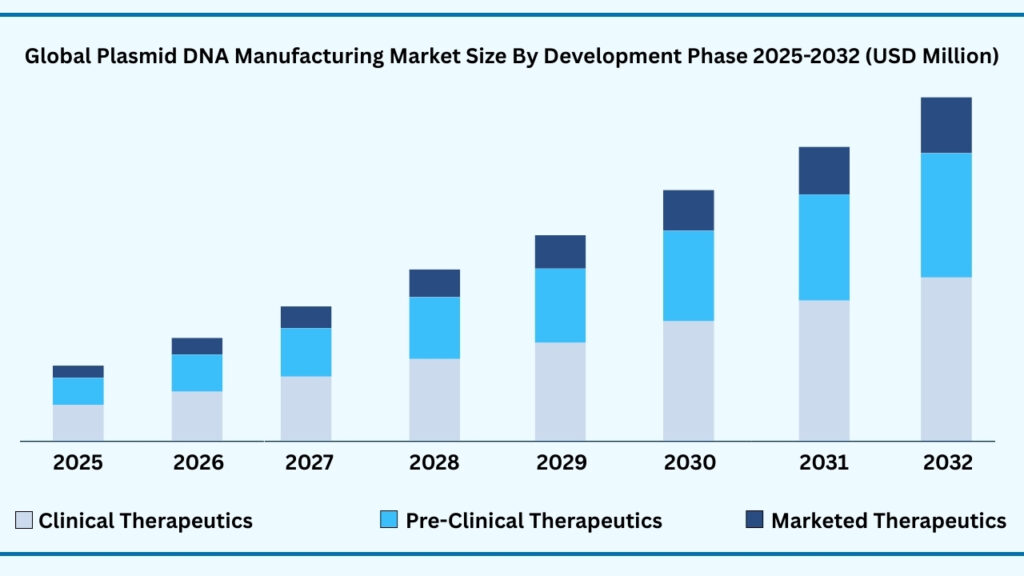

Clinical Therapeutics segment accounted for market share of share 54.86% in 2024 in the global Plasmid DNA Manufacturing market.

The development phase segmentation of the plasmid DNA manufacturing market is led by the clinical therapeutics category, which accounted for 54.86% of the market share in 2024. This segment is projected to expand at a CAGR of 22.24%, reaching nearly USD 5,826.10 million during forecast period from 2025 to 2032. The dominance of clinical-stage therapeutics reflects the growing pipeline of plasmid-enabled treatments, particularly in cell and gene therapy trials, DNA-based vaccines, and mRNA therapeutics. Plasmids are indispensable at this stage as they serve as the blueprint for viral vector production and as raw materials for nucleic acid–based drugs. With hundreds of ongoing global clinical trials in oncology, rare genetic disorders, and infectious diseases, the demand for GMP-grade plasmids continues to rise. For example, companies like Oxford Biomedica and Lonza are scaling their plasmid platforms to meet surging requirements from biotech firms advancing therapies into late-stage clinical testing.

Alongside clinical applications, the pre-clinical therapeutics segment plays a critical role in driving innovation and validating new therapeutic approaches. Plasmids produced for pre-clinical use support proof-of-concept studies in animal models, enabling researchers to evaluate safety, efficacy, and dosing strategies before entering human trials. This stage is particularly important for emerging modalities such as CRISPR-based gene editing and RNA therapeutics, where reliable plasmid supply accelerates the translation of early research into viable candidates. Contract development and manufacturing organizations (CDMOs) often offer both R&D- and GMP-grade plasmids, creating a smooth transition from discovery through pre-clinical development into clinical-scale production.

In comparison, the marketed therapeutics segment remains smaller but represents a fast-maturing area as the first wave of plasmid-enabled therapies gains regulatory approval. DNA vaccines, gene therapies, and CAR-T products that rely on plasmid DNA are gradually expanding into the commercial space, paving the way for wider adoption. While clinical therapeutics currently dominate due to the large volume of ongoing trials, pre-clinical plasmids remain the backbone of discovery, and marketed products signal the industry’s ability to translate pipeline advances into approved therapies. Together, these three development phases illustrate the critical role of plasmid DNA manufacturing in supporting the continuum from early research to commercial rollout, with clinical-stage demand serving as the primary revenue driver today.

Global Plasmid DNA Manufacturing Market, By Development Phase (USD million)

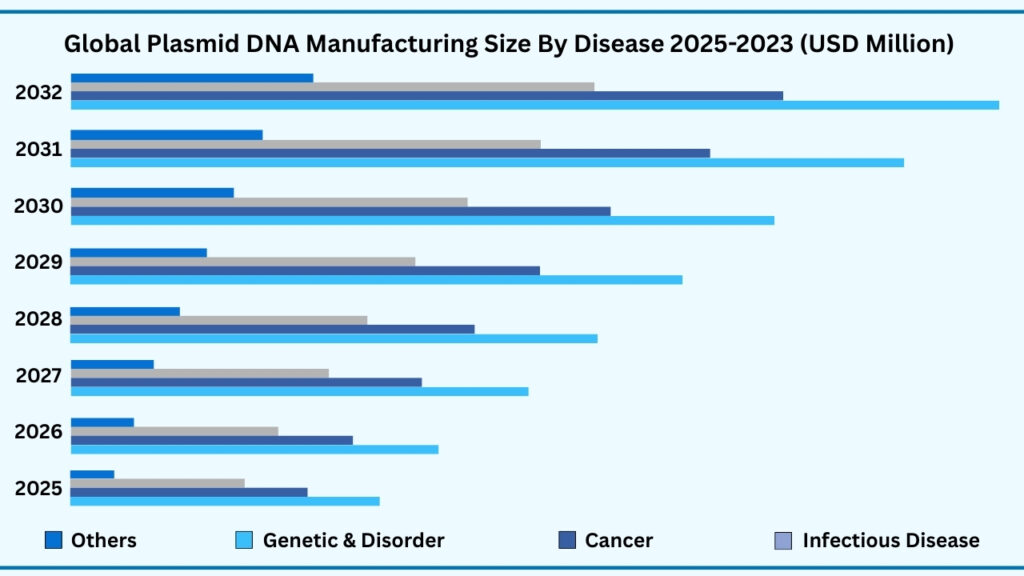

Global Plasmid DNA Manufacturing Market by Disease Insights:

Infectious Disease segment accounted for market share of share 38.59% in 2024 in the global Plasmid DNA Manufacturing market.

The infectious disease segment leads the global plasmid DNA manufacturing market, accounting for 38.59% of revenues in 2024. This category is projected to reach nearly USD 4,105.01 million during forecast period from 2025 to 2032, growing at a CAGR of 22.26%. The leadership of this segment is largely driven by the growing role of plasmid DNA in vaccine development against viral and bacterial infections. DNA vaccines, which rely on plasmid backbones, have gained significant momentum due to their rapid development timelines, stability, and ability to induce strong immune responses. Pharmaceutical companies and biotech firms are increasingly using plasmid-based platforms for both pandemic preparedness and routine immunization programs. For instance, several plasmid DNA vaccines targeting diseases such as Zika virus, HIV, and influenza are in clinical pipelines, while COVID-19 accelerated industry-wide adoption of DNA and RNA vaccine technologies.

