Market Synopsis

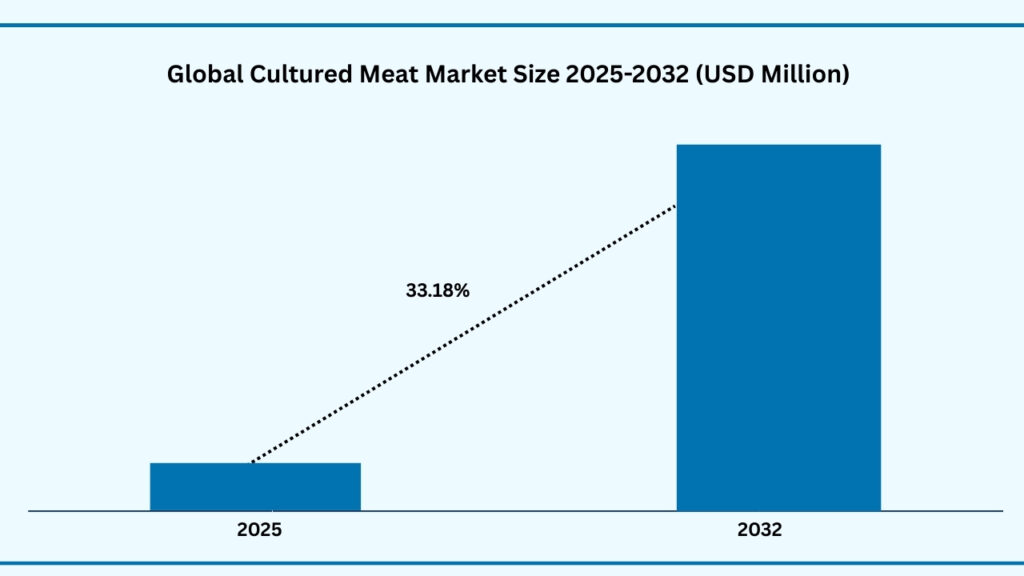

The global Cultured meat market size was USD 360.75 Million in 2024 and is expected to reach USD 3,534.86 million at a CAGR of 33.18%% during the forecast period. The global cultured meat market was valued at USD 360.75 million in 2024 and is projected to reach USD 3,534.86 million by 2032, growing at a strong CAGR of 33.18%. The growth is being fueled by increasing demand for sustainable and cruelty-free protein alternatives, rising concerns over the environmental impact of traditional meat production, and the health benefits associated with lab-grown meat, which eliminates risks linked to antibiotics, hormones, and zoonotic diseases. In addition, technological advancements in cellular agriculture, bioreactors, and growth media are reducing production costs and improving scalability, while government initiatives and rising venture capital funding are further accelerating commercialization.

Regionally, North America currently dominates the market due to high investments, an established startup ecosystem, and supportive regulatory developments. Europe is also witnessing significant growth, supported by strict animal welfare policies and strong consumer awareness of sustainability. However, Asia-Pacific is projected to be the fastest-growing region, driven by a large population, rising protein consumption, and supportive initiatives in countries such as Singapore, Japan, and China. The Middle East, particularly Israel and the UAE, is also emerging as a promising hub, as governments invest in food security and advanced food technologies.

Global Cultured Meat Market (USD Million)

Global Cultured Meat Market By Source Type Insights:

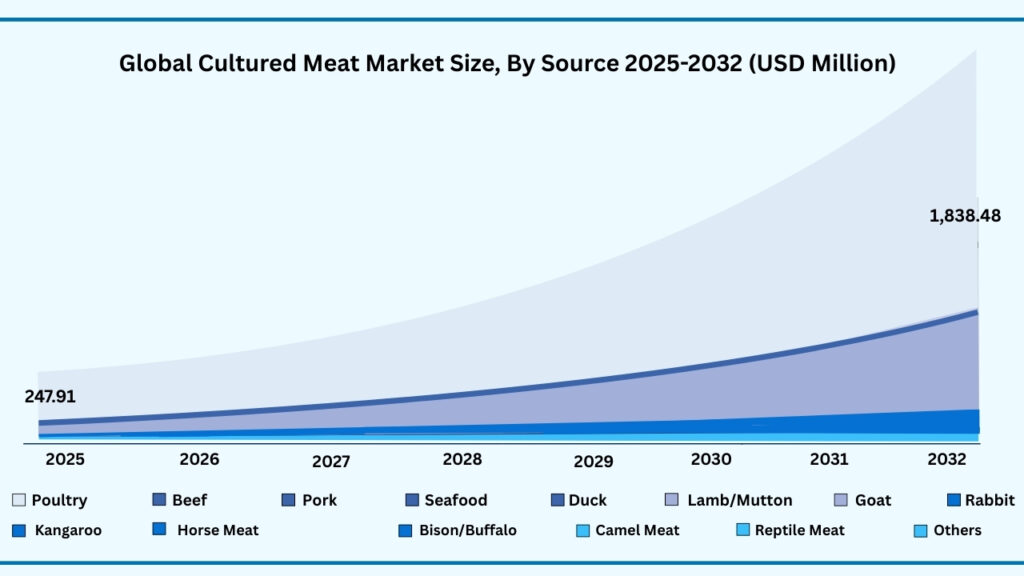

Poultry segment accounted for market share of share 52.11% in 2024 in the global cultured meat market.

The poultry segment accounted for the largest share of the global Cultured meat market in 2024, representing 52.11% of total revenues. Poultry segment is expected to register a CAGR of 33.14% during the forecast year from 2025 to 2032 and expected to reach USD 1,838.48 million in 2032. This high growth is primarily driven by the fact that poultry is the most widely consumed meat globally, offering a lower-cost and more familiar entry point for cultured meat adoption compared to other meat categories such as beef or seafood. The relatively shorter production cycles, lower complexity in cell cultivation, and lower cost of scaling poultry cells make it commercially more viable for producers, helping them reach cost parity faster.

In addition, growing consumer demand for healthier, antibiotic-free, and hormone-free chicken is accelerating acceptance of lab-grown poultry products, especially among health-conscious and environmentally aware consumers. Supportive regulatory approvals, particularly in Asia (e.g., Singapore) and expected in North America and Europe, along with strong investments from cultured meat startups focusing on poultry, are further boosting market penetration. Moreover, the ability of poultry-based cultured meat to be used in a variety of widely accepted formats such as nuggets, patties, and ready-to-cook products enhances its appeal, thereby positioning the poultry segment for rapid and sustained growth over the forecast period.

Global Cultured Meat Market by Source Type (USD Million)

Global Cultured Meat Maret by Production Technique Insights:

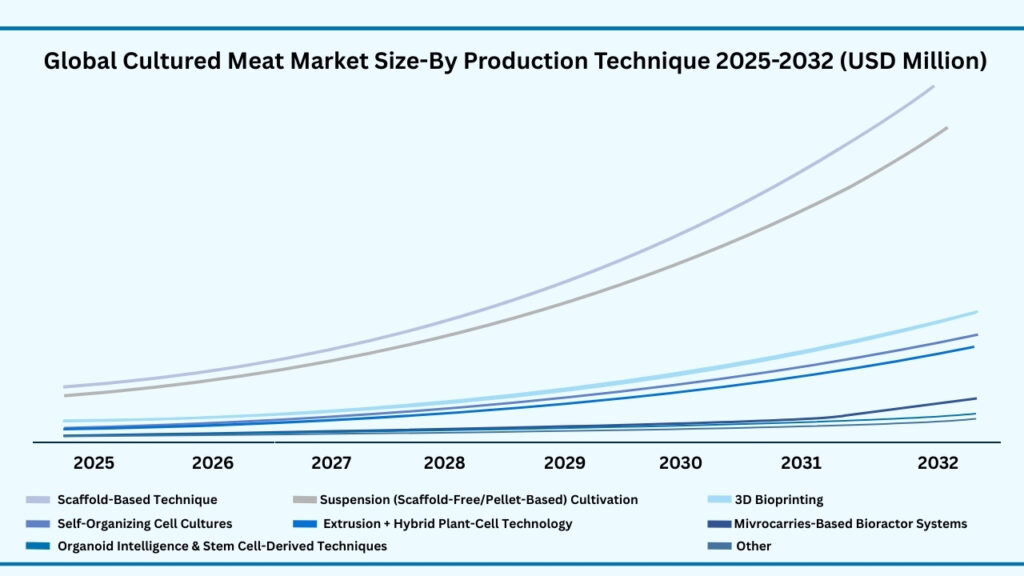

Scaffold-Based Technique segment accounted for the largest market share of share 34.24% in 2024 in the global Cultured meat market.

Based on the production technique, Scaffold-Based Technique segment held the largest revenue share of 34.24% 2024, and expected to register a CAGR of 33.00% between 2025 to 2032 and the market is expected to reach USD 1,199.34 by 2032. This strong growth is attributed to the ability of scaffold-based techniques to mimic the natural structure and texture of conventional meat, enabling the production of more realistic meat cuts such as steaks, fillets, and whole-muscle products. Unlike simple cell aggregation, scaffolds provide a framework for cells to adhere, grow, and differentiate, which significantly improves the sensory attributes—taste, texture, and appearance—closely aligning with consumer expectations.

