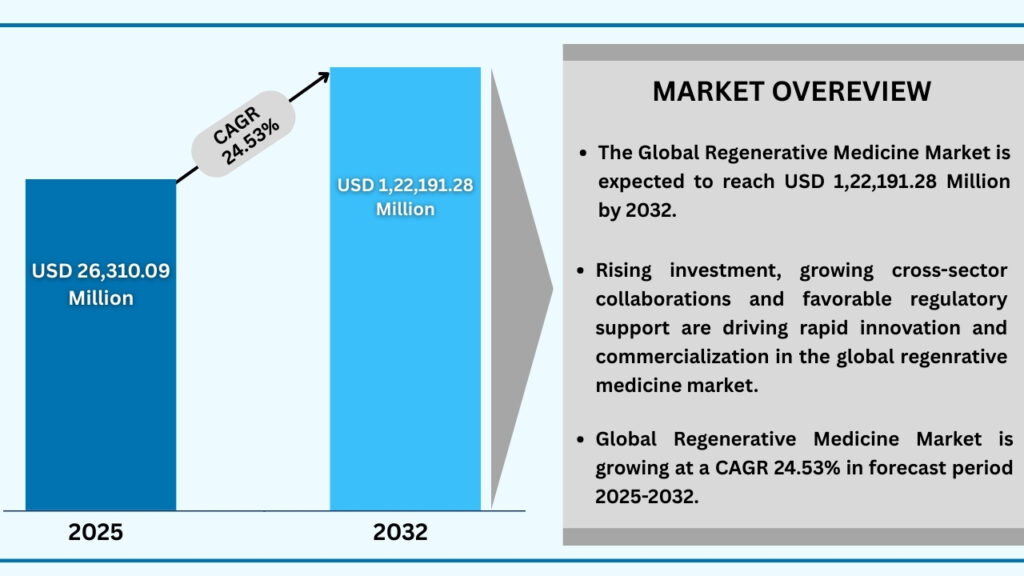

Market Synopsis

The global regenerative medicine market size was USD 21,127.51 million in 2024 and is expected to reach USD 1,22,191.28 million at a CAGR of 24.53% during the forecast period from 2025 to 2032.The global regenerative medicine market is witnessing strong growth, driven by the rising demand for innovative therapies that can repair, replace, or regenerate damaged tissues and organs. Increasing prevalence of chronic diseases, genetic disorders, and age-related conditions is accelerating adoption across healthcare, biotechnology, and pharmaceutical sectors. Limitations of conventional treatment approaches and the need for curative solutions are further propelling the shift toward regenerative therapies, which offer long-term efficacy and functional restoration. Market expansion is supported by advancements in stem cell research, tissue engineering, gene editing, and biomaterials that are broadening applications in orthopaedics, neurology, cardiology, and wound healing. Growing clinical trials, expanding regulatory support, and significant investments from both private and public sectors are fostering innovation and commercialization. Strategic collaborations between academia, industry, and research institutes are also enhancing translational outcomes. With global healthcare expenditure and R&D funding on the rise, regenerative medicine technologies are rapidly emerging as transformative solutions, set to revolutionize personalized medicine, drug development, and advanced therapeutic practices, particularly in regions prioritizing biotech innovation and clinical integration.

Global Regenerative Medicine Market (USD Million)

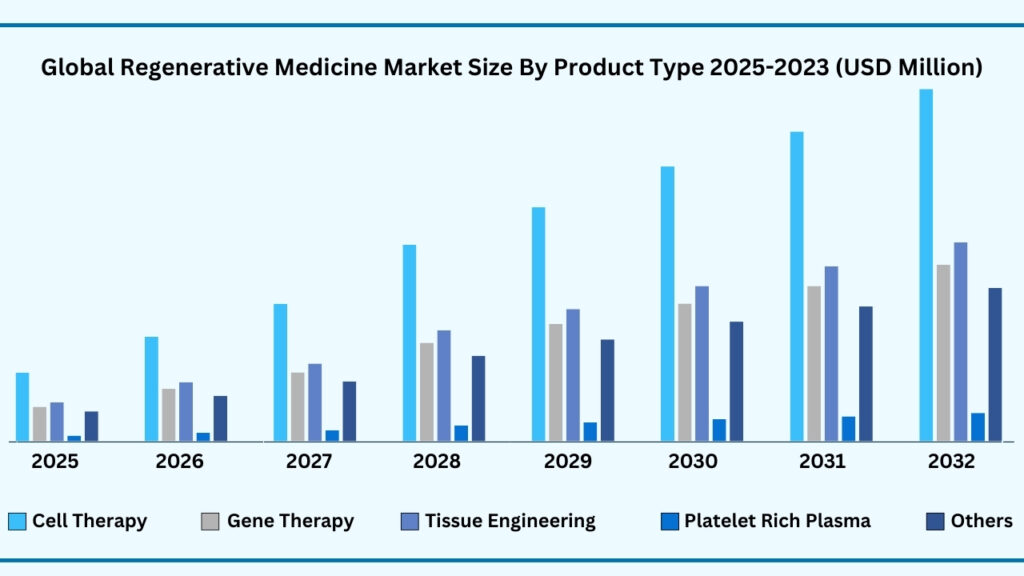

Global Regenerative Medicine Market by Product Type Insights:

Cell Therapy segment accounted for market share of share 44.83% in 2024 in the global regenerative medicine market.

The product type segment of the global regenerative medicine market demonstrates a wide spectrum of therapeutic approaches, with cell therapy emerging as the dominant category, accounting for 44.83% of the market in 2024. This segment alone is projected to expand at a CAGR of 24.57%, reaching USD 54,906.50 million during the forecast period. The rapid adoption of cell-based therapies stems from their unparalleled potential to restore or replace damaged tissues, offering curative options for conditions ranging from haematological disorders to neurodegenerative diseases. Breakthroughs in stem cell technologies, alongside an expanding pipeline of CAR-T and MSC-based therapies, have significantly accelerated clinical translation and commercialization. Companies like Novartis (with its CAR-T therapy Kymriah) and Gilead Sciences (with Yescarta) have already set milestones in oncology, while academic institutions and biotech firms continue advancing next-generation cell therapy platforms for cardiovascular, musculoskeletal, and autoimmune disorders.