Beyond infectious diseases, the cancer segment represents one of the most dynamic growth areas for plasmid DNA applications. Plasmids are extensively used in the production of viral vectors for cancer immunotherapies, including chimeric antigen receptor T-cell (CAR-T) treatments, oncolytic viruses, and DNA-based cancer vaccines. Clinical trials continue to expand in oncology, with plasmid-driven therapies being evaluated for solid tumours and haematological malignancies. Similarly, the genetic disorder segment relies heavily on plasmid DNA as a backbone for gene replacement and editing therapies. Rare diseases such as spinal muscular atrophy and haemophilia are areas where plasmid-enabled vectors are being developed to correct underlying genetic defects, offering patients treatment options where no alternatives previously existed.

The “others” category, which includes autoimmune and cardiovascular diseases, is steadily emerging as an important application area. Plasmid DNA is being explored in therapies designed to modulate immune responses in autoimmune conditions or stimulate angiogenesis in cardiovascular disorders. While these areas currently hold smaller market shares, they highlight the broadening scope of plasmid DNA beyond infectious disease and oncology. In comparison, infectious diseases currently dominate due to the urgent global demand for vaccines and antiviral solutions, but cancer and genetic disorder pipelines are rapidly catching up with strong clinical and commercial potential. Collectively, these disease-focused applications demonstrate how plasmid DNA manufacturing is not only meeting immediate global health needs but also shaping the future of personalized and precision medicine across diverse therapeutic areas.

Global Plasmid DNA Manufacturing Market, By Disease (USD million)

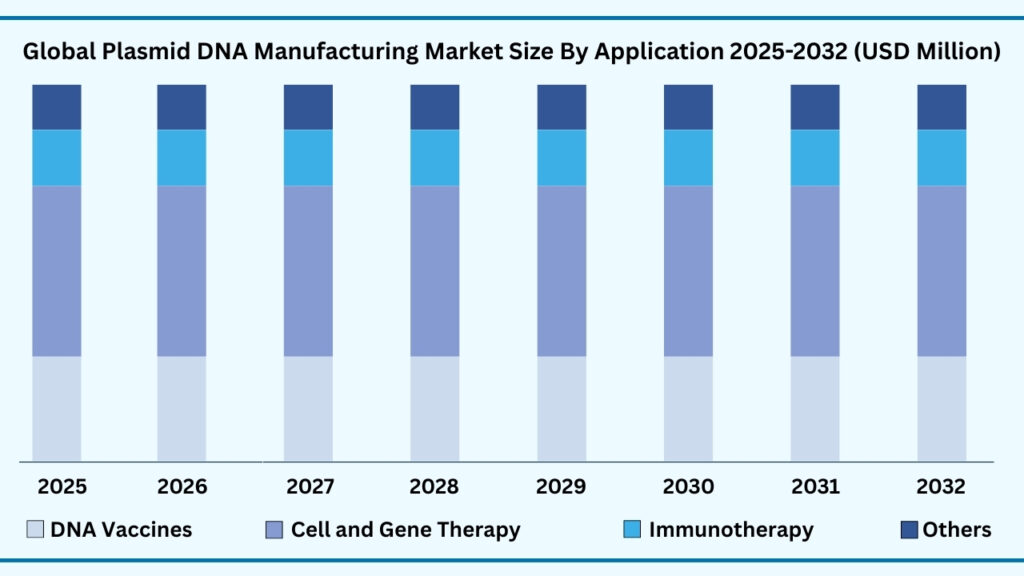

Global Plasmid DNA Manufacturing Market by Application Insights:

Cell and Gene Therapy segment accounted for market share of share 56.32% in 2024 in the global Plasmid DNA Manufacturing market.

The cell and gene therapy segment leads the global plasmid DNA manufacturing market, capturing 56.32% of the share in 2024. Revenues from this segment are expected to reach nearly USD 5,980.63 million during forecast period from 2025 to 2032, expanding at a CAGR of 22.24%. This leadership reflects the essential role of plasmids as raw materials for producing viral vectors such as Adeno-Associated Virus (AAV) and lentivirus, which power a wide range of cell and gene therapy programs. With hundreds of therapies in clinical trials targeting oncology, rare genetic disorders, and regenerative medicine, demand for GMP-grade plasmids is accelerating. For instance, Aldevron (Danaher) and VGXI, Inc. have expanded their large-scale plasmid manufacturing platforms specifically to meet the surge in gene therapy pipelines advancing toward commercialization.

Beyond cell and gene therapy, plasmid DNA is a cornerstone for other high-growth applications. DNA vaccines are a major area of focus, offering stability, rapid design, and strong immune responses. Following the momentum gained during the COVID-19 pandemic, DNA vaccine development has broadened into targets such as HIV, Zika virus, and various influenza strains. At the same time, plasmid-driven immunotherapies are gaining ground in oncology, where they support the production of CAR-T cells, oncolytic viruses, and cancer vaccines. These approaches are redefining cancer treatment by enabling patient-specific and durable responses. The “others” category, which includes research reagents, antibody discovery, and general molecular biology applications, continues to provide steady demand, particularly from academic institutions and smaller biotech firms engaged in early-stage innovation.

In comparison, cell and gene therapy applications dominate today because they represent the fastest-growing area of modern medicine, translating plasmid DNA into tangible therapeutic breakthroughs. DNA vaccines and immunotherapies, however, are expanding rapidly and are poised to capture a larger share as more products move through clinical validation. Together, these applications underscore how plasmid DNA manufacturing is enabling a broad spectrum of biomedical advancements—from personalized treatments and genetic cures to global vaccine programs—cementing its position at the heart of next-generation healthcare.