Additionally, this method supports better nutrient and oxygen diffusion, enhancing cell proliferation and scalability, which is critical for commercial production. Growing R&D investments in biomaterials and 3D bioprinting technologies are further advancing scaffold design, making them more cost-efficient and biocompatible. The rising demand for premium cultured meat products, particularly in high-value markets such as North America and Europe, combined with strong interest from food manufacturers to replicate traditional meat cuts, will continue to drive the dominance and rapid expansion of the scaffold-based technique segment.

Global Cultured Meat Market by Production Technique (USD Million)

Global Cultured Meat Maret by Application Insights:

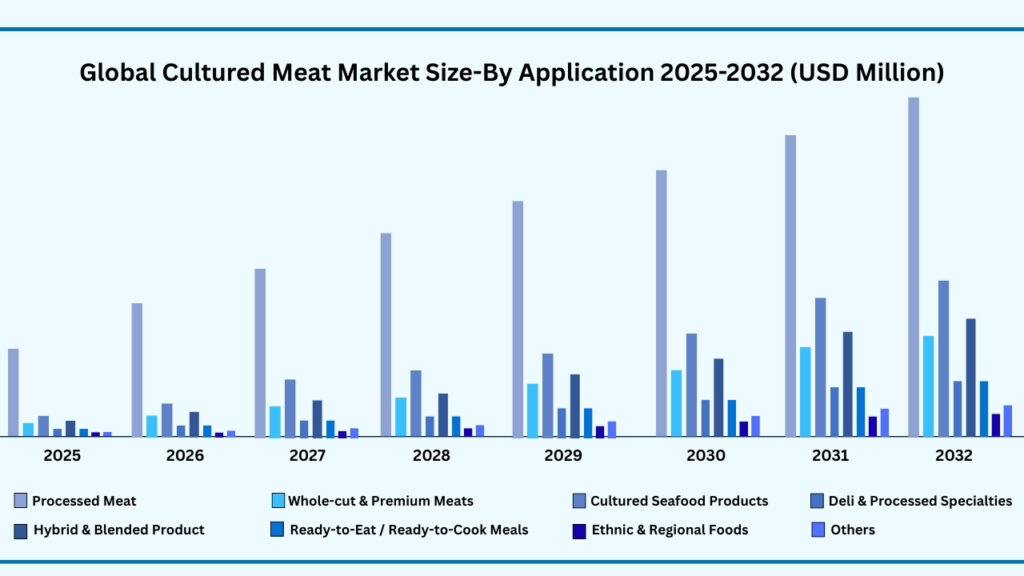

Processed Meat segment accounted for the largest market share of share 51.24% in 2024 in the global cultured meat market.

Based on application, processed meat segment held the largest revenue share of 51.24% in the global cultured meat market in 2024 and expected to register a CAGR of 33.23% from 2025 to 2032 and expected to reach USD 1,816.00 million. This strong growth is mainly driven by the widespread consumer acceptance and familiarity of processed meat products such as nuggets, patties, sausages, and deli slices, which makes them the most suitable entry point for cultured meat adoption. Since these products typically require smaller amounts of structured meat and can be blended with other ingredients, they are easier and more cost-effective to produce using current cultured meat technologies compared to whole cuts.

In addition, rising demand for convenient, ready-to-cook, and ready-to-eat food products, particularly among urban and younger consumers, is further fueling the segment’s growth. Processed cultured meat also offers opportunities for product innovation, allowing manufacturers to enhance flavor, nutrition, and functionality while maintaining affordability. Supportive regulatory approvals for cultured meat in processed formats, along with increasing partnerships between food tech startups and established processed food brands, are expected to accelerate commercialization and market penetration, reinforcing the segment’s leading position over the forecast period.

Global Cultured Meat Market by Application (USD Million)

Global Cultured Meat Food Market by Distribution Channel Insights:

Hypermarkets & Supermarkets segment accounted for the largest market share of share 37.45% in 2024 in the global cultured meat market.

Based on distribution channel, Hypermarkets & Supermarkets segment held the largest revenue share of 37.45% in the global cultured meat market in 2024 and expected to register a CAGR of 33.03% from 2025 to 2032 is expected to reach USD 1,324.82 million. This growth is supported by the fact that supermarkets and hypermarkets remain the most trusted and widely accessed retail channels for fresh and processed food purchases, providing consumers with greater convenience and variety under one roof. These outlets have strong infrastructure for cold storage and handling, which is essential for maintaining the quality and safety of cultured meat products.

Moreover, supermarkets serve as key platforms for product launches, sampling, and brand visibility, enabling cultured meat producers to build consumer awareness and trust in new products. Their ability to offer discounts, promotional campaigns, and bundled deals further encourages trial and adoption. The rising global penetration of organized retail chains, particularly in urban areas of Asia-Pacific, North America, and Europe, along with increasing collaborations between cultured meat startups and large retail groups, will continue to strengthen the dominance of hypermarkets and supermarkets as the leading distribution channel in the cultured meat market.

Global Cultured Meat Market by Distribution Channel (USD Million)

Global Cultured Meat Market by End Use Insights:

HoReCa segment accounted for the largest market share of share 49.33% in 2024 in the global cultured meat market.

Based on end use HoReCa segment held the largest revenue share of 49.33% in the global cultured meat market in 2024 and expected to register a CAGR of 33.18% from 2025 to 2032 and expected to reach USD 1,743.75 million in 2032. This dominance is driven by the fact that restaurants and foodservice outlets are often the first point of introduction for novel food products, as consumers are more open to trying innovative offerings in dining settings compared to purchasing them directly for home use. Chefs and premium restaurants play a vital role in shaping consumer perceptions by showcasing cultured meat in familiar and appealing dishes, which helps build trust and acceptance.

In addition, the HoReCa channel provides an ideal platform for cultured meat companies to position their products as premium, sustainable, and experiential foods before scaling into mass retail. Strategic collaborations between cultured meat producers and leading restaurant chains are also accelerating market entry and consumer reach. The growing trend of sustainable dining, particularly among younger and urban consumers, coupled with strong food innovation initiatives in regions like North America, Europe, and Asia-Pacific, further supports the segment’s rapid expansion. Over the forecast period, HoReCa will remain the primary gateway for cultured meat adoption and awareness, driving its continued leadership in the market.

Global Cultured Meat by End Use (USD Million)

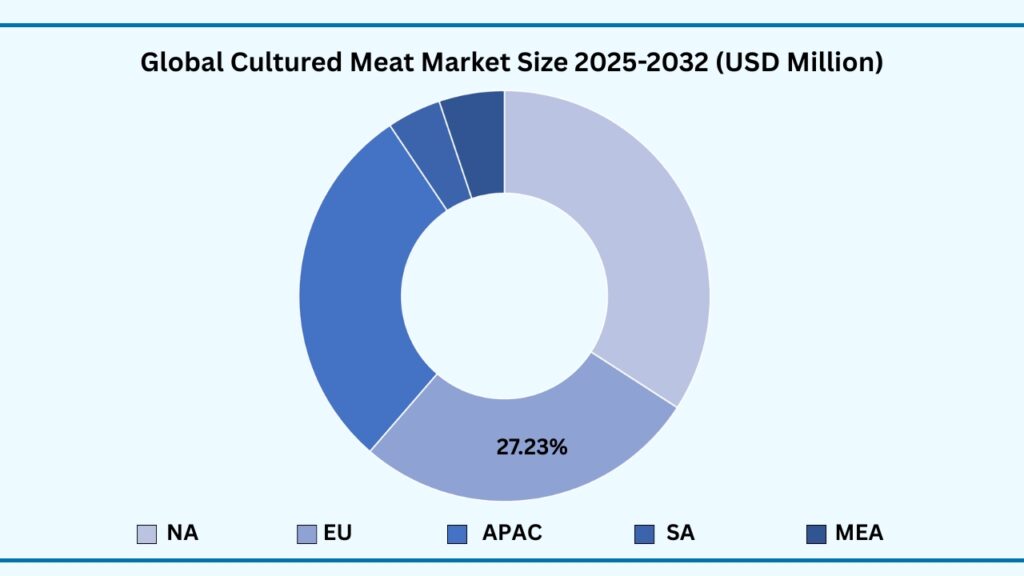

Global Cultured Meat Market by Region Insights:

North America segment accounted for the largest market share of share of 34.13% in 2024 in the global cultured meat market.

Based on region, the global cultured meat market is segmented into Europe, Asia-Pacific, North America, Latin America and Middle East & Africa. Among these, North America region held the largest revenue share of 34.13% in the global cultured meat market in 2024 and expected to register a CAGR of 27.46% from 2024 to 2032 and expected to reach USD 887.60 million in 2032. This growth is supported by the region’s strong ecosystem of food-tech startups, advanced R&D facilities, and high venture capital funding, which are accelerating innovation and commercialization of cultured meat. Favorable regulatory progress in the U.S., such as the FDA and USDA approvals for the sale of cultivated chicken, has further boosted consumer and industry confidence, making North America one of the first regions to see commercial launches.

Additionally, high consumer awareness around sustainability, animal welfare, and the health risks associated with conventional meat is driving adoption of alternative proteins in the region. Partnerships between cultured meat companies and established food manufacturers, along with the growing presence of pilot production facilities, are further strengthening supply chains and market readiness. The strong purchasing power of consumers, combined with their willingness to try innovative and premium food products, positions North America as a key growth driver for the cultured meat market over the forecast period.