Beyond cell therapy, other product types are gaining traction as complementary pillars of regenerative medicine. Gene therapy is making headway with landmark FDA approvals such as Zolgensma for spinal muscular atrophy, reflecting its promise in correcting rare genetic diseases at their root cause. Tissue engineering is reshaping reconstructive medicine by combining biomaterials with living cells to create functional tissue substitutes, with applications ranging from skin grafts to cartilage regeneration. Platelet-Rich Plasma (PRP) therapies are being increasingly utilized in orthopedics and sports medicine to promote healing and reduce recovery times, showcasing high patient acceptance. The “Others” category, encompassing biomaterials, immunotherapy, and small molecules, is equally vital, as innovations in bioactive scaffolds, immune modulation, and biologics are enhancing integration and therapeutic outcomes. Collectively, these sub-segments highlight how regenerative medicine is evolving into a multi-pronged field where synergistic technologies—supported by growing investments, expanding clinical trials, and collaborative networks—are steadily transforming patient care and accelerating the journey toward personalized and durable treatments.

Gobal Regenerative Medicine Market, By Product Type (USD Million)

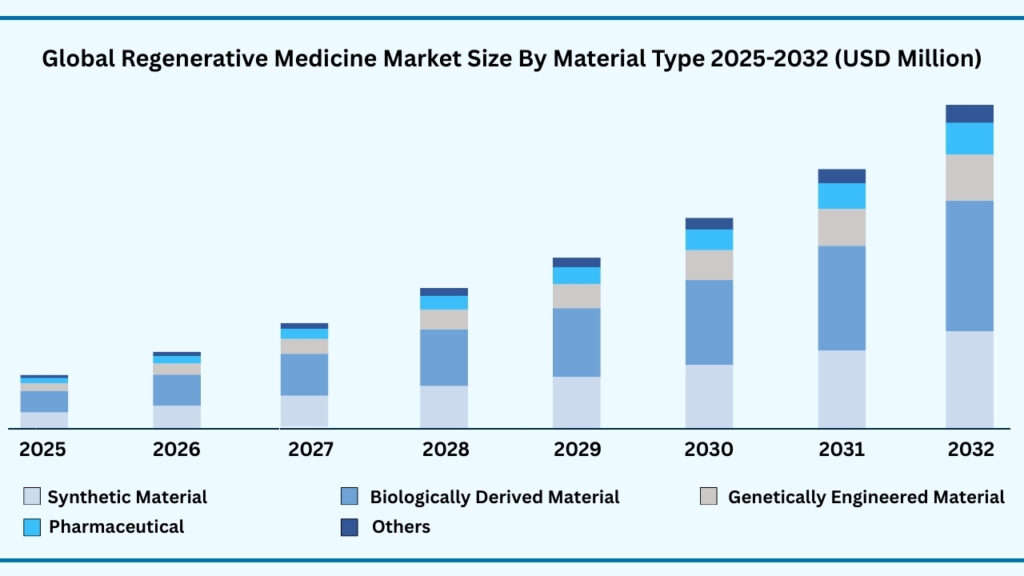

Global Regenerative Medicine Market by Material Type Insights:

Biologically Derived Material segment accounted for market share of share 47.31% in 2024 in the global regenerative medicine market.

The Material Type segment of the global regenerative medicine market highlights the pivotal role of biomaterials in advancing therapeutic applications, with biologically derived materials leading the field at 47.31% of the market share in 2024. This segment is projected to grow at a CAGR of 24.63%, reaching USD 58,178.21 million during the forecast period. The dominance of biologically derived materials, such as collagen, fibrin, hyaluronic acid, and decellularized extracellular matrices, is attributed to their superior biocompatibility and ability to mimic natural tissue environments. These materials provide the structural and biochemical cues necessary for cell adhesion, proliferation, and differentiation, making them indispensable in wound healing, cartilage repair, and cardiovascular regeneration. For example, collagen-based scaffolds are widely used in reconstructive surgeries and skin regeneration therapies, offering clinically validated outcomes and high acceptance among physicians and patients alike.

In parallel, other material categories are shaping the future of regenerative solutions through innovation and specialization. Synthetic materials and genetically engineered materials are gaining traction due to their tuneable properties, scalability, and potential for precise customization. Synthetic polymers, for instance, are being engineered to provide controlled degradation rates and mechanical strength, essential for applications in orthopedics and load-bearing tissues. Genetically engineered biomaterials, meanwhile, are opening doors to novel therapeutic approaches, such as growth factor–loaded matrices and immune-modulating scaffolds, that can actively guide tissue repair. The pharmaceutical segment is also leveraging biomaterial innovations to design advanced drug delivery systems, integrating regenerative capabilities with sustained therapeutic release. The Others category, encompassing artificial materials and man-made polymers, continues to support cost-effective and large-scale production, providing alternatives where natural materials may be limited. Looking forward, the integration of smart biomaterials with emerging technologies like 3D bioprinting and nanotechnology is expected to transform this segment further, enabling next-generation implants, functional tissue substitutes, and precision-targeted regenerative therapies. This multi-faceted evolution underscores the central role of biomaterials in translating regenerative medicine from lab innovation to widespread clinical practice.

Global Regenerative Medicine Market, By Material Type (USD Million)

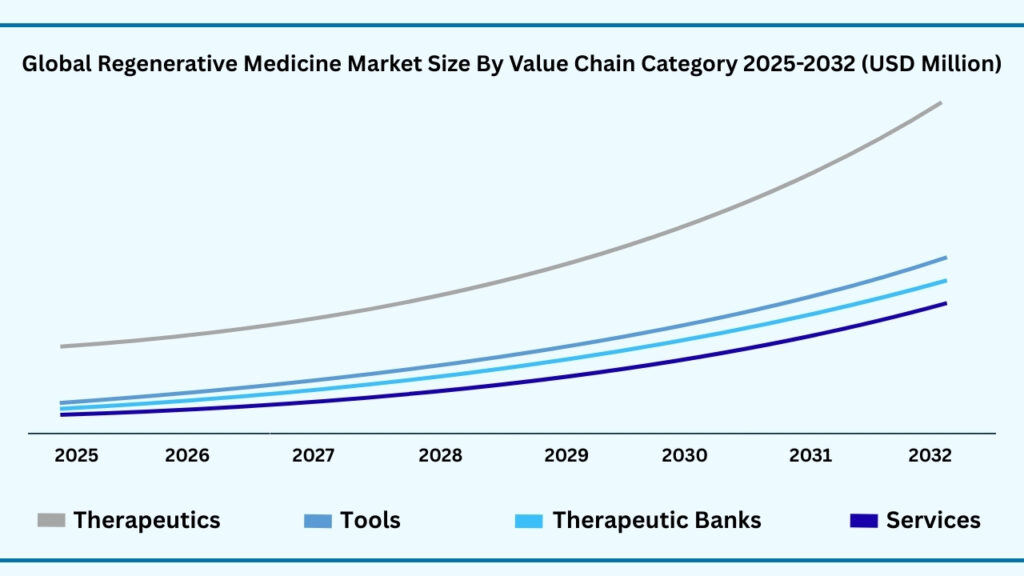

Global Regenerative Medicine Market by Value-Chain Category Type Insights:

Therapeutics segment accounted for market share of share 44.07% in 2024 in the global regenerative medicine market.