Global Plasmid DNA Manufacturing Market, By Application (USD million)

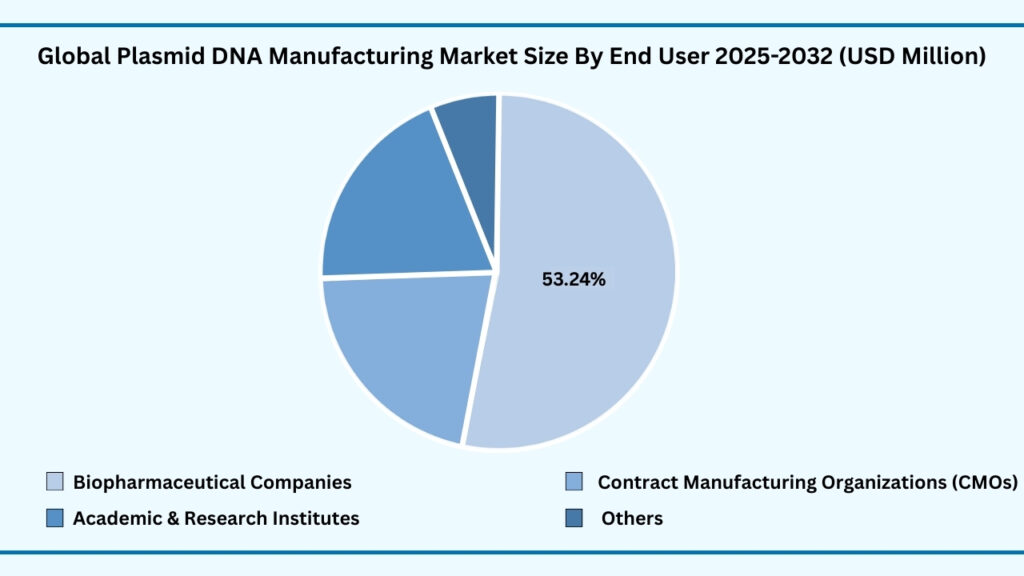

Global Plasmid DNA Manufacturing Market by End User Insights:

Biopharmaceutical Companies segment accounted for market share of share 53.37% in 2024 in the global Plasmid DNA Manufacturing market.

The biopharmaceutical companies segment leads the global plasmid DNA manufacturing market, representing 53.37% of the share in 2024. Revenues from this segment are projected to reach around USD 5,658.98 million during forecast period from 2025 to 2032, growing at a CAGR of 22.21%. This leadership is attributed to the central role of plasmids in biopharma pipelines, where they serve as essential starting materials for producing viral vectors, messenger RNA (mRNA), and engineered cell therapies. Companies are scaling up demand for Good Manufacturing Practice (GMP)-grade plasmids to support late-stage clinical trials and product launches across oncology, rare diseases, and regenerative medicine. For example, Pfizer and BioNTech relied on large-scale plasmid supply chains during the COVID-19 mRNA vaccine rollout, underscoring the strategic importance of plasmid availability for rapid product development and global distribution.

Beyond biopharma, Contract Manufacturing Organizations (CMOs) have emerged as critical partners, offering flexible, end-to-end plasmid production capabilities to both startups and large pharmaceutical firms. Their expertise in scaling processes, ensuring regulatory compliance, and reducing time-to-market makes them indispensable in today’s competitive therapeutic landscape. Academic and research institutes also play a significant role, driving innovation in next-generation plasmid design and small-batch production for early-stage projects in gene editing, synthetic biology, and novel vaccine approaches. Meanwhile, the “Others” category, which includes government laboratories and non-profit entities, contributes to the development of standardized frameworks and quality benchmarks, while also supporting public health initiatives through collaborative research.

In comparison, biopharmaceutical companies dominate due to their immediate commercial needs for reliable and scalable plasmid supply. However, the growing presence of CMOs, academic innovators, and government-backed programs reflects the collaborative fabric of the market, where each end-user segment plays a complementary role. Together, this ecosystem ensures that plasmid DNA manufacturing continues to expand in scope—fuelling therapeutic breakthroughs, advancing research, and strengthening healthcare resilience on a global scale.

Global Plasmid DNA Manufacturing Market, By End User (USD million)

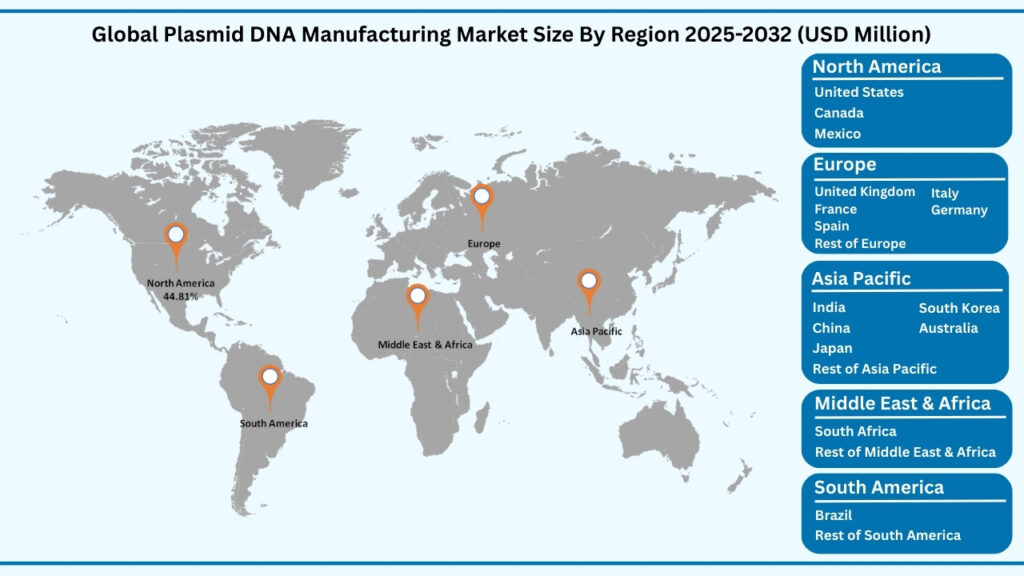

Global Plasmid DNA Manufacturing Market by Region Insights:

North America segment accounted for market share of share 44.81% in 2024 in the global Plasmid DNA Manufacturing market.

The North America region leads the global plasmid DNA manufacturing market, accounting for 44.81% of the share in 2024. Revenues from this region are projected to reach USD 4,743.16 million during forecast period from 2025 to 2032, expanding at a CAGR of 22.19%. North America’s dominance is rooted in its strong biopharmaceutical sector, advanced contract manufacturing capabilities, and growing adoption of cell and gene therapies that rely heavily on GMP-grade plasmids. The United States, in particular, has become a key hub, with major companies and research institutions scaling production to support DNA vaccines, immunotherapies, and regenerative medicine programs. Strategic government initiatives, such as funding for pandemic preparedness and precision medicine, are further accelerating innovation. For instance, several U.S.-based manufacturing consortia have expanded plasmid capacity to meet the rising demand for viral vectors and mRNA platforms, ensuring faster product development and regulatory approvals.

Beyond North America, Europe represents another significant market, benefiting from strong regulatory frameworks that emphasize quality standards in advanced therapies and active collaboration between biotech firms and academic institutions. Countries such as Germany, the U.K., and Switzerland are particularly focused on scaling plasmid DNA production for clinical applications, with growing emphasis on sustainable, large-scale bioprocessing. Meanwhile, the Asia Pacific region is emerging as the fastest-growing market, supported by increasing R&D spending, rapidly expanding biotechnology industries, and government-driven initiatives in China, Japan, and South Korea to localize plasmid manufacturing for gene therapy and vaccine pipelines. In contrast, Latin America (LATAM) and the Middle East & Africa (MEA) currently hold smaller market shares but are witnessing gradual growth as research infrastructure develops and international collaborations strengthen.