Global Cultured Meat Market by Region (USD Million)

Major Companies and Competitive Landscape

The global cultured meat market is fragmented, with a mix of large multinational companies and emerging startups competing for market share. Major players are actively pursuing strategies such as mergers and acquisitions, collaborations with foodservice providers, and partnerships with retail and HoReCa channels to expand their presence. Many companies are also investing heavily in product innovation — developing cultured poultry, beef, seafood, and processed meat products — to cater to diverse consumer preferences. These efforts aim to enhance taste, texture, and quality, while ensuring scalability and consistent production standards across both online and offline channels.

In addition, leading players are increasingly focusing on sustainable production methods, reducing environmental impact, and transparent labeling to strengthen consumer trust and brand loyalty. The rise of health-conscious and environmentally aware consumers is pushing companies to refine their cultured meat offerings, emphasizing antibiotic-free, hormone-free, and nutrient-rich products. This innovation pipeline, combined with premiumization strategies, regulatory approvals, and expansion of distribution networks, is driving growth and increasing accessibility of cultured meat across global markets.

Some of the leading companies profiled in the global cultured meat market report include:

- Aleph Farms

- Mosa Meat

- Eat Just (Good Meat)

- Future Meat Technologies

- Shiok Meats

- Vow Foods

- Meatable

- BlueNalu

- Biftek Inc.

- Avant Meats

- Finless Foods

- ClearMeat

- Clever Carnivore

- Sticta Biologicals

- Sallea

Strategic Development

- Aleph Farms (Israel)- In 2024, Aleph Farms raised USD 29 million to enhance its core technology, aiming to produce whole cuts of meat more cost-effectively. Additionally, the company secured regulatory approval in Israel to market its thin-cut beef steaks, marking a significant milestone in commercialization.

- Mosa Meat (Netherlands)-Mosa Meat raised USD 42 million in 2024 to scale up production processes and prepare for market entry. The company is also focusing on reducing production costs to make cultured beef more accessible to consumers.

- Eat Just (Good Meat) (USA)-As of 2024, Eat Just has raised over $460 million in total funding. The company continues to expand its cultivated meat offerings, including its Good Meat brand, and has secured regulatory approvals in various markets.

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 127.76 Billion |

| CAGR (2024–2032) | 34.18% |

| Revenue forecast to 2033 | USD 3,534.86 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million, and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | “By Source Type, By Production Technique, By Application, By Distribution Channel By End Use (Region Forecast to 2032” |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, UAE, South Africa, Turkey, Rest of MEA |

| Key companies profiled | “Mosa Meat, Meatable, Ivy Farm Technologies, Uncommon (Higher Steaks), BioTech Foods, Cubiq Foods, Peace of Meat, Aleph Farms SuperMeat, Believer Meats, Shiok Meats, Ants Innovate, Avant Meats, CellX, Joes Future Food, IntegriCulture, DaNAgreen, SeaWith, EatKube, Upside Foods, GOOD Meat BlueNalu, Finless Foods, Mission Barns, New Age Eats” |

| Customization scope | 10 hours of free customization and expert consultation |

Some Key Questions the Report Will Answer

- What is the expected revenue Compound Annual Growth Rate (CAGR) of the global cultured meat market over the forecast period (2025–2032)?

- The global cultured meat market revenue is expected to register a Compound Annual Growth Rate (CAGR) of 33.18% during the forecast period.

- What was the size of the global cultured meat in 2024?

- The global alkyl amines market size was USD 360.75 Million in 2024.

- Which factors are expected to drive the global cultured meat market growth?

- Key factors driving the global cultured meat market growth include rising demand for sustainable and cruelty-free protein, increasing health and safety awareness, technological advancements in cell cultivation, supportive government regulations, and growing consumer acceptance of alternative proteins.

- Which was the leading segment in the global cultured meat market in terms of source type in 2024?

- Poultry segment was leading in the cultured meat market on the basis of product type in 2024.

- What are some restraints for revenue growth of the global cultured meat market?

- The global cultured meat market faces restraints such as high production costs, limited large-scale manufacturing infrastructure, and regulatory challenges in several regions. Additionally, consumer skepticism regarding taste, safety, and acceptance of lab-grown meat may slow adoption and affect revenue growth.

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of Cultured Meat market

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1.Primary

2.1.2.Secondary

2.1.3.Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1.Market value

2.3.2.Market volume

2.3.3.Exchange rate

2.3.4.Price

2.3.5.Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2025–2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10.Formulation & manufacturing

4.11.Distribution & retail

4.12.Import-export analysis

4.13.Brand comparative analysis

4.14.Technological advancements

4.15.Porter’s five force

4.15.1.Threat of new entrants

4.15.1.1.Capital requirment

4.15.1.2.Product knowledge

4.15.1.3.Technical knowledge

4.15.1.4.Customer relation

4.15.1.5.Access to appliation and technology

4.15.2.Threat of substitutes

4.15.2.1.Cost

4.15.2.2.Performance

4.15.2.3.Availability

4.15.2.4.Technical knowledge

4.15.2.5.Durability

4.15.3.Bargainning power of buyers

4.15.3.1.Numbers of buyers relative to suppliers

4.15.3.2.Product differentiation

4.15.3.3.Threat of forward integration

4.15.3.4.Buyers volume

4.15.4.Bargainning power of suppliers

4.15.4.1.Suppliers concentration

4.15.4.2.Buyers switching cost to other suppliers

4.15.4.3.Threat of backward integration

4.15.5.Bargainning power of suppliers

4.15.5.1.Industry concentration

4.15.5.2.Industry growth rate

4.15.5.3.Product differentiation

4.16.Patent analysis

4.17.Regulation coverage

4.18.Pricing analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1.Rising Demand for Sustainable Protein

5.1.2.Ethical & Animal Welfare Concerns

5.1.3.Technological Advancements & Regulatory Approvals

5.2. Restraints

5.2.1.High Production Costs & Scalability Issues

5.2.2.Consumer Acceptance & Perception

5.3. Opportunities

5.3.1.Expansion into Diverse Protein Sources

5.3.2.Strategic Collaborations & Investments

5.3.3.Emerg Market Adoption

5.4. Threat

5.4.1.Competition from Alternative Proteins

5.4.2.Regulatory & Policy Uncertainty

Chapter 6. Cultured Meat Market By Source Type Insights & Trends, Revenue (USD Million),

6.1. Source Dynamics & Market Share, 2025–2032

6.1.1.1.Poultry

6.1.1.2.Beef

6.1.1.3.Pork

6.1.1.4.Seafood

6.1.1.5.Duck

6.1.1.6.Lamb / Mutton

6.1.1.7.Goat

6.1.1.8.Rabbit

6.1.1.9.Kangaroo

6.1.1.10.Horse Meat

6.1.1.11.Bison / Buffalo

6.1.1.12.Camel Meat

6.1.1.13.Reptile Meat

6.1.1.14.Others

Chapter 7. Cultured Meat Market By Production Technique Insights & Trends, Revenue (USD

Million),

7.1. Production Technique Dynamics & Market Share, 2025–2032

7.1.1.Scaffold-Based Technique

7.1.2.Suspension (Scaffold-Free / Pellet-Based) Cultivation

7.1.3.3D Bioprinting

7.1.4.Self-Organizing Cell Cultures

7.1.5.Hybrid Plant-Cell Technology

7.1.6.Microcarrier-Based Bioreactor Systems

7.1.7.Organoid Intelligence & Stem Cell-Derived Techniques

7.1.8.Other

Chapter 8. Cultured Meat Market By Application Insights & Trends, Revenue (USD Million),

8.1. Application Dynamics & Market Share, 2025–2032

8.1.1.Processed Meat

8.1.1.1.Bars

8.1.1.2.Nuggets

8.1.1.3.Burgers & Burger Patties

8.1.1.4.Meatballs

8.1.1.5.Sausages

8.1.1.6.Hot Dogs

8.1.1.7.Minced Meat / Strips

8.1.2.Whole-Cut & Premium Meats

8.1.2.1.Cultured Steak

8.1.2.2.Cultured Chicken Breast

8.1.2.3.Cultured Pork Chops

8.1.2.4.Cultured Lamb

8.1.2.5.Duck Breast & Exotic Cuts

8.1.3.Cultured Seafood Products

8.1.3.1.Cultured Salmon

8.1.3.2.Cultured Tuna

8.1.3.3.Cultured Shrimp

8.1.3.4.Cultured Crab / Lobster

8.1.3.5.Cultured Whitefish

8.1.3.6.Other

8.1.4.Deli & Processed Specialties

8.1.4.1.Cultured Cold Cuts

8.1.4.2.Cultured Salami

8.1.4.3.Cultured Pepperoni

8.1.4.4.Cultured Pastrami

8.1.4.5.Cultured Sandwich Fillings

8.1.5.Hybrid & Blended Products

8.1.5.1.Meat and Plant Blends

8.1.5.2.Conventional Meat Blends

8.1.5.3.Cultured Protein–Infused Snacks

8.1.5.4.Bakery Fillings

8.1.6.Ready-to-Eat / Ready-to-Cook Meals

8.1.6.1.Frozen Meals

8.1.6.2.Pre-Cooked Meals

8.1.6.3.Cultured Meat Meal

8.1.6.4.Soups & Stews with Cultured Meat

8.1.7.Ethnic & Regional Foods

8.1.8.Other

Chapter 9. Cultured Meat Market By Distribution Channel Insights & Trends, Revenue (USD