The Value-Chain Category segment of the global regenerative medicine market is led by therapeutics, which captured 44.07% of the share in 2024. Revenues from this category are projected to grow at a CAGR of 24.64%, reaching USD 54,235.90 million during the forecast period. The strength of the therapeutics segment lies in its direct clinical impact, as regenerative therapies are being developed and commercialized to address chronic, degenerative, and genetic disorders that lack effective treatments. Breakthroughs in cell therapies, gene therapies, and tissue-engineered products are reshaping patient outcomes in areas such as oncology, neurology, orthopedics, and cardiovascular care. For example, CAR-T therapies from companies like Novartis and Gilead have already set benchmarks in cancer treatment, while tissue-engineered skin substitutes and stem cell–based therapies are being widely explored for wound healing and musculoskeletal repair. The momentum in this sub-segment reflects not only scientific innovation but also growing regulatory support and rising investment in late-stage clinical programs.

Beyond therapeutics, other categories within the value chain play vital roles in enabling the ecosystem. Tools—including culture systems, gene editing platforms, and 3D bioprinters—are accelerating research workflows and expanding translational applications by improving precision and scalability. Therapeutic banks, which store stem cells and other regenerative resources, are becoming increasingly important for both personalized medicine and future-ready treatment strategies, ensuring that patients can access tailored therapies when needed. Meanwhile, services such as contract development, manufacturing, and specialized R&D support are helping bridge the gap between discovery and commercialization, allowing smaller biotech firms and academic groups to scale their innovations efficiently. Collectively, these complementary sub-segments strengthen the regenerative medicine value chain, but therapeutics will remain the cornerstone, driving clinical adoption and revenue growth as the industry continues to transition from experimental research toward mainstream healthcare solutions.

Global Regenerative Medicine Market, By Value-Chain Category (USD Million)

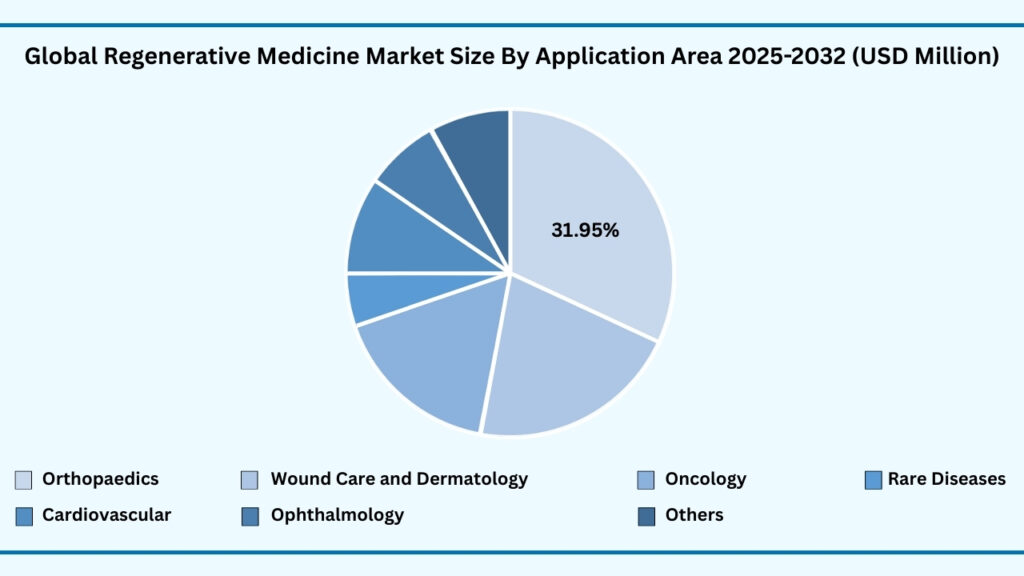

Global Regenerative Medicine Market by Application Area Insights:

Orthopedics segment accounted for market share of share 32% in 2024 in the global regenerative medicine market.

The Application Area segment of the global regenerative medicine market is led by orthopedics, which captured 32% of the share in 2024. Revenues from this category are expected to grow at a CAGR of 24.57%, reaching USD 39,192.65 million during the forecast period. Orthopedics dominates the market due to the rising global burden of musculoskeletal disorders, fractures, cartilage injuries, and degenerative conditions such as osteoarthritis. Regenerative solutions, particularly stem cell–based therapies, bone graft substitutes, and tissue-engineered cartilage, are being widely adopted to restore function, reduce recovery times, and provide alternatives to invasive surgeries. For instance, mesenchymal stem cell (MSC) therapies have shown promise in cartilage repair and spinal injuries, while biomaterial-based implants are increasingly used to accelerate bone regeneration. The appeal of regenerative orthopedics lies in its ability to not just repair but also regenerate damaged tissues, improving long-term patient outcomes.

Beyond orthopedics, other therapeutic areas are steadily gaining ground as regenerative medicine expands its footprint. Wound care and dermatology represent a major growth driver, with tissue-engineered skin grafts and cell-based dressings transforming the treatment of burns, chronic ulcers, and cosmetic applications. Oncology is another fast-evolving area, as cell and gene therapies are being designed to target cancers at the molecular level, supported by initiatives like CAR-T therapies. Regenerative medicine is also making strides in cardiovascular care, where stem cell injections and engineered tissues are being explored to repair heart damage post–myocardial infarction. Meanwhile, ophthalmology applications, such as stem cell–derived retinal therapies, are offering hope for degenerative eye diseases like macular degeneration. The “Others” category, covering neurology and rare diseases, underscores the diversity of applications, with breakthroughs in neural stem cell therapies and gene editing opening possibilities for conditions once deemed untreatable. Together, these areas illustrate how regenerative medicine is not only addressing widespread health challenges like orthopaedic disorders but also pushing into specialized domains, shaping the future of personalized and restorative healthcare.