In comparison, North America currently dominates due to its robust research ecosystem, advanced production capacity, and high investment flows from both private and public sectors. However, Europe’s regulatory strength and Asia Pacific’s rapid industrial expansion signal a global diversification of plasmid DNA manufacturing. Together, these regions are shaping a dynamic and interconnected market landscape, ensuring that plasmid technologies remain central to the progress of modern biopharmaceuticals, gene therapies, and next-generation vaccines worldwide.

Global Plasmid DNA Manufacturing Market, By Region (USD million)

Major Companies and Competitive Landscape

The global plasmid DNA manufacturing market is advancing at a rapid pace, fuelled by the growing adoption of gene-based therapies and next-generation vaccines. Competition is intensifying as leading biopharma companies and specialized contract manufacturers expand their presence through strategic collaborations, licensing deals, acquisitions, and facility upgrades. A strong focus is being placed on improving both upstream and downstream workflows, ensuring compliance with Good Manufacturing Practice (GMP) standards, and boosting large-scale production to support applications in cell and gene therapy, DNA vaccines, and immunotherapy. These developments are helping accelerate clinical pipelines, enhance manufacturing efficiency, and address the rising demand for reliable, high-quality plasmid DNA worldwide. Key players highlighted in the global plasmid DNA manufacturing market report include:

- Aldevron

- VGXI, Inc.

- Thermo Fisher Scientific

- Charles River Laboratories

- Catalent

- Wuxi Biologics

- GenScript ProBio

- AGC Biologics

- Cobra Biologics

- PlasmidFactory GmbH & Co. KG

- Waisman Biomanufacturing

- Bio Elpida

- Biovian

- Richter-Helm BioLogics

- Eurofins Genomics

- Cell and Gene Therapy Catapult

- Nature Technology Corporation

- Akron Biotech

- Xpress Biologics

- NorthX Biologics

- BioCina

- RD-Biotech

- Wacker Biotech

- Polyplus

- Touchlight Genetics Ltd.

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 2,602.70 Million |

| CAGR (2024–2032) | 22.15% |

| Revenue forecast to 2033 | USD 10,560.35 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Grade, By Workflow, By Development Phase, By Disease, By Application, By End User and By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, UAE, South Africa, Turkey, Rest of MEA |

| Key companies profiled | Aldevron, VGXI, Inc., Thermo Fisher Scientific, Charles River Laboratories, Catalent, Wuxi Biologics, GenScript ProBio, AGC Biologics, Cobra Biologics, PlasmidFactory GmbH & Co. KG, Waisman Biomanufacturing, Bio Elpida, Biovian, Richter-Helm BioLogics, Eurofins Genomics, Cell and Gene Therapy Catapult, Nature Technology Corporation, Akron Biotech, Xpress Biologics, NorthX Biologics, BioCina, RD-Biotech, Wacker Biotech, Polyplus, and Touchlight Genetics Ltd. |

| Customization scope | 10 hours of free customization and expert consultation |

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of global plasmid DNA manufacturing market

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1.Primary

2.1.2.Secondary

2.1.3.Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1.Market value

2.3.2.Market volume

2.3.3.Exchange rate

2.3.4.Price

2.3.5.Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2025-2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10. Formulation & manufacturing

4.11. Distribution & retail

4.12. Import-export analysis

4.13. Brand comparative analysis

4.14. Technological advancements

4.15. Porter’s five force

4.15.1. Threat of new entrants

4.15.1.1. Capital requirment

4.15.1.2. Product knowledge

4.15.1.3. Technical knowledge

4.15.1.4. Customer relation

4.15.1.5. Access to appliation and technology

4.15.2. Threat of substitutes

4.15.2.1. Cost

4.15.2.2. Performance

4.15.2.3. Availability

4.15.2.4. Technical knowledge

4.15.2.5. Durability

4.15.3. Bargainning power of buyers

4.15.3.1. Numbers of buyers relative to suppliers

4.15.3.2. Product differentiation

4.15.3.3. Threat of forward integration

4.15.3.4. Buyers volume

4.15.4. Bargainning power of suppliers

4.15.4.1. Suppliers concentration

4.15.4.2. Buyers switching cost to other suppliers

4.15.4.3. Threat of backward integration

4.15.5. Bargainning power of suppliers

4.15.5.1. Industry concentration

4.15.5.2. Industry growth rate

4.15.5.3. Product differentiation

4.15.6. Patent analysis

4.16. Patent quality and strength

4.17. Regulation coverage

4.18. Pricing analysis

4.19. Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1.Expanding demand for plasmid DNA as a critical raw material in cell & gene therapies,

mRNA vaccines, and DNA vaccines

5.1.2.Advances in large-scale bioreactors, fermentation systems, and downstream purification

improving yield and scalability

5.1.3.Strategic collaborations between biotech, Contract Development and Manufacturing

Organizations (CDMOs), and pharma companies to secure supply for clinical and

commercial pipelines

5.2. Restraints

5.2.1.Complex manufacturing processes with high variability in plasmid quality, supercoiled

content, and yield

5.2.2.High production costs due to specialized fermentation media, purification resins, and

stringent GMP compliance

5.3. Opportunities

5.3.1.Growing adoption of synthetic biology and next-generation plasmid designs for improved

performance

5.3.2.Rising outsourcing to Contract Development and Manufacturing Organizations (CDMOs)

offering scalable, GMP-compliant plasmid manufacturing for clinical and commercial

supply

5.3.3.Expansion into personalized medicine workflows, including patient-specific gene

therapies and autologous cell-based treatments

5.4. Threat

5.4.1.Regulatory uncertainty regarding evolving global GMP standards, release testing, and

comparability requirements across regions

5.4.2.Intellectual property constraints on plasmid backbones, promoters, and optimized

manufacturing methods restricting broader adoption

Chapter 6. Global Plasmid DNA Manufacturing Market By Grade Type Insights & Trends,

Revenue (USD Million)

6.1. Grade Type Dynamics & Market Share, 2025–2032

6.1.1.R&D Grade

6.1.1.1. Viral Vector Development

6.1.1.1.1. AVV

6.1.1.1.2. Lentivirus

6.1.1.1.3. Adenovirus

6.1.1.1.4. Retrovirus

6.1.1.1.5. Others (Baculovirus, Herpes Simplex Virus (HSV) vectors)

6.1.1.2. mRNA Development

6.1.1.3. Antibody Development

6.1.1.4. DNA Vaccine Development

6.1.1.5. Others (Gene Editing Tools Development, RNA Therapeutics Research)

6.1.2.GMP Grade

6.1.2.1. Viral Vector Production

6.1.2.1.1. AAV (Adeno-Associated Virus)

6.1.2.1.2. Lentivirus

6.1.2.1.3. Adenovirus

6.1.2.1.4. Retrovirus

6.1.2.1.5. Others (Baculovirus, HSV, Poxvirus, Sendai virus)

6.1.2.2. mRNA Therapeutics Production

6.1.2.3. Antibody Therapeutics Production

6.1.2.4. DNA Vaccine Commercial Manufacturing

6.1.2.5. Gene & Cell Therapy Manufacturing

6.1.2.6. Others (engineered probiotics, oncolytic viruses)

Chapter 7. Global Plasmid DNA Manufacturing Market By Workflow Insights & Trends, Revenue