Million),

9.1. Distribution Channel & Market Share, 2025–2032

9.1.1.Offline

9.1.1.1.Hypermarkets & Supermarkets

9.1.1.2.Convenience Stores

9.1.1.3.Food & Drink Specialty Stores

9.1.2.Online

9.1.2.1.E-commerce Platforms

9.1.2.2.Direct-to-Consumer (D2C) Websites

Chapter 10. Cultured Meat Market By End Use Insights & Trends, Revenue (USD Million),

10.1. End Use Dynamics & Market Share, 2025–2032

10.1.1.HoReCa

10.1.2.Household / Retail

10.1.3.Processed Food Industry

10.1.4.Others

Chapter 11. Cultured Meat Market Regional Outlook

11.1.Cultured Meat Share By Region, 2025–2032

11.2.North America

11.2.1.Market By Source Type, Market Estimates and Forecast, USD Million,2025-2032

11.2.1.1.Poultry

11.2.1.2.Beef

11.2.1.3.Pork

11.2.1.4.Seafood

11.2.1.5.Duck

11.2.1.6.Lamb / Mutton

11.2.1.7.Goat

11.2.1.8.Rabbit

11.2.1.9.Kangaroo

11.2.1.10.Horse Meat

11.2.1.11.Bison / Buffalo

11.2.1.12.Camel Meat

11.2.1.13.Reptile Meat

11.2.1.14.Others

11.3.Market By Production Technique Estimates and Forecast, USD Million, 2025-2032

11.3.1.Scaffold-Based Technique

11.3.2.Suspension (Scaffold-Free / Pellet-Based) Cultivation

11.3.3.3D Bioprinting

11.3.4.Self-Organizing Cell Cultures

11.3.5.Extrusion + Hybrid Plant-Cell Technology

11.3.6.Microcarrier-Based Bioreactor Systems

11.3.7.Organoid Intelligence & Stem Cell-Derived Techniques

11.3.8.Others

11.4.Market By Application, Market Estimates and Forecast, USD Million, 2025-2032

11.4.1.Processed Meat

11.4.1.1.Bars

11.4.1.2.Nuggets

11.4.1.3.Burgers & Burger Patties

11.4.1.4.Meatballs

11.4.1.5.Sausages

11.4.1.6.Hot Dogs

11.4.1.7.Minced Meat / Strips

11.4.2.Whole-Cut & Premium Meats

11.4.2.1.Cultured Steak

11.4.2.2.Cultured Chicken Breast

11.4.2.3.Cultured Pork Chops

11.4.2.4.Cultured Lamb

11.4.2.5.Duck Breast & Exotic Cuts

11.4.3.Cultured Seafood Products

11.4.3.1.Cultured Salmon

11.4.3.2.Cultured Tuna

11.4.3.3.Cultured Shrimp

11.4.3.4.Cultured Crab / Lobster

11.4.3.5.Cultured Whitefish

11.4.3.6.Other

11.4.4.Deli & Processed Specialties

11.4.4.1.Cultured Cold Cuts

11.4.4.2.Cultured Salami

11.4.4.3.Cultured Pepperoni

11.4.4.4.Cultured Pastrami

11.4.4.5.Cultured Sandwich Fillings

11.4.5.Hybrid & Blended Products

11.4.5.1.Meat and Plant Blends

11.4.5.2.Conventional Meat Blends

11.4.5.3.Cultured Protein–Infused Snacks

11.4.5.4.Bakery Fillings

11.4.6.Ready-to-Eat / Ready-to-Cook Meals

11.4.6.1.Frozen Meals

11.4.6.2.Pre-Cooked Meals

11.4.6.3.Cultured Meat Meal

11.4.6.4.Soups & Stews with Cultured Meat

11.4.7.Ethnic & Regional Foods

11.4.8.Other

11.5.Market By Distribution Channel, Market Estimates and Forecast, USD Million, 2025-2032

11.6.Distribution Channel & Market Share, 2025–2032

11.6.1.Offline

11.6.1.1.Hypermarkets & Supermarkets

11.6.1.2.Convenience Stores

11.6.1.3.Food & Drink Specialty Stores

11.6.2.Online

11.6.2.1.E-commerce Platforms

11.6.2.2.Direct-to-Consumer (D2C) Websites

11.7.Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

11.7.1.HoReCa

11.7.2.Household / Retail

11.7.3.Processed Food Industry

11.7.4.Others

11.8.Market By Country, Market Estimates and Forecast, USD Million, 2025-2032

11.8.1.US

11.8.2.Canada

11.8.3.Mexico

11.9.Europe

11.9.1. Market By Source Type, Market Estimates and Forecast, USD Million,2025-2032

11.9.1.1.Poultry

11.9.1.2.Beef

11.9.1.3.Pork

11.9.1.4.Seafood

11.9.1.5.Duck

11.9.1.6.Lamb / Mutton

11.9.1.7.Goat

11.9.1.8.Rabbit

11.9.1.9.Kangaroo

11.9.1.10.Horse Meat

11.9.1.11.Bison / Buffalo

11.9.1.12.Camel Meat

11.9.1.13.Reptile Meat

11.9.1.14.Others

11.10.Market By Production Technique Estimates and Forecast, USD Million, 2025-2032

11.10.1.Scaffold-Based Technique

11.10.2.Suspension (Scaffold-Free / Pellet-Based) Cultivation

11.10.3.3D Bioprinting

11.10.4.Self-Organizing Cell Cultures

11.10.5.Extrusion + Hybrid Plant-Cell Technology

11.10.6.Microcarrier-Based Bioreactor Systems

11.10.7.Organoid Intelligence & Stem Cell-Derived Techniques

11.10.8.Others

11.11.Market By Application, Market Estimates and Forecast, USD Million, 2025-2032

11.11.1.Processed Meat

11.11.1.1.Bars

11.11.1.2.Nuggets

11.11.1.3.Burgers & Burger Patties

11.11.1.4.Meatballs

11.11.1.5.Sausages

11.11.1.6.Hot Dogs

11.11.1.7.Minced Meat / Strips

11.11.2.Whole-Cut & Premium Meats

11.11.2.1.Cultured Steak

11.11.2.2.Cultured Chicken Breast

11.11.2.3.Cultured Pork Chops

11.11.2.4.Cultured Lamb

11.11.2.5.Duck Breast & Exotic Cuts

11.11.3.Cultured Seafood Products

11.11.3.1.Cultured Salmon

11.11.3.2.Cultured Tuna

11.11.3.3.Cultured Shrimp

11.11.3.4.Cultured Crab / Lobster

11.11.3.5.Cultured Whitefish

11.11.3.6.Other

11.11.4.Deli & Processed Specialties

11.11.4.1.Cultured Cold Cuts

11.11.4.2.Cultured Salami

11.11.4.3.Cultured Pepperoni

11.11.4.4.Cultured Pastrami

11.11.4.5.Cultured Sandwich Fillings

11.11.5.Hybrid & Blended Products

11.11.5.1.Meat and Plant Blends

11.11.5.2.Conventional Meat Blends

11.11.5.3.Cultured Protein–Infused Snacks

11.11.5.4.Bakery Fillings

11.11.6.Ready-to-Eat / Ready-to-Cook Meals

11.11.6.1.Frozen Meals

11.11.6.2.Pre-Cooked Meals

11.11.6.3.Cultured Meat Meal

11.11.6.4.Soups & Stews with Cultured Meat

11.11.7.Ethnic & Regional Foods

11.11.8.Other

11.12.Market By Distribution Channel, Market Estimates and Forecast, USD Million, 2025-2032

11.13.Distribution Channel & Market Share, 2025–2032

11.13.1.Offline

11.13.1.1.Hypermarkets & Supermarkets

11.13.1.2.Convenience Stores

11.13.1.3.Food & Drink Specialty Stores

11.13.2.Online

11.13.2.1.E-commerce Platforms

11.13.2.2.Direct-to-Consumer (D2C) Websites

11.14.Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

11.14.1.HoReCa

11.14.2.Household / Retail

11.14.3.Processed Food Industry

11.14.4.Others

11.15.Market By Country, Market Estimates and Forecast, USD Million,

11.15.1.Germany

11.15.2.France

11.15.3.U.K

11.15.4.Italy

11.15.5.Spain

11.15.6.Benelux

11.15.7.Russia

11.15.8.Finland

11.15.9.Sweden

11.15.10.Rest Of Europe

11.16.Asia-Pacific

11.16.1.Market By Source Type, Market Estimates and Forecast, USD Million,2025-2032

11.16.1.1.Poultry

11.16.1.2.Beef

11.16.1.3.Pork

11.16.1.4.Seafood

11.16.1.5.Duck

11.16.1.6.Lamb / Mutton

11.16.1.7.Goat

11.16.1.8.Rabbit

11.16.1.9.Kangaroo

11.16.1.10.Horse Meat

11.16.1.11.Bison / Buffalo

11.16.1.12.Camel Meat

11.16.1.13.Reptile Meat

11.16.1.14.Others

11.17.Market By Production Technique Estimates and Forecast, USD Million, 2025-2032

11.17.1.Scaffold-Based Technique

11.17.2.Suspension (Scaffold-Free / Pellet-Based) Cultivation

11.17.3.3D Bioprinting

11.17.4.Self-Organizing Cell Cultures

11.17.5.Extrusion + Hybrid Plant-Cell Technology

11.17.6.Microcarrier-Based Bioreactor Systems

11.17.7.Organoid Intelligence & Stem Cell-Derived Techniques

11.17.8.Others

11.18.Market By Application, Market Estimates and Forecast, USD Million, 2025-2032