Global Regenerative Medicine Market, By Application Area (USD Million)

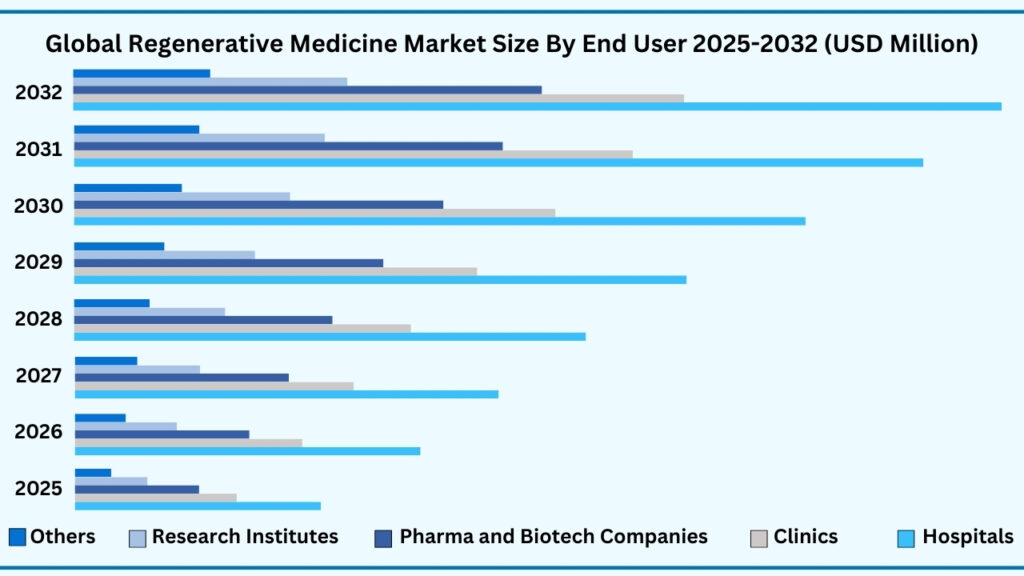

Global Regenerative Medicine Market by End User Insights:

Hospitals segment accounted for market share of share 44.18% in 2024 in the global regenerative medicine market.

The End User segment of the global regenerative medicine market is led by hospitals, which accounted for 44.18% of the share in 2024. Revenues from this category are projected to rise to USD 54,109.16 million during the forecast period, growing at a CAGR of 24.57%. Hospitals dominate due to their central role in delivering advanced therapies ranging from stem cell and gene-based treatments to tissue-engineered implants and wound-healing products. With their advanced infrastructure, specialized surgical units, and access to multidisciplinary teams, hospitals remain the primary point of care for patients requiring regenerative interventions. For instance, several leading hospitals in the U.S. and Europe have established dedicated regenerative medicine centres that perform stem cell transplants, offer cell-based therapies for orthopaedic injuries, and conduct experimental treatments for heart failure and neurological conditions. This growing clinical adoption underscores the hospital sector’s pivotal role in moving regenerative therapies from research settings into everyday patient care.

In addition to hospitals, other end-user segments are playing an increasingly vital role in shaping the regenerative medicine ecosystem. Clinics are emerging as key providers of outpatient regenerative therapies, particularly in orthopedics, dermatology, and aesthetic care. Pharmaceutical and biotechnology companies are driving large-scale innovation by investing heavily in advanced cell therapies, regenerative platforms, and commercialization strategies. Meanwhile, government and academic research institutes are advancing translational research and clinical validation through cross-sector collaborations and large-scale trials. The “Others” category—which includes nonprofit centres, specialty clinics, and contract manufacturers—further strengthens the landscape by contributing specialized expertise, manufacturing support, and patient-cantered services. Collectively, these diverse stakeholders complement the dominance of hospitals and work in tandem to accelerate the global adoption and accessibility of regenerative medicine.

Global Regenerative Medicine Market, By End User (USD million)

Global Regenerative Medicine Market by Region Insights:

North America segment accounted for market share of share 48.70% in 2024 in the global regenerative medicine market.

North America leads the global regenerative medicine market, capturing 48.70% of the share in 2024. Revenues from this region are projected to reach USD 59,653.78 million during the forecast period from 2025 to 2032, growing at a CAGR of 24.57%. The region’s dominance is shaped by strong investments in advanced therapies, robust healthcare infrastructure, and a favorable regulatory environment that supports innovation. The U.S. in particular acts as a hub for regenerative medicine, driven by the presence of leading pharmaceutical and biotechnology firms, world-class research institutes, and numerous clinical trials spanning cell therapies, gene therapies, and tissue-engineered products. For example, the FDA’s Regenerative Medicine Advanced Therapy (RMAT) designation has provided a fast-track pathway for several novel treatments, enabling quicker translation from bench to bedside. Canada also plays a vital role, with its growing network of stem cell research centers and collaborations aimed at expanding access to next-generation therapies.

Beyond North America, other regions are accelerating their presence in regenerative medicine. Europe continues to advance through strong government-backed initiatives and innovation clusters in countries like Germany, the U.K., and Switzerland, where cell and gene therapies are being integrated into healthcare systems. Asia Pacific is emerging as the fastest-growing hub, supported by large patient pools, rapid adoption of stem cell therapies in countries such as Japan, China, and South Korea, and proactive government policies encouraging biotech innovation. Meanwhile, Latin America (LATAM) and the Middle East & Africa (MEA) are building momentum through medical tourism, rising healthcare investments, and partnerships with global players to bring advanced regenerative treatments to local markets. Collectively, while North America anchors the industry today, the global landscape is steadily broadening, ensuring regenerative medicine becomes more accessible and impactful worldwide.

Global Regenerative Medicine Market, By Region (USD million)

Major Companies and Competitive Landscape

The global regenerative medicine market is expanding rapidly, driven by strong investments, scientific advances, and rising clinical adoption. Both leading life sciences companies and emerging biotechs are pursuing collaborations, licensing deals, and M&A to strengthen capabilities and scale innovations. Focus areas include stem cell therapies, gene editing, tissue engineering, and scalable manufacturing to accelerate commercialization and reduce costs. Supportive regulatory pathways and the shift toward personalized medicine are further boosting growth. Key players profiled in the global regenerative medicine market report include:

- Integra LifeSciences Corporation

- Bristol-Myers Squibb Company

- Tissue Regenix

- Smith & Nephew

- MIMEDX

- Novartis AG

- Allergan Aesthetics (AbbVie Inc.)