(USD Million)

7.1. Workflow Dynamics & Market Share, 2025-2032

7.1.1. Upstream Manufacturing

7.1.1.1. Vector Amplification & Expansion

7.1.1.2. Vector Recovery/Harvesting

7.1.2. Downstream Manufacturing

7.1.2.1. Purification

7.1.2.2. Fill Finish

Chapter 8. Global Plasmid DNA Manufacturing Market By Developmental Phase Insights &

Trends, Revenue (USD Million)

8.1. Developmental Phase Dynamics & Market Share, 2025-2032

8.1.1.Marketed Therapeutics

8.1.2.Pre-Clinical Therapeutics

8.1.3.Clinical Therapeutics

Chapter 9. Global Plasmid DNA Manufacturing Market By Disease Insights & Trends, Revenue

(USD Million)

9.1. Disease Dynamics & Market Share, 2025-2032

9.1.1.Infectious Disease

9.1.2.Cancer

9.1.3.Genetic Disorder

9.1.4.Others (autoimmune disorders, cardiovascular)

Chapter 10. Global Plasmid DNA Manufacturing Market By Application Insights & Trends,

Revenue (USD Million)

10.1. Application Dynamics & Market Share, 2025-2032

10.1.1. DNA Vaccines

10.1.2. Cell and Gene Therapy

10.1.3. Immunotherapy

10.1.4. Others (Research reagents, antibody discovery, general molecular biology)

Chapter 11. Global Plasmid DNA Manufacturing Market By End User Insights & Trends, Revenue

(USD Million)