11.18.1.Processed Meat

11.18.1.1.Bars

11.18.1.2.Nuggets

11.18.1.3.Burgers & Burger Patties

11.18.1.4.Meatballs

11.18.1.5.Sausages

11.18.1.6.Hot Dogs

11.18.1.7.Minced Meat / Strips

11.18.2.Whole-Cut & Premium Meats

11.18.2.1.Cultured Steak

11.18.2.2.Cultured Chicken Breast

11.18.2.3.Cultured Pork Chops

11.18.2.4.Cultured Lamb

11.18.2.5.Duck Breast & Exotic Cuts

11.18.3.Cultured Seafood Products

11.18.3.1.Cultured Salmon

11.18.3.2.Cultured Tuna

11.18.3.3.Cultured Shrimp

11.18.3.4.Cultured Crab / Lobster

11.18.3.5.Cultured Whitefish

11.18.3.6.Other

11.18.4.Deli & Processed Specialties

11.18.4.1.Cultured Cold Cuts

11.18.4.2.Cultured Salami

11.18.4.3.Cultured Pepperoni

11.18.4.4.Cultured Pastrami

11.18.4.5.Cultured Sandwich Fillings

11.18.5.Hybrid & Blended Products

11.18.5.1.Meat and Plant Blends

11.18.5.2.Conventional Meat Blends

11.18.5.3.Cultured Protein–Infused Snacks

11.18.5.4.Bakery Fillings

11.18.6.Ready-to-Eat / Ready-to-Cook Meals

11.18.6.1.Frozen Meals

11.18.6.2.Pre-Cooked Meals

11.18.6.3.Cultured Meat Meal

11.18.6.4.Soups & Stews with Cultured Meat

11.18.7.Ethnic & Regional Foods

11.18.8.Other

11.19.Market By Distribution Channel, Market Estimates and Forecast, USD Million, 2025-2032

11.20.Distribution Channel & Market Share, 2025–2032

11.20.1.Offline

11.20.1.1.Hypermarkets & Supermarkets

11.20.1.2.Convenience Stores

11.20.1.3.Food & Drink Specialty Stores

11.20.2.Online

11.20.2.1.E-commerce Platforms

11.20.2.2.Direct-to-Consumer (D2C) Websites

11.21.Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

11.21.1.HoReCa

11.21.2.Household / Retail

11.21.3.Processed Food Industry

11.21.4.Others

11.22.Market By Country, Market Estimates and Forecast, USD Million,

11.22.1.1.China

11.22.1.2.India

11.22.1.3.Japan

11.22.1.4.South Korea

11.22.1.5.Indonesia

11.22.1.6.Thailand

11.22.1.7.Vietnam

11.22.1.8.Australia

11.22.1.9.New Zeland

11.22.1.10.Rest of APAC

11.23.Latin America

11.23.1.Market By Source Type, Market Estimates and Forecast, USD Million,2025-2032

11.23.1.1.Poultry

11.23.1.2.Beef

11.23.1.3.Pork

11.23.1.4.Seafood

11.23.1.5.Duck

11.23.1.6.Lamb / Mutton

11.23.1.7.Goat

11.23.1.8.Rabbit

11.23.1.9.Kangaroo

11.23.1.10.Horse Meat

11.23.1.11.Bison / Buffalo

11.23.1.12.Camel Meat

11.23.1.13.Reptile Meat

11.23.1.14.Others

11.24.Market By Production Technique Estimates and Forecast, USD Million, 2025-2032

11.24.1.Scaffold-Based Technique

11.24.2.Suspension (Scaffold-Free / Pellet-Based) Cultivation

11.24.3.3D Bioprinting

11.24.4.Self-Organizing Cell Cultures

11.24.5.Extrusion + Hybrid Plant-Cell Technology

11.24.6.Microcarrier-Based Bioreactor Systems

11.24.7.Organoid Intelligence & Stem Cell-Derived Techniques

11.24.8.Others

11.25.Market By Application, Market Estimates and Forecast, USD Million, 2025-2032

11.25.1.Processed Meat

11.25.1.1.Bars

11.25.1.2.Nuggets

11.25.1.3.Burgers & Burger Patties

11.25.1.4.Meatballs

11.25.1.5.Sausages

11.25.1.6.Hot Dogs

11.25.1.7.Minced Meat / Strips

11.25.2.Whole-Cut & Premium Meats

11.25.2.1.Cultured Steak

11.25.2.2.Cultured Chicken Breast

11.25.2.3.Cultured Pork Chops

11.25.2.4.Cultured Lamb

11.25.2.5.Duck Breast & Exotic Cuts

11.25.3.Cultured Seafood Products

11.25.3.1.Cultured Salmon

11.25.3.2.Cultured Tuna

11.25.3.3.Cultured Shrimp

11.25.3.4.Cultured Crab / Lobster

11.25.3.5.Cultured Whitefish

11.25.3.6.Other

11.25.4.Deli & Processed Specialties

11.25.4.1.Cultured Cold Cuts

11.25.4.2.Cultured Salami

11.25.4.3.Cultured Pepperoni

11.25.4.4.Cultured Pastrami

11.25.4.5.Cultured Sandwich Fillings

11.25.5.Hybrid & Blended Products

11.25.5.1.Meat and Plant Blends

11.25.5.2.Conventional Meat Blends

11.25.5.3.Cultured Protein–Infused Snacks

11.25.5.4.Bakery Fillings

11.25.6.Ready-to-Eat / Ready-to-Cook Meals

11.25.6.1.Frozen Meals

11.25.6.2.Pre-Cooked Meals

11.25.6.3.Cultured Meat Meal

11.25.6.4.Soups & Stews with Cultured Meat

11.25.7.Ethnic & Regional Foods

11.25.8.Other

11.26.Market By Distribution Channel, Market Estimates and Forecast, USD Million,2025-2032

11.27.Distribution Channel & Market Share, 2025–2032

11.27.1.Offline

11.27.1.1.Hypermarkets & Supermarkets

11.27.1.2.Convenience Stores

11.27.1.3.Food & Drink Specialty Stores

11.27.2.Online

11.27.2.1.E-commerce Platforms

11.27.2.2.Direct-to-Consumer (D2C) Websites

11.28.Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

11.28.1.HoReCa

11.28.2.Household / Retail

11.28.3.Processed Food Industry

11.28.4.Others

11.28.5.Market By Country, Market Estimates and Forecast, USD Million,

11.28.5.1.Brazil

11.28.5.2.Rest of LATAM

11.29.Middle East & Africa

11.29.1.Market By Source Type, Market Estimates and Forecast, USD Million,2025-2032

11.29.1.1.Poultry

11.29.1.2.Beef

11.29.1.3.Pork

11.29.1.4.Seafood

11.29.1.5.Duck

11.29.1.6.Lamb / Mutton

11.29.1.7.Goat

11.29.1.8.Rabbit

11.29.1.9.Kangaroo

11.29.1.10.Horse Meat

11.29.1.11.Bison / Buffalo

11.29.1.12.Camel Meat

11.29.1.13.Reptile Meat

11.29.1.14.Others

11.30.Market By Production Technique Estimates and Forecast, USD Million, 2025-2032

11.30.1.Scaffold-Based Technique

11.30.2.Suspension (Scaffold-Free / Pellet-Based) Cultivation

11.30.3.3D Bioprinting

11.30.4.Self-Organizing Cell Cultures

11.30.5.Extrusion + Hybrid Plant-Cell Technology

11.30.6.Microcarrier-Based Bioreactor Systems

11.30.7.Organoid Intelligence & Stem Cell-Derived Techniques

11.30.8.Others

11.31.Market By Application, Market Estimates and Forecast, USD Million, 2025-2032

11.31.1.Processed Meat

11.31.1.1.Bars

11.31.1.2.Nuggets

11.31.1.3.Burgers & Burger Patties

11.31.1.4.Meatballs

11.31.1.5.Sausages

11.31.1.6.Hot Dogs

11.31.1.7.Minced Meat / Strips

11.31.2.Whole-Cut & Premium Meats

11.31.2.1.Cultured Steak

11.31.2.2.Cultured Chicken Breast

11.31.2.3.Cultured Pork Chops

11.31.2.4.Cultured Lamb

11.31.2.5.Duck Breast & Exotic Cuts

11.31.3.Cultured Seafood Products

11.31.3.1.Cultured Salmon

11.31.3.2.Cultured Tuna

11.31.3.3.Cultured Shrimp

11.31.3.4.Cultured Crab / Lobster

11.31.3.5.Cultured Whitefish

11.31.3.6.Other

11.31.4.Deli & Processed Specialties

11.31.4.1.Cultured Cold Cuts

11.31.4.2.Cultured Salami

11.31.4.3.Cultured Pepperoni

11.31.4.4.Cultured Pastrami

11.31.4.5.Cultured Sandwich Fillings

11.31.5.Hybrid & Blended Products

11.31.5.1.Meat and Plant Blends

11.31.5.2.Conventional Meat Blends

11.31.5.3.Cultured Protein–Infused Snacks

11.31.5.4.Bakery Fillings

11.31.6.Ready-to-Eat / Ready-to-Cook Meals

11.31.6.1.Frozen Meals

11.31.6.2.Pre-Cooked Meals

11.31.6.3.Cultured Meat Meal

11.31.6.4.Soups & Stews with Cultured Meat

11.31.7.Ethnic & Regional Foods

11.31.8.Other

11.32.Market By Distribution Channel, Market Estimates and Forecast, USD Million, 2025-2032