- Stryker

- American CryoStem Corporation

- Kite (Gilead Sciences, Inc.)

- AlloSource

- bluebird bio, Inc.

- CRISPR Therapeutics

- Janssen Global Services, LLC (Johnson & Johnson Services, Inc.)

- Tegoscience

- Mesoblast Limited

- Organogenesis, Inc.

- Vericel Corporation

- Medtronic plc

- Zimmer Biomet

- Aroa Biosurgery

- Sana Biotechnology, Inc.

- Spark Therapeutics AG

- VivoTex

- NurExone Biologic

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 26,310.09 Million |

| CAGR (2024–2032) | 24.53% |

| Revenue forecast to 2033 | USD 1,22,191.28 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Product Type, By Material Type, By Value-Chain Category, By Application Area, By End User and By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, UAE, South Africa, Turkey, Rest of MEA |

| Key companies profiled | Integra LifeSciences Corporation, Bristol-Myers Squibb Company, Tissue Regenix, Smith & Nephew, MIMEDX, Novartis AG, Allergan Aesthetics (AbbVie Inc.), Stryker, American CryoStem Corporation, Kite (Gilead Sciences, Inc.), AlloSource, bluebird bio, Inc., CRISPR Therapeutics, Janssen Global Services, LLC (Johnson & Johnson Services, Inc.), Tegoscience, Mesoblast Limited, Organogenesis, Inc., Vericel Corporation, Medtronic plc, Zimmer Biomet, Aroa Biosurgery, Sana Biotechnology, Inc., Spark Therapeutics AG, VivoTex, and NurExone Biologic. |

| Customization scope | 10 hours of free customization and expert consultation |

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of global regenerative medicine market

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1.Primary

2.1.2.Secondary

2.1.3.Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1.Market value

2.3.2.Market volume

2.3.3.Exchange rate

2.3.4.Price

2.3.5.Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2019–2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10. Formulation & manufacturing

4.11. Distribution & retail

4.12. Import-export analysis

4.13. Brand comparative analysis

4.14. Technological advancements

4.15. Porter’s five force

4.15.1. Threat of new entrants

4.15.1.1. Capital requirment

4.15.1.2. Product knowledge

4.15.1.3. Technical knowledge

4.15.1.4. Customer relation

4.15.1.5. Access to appliation and technology

4.15.2. Threat of substitutes

4.15.2.1. Cost

4.15.2.2. Performance

4.15.2.3. Availability

4.15.2.4. Technical knowledge

4.15.2.5. Durability

4.15.3. Bargainning power of buyers

4.15.3.1. Numbers of buyers relative to suppliers

4.15.3.2. Product differentiation

4.15.3.3. Threat of forward integration

4.15.3.4. Buyers volume

4.15.4. Bargainning power of suppliers

4.15.4.1. Suppliers concentration

4.15.4.2. Buyers switching cost to other suppliers

4.15.4.3. Threat of backward integration

4.15.5. Bargainning power of suppliers

4.15.5.1. Industry concentration

4.15.5.2. Industry growth rate

4.15.5.3. Product differentiation

4.15.6. Patent analysis

4.16. Patent quality and strength

4.17. Regulation coverage

4.18. Pricing analysis

4.19. Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1.Increasing prevalence of chronic diseases, genetic disorders, and degenerative

conditions fueling demand for regenerative therapies

5.1.2.Advances in stem cell research, tissue engineering, and biomaterials accelerating

clinical applications

5.1.3.Rising investment by pharma/biotech companies and government initiatives to support

regenerative medicine R&D

5.2. Restraints

5.2.1.High cost of regenerative therapies, limiting accessibility and widespread adoption

5.2.2.Manufacturing complexity and scalability challenges in cell and gene-based therapies

5.3. Opportunities

5.3.1.Growing adoption of personalized and precision medicine approaches integrating

regenerative therapies

5.3.2.Expansion of 3D bioprinting, advanced biomaterials, and exosome-based therapies for

tissue regeneration

5.3.3.Rising potential in organ transplantation alternatives, wound healing, and

musculoskeletal repair

5.4. Threat

5.4.1.Regulatory uncertainty regarding long-term safety, efficacy validation, and global

approval standards

5.4.2.Intellectual Property constraints on media, matrices, and Patient-Derived Organoids

derivation methods limiting broad adoption

Chapter 6. Global Regenrative Medicine Market By Product Type Insights & Trends, Revenue

(USD Million) , 2019–2032

6.1. Product Type Dynamics & Market Share, 2019–2032

6.1.1.Cell Therapy

6.1.2.Gene Therapy

6.1.3.Tissue Engineering

6.1.4.Platelet Rich Plasma

6.1.5.Others (Biomaterial, Immunotherapy, Small molecule & biologics)

Chapter 7. Global Regenerative Medicine Market By Material Type Insights & Trends, Revenue

(USD Million) , 2019–2032

7.1. Material Type Dynamics & Market Share, 2019–2032

7.1.1.Synthetic Material

7.1.2.Biologically Derived Material

7.1.3.Genetically Engineered Material

7.1.4.Pharmaceutical

7.1.5.Others (Artificial Materials, Man-Made Polymers)

Chapter 8. Global Regenerative Medicine Market By Value-Chain Category Insights & Trends,

Revenue (USD Million) , 2019–2032

8.1. Value-Chain Category Dynamics & Market Share, 2019–2032

8.1.1.Therapeutics

8.1.2.Tools

8.1.3.Therapeutic Banks

8.1.4.Services

Chapter 9. Global Regenerative Medicine Market By Application Area Insights & Trends,

Revenue (USD Million) , 2019–2032

9.1. Application Area Dynamics & Market Share, 2019–2032

9.1.1.Orthopaedics

9.1.2.Wound Care and Dermatology

9.1.3.Oncology

9.1.4.Rare Diseases

9.1.5.Cardiovascular

9.1.6.Ophthalmology

9.1.7.Others (Neurology, Rare Diseases)

Chapter 10. Global Regenerative Medicine Market By End User Insights & Trends, Revenue (USD

Million) , 2019–2032

10.1. End User Dynamics & Market Share, 2019–2032

10.1.1.Pharmaceutical and Biotechnology Companies

10.1.2.Government & Academic Research Institutes

10.1.3.Others (non-profit centers, specialty clinics, contract manufacturers)