11.1. End User Dynamics & Market Share, 2025-2032

11.1.1. Biopharmaceutical Companies

11.1.2. Contract Manufacturing Organizations (CMOs)

11.1.3. Academic & Research Institutes

11.1.4. Others (Government labs, non-profit research entities)

Chapter 12. Global Plasmid DNA Manufacturing Market Regional Outlook

12.1. Global Plasmid DNA Manufacturing Market Share By Region, 2025-2032

12.2. North America

12.3. Market By Grade , Market Estimates and Forecast, USD Million

12.3.1. R&D

12.3.1.1. Viral Vector Development

12.3.1.1.1. AVV

12.3.1.1.2. Lentivirus

12.3.1.1.3. Adenovirus

12.3.1.1.4. Retrovirus

12.3.1.1.5. Others (Baculovirus, Herpes Simplex Virus (HSV) vectors)

12.3.1.2. mRNA Development

12.3.1.3. Antibody Development

12.3.1.4. DNA Vaccine Development

12.3.1.5. Others (Gene Editing Tools Development, RNA Therapeutics Research)

12.3.2. GMP Grade

12.3.2.1. Viral Vector Production

12.3.2.1.1. AAV (Adeno-Associated Virus)

12.3.2.1.2. Lentivirus

12.3.2.1.3. Adenovirus

12.3.2.1.4. Retrovirus

12.3.2.1.5. Others (Baculovirus, HSV, Poxvirus, Sendai virus)

12.3.2.2. mRNA Therapeutics Production

12.3.2.3. Antibody Therapeutics Production

12.3.2.4. DNA Vaccine Commercial Manufacturing

12.3.2.5. Gene & Cell Therapy Manufacturing

12.3.2.6. Others (engineered probiotics, oncolytic viruses)

12.3.3.Market By Workflow, Market Estimates and Forecast, USD Million

12.3.3.1. Upstream Manufacturing

12.3.3.1.1. Vector Amplification & Expansion

12.3.3.1.2. Vector Recovery/Harvesting

12.3.3.2. Downstream Manufacturing

12.3.3.2.1. Purification

12.3.3.2.2. Fill Finish

12.3.4.Market By Development Phase, Market Estimates and Forecast, USD Million

12.3.4.1. Marketed Therapeutics

12.3.4.2. Pre-Clinical Therapeutics

12.3.4.3. Clinical Therapeutics

12.3.5.Market By Disease, Market Estimates and Forecast, USD Million

12.3.5.1. Infectious Disease

12.3.5.2. Cancer

12.3.5.3. Genetic Disorder

12.3.5.4. Others (autoimmune disorders, cardiovascular)

12.3.6.Market By Application, Market Estimates and Forecast, USD Million

12.3.6.1. DNA Vaccines

12.3.6.2. Cell and Gene Therapy

12.3.6.3. Immunotherapy

12.3.6.4. Others (Research reagents, antibody discovery, general molecular biology)

12.3.7.Market By End User, Market Estimates and Forecast, USD Million

12.3.7.1. Biopharmaceutical Companies

12.3.7.2. Contract Manufacturing Organizations (CMOs)

12.3.7.3. Academic & Research Institutes

12.3.7.4. Others (Government labs, non-profit research entities)

12.3.8.Market By Country, Market Estimates and Forecast, USD Million

12.3.8.1. US

12.3.8.2. Canada

12.3.8.3. Mexico

12.4. Europe

12.4.1.Market By Grade Type, Market Estimates and Forecast, USD Million

12.4.1.1. R&D

12.4.1.1.1. Viral Vector Development

12.4.1.1.1.1. AVV

12.4.1.1.1.2. Lentivirus

12.4.1.1.1.3. Adenovirus

12.4.1.1.1.4. Retrovirus

12.4.1.1.1.5. Others (Baculovirus, Herpes Simplex Virus (HSV) vectors)

12.4.1.1.2. mRNA Development

12.4.1.1.3. Antibody Development

12.4.1.1.4. DNA Vaccine Development

12.4.1.1.5. Others (Gene Editing Tools Development, RNA Therapeutics Research)

12.4.1.2. GMP Grade

12.4.1.2.1. Viral Vector Production

12.4.1.2.1.1. AAV (Adeno-Associated Virus)

12.4.1.2.1.2. Lentivirus

12.4.1.2.1.3. Adenovirus

12.4.1.2.1.4. Retrovirus

12.4.1.2.1.5. Others (Baculovirus, HSV, Poxvirus, Sendai virus)

12.4.1.2.2. mRNA Therapeutics Production

12.4.1.2.3. Antibody Therapeutics Production

12.4.1.2.4. DNA Vaccine Commercial Manufacturing

12.4.1.2.5. Gene & Cell Therapy Manufacturing

12.4.1.2.6. Others (engineered probiotics, oncolytic viruses)

12.4.2.Market By Workflow, Market Estimates and Forecast, USD Million

12.4.2.1. Upstream Manufacturing

12.4.2.1.1. Vector Amplification & Expansion

12.4.2.1.2. Vector Recovery/Harvesting

12.4.2.2. Downstream Manufacturing

12.4.2.2.1. Purification

12.4.2.2.2. Fill Finish

12.4.3.Market By Development Phase, Market Estimates and Forecast, USD Million,

12.4.3.1. Marketed Therapeutics

12.4.3.2. Pre-Clinical Therapeutics

12.4.3.3. Clinical Therapeutics

12.4.4.Market By Disease, Market Estimates and Forecast, USD Million

12.4.4.1. Infectious Disease

12.4.4.2. Cancer

12.4.4.3. Genetic Disorder

12.4.4.4. Others (autoimmune disorders, cardiovascular)

12.4.5.Market By Application, Market Estimates and Forecast, USD Million,

12.4.5.1. DNA Vaccines

12.4.5.2. Cell and Gene Therapy

12.4.5.3. Immunotherapy

12.4.5.4. Others (Research reagents, antibody discovery, general molecular biology)

12.4.6.Market By End User, Market Estimates and Forecast, USD Million

12.4.6.1. Biopharmaceutical Companies

12.4.6.2. Contract Manufacturing Organizations (CMOs)

12.4.6.3. Academic & Research Institutes

12.4.6.4. Others (Government labs, non-profit research entities)

12.4.7.Market By Country, Market Estimates and Forecast, USD Million

12.4.7.1. Germany

12.4.7.2. France

12.4.7.3. U.K

12.4.7.4. Italy

12.4.7.5. Spain

12.4.7.6. Benelux

12.4.7.7. Russia

12.4.7.8. Finland

12.4.7.9. Sweden

12.4.7.10. Rest Of Europe

12.5. Asia-Pacific

12.5.1.Market By Grade Type, Market Estimates and Forecast, USD Million

12.5.1.1. R&D

12.5.1.1.1. Viral Vector Development

12.5.1.1.1.1. AVV

12.5.1.1.1.2. Lentivirus

12.5.1.1.1.3. Adenovirus

12.5.1.1.1.4. Retrovirus

12.5.1.1.1.5. Others (Baculovirus, Herpes Simplex Virus (HSV) vectors)

12.5.1.1.2. mRNA Development

12.5.1.1.3. Antibody Development

12.5.1.1.4. DNA Vaccine Development

12.5.1.1.5. Others (Gene Editing Tools Development, RNA Therapeutics Research)

12.5.1.2. GMP Grade

12.5.1.2.1. Viral Vector Production

12.5.1.2.1.1. AAV (Adeno-Associated Virus)

12.5.1.2.1.2. Lentivirus

12.5.1.2.1.3. Adenovirus

12.5.1.2.1.4. Retrovirus

12.5.1.2.1.5. Others (Baculovirus, HSV, Poxvirus, Sendai virus)

12.5.1.2.2. mRNA Therapeutics Production

12.5.1.2.3. Antibody Therapeutics Production

12.5.1.2.4. DNA Vaccine Commercial Manufacturing

12.5.1.2.5. Gene & Cell Therapy Manufacturing

12.5.1.2.6. Others (engineered probiotics, oncolytic viruses)

12.5.2. Market By Workflow, Market Estimates and Forecast, USD Million

12.5.2.1. Upstream Manufacturing

12.5.2.1.1. Vector Amplification & Expansion

12.5.2.1.2. Vector Recovery/Harvesting

12.5.2.2. Downstream Manufacturing

12.5.2.2.1. Purification

12.5.2.2.2. Fill Finish

12.5.3. Market By Development Phase, Market Estimates and Forecast, USD Million

12.5.3.1. Marketed Therapeutics

12.5.3.2. Pre-Clinical Therapeutics

12.5.3.3. Clinical Therapeutics

12.5.4. Market By Disease, Market Estimates and Forecast, USD Million

12.5.4.1. Infectious Disease

12.5.4.2. Cancer

12.5.4.3. Genetic Disorder

12.5.4.4. Others (autoimmune disorders, cardiovascular)

12.5.5. Market By Application, Market Estimates and Forecast, USD Million

12.5.5.1. DNA Vaccines

12.5.5.2. Cell and Gene Therapy

12.5.5.3. Immunotherapy

12.5.5.4. Others (Research reagents, antibody discovery, general molecular biology)

12.5.6. Market By End User, Market Estimates and Forecast, USD Million

12.5.6.1. Biopharmaceutical Companies

12.5.6.2. Contract Manufacturing Organizations (CMOs)

12.5.6.3. Academic & Research Institutes

12.5.6.4. Others (Government labs, non-profit research entities)

12.5.7. Market By Country, Market Estimates and Forecast, USD Million

12.5.7.1. China

12.5.7.2. India

12.5.7.3. Japan

12.5.7.4. South Korea

12.5.7.5. Indonesia

12.5.7.6. Thailand

12.5.7.7. Vietnam

12.5.7.8. Australia

12.5.7.9. New Zeland

12.5.7.10. Rest of APAC

12.6. Latin America

12.6.1.Market By Grade Type, Market Estimates and Forecast, USD Million

12.6.1.1. R&D

12.6.1.1.1. Viral Vector Development

12.6.1.1.1.1. AVV

12.6.1.1.1.2. Lentivirus

12.6.1.1.1.3. Adenovirus

12.6.1.1.1.4. Retrovirus

12.6.1.1.1.5. Others (Baculovirus, Herpes Simplex Virus (HSV) vectors)

12.6.1.1.2. mRNA Development

12.6.1.1.3. Antibody Development

12.6.1.1.4. DNA Vaccine Development

12.6.1.1.5. Others (Gene Editing Tools Development, RNA Therapeutics Research)

12.6.1.2. GMP Grade

12.6.1.2.1. Viral Vector Production

12.6.1.2.1.1. AAV (Adeno-Associated Virus)

12.6.1.2.1.2. Lentivirus

12.6.1.2.1.3. Adenovirus

12.6.1.2.1.4. Retrovirus

12.6.1.2.1.5. Others (Baculovirus, HSV, Poxvirus, Sendai virus)

12.6.1.2.2. mRNA Therapeutics Production

12.6.1.2.3. Antibody Therapeutics Production

12.6.1.2.4. DNA Vaccine Commercial Manufacturing

12.6.1.2.5. Gene & Cell Therapy Manufacturing

12.6.1.2.6. Others (engineered probiotics, oncolytic viruses)

12.6.2.Market By Workflow, Market Estimates and Forecast, USD Million

12.6.2.1. Upstream Manufacturing

12.6.2.1.1. Vector Amplification & Expansion

12.6.2.1.2. Vector Recovery/Harvesting

12.6.2.2. Downstream Manufacturing

12.6.2.2.1. Purification

12.6.2.2.2. Fill Finish

12.6.3.Market By Development Phase, Market Estimates and Forecast, USD Million

12.6.3.1. Marketed Therapeutics

12.6.3.2. Pre-Clinical Therapeutics

12.6.3.3. Clinical Therapeutics

12.6.4.Market By Disease, Market Estimates and Forecast, USD Million

12.6.4.1. Infectious Disease

12.6.4.2. Cancer

12.6.4.3. Genetic Disorder

12.6.4.4. Others (autoimmune disorders, cardiovascular)

12.6.5.Market By Application, Market Estimates and Forecast, USD Million