11.33.Distribution Channel & Market Share, 2025–2032

11.33.1.Offline

11.33.1.1.Hypermarkets & Supermarkets

11.33.1.2.Convenience Stores

11.33.1.3.Food & Drink Specialty Stores

11.33.2.Online

11.33.2.1.E-commerce Platforms

11.33.2.2.Direct-to-Consumer (D2C) Websites

11.34.Market By End Use, Market Estimates and Forecast, USD Million, 2025-2032

11.34.1.HoReCa

11.34.2.Household / Retail

11.34.3.Processed Food Industry

11.34.4.Others

11.34.5.Market By Country, Market Estimates and Forecast, USD Million,

11.34.5.1.Saudi Arabia

11.34.5.2.UAE

11.34.5.3.South Africa

11.34.5.4.Rest of MEA

Chapter 12. Competitive Landscape

12.1. Market Revenue Share By Manufacturers

12.2. Mergers & Acquisitions

12.3. Competitor’s Positioning

12.4. Strategy Benchmarking

12.5. Vendor Landscape

12.5.1.Distributors

12.5.1.1.North America

12.5.1.2.Europe

12.5.1.3.Asia Pacific

12.5.1.4.Middle East & Africa

12.5.1.5.Latin America

Chapter 13. Company Profiles

13.1. Mosa Meat

13.1.1.Company Overview

13.1.2.Product & Service Offerings

13.1.3.Strategic Initiatives

13.1.4.Financials

13.1.5.Research Insights

13.2.Meatable

13.2.1.Company Overview

13.2.2.Product & Service Offerings

13.2.3.Strategic Initiatives

13.2.4.Financials

13.2.5.Research Insights

13.3.Ivy Farm Technologies

13.3.1.Company Overview

13.3.2.Product & Service Offerings

13.3.3.Strategic Initiatives

13.3.4.Financials

13.3.5.Research Insights

13.4.Uncommon (Higher Steaks)

13.4.1.Company Overview

13.4.2.Product & Service Offerings

13.4.3.Strategic Initiatives

13.4.4.Financials

13.4.5.Research Insights

13.5.BioTech Foods

13.5.1.Company Overview

13.5.2.Product & Service Offerings

13.5.3.Strategic Initiatives

13.5.4.Financials

13.5.5.Research Insights

13.6.Cubiq Foods

13.6.1.Company Overview

13.6.2.Product & Service Offerings

13.6.3.Strategic Initiatives

13.6.4.Financials

13.6.5.Research Insights

13.7.Peace of Meat

13.7.1.Company Overview

13.7.2.Product & Service Offerings

13.7.3.Strategic Initiatives

13.7.4.Financials

13.7.5.Conclusion

13.8.Aleph Farms

13.8.1.Company Overview

13.8.2.Product & Service Offerings

13.8.3.Strategic Initiatives

13.8.4.Financials

13.8.5.Conclusion

13.9.SuperMeat

13.9.1.Company Overview

13.9.2.Product & Service Offerings

13.9.3.Strategic Initiatives

13.9.4.Financials

13.9.5.Conclusion

13.10.Believer Meats

13.10.1.Company Overview

13.10.2.Product & Service Offerings

13.10.3.Strategic Initiatives

13.10.4.Financials

13.10.5.Conclusion

13.11.Shiok Meats

13.11.1.Company Overview

13.11.2.Product & Service Offerings

13.11.3.Strategic Initiatives

13.11.4.Financials

13.11.5.Conclusion

13.12.Ants Innovate

13.12.1.Company Overview

13.12.2.Product & Service Offerings

13.12.3.Strategic Initiatives

13.12.4.Financials

13.12.5.Conclusion

13.13.Avant Meats

13.13.1.Company Overview

13.13.2.Product & Service Offerings

13.13.3.Strategic Initiatives

13.13.4.Financials

13.13.5.Conclusion

13.14.CellX

13.14.1.Company Overview

13.14.2.Product & Service Offerings

13.14.3.Strategic Initiatives

13.14.4.Financials

13.14.5.Conclusion

13.15.Joes Future Food

13.15.1.Company Overview

13.15.2.Product & Service Offerings

13.15.3.Strategic Initiatives

13.15.4.Financials

13.15.5.Conclusion

13.16.IntegriCulture

13.16.1.Company Overview

13.16.2.Product & Service Offerings

13.16.3.Strategic Initiatives

13.16.4.Financials

13.16.5.Conclusion

13.17.DaNAgreen

13.17.1.Company Overview

13.17.2.Product & Service Offerings

13.17.3.Strategic Initiatives

13.17.4.Financials

13.17.5.Conclusion

13.18.SeaWith

13.18.1.Company Overview

13.18.2.Product & Service Offerings

13.18.3.Strategic Initiatives

13.18.4.Financials

13.18.5.Conclusion

13.19.EatKube

13.19.1.Company Overview

13.19.2.Product & Service Offerings

13.19.3.Strategic Initiatives

13.19.4.Financials

13.19.5.Conclusion

13.20.Upside Foods

13.20.1.Company Overview

13.20.2.Product & Service Offerings

13.20.3.Strategic Initiatives

13.20.4.Financials

13.20.5.Conclusion

13.21.GOOD Meat

13.21.1.Company Overview

13.21.2.Product & Service Offerings

13.21.3.Strategic Initiatives

13.21.4.Financials

13.21.5.Conclusion

13.22.BlueNalu

13.22.1.Company Overview

13.22.2.Product & Service Offerings

13.22.3.Strategic Initiatives

13.22.4.Financials

13.22.5.Conclusion

13.23.Finless Foods

13.23.1.Company Overview

13.23.2.Product & Service Offerings

13.23.3.Strategic Initiatives

13.23.4.Financials

13.23.5.Conclusion

13.24.Mission Barns

13.24.1.Company Overview

13.24.2.Product & Service Offerings

13.24.3.Strategic Initiatives

13.24.4.Financials

13.24.5.Conclusion

13.25.New Age Eats

13.25.1.Company Overview

13.25.2.Product & Service Offerings

13.25.3.Strategic Initiatives

13.25.4.Financials

13.25.5.Conclusion

Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP. has segmented global cultured meat market on the basis of By Source Type, By Production Technique, By Application, By Distribution Channel, By End Use and By region for 2019 to 2032

Global Source Type Outlook (Revenue, USD Million 2019-2032)

-

- Poultry

-

- Beef

-

- Pork

-

- Seafood

-

- Duck

-

- Lamb / Mutton

-

- Goat

-

- Rabbit

-

- Kangaroo

-

- Horse Meat

-

- Bison / Buffalo

-

- Camel Meat

-

- Reptile Meat

-

- Others

Global Production Technique (Revenue, USD Million; 2019-2032)

-

- Scaffold-Based Technique

-

- Suspension (Scaffold-Free / Pellet-Based) Cultivation

-

- 3D Bioprinting

-

- Self-Organizing Cell Cultures

-

- Hybrid Plant-Cell Technology

-

- Microcarrier-Based Bioreactor Systems

-

- Organoid Intelligence & Stem Cell-Derived Techniques

-

- Other

Global Application Outlook (Revenue, USD Million; 2019-2032)

-

- Processed Meat

-

- Bars

-

- Nuggets

-

- Burgers & Burger Patties

-

- Meatballs

-

- Sausages

-

- Hot Dogs

-

- Minced Meat / Strips

- Whole-Cut & Premium Meats

-

- Cultured Steak

-

- Cultured Chicken Breast

-

- Cultured Pork Chops

-

- Cultured Lamb

-

- Duck Breast & Exotic Cuts

- Cultured Seafood Products

-

- Cultured Salmon

-

- Cultured Tuna

-

- Cultured Shrimp

-

- Cultured Crab / Lobster

-

- Cultured Whitefish

-

- Other

- Deli & Processed Specialties

-

- Cultured Cold Cuts

-

- Cultured Salami

-

- Cultured Pepperoni

-

- Cultured Pastrami

-

- Cultured Sandwich Fillings

- Hybrid & Blended Products

-

- Meat and Plant Blends

-

- Conventional Meat Blends

-

- Cultured Protein–Infused Snacks

-

- Bakery Fillings

- Ready-to-Eat / Ready-to-Cook Meals

-

- Frozen Meals

-

- Pre-Cooked Meals

-

- Cultured Meat Meal

-

- Soups & Stews with Cultured Meat

- Ethnic & Regional Foods

- Other

- Global Distribution Channel (Revenue, USD Million; 2019-2032)

-

- Hypermarkets & Supermarkets

-

- Convenience Stores

-

- Food & Drink Specialty Stores

-

- Online

- Global End Use (Revenue, USD Million; 2019-2032)

-

- HoReCa

-

- Household / Retail

-

- Processed Food Industry

-

- Pet Food Industry

-

- Others

- North America

- North America Source Type Outlook (Revenue, USD Million 2019-2032)

-

- Poultry

-

- Beef

-

- Pork

-

- Seafood

-

- Duck

-

- Lamb / Mutton

-

- Goat

-

- Rabbit

-

- Kangaroo

-

- Horse Meat

-

- Bison / Buffalo

-

- Camel Meat

-

- Reptile Meat

-

- Others

- North America Production Technique Outlook (Revenue, USD Million; 2019-2032)