Chapter 11. Global Regenerative Medicine Market Regional Outlook

11.1. Global Regenerative MedicineMarket Share By Region, 2019–2032

11.2. North America

11.2.1. Market By Product Type, Market Estimates and Forecast, USD Million, 2019–2032

11.2.1.1. Cell Therapy

11.2.1.2. Gene Therapy

11.2.1.3. Tissue Engineering

11.2.1.4. Platelet Rich Plasma

11.2.1.5. Others (Biomaterial, Immunotherapy, Small molecule & biologics)

11.2.2. Market By Material Type, Market Estimates and Forecast, USD Million, 2019–2032

11.2.2.1. Synthetic Material

11.2.2.2. Biologically Derived Material

11.2.2.3. Genetically Engineered Material

11.2.2.4. Pharmaceutical

11.2.2.5. Others (Artificial Materials, Man-Made Polymers)

11.2.3. Market By Value-Chain Category, Market Estimates and Forecast, USD Million, 2019–

2032

11.2.3.1. Therapeutics

11.2.3.2. Tools

11.2.3.3. Therapeutic Banks

11.2.3.4. Services

11.2.4. Market By Application Area, Market Estimates and Forecast, USD Million, 2019–2032

11.2.4.1. Orthopaedics

11.2.4.2. Wound Care and Dermatology

11.2.4.3. Oncology

11.2.4.4. Rare Diseases

11.2.4.5. Cardiovascular

11.2.4.6. Ophthalmology

11.2.4.7. Others (Neurology, Rare Diseases)

11.2.5. Market By End User, Market Estimates and Forecast, USD Million, 2019–2032

11.2.5.1. Pharmaceutical and Biotechnology Companies

11.2.5.2. Government & Academic Research Institutes

11.2.5.3. Others (non-profit centers, specialty clinics, contract manufacturers)

11.2.6. Market By Country, Market Estimates and Forecast, USD Million, 2019–2032

11.2.6.1. US

11.2.6.2. Canada

11.2.6.3. Mexico

11.3. Europe

11.3.1.Market By Product Type, Market Estimates and Forecast, USD Million, 2019–2032

11.3.1.1. Cell Therapy

11.3.1.2. Gene Therapy

11.3.1.3. Tissue Engineering

11.3.1.4. Platelet Rich Plasma

11.3.1.5. Others (Biomaterial, Immunotherapy, Small molecule & biologics)

11.3.2.Market By Material Type, Market Estimates and Forecast, USD Million, 2019–2032

11.3.2.1. Synthetic Material

11.3.2.2. Biologically Derived Material

11.3.2.3. Genetically Engineered Material

11.3.2.4. Pharmaceutical

11.3.2.5. Others (Artificial Materials, Man-Made Polymers)

11.3.3.Market By Value-Chain Category, Market Estimates and Forecast, USD Million, 2019–

2032

11.3.3.1. Therapeutics

11.3.3.2. Tools

11.3.3.3. Therapeutic Banks

11.3.3.4. Services

11.3.4.Market By Application Area, Market Estimates and Forecast, USD Million, 2019–2032

11.3.4.1. Orthopaedics

11.3.4.2. Wound Care and Dermatology

11.3.4.3. Oncology

11.3.4.4. Rare Diseases

11.3.4.5. Cardiovascular

11.3.4.6. Ophthalmology

11.3.4.7. Others (Neurology, Rare Diseases)

11.3.5.Market By End User, Market Estimates and Forecast, USD Million, 2019–2032

11.3.5.1. Pharmaceutical and Biotechnology Companies

11.3.5.2. Government & Academic Research Institutes

11.3.5.3. Others (non-profit centers, specialty clinics, contract manufacturers)

11.3.6.Market By Country, Market Estimates and Forecast, USD Million, 2019–2032

11.3.6.1. Germany

11.3.6.2. France

11.3.6.3. U.K

11.3.6.4. Italy

11.3.6.5. Spain

11.3.6.6. Benelux

11.3.6.7. Russia

11.3.6.8. Finland

11.3.6.9. Sweden

11.3.6.10.Rest Of Europe

11.4. Asia-Pacific

11.4.1. Market By Product Type, Market Estimates and Forecast, USD Million, 2019–2032

11.4.1.1. Cell Therapy

11.4.1.2. Gene Therapy

11.4.1.3. Tissue Engineering

11.4.1.4. Platelet Rich Plasma

11.4.1.5. Others (Biomaterial, Immunotherapy, Small molecule & biologics)

11.4.2.Market By Material Type, Market Estimates and Forecast, USD Million, 2019–2032

11.4.2.1. Synthetic Material

11.4.2.2. Biologically Derived Material

11.4.2.3. Genetically Engineered Material

11.4.2.4. Pharmaceutical

11.4.2.5. Others (Artificial Materials, Man-Made Polymers)

11.4.3.Market By Value-Chain Category, Market Estimates and Forecast, USD Million, 2019–

2032

11.4.3.1. Therapeutics

11.4.3.2. Tools

11.4.3.3. Therapeutic Banks

11.4.3.4. Services

11.4.4.Market By Application Area, Market Estimates and Forecast, USD Million, 2019–2032

11.4.4.1. Orthopaedics

11.4.4.2. Wound Care and Dermatology

11.4.4.3. Oncology

11.4.4.4. Rare Diseases

11.4.4.5. Cardiovascular

11.4.4.6. Ophthalmology

11.4.4.7. Others (Neurology, Rare Diseases)

11.4.5.Market By End User, Market Estimates and Forecast, USD Million, 2019–2032

11.4.5.1. Pharmaceutical and Biotechnology Companies

11.4.5.2. Government & Academic Research Institutes

11.4.5.3. Others (non-profit centers, specialty clinics, contract manufacturers)

11.4.6.Market By Country, Market Estimates and Forecast, USD Million, 2019–2032

11.4.6.1. China

11.4.6.2. India

11.4.6.3. Japan

11.4.6.4. South Korea

11.4.6.5. Indonesia

11.4.6.6. Thailand

11.4.6.7. Vietnam

11.4.6.8. Australia

11.4.6.9. New Zeland

11.4.6.10.Rest of APAC

11.5. Latin America

11.5.1. Market By Product Type, Market Estimates and Forecast, USD Million, 2019–2032

11.5.1.1. Cell Therapy

11.5.1.2. Gene Therapy

11.5.1.3. Tissue Engineering

11.5.1.4. Platelet Rich Plasma

11.5.1.5. Others (Biomaterial, Immunotherapy, Small molecule & biologics)

11.5.2.Market By Material Type, Market Estimates and Forecast, USD Million, 2019–2032