12.6.5.1. DNA Vaccines

12.6.5.2. Cell and Gene Therapy

12.6.5.3. Immunotherapy

12.6.5.4. Others (Research reagents, antibody discovery, general molecular biology)

12.6.6.Market By End User, Market Estimates and Forecast, USD Million

12.6.6.1. Biopharmaceutical Companies

12.6.6.2. Contract Manufacturing Organizations (CMOs)

12.6.6.3. Academic & Research Institutes

12.6.6.4. Others (Government labs, non-profit research entities)

12.6.7.Market By Country, Market Estimates and Forecast, USD Million

12.6.7.1. Brazil

12.6.7.2. Rest of LATAM

12.7. Middle East & Africa

12.7.1.Market By Grade Type, Market Estimates and Forecast, USD Million

12.7.1.1. R&D

12.7.1.1.1. Viral Vector Development

12.7.1.1.1.1. AVV

12.7.1.1.1.2. Lentivirus

12.7.1.1.1.3. Adenovirus

12.7.1.1.1.4. Retrovirus

12.7.1.1.1.5. Others (Baculovirus, Herpes Simplex Virus (HSV) vectors)

12.7.1.1.2. mRNA Development

12.7.1.1.3. Antibody Development

12.7.1.1.4. DNA Vaccine Development

12.7.1.1.5. Others (Gene Editing Tools Development, RNA Therapeutics Research)

12.7.1.2. GMP Grade

12.7.1.2.1. Viral Vector Production

12.7.1.2.1.1. AAV (Adeno-Associated Virus)

12.7.1.2.1.2. Lentivirus

12.7.1.2.1.3. Adenovirus

12.7.1.2.1.4. Retrovirus

12.7.1.2.1.5. Others (Baculovirus, HSV, Poxvirus, Sendai virus)

12.7.1.2.2. mRNA Therapeutics Production

12.7.1.2.3. Antibody Therapeutics Production

12.7.1.2.4. DNA Vaccine Commercial Manufacturing

12.7.1.2.5. Gene & Cell Therapy Manufacturing

12.7.1.2.6. Others (engineered probiotics, oncolytic viruses)

12.7.2.Market By Workflow, Market Estimates and Forecast, USD Million

12.7.2.1. Upstream Manufacturing

12.7.2.1.1. Vector Amplification & Expansion

12.7.2.1.2. Vector Recovery/Harvesting

12.7.2.2. Downstream Manufacturing

12.7.2.2.1. Purification

12.7.2.2.2. Fill Finish

12.7.3.Market By Development Phase, Market Estimates and Forecast, USD Million

12.7.3.1. Marketed Therapeutics

12.7.3.2. Pre-Clinical Therapeutics

12.7.3.3. Clinical Therapeutics

12.7.4.Market By Disease, Market Estimates and Forecast, USD Million

12.7.4.1. Infectious Disease

12.7.4.2. Cancer

12.7.4.3. Genetic Disorder

12.7.4.4. Others (autoimmune disorders, cardiovascular)

12.7.5.Market By Application, Market Estimates and Forecast, USD Million

12.7.5.1. DNA Vaccines

12.7.5.2. Cell and Gene Therapy

12.7.5.3. Immunotherapy

12.7.5.4. Others (Research reagents, antibody discovery, general molecular biology)

12.7.6.Market By End User, Market Estimates and Forecast, USD Million

12.7.6.1. Biopharmaceutical Companies

12.7.6.2. Contract Manufacturing Organizations (CMOs)

12.7.6.3. Academic & Research Institutes

12.7.6.4. Others (Government labs, non-profit research entities)

12.7.7.Market By Country, Market Estimates and Forecast, USD Million

12.7.7.1. Saudi Arabia

12.7.7.2. UAE

12.7.7.3. South Africa

12.7.7.4. Turkey

12.7.7.5. Rest of MEA

Chapter 13. Competitive Landscape

13.1. Market Revenue Share By Manufacturers

13.2. Mergers & Acquisitions

13.3. Competitor’s Positioning

13.4. Strategy Benchmarking

13.5. Vendor Landscape

13.6. Distributors

13.6.1.North America

13.6.2.Europe

13.6.3.Asia Pacific

13.6.4.Middle East & Africa

13.6.5.Latin America

13.7. Others

Chapter 14. Company Profiles

14.1. Charles River Laboratories

14.1.1. Company Overview

14.1.2. Product & Service Offerings

14.1.3. Strategic Initiatives

14.1.4. Financials

14.1.5. Research Insights

14.2. VGXI, Inc.

14.2.1. Company Overview

14.2.2. Product & Service Offerings

14.2.3. Strategic Initiatives

14.2.4. Financials

14.2.5. Research Insights

14.3. Danaher (Aldevron)

14.3.1. Company Overview

14.3.2. Product & Service Offerings

14.3.3. Strategic Initiatives

14.3.4. Financials

14.3.5. Research Insights

14.4. Kaneka Corp.

14.4.1. Company Overview

14.4.2. Product & Service Offerings

14.4.3. Strategic Initiatives

14.4.4. Financials

14.4.5. Research Insights

14.5. Nature Technology

14.5.1. Company Overview

14.5.2. Product & Service Offerings

14.5.3. Strategic Initiatives

14.5.4. Financials

14.5.5. Research Insights

14.6. Cell and Gene Therapy Catapult

14.6.1. Company Overview

14.6.2. Product & Service Offerings

14.6.3. Strategic Initiatives

14.6.4. Financials

14.6.5. Research Insights

14.7. Eurofins Genomics

14.7.1. Company Overview

14.7.2. Product & Service Offerings

14.7.3. Strategic Initiatives

14.7.4. Financials

14.7.5. Research Insights

14.8. Lonza

14.8.1. Company Overview

14.8.2. Product & Service Offerings

14.8.3. Strategic Initiatives

14.8.4. Financials

14.8.5. Conclusion

14.9. Luminous BioSciences, LLC

14.9.1. Company Overview

14.9.2. Product & Service Offerings

14.9.3. Strategic Initiatives

14.9.4. Financials

14.9.5. Conclusion

14.10. Akron Biotech

14.10.1. Company Overview

14.10.2. Product & Service Offerings

14.10.3. Strategic Initiatives

14.10.4. Financials

14.10.5. Conclusion

14.11. Aldevron LLC by Danaher Corporation

14.11.1. Company Overview

14.11.2. Product & Service Offerings

14.11.3. Strategic Initiatives

14.11.4. Financials

14.11.5. Conclusion

14.12. Almac Group Limited

14.12.1. Company Overview

14.12.2. Product & Service Offerings

14.12.3. Strategic Initiatives

14.12.4. Financials

14.12.5. Conclusion

14.13. Ansa Biotechnologies, Inc.

14.13.1. Company Overview

14.13.2. Product & Service Offerings

14.13.3. Strategic Initiatives

14.13.4. Financials

14.13.5. Conclusion

14.14. Biotium, Inc.

14.14.1. Company Overview

14.14.2. Product & Service Offerings

14.14.3. Strategic Initiatives

14.14.4. Financials

14.14.5. Conclusion

14.15. Biozym Scientific GmbH

14.15.1. Company Overview

14.15.2. Product & Service Offerings

14.15.3. Strategic Initiatives

14.15.4. Financials

14.15.5. Conclusion

14.16. Camena Bioscience

14.16.1. Company Overview

14.16.2. Product & Service Offerings

14.16.3. Strategic Initiatives

14.16.4. Financials

14.16.5. Conclusion

14.17. CD Genomics

14.17.1. Company Overview

14.17.2. Product & Service Offerings

14.17.3. Strategic Initiatives

14.17.4. Financials

14.17.5. Conclusion

14.18. DNA Script

14.18.1. Company Overview

14.18.2. Product & Service Offerings

14.18.3. Strategic Initiatives

14.18.4. Financials

14.18.5. Conclusion

14.19. Evonetix Ltd.

14.19.1. Company Overview

14.19.2. Product & Service Offerings

14.19.3. Strategic Initiatives

14.19.4. Financials

14.19.5. Conclusion

14.20. Merck KGaA

14.20.1. Company Overview

14.20.2. Product & Service Offerings

14.20.3. Strategic Initiatives

14.20.4. Financials

14.20.5. Conclusion

14.21. Thermo Fisher Scientific

14.21.1. Company Overview

14.21.2. Product & Service Offerings

14.21.3. Strategic Initiatives

14.21.4. Financials

14.21.5. Conclusion

14.22. Catalent Pharma Solutions

14.22.1. Company Overview

14.22.2. Product & Service Offerings

14.22.3. Strategic Initiatives

14.22.4. Financials

14.22.5. Conclusion

14.23. Centre for Breakthrough Medicines (CBM)

14.23.1. Company Overview

14.23.2. Product & Service Offerings

14.23.3. Strategic Initiatives

14.23.4. Financials

14.23.5. Conclusion

14.24. ProBio Inc.

14.24.1. Company Overview

14.24.2. Product & Service Offerings

14.24.3. Strategic Initiatives

14.24.4. Financials

14.24.5. Conclusion

14.25. SK pharmteco

14.25.1. Company Overview

14.25.2. Product & Service Offerings

14.25.3. Strategic Initiatives

14.25.4. Financials

14.25.5. Conclusion

Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP. has segmented global Plasmid DNA Manufacturing market on the basis of By Grade Type, By Workflow, Development Phase, By Disease, By Application, By End User and by region for 2019 to 2032.

- Global Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Global Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Global Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Global Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Global Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Global End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- North America

- North America Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- North America Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- North America Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- North America Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- North America Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- North America End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- U.S

- U.S Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- U.S Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- U.S Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- U.S Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- U.S Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- U.S End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Canada

- Canada Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Canada Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Canada Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Canada Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Canada Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Canada End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Mexico