-

- Scaffold-Based Technique

-

- Suspension (Scaffold-Free / Pellet-Based) Cultivation

-

- 3D Bioprinting

-

- Self-Organizing Cell Cultures

-

- Extrusion + Hybrid Plant-Cell Technology

-

- Microcarrier-Based Bioreactor Systems

-

- Organoid Intelligence & Stem Cell-Derived Techniques

-

- Other

- North America Application Outlook (Revenue, USD Million; 2019-2032)

-

- Processed Meat

-

- Bars

-

- Nuggets

-

- Burgers & Burger Patties

-

- Meatballs

-

- Sausages

-

- Hot Dogs

-

- Minced Meat / Strips

- Whole-Cut & Premium Meats

-

- Cultured Steak

-

- Cultured Chicken Breast

-

- Cultured Pork Chops

-

- Cultured Lamb

-

- Duck Breast & Exotic Cuts

- Cultured Seafood Products

-

- Cultured Salmon

-

- Cultured Tuna

-

- Cultured Shrimp

-

- Cultured Crab / Lobster

-

- Cultured Whitefish

-

- Other

- Deli & Processed Specialties

-

- Cultured Cold Cuts

-

- Cultured Salami

-

- Cultured Pepperoni

-

- Cultured Pastrami

-

- Cultured Sandwich Fillings

- Hybrid & Blended Products

-

- Meat and Plant Blends

-

- Conventional Meat Blends

-

- Cultured Protein–Infused Snacks

-

- Bakery Fillings

- Ready-to-Eat / Ready-to-Cook Meals

-

- Frozen Meals

-

- Pre-Cooked Meals

-

- Cultured Meat Meal

-

- Soups & Stews with Cultured Meat

- Ethnic & Regional Foods

- Others

- North America Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

-

- Hypermarkets & Supermarkets

-

- Convenience Stores

-

- Food & Drink Specialty Stores

-

- Online

- North America End Use Outlook (Revenue, USD Million; 2019-2032)

-

- HoReCa

-

- Household / Retail

-

- Processed Food Industry

-

- Pet Food Industry

-

- Others

- U.S

- North America Source Type Outlook (Revenue, USD Million 2019-2032)

-

- Poultry

-

- Beef

-

- Pork

-

- Seafood

-

- Duck

-

- Lamb / Mutton

-

- Goat

-

- Rabbit

-

- Kangaroo

-

- Horse Meat

-

- Bison / Buffalo

-

- Camel Meat

-

- Reptile Meat

-

- Others

- U.S Production Technique Outlook (Revenue, USD Million; 2019-2032)

-

- Scaffold-Based Technique

-

- Suspension (Scaffold-Free / Pellet-Based) Cultivation

-

- 3D Bioprinting

-

- Self-Organizing Cell Cultures

-

- Extrusion + Hybrid Plant-Cell Technology

-

- Microcarrier-Based Bioreactor Systems

-

- Organoid Intelligence & Stem Cell-Derived Techniques

-

- Other

- U.S Application Outlook (Revenue, USD Million; 2019-2032)

-

- Processed Meat

-

- Bars

-

- Nuggets

-

- Burgers & Burger Patties

-

- Meatballs

-

- Sausages

-

- Hot Dogs

-

- Minced Meat / Strips

- Whole-Cut & Premium Meats

-

- Cultured Steak

-

- Cultured Chicken Breast

-

- Cultured Pork Chops

-

- Cultured Lamb

-

- Duck Breast & Exotic Cuts

- Cultured Seafood Products

-

- Cultured Salmon

-

- Cultured Tuna

-

- Cultured Shrimp

-

- Cultured Crab / Lobster

-

- Cultured Whitefish

-

- Other

- Deli & Processed Specialties

-

- Cultured Cold Cuts

-

- Cultured Salami

-

- Cultured Pepperoni

-

- Cultured Pastrami

-

- Cultured Sandwich Fillings

- Hybrid & Blended Products

-

- Meat and Plant Blends

-

- Conventional Meat Blends

-

- Cultured Protein–Infused Snacks

-

- Bakery Fillings

- Ready-to-Eat / Ready-to-Cook Meals

-

- Frozen Meals

-

- Pre-Cooked Meals

-

- Cultured Meat Meal

-

- Soups & Stews with Cultured Meat

- Ethnic & Regional Foods

- Others

- U.S Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

-

- Hypermarkets & Supermarkets

-

- Convenience Stores

-

- Food & Drink Specialty Stores

-

- Online

- U.S End Use Outlook (Revenue, USD Million; 2019-2032)

-

- HoReCa

-

- Household / Retail

-

- Processed Food Industry

-

- Pet Food Industry

-

- Others

- Canada

|

- Mexico

- Mexico Source Type Outlook (Revenue, USD Million 2019-2032)

-

- Poultry

-

- Beef

-

- Pork

-

- Seafood

-

- Duck

-

- Lamb / Mutton

-

- Goat

-

- Rabbit

-

- Kangaroo

-

- Horse Meat

-

- Bison / Buffalo

-

- Camel Meat

-

- Reptile Meat

-

- Others

- Mexico Production Technique Outlook (Revenue, USD Million; 2019-2032)

-

- Scaffold-Based Technique

-

- Suspension (Scaffold-Free / Pellet-Based) Cultivation

-

- 3D Bioprinting

-

- Self-Organizing Cell Cultures

-

- Extrusion + Hybrid Plant-Cell Technology

-

- Microcarrier-Based Bioreactor Systems

-

- Organoid Intelligence & Stem Cell-Derived Techniques

-

- Other

- Mexico Application Outlook (Revenue, USD Million; 2019-2032)

-

- Processed Meat

-

- Bars

-

- Nuggets

-

- Burgers & Burger Patties

-

- Meatballs

-

- Sausages

-

- Hot Dogs

-

- Minced Meat / Strips

- Whole-Cut & Premium Meats

-

- Cultured Steak

-

- Cultured Chicken Breast

-

- Cultured Pork Chops

-

- Cultured Lamb

-

- Duck Breast & Exotic Cuts

- Cultured Seafood Products

-

- Cultured Salmon

-

- Cultured Tuna

-

- Cultured Shrimp

-

- Cultured Crab / Lobster

-

- Cultured Whitefish

-

- Other

- Deli & Processed Specialties

-

- Cultured Cold Cuts

-

- Cultured Salami

-

- Cultured Pepperoni

-

- Cultured Pastrami

-

- Cultured Sandwich Fillings

- Hybrid & Blended Products

-

- Meat and Plant Blends

-

- Conventional Meat Blends

-

- Cultured Protein–Infused Snacks

-

- Bakery Fillings

- Ready-to-Eat / Ready-to-Cook Meals

-

- Frozen Meals

-

- Pre-Cooked Meals

-

- Cultured Meat Meal

-

- Soups & Stews with Cultured Meat

- Ethnic & Regional Foods

- Others

- Mexico Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

-

- Hypermarkets & Supermarkets

-

- Convenience Stores

-

- Food & Drink Specialty Stores

-

- Online

- Mexico End Use Outlook (Revenue, USD Million; 2019-2032)

-

- HoReCa

-

- Household / Retail

-

- Processed Food Industry

-

- Pet Food Industry

-

- Others

- Europe

- Europe Source Type Outlook (Revenue, USD Million 2019-2032)

-

- Poultry

-

- Beef

-

- Pork

-

- Seafood

-

- Duck

-

- Lamb / Mutton

-

- Goat

-

- Rabbit

-

- Kangaroo

-

- Horse Meat

-

- Bison / Buffalo

-

- Camel Meat

-

- Reptile Meat

-

- Others

- Europe Production Technique Outlook (Revenue, USD Million; 2019-2032)

-

- Scaffold-Based Technique

-

- Suspension (Scaffold-Free / Pellet-Based) Cultivation

-

- 3D Bioprinting

-

- Self-Organizing Cell Cultures

-

- Extrusion + Hybrid Plant-Cell Technology

-

- Microcarrier-Based Bioreactor Systems

-

- Organoid Intelligence & Stem Cell-Derived Techniques

-

- Other

- Europe Application Outlook (Revenue, USD Million; 2019-2032)

- Processed Meat

-

- Bars

-

- Nuggets

-

- Burgers & Burger Patties

-

- Meatballs

-

- Sausages

-

- Hot Dogs

-

- Minced Meat / Strips

- Whole-Cut & Premium Meats

-

- Cultured Steak

-

- Cultured Chicken Breast

-

- Cultured Pork Chops

-

- Cultured Lamb

-

- Duck Breast & Exotic Cuts

- Cultured Seafood Products

-

- Cultured Salmon

-

- Cultured Tuna

-

- Cultured Shrimp

-

- Cultured Crab / Lobster

-

- Cultured Whitefish

-

- Other

- Deli & Processed Specialties

-

- Cultured Cold Cuts

-

- Cultured Salami

-

- Cultured Pepperoni

-

- Cultured Pastrami

-

- Cultured Sandwich Fillings

- Hybrid & Blended Products

-

- Meat and Plant Blends

-

- Conventional Meat Blends

-

- Cultured Protein–Infused Snacks

-

- Bakery Fillings

- Ready-to-Eat / Ready-to-Cook Meals

-

- Frozen Meals

-

- Pre-Cooked Meals

-

- Cultured Meat Meal

-

- Soups & Stews with Cultured Meat

- Ethnic & Regional Foods

- Others

- Europe Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

-

- Hypermarkets & Supermarkets

-

- Convenience Stores

-

- Food & Drink Specialty Stores

-

- Online

- Europe End Use Outlook (Revenue, USD Million; 2019-2032)