11.5.2.1. Synthetic Material

11.5.2.2. Biologically Derived Material

11.5.2.3. Genetically Engineered Material

11.5.2.4. Pharmaceutical

11.5.2.5. Others (Artificial Materials, Man-Made Polymers)

11.5.3.Market By Value-Chain Category, Market Estimates and Forecast, USD Million, 2019–

2032

11.5.3.1. Therapeutics

11.5.3.2. Tools

11.5.3.3. Therapeutic Banks

11.5.3.4. Services

11.5.4.Market By Application Area, Market Estimates and Forecast, USD Million, 2019–2032

11.5.4.1. Orthopaedics

11.5.4.2. Wound Care and Dermatology

11.5.4.3. Oncology

11.5.4.4. Rare Diseases

11.5.4.5. Cardiovascular

11.5.4.6. Ophthalmology

11.5.4.7. Others (Neurology, Rare Diseases)

11.5.5.Market By End User, Market Estimates and Forecast, USD Million, 2019–2032

11.5.5.1. Pharmaceutical and Biotechnology Companies

11.5.5.2. Government & Academic Research Institutes

11.5.5.3. Others (non-profit centers, specialty clinics, contract manufacturers)

11.5.6.Market By Country, Market Estimates and Forecast, USD Million, 2019–2032

11.5.6.1. Brazil

11.5.6.2. Rest of LATAM

11.6. Middle East & Africa

11.6.1. Market By Product Type, Market Estimates and Forecast, USD Million, 2019–2032

11.6.1.1. Cell Therapy

11.6.1.2. Gene Therapy

11.6.1.3. Tissue Engineering

11.6.1.4. Platelet Rich Plasma

11.6.1.5. Others (Biomaterial, Immunotherapy, Small molecule & biologics)

11.6.2.Market By Material Type, Market Estimates and Forecast, USD Million, 2019–2032

11.6.2.1. Synthetic Material

11.6.2.2. Biologically Derived Material

11.6.2.3. Genetically Engineered Material

11.6.2.4. Pharmaceutical

11.6.2.5. Others (Artificial Materials, Man-Made Polymers)

11.6.3.Market By Value-Chain Category, Market Estimates and Forecast, USD Million, 2019–

2032

11.6.3.1. Therapeutics

11.6.3.2. Tools

11.6.3.3. Therapeutic Banks

11.6.3.4. Services

11.6.4.Market By Application Area, Market Estimates and Forecast, USD Million, 2019–2032