- Mexico Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Mexico Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Mexico Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Mexico Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Mexico Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Mexico End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Europe

- Europe Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Europe Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Europe Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Europe Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Europe Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Europe End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Germany

- Germany Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Germany Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Germany Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Germany Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Germany Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Germany End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- France

- France Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- France Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- France Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- France Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- France Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- France End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- U.K

- U.K Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- U.K Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- U.K Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- U.K Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- U.K Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- U.K End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Italy

- Italy Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Italy Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Italy Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Italy Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Italy Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

Italy End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Spain

- Spain Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Spain Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Spain Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Spain Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Spain Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Spain End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Benelux

- Benelux Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Benelux Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Benelux Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Benelux Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Benelux Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Benelux End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Russia

- Russia Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Russia Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Russia Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Russia Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Russia Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Russia End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Finland

- Finland Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Finland Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Finland Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Finland Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Finland Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Finland End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Sweden

- Sweden Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Sweden Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Sweden Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Sweden Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Sweden Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Sweden End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Rest of Europe

- Rest of Europe Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Rest of Europe Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Rest of Europe Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Rest of Europe Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Rest of Europe Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Rest of Europe End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Asia-Pacific

- Asia-Pacific Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Asia-Pacific Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Asia-Pacific Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Asia-Pacific Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Asia-Pacific Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Asia-Pacific End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- China

- China Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- China Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- China Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- China Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- China Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- China End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- India

- India Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- India Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- India Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- India Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- India Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- India End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Japan

- Japan Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Japan Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Japan Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Japan Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Japan Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Japan End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- South Korea

- South Korea Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- South Korea Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- South Korea Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- South Korea Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- South Korea Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- South Korea End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Indonesia

- Indonesia Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Indonesia Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Indonesia Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Indonesia Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Indonesia Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Indonesia End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Thailand

- Thailand Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Thailand Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Thailand Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Thailand Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Thailand Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Thailand End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

Vietnam

- Vietnam Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Vietnam Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Vietnam Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Vietnam Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Vietnam Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Vietnam End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Australia

- Australia Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Australia Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Australia Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Australia Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Australia Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Australia End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- New Zeeland

- New Zeeland Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- New Zeeland Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- New Zeeland Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- New Zeeland Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- New Zeeland Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- New Zeeland End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others

- Rest of APAC

- Rest of APAC Grade Type Outlook (Revenue, USD Million; 2019-2032)

-

- R&D Grade

-

- GMP Grade

- Rest of APAC Workflow Outlook (Revenue, USD Million; 2019-2032)

-

- Upstream Manufacturing

-

- Downstream Manufacturing

- Rest of APAC Development Phase Outlook (Revenue, USD Million; 2019-2032)

-

- Marketed Therapeutics

-

- Pre-Clinical Therapeutics

-

- Clinical Therapeutics

- Rest of APAC Disease Outlook (Revenue, USD Million; 2019-2032)

-

- Infectious Disease

-

- Cancer

-

- Genetic Disorder

-

- Others

- Rest of APAC Application Outlook (Revenue, USD Million; 2019-2032)

-

- DNA Vaccines

-

- Cell and Gene Therapy

-

- Immunotherapy

-

- Others

- Rest of APAC End User Outlook (Revenue, USD Million; 2019-2032)

-

- Biopharmaceutical Companies

-

- Contract Manufacturing Organizations (CMOs)

-

- Academic & Research Institutes

-

- Others