11.6.4.1. Orthopaedics

11.6.4.2. Wound Care and Dermatology

11.6.4.3. Oncology

11.6.4.4. Rare Diseases

11.6.4.5. Cardiovascular

11.6.4.6. Ophthalmology

11.6.4.7. Others (Neurology, Rare Diseases)

11.6.5.Market By End User, Market Estimates and Forecast, USD Million, 2019–2032

11.6.5.1. Pharmaceutical and Biotechnology Companies

11.6.5.2. Government & Academic Research Institutes

11.6.5.3. Others (non-profit centers, specialty clinics, contract manufacturers)

11.6.6.Market By Country, Market Estimates and Forecast, USD Million, 2019–2032

11.6.6.1. Saudi Arabia

11.6.6.2. UAE

11.6.6.3. South Africa

11.6.6.4. Turkey

11.6.6.5. Rest of MEA

Chapter 12. Competitive Landscape

12.1. Market Revenue Share By Manufacturers

12.2. Mergers & Acquisitions

12.3. Competitor’s Positioning

12.4. Strategy Benchmarking

12.5. Vendor Landscape

12.6. Distributors

12.6.1.North America

12.6.2.Europe

12.6.3.Asia Pacific

12.6.4.Middle East & Africa

12.6.5.Latin America

12.7. Others

Chapter 13. Company Profiles

13.1. Integra LifeSciences Corporation

13.1.1. Company Overview

13.1.2. Product & Service Offerings

13.1.3. Strategic Initiatives

13.1.4. Financials

13.1.5. Emergen Research Insights

13.2. Bristol-Myers Squibb Company

13.2.1. Company Overview

13.2.2. Product & Service Offerings

13.2.3. Strategic Initiatives

13.2.4. Financials

13.2.5. Emergen Research Insights

13.3. Tissue Regenix

13.3.1. Company Overview

13.3.2. Product & Service Offerings

13.3.3. Strategic Initiatives

13.3.4. Financials

13.3.5. Emergen Research Insights

13.4. Smith & Nephew

13.4.1. Company Overview

13.4.2. Product & Service Offerings

13.4.3. Strategic Initiatives

13.4.4. Financials

13.4.5. Emergen Research Insights

13.5. MIMEDX

13.5.1. Company Overview

13.5.2. Product & Service Offerings

13.5.3. Strategic Initiatives

13.5.4. Financials

13.5.5. Emergen Research Insights

13.6. Novartis AG

13.6.1. Company Overview

13.6.2. Product & Service Offerings

13.6.3. Strategic Initiatives

13.6.4. Financials

13.6.5. Emergen Research Insights

13.7. Allergan Aesthetics (AbbVie Inc.)

13.7.1. Company Overview

13.7.2. Product & Service Offerings

13.7.3. Strategic Initiatives

13.7.4. Financials

13.7.5. Emergen Research Insights

13.8. Stryker

13.8.1. Company Overview

13.8.2. Product & Service Offerings

13.8.3. Strategic Initiatives

13.8.4. Financials

13.8.5. Conclusion

13.9. American CryoStem Corporation

13.9.1. Company Overview

13.9.2. Product & Service Offerings

13.9.3. Strategic Initiatives

13.9.4. Financials

13.9.5. Conclusion

13.10. Kite (Gilead Sciences, Inc.)

13.10.1. Company Overview

13.10.2. Product & Service Offerings

13.10.3. Strategic Initiatives

13.10.4. Financials

13.10.5. Conclusion

13.11. AlloSource

13.11.1. Company Overview

13.11.2. Product & Service Offerings

13.11.3. Strategic Initiatives

13.11.4. Financials

13.11.5. Conclusion

13.12. Bluebird bio, Inc.

13.12.1. Company Overview

13.12.2. Product & Service Offerings

13.12.3. Strategic Initiatives

13.12.4. Financials

13.12.5. Conclusion

13.13. CRISPR Therapeutics

13.13.1. Company Overview

13.13.2. Product & Service Offerings

13.13.3. Strategic Initiatives

13.13.4. Financials

13.13.5. Conclusion

13.14. Janssen Global Services, LLC

13.14.1. Company Overview

13.14.2. Product & Service Offerings

13.14.3. Strategic Initiatives

13.14.4. Financials

13.14.5. Conclusion

13.15. Tegoscience

13.15.1. Company Overview

13.15.2. Product & Service Offerings

13.15.3. Strategic Initiatives

13.15.4. Financials

13.15.5. Conclusion

13.16. Mesoblast Limited

13.16.1. Company Overview

13.16.2. Product & Service Offerings

13.16.3. Strategic Initiatives

13.16.4. Financials

13.16.5. Conclusion

13.17. Organogenesis, Inc.

13.17.1. Company Overview

13.17.2. Product & Service Offerings

13.17.3. Strategic Initiatives

13.17.4. Financials

13.17.5. Conclusion

13.18. Vericel Corporation

13.18.1. Company Overview

13.18.2. Product & Service Offerings

13.18.3. Strategic Initiatives

13.18.4. Financials

13.18.5. Conclusion

13.19. Medtronic plc

13.19.1. Company Overview

13.19.2. Product & Service Offerings

13.19.3. Strategic Initiatives

13.19.4. Financials

13.19.5. Conclusion

13.20. Zimmer Biomet

13.20.1. Company Overview

13.20.2. Product & Service Offerings

13.20.3. Strategic Initiatives

13.20.4. Financials

13.20.5. Conclusion

13.21. Aroa Biosurgery

13.21.1. Company Overview

13.21.2. Product & Service Offerings

13.21.3. Strategic Initiatives

13.21.4. Financials

13.21.5. Conclusion

13.22. Sana Biotechnology, Inc.

13.22.1. Company Overview

13.22.2. Product & Service Offerings

13.22.3. Strategic Initiatives

13.22.4. Financials

13.22.5. Conclusion

13.23. Spark Therapeutics AG

13.23.1. Company Overview

13.23.2. Product & Service Offerings

13.23.3. Strategic Initiatives

13.23.4. Financials

13.23.5. Conclusion

13.24. VivoTex

13.24.1. Company Overview

13.24.2. Product & Service Offerings

13.24.3. Strategic Initiatives

13.24.4. Financials

13.24.5. Conclusion

13.25. NurExone Biologic

13.25.1. Company Overview

13.25.2. Product & Service Offerings

13.25.3. Strategic Initiatives

13.25.4. Financials

13.25.5. Conclusion

Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP. has segmented global Regenerative Medicine market on the basis of By Product Type, By Material Type, Value-Chain Category, By Application Area, By End User and by region for 2019 to 2032.

- Global Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Global Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Global Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Global Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Global Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Global End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- North America

- North America Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- North America Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- North America Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- North America Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- North America Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- North America End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- U.S

- U.S Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- U.S Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- U.S Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- U.S Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- U.S Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- U.S End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Canada

- Canada Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Canada Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Canada Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Canada Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Canada Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Canada End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Mexico

- Mexico Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Mexico Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Mexico Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Mexico Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Mexico Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Mexico End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Europe

- Europe Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Europe Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Europe Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Europe Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Europe Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Europe End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Germany

- Germany Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Germany Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Germany Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Germany Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Germany Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Germany End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- France

- France Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- France Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- France Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- France Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- France Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- France End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- U.K

- U.K Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- U.K Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- U.K Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- U.K Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- U.K Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- U.K End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Italy

- Italy Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Italy Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Italy Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Italy Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Italy Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Italy End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Spain

- Spain Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Spain Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Spain Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Spain Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Spain Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Spain End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Benelux

- Benelux Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Benelux Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Benelux Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Benelux Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Benelux Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Benelux End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Russia

- Russia Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Russia Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Russia Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Russia Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Russia Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Russia End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Finland

- Finland Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Finland Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Finland Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Finland Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Finland Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Finland End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Sweden

- Sweden Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Sweden Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Sweden Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Sweden Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Sweden Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Sweden End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Rest of Europe

- Rest of Europe Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Rest of Europe Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Rest of Europe Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Rest of Europe Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Rest of Europe Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Rest of Europe End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Asia-Pacific

- Asia-Pacific Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Asia-Pacific Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Asia-Pacific Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Asia-Pacific Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Asia-Pacific Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Asia-Pacific End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- China

- China Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- China Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- China Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- China Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- China Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- China End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- India

- India Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- India Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- India Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- India Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- India Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- India End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Japan

- Japan Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Japan Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Japan Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Japan Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Japan Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Japan End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- South Korea

- South Korea Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- South Korea Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- South Korea Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- South Korea Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- South Korea Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- South Korea End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Indonesia

- Indonesia Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Indonesia Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Indonesia Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Indonesia Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Indonesia Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Indonesia End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Thailand

- Thailand Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Thailand Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Thailand Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Thailand Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Thailand Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Thailand End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Vietnam

- Vietnam Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Vietnam Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Vietnam Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Vietnam Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Vietnam Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-

- Oncology

-

- Rare Diseases

-

- Cardiovascular

-

- Ophthalmology

-

- Others (Neurology, Rare Diseases)

- Vietnam End User Outlook (Revenue, USD Million; 2019-2032)

-

- Pharmaceutical and Biotechnology Companies

-

- Government & Academic Research Institutes

-

- Others (non-profit centers, specialty clinics, contract manufacturers)

- Australia

- Australia Product Type Outlook (Revenue, USD Million; 2019-2032)

-

- Cell Therapy

-

- Gene Therapy

-

- Tissue Engineering

-

- Platelet Rich Plasma

-

- Others (Biomaterial, Immunotherapy, Small molecule & biologics)

- Australia Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Synthetic Material

-

- Biologically Derived Material

-

- Genetically Engineered Material

-

- Pharmaceutical

-

- Others (Artificial Materials, Man-Made Polymers)

- Australia Material Type Outlook (Revenue, USD Million; 2019-2032)

-

- Induced Pluripotent Stem Cells (iPSCs)

-

- Embryonic Stem Cells (ESCs)

-

- Adult Stem Cells

- Australia Value-Chain Category Outlook (Revenue, USD Million; 2019-2032)

-

- Therapeutics

-

- Tools

-

- Therapeutic Banks

-

- Services

- Australia Application Area Outlook (Revenue, USD Million; 2019-2032)

-

- Orthopedics

-

- Wound Care and Dermatology

-