-

- HoReCa

-

- Household / Retail

-

- Processed Food Industry

-

- Pet Food Industry

-

- Others

- Germany

- Germany Source Type Outlook (Revenue, USD Million 2019-2032)

-

- Poultry

-

- Beef

-

- Pork

-

- Seafood

-

- Duck

-

- Lamb / Mutton

-

- Goat

-

- Rabbit

-

- Kangaroo

-

- Horse Meat

-

- Bison / Buffalo

-

- Camel Meat

-

- Reptile Meat

-

- Others

- Germany Production Technique Outlook (Revenue, USD Million; 2019-2032)

-

- Scaffold-Based Technique

-

- Suspension (Scaffold-Free / Pellet-Based) Cultivation

-

- 3D Bioprinting

-

- Self-Organizing Cell Cultures

-

- Extrusion + Hybrid Plant-Cell Technology

-

- Microcarrier-Based Bioreactor Systems

-

- Organoid Intelligence & Stem Cell-Derived Techniques

-

- Other

- Germany Application Outlook (Revenue, USD Million; 2019-2032)

-

- Processed Meat

-

- Bars

-

- Nuggets

-

- Burgers & Burger Patties

-

- Meatballs

-

- Sausages

-

- Hot Dogs

-

- Minced Meat / Strips

- Whole-Cut & Premium Meats

-

- Cultured Steak

-

- Cultured Chicken Breast

-

- Cultured Pork Chops

-

- Cultured Lamb

-

- Duck Breast & Exotic Cuts

- Cultured Seafood Products

-

- Cultured Salmon

-

- Cultured Tuna

-

- Cultured Shrimp

-

- Cultured Crab / Lobster

-

- Cultured Whitefish

-

- Other

- Deli & Processed Specialties

-

- Cultured Cold Cuts

-

- Cultured Salami

-

- Cultured Pepperoni

-

- Cultured Pastrami

-

- Cultured Sandwich Fillings

- Hybrid & Blended Products

-

- Meat and Plant Blends

-

- Conventional Meat Blends

-

- Cultured Protein–Infused Snacks

-

- Bakery Fillings

- Ready-to-Eat / Ready-to-Cook Meals

-

- Frozen Meals

-

- Pre-Cooked Meals

-

- Cultured Meat Meal

-

- Soups & Stews with Cultured Meat

- Ethnic & Regional Foods

- Others

- Germany Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

-

- Hypermarkets & Supermarkets

-

- Convenience Stores

-

- Food & Drink Specialty Stores

-

- Online

- Germany End Use Outlook (Revenue, USD Million; 2019-2032)

-

- HoReCa

-

- Household / Retail

-

- Processed Food Industry

-

- Pet Food Industry

-

- Others

- France

- France Source Type Outlook (Revenue, USD Million 2019-2032)

-

- Poultry

-

- Beef

-

- Pork

-

- Seafood

-

- Duck

-

- Lamb / Mutton

-

- Goat

-

- Rabbit

-

- Kangaroo

-

- Horse Meat

-

- Bison / Buffalo

-

- Camel Meat

-

- Reptile Meat

-

- Others

- France Production Technique Outlook (Revenue, USD Million; 2019-2032)

-

- Scaffold-Based Technique

-

- Suspension (Scaffold-Free / Pellet-Based) Cultivation

-

- 3D Bioprinting

-

- Self-Organizing Cell Cultures

-

- Extrusion + Hybrid Plant-Cell Technology

-

- Microcarrier-Based Bioreactor Systems

-

- Organoid Intelligence & Stem Cell-Derived Techniques

-

- Other

- France Application Outlook (Revenue, USD Million; 2019-2032)

-

- Processed Meat

-

- Bars

-

- Nuggets

-

- Burgers & Burger Patties

-

- Meatballs

-

- Sausages

-

- Hot Dogs

-

- Minced Meat / Strips

- Whole-Cut & Premium Meats

-

- Cultured Steak

-

- Cultured Chicken Breast

-

- Cultured Pork Chops

-

- Cultured Lamb

-

- Duck Breast & Exotic Cuts

- Cultured Seafood Products

-

- Cultured Salmon

-

- Cultured Tuna

-

- Cultured Shrimp

-

- Cultured Crab / Lobster

-

- Cultured Whitefish

-

- Other

- Deli & Processed Specialties

-

- Cultured Cold Cuts

-

- Cultured Salami

-

- Cultured Pepperoni

-

- Cultured Pastrami

-

- Cultured Sandwich Fillings

- Hybrid & Blended Products

-

- Meat and Plant Blends

-

- Conventional Meat Blends

-

- Cultured Protein–Infused Snacks

-

- Bakery Fillings

- Ready-to-Eat / Ready-to-Cook Meals

-

- Frozen Meals

-

- Pre-Cooked Meals

-

- Cultured Meat Meal

-

- Soups & Stews with Cultured Meat

- Ethnic & Regional Foods

- Others

- France Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

-

- Hypermarkets & Supermarkets

-

- Convenience Stores

-

- Food & Drink Specialty Stores

-

- Online

- France End Use Outlook (Revenue, USD Million; 2019-2032)

-

- HoReCa

-

- Household / Retail

-

- Processed Food Industry

-

- Pet Food Industry

-

- Others

- U.K

- U.K Source Type Outlook (Revenue, USD Million 2019-2032)

-

- Scaffold-Based Technique

-

- Suspension (Scaffold-Free / Pellet-Based) Cultivation

-

- 3D Bioprinting

- U.K Production Technique Outlook (Revenue, USD Million; 2019-2032)

-

- Scaffold-Based Technique

-

- Suspension (Scaffold-Free / Pellet-Based) Cultivation

-

- 3D Bioprinting

-

- Self-Organizing Cell Cultures

-

- Extrusion + Hybrid Plant-Cell Technology

-

- Microcarrier-Based Bioreactor Systems

-

- Organoid Intelligence & Stem Cell-Derived Techniques

-

- Other

- U.K Application Outlook (Revenue, USD Million; 2019-2032)

-

- Processed Meat

-

- Bars

-

- Nuggets

-

- Burgers & Burger Patties

-

- Meatballs

-

- Sausages

-

- Hot Dogs

-

- Minced Meat / Strips

- Whole-Cut & Premium Meats

-

- Cultured Steak

-

- Cultured Chicken Breast

-

- Cultured Pork Chops

-

- Cultured Lamb

-

- Duck Breast & Exotic Cuts

- Cultured Seafood Products

-

- Cultured Salmon

-

- Cultured Tuna

-

- Cultured Shrimp

-

- Cultured Crab / Lobster

-

- Cultured Whitefish

-

- Other

- Deli & Processed Specialties

-

- Cultured Cold Cuts

-

- Cultured Salami

-

- Cultured Pepperoni

-

- Cultured Pastrami

-

- Cultured Sandwich Fillings

- Hybrid & Blended Products

-

- Meat and Plant Blends

-

- Conventional Meat Blends

-

- Cultured Protein–Infused Snacks

-

- Bakery Fillings

- Ready-to-Eat / Ready-to-Cook Meals

-

- Frozen Meals

-

- Pre-Cooked Meals

-

- Cultured Meat Meal

-

- Soups & Stews with Cultured Meat

- Ethnic & Regional Foods

- Others

- U.K Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

-

- Hypermarkets & Supermarkets

-

- Convenience Stores

-

- Food & Drink Specialty Stores

-

- Online

- U.K End Use Outlook (Revenue, USD Million; 2019-2032)

-

- HoReCa

-

- Household / Retail

-

- Processed Food Industry

-

- Pet Food Industry

-

- Others

- U.K

- U.K Source Type Outlook (Revenue, USD Million 2019-2032)

-

- Poultry

-

- Beef

-

- Pork

-

- Seafood

-

- Duck

-

- Lamb / Mutton

-

- Goat

-

- Rabbit

-

- Kangaroo

-

- Horse Meat

-

- Bison / Buffalo

-

- Camel Meat

-

- Reptile Meat

-

- Others

- U.K Production Technique Outlook (Revenue, USD Million; 2019-2032)

-

- Scaffold-Based Technique

-

- Suspension (Scaffold-Free / Pellet-Based) Cultivation

-

- 3D Bioprinting

-

- Self-Organizing Cell Cultures

-

- Extrusion + Hybrid Plant-Cell Technology

-

- Microcarrier-Based Bioreactor Systems

-

- Organoid Intelligence & Stem Cell-Derived Techniques

-

- Other

- U.K Application Outlook (Revenue, USD Million; 2019-2032)

-

- Processed Meat

-

- Bars

-

- Nuggets

-

- Burgers & Burger Patties

-

- Meatballs

-

- Sausages

-

- Hot Dogs

-

- Minced Meat / Strips

- Whole-Cut & Premium Meats

-

- Cultured Steak

-

- Cultured Chicken Breast

-

- Cultured Pork Chops

-

- Cultured Lamb

-

- Duck Breast & Exotic Cuts

- Cultured Seafood Products

-

- Cultured Salmon

-

- Cultured Tuna

-

- Cultured Shrimp

-

- Cultured Crab / Lobster

-

- Cultured Whitefish

-

- Other

- Deli & Processed Specialties

-

- Cultured Cold Cuts

-

- Cultured Salami

-

- Cultured Pepperoni

-

- Cultured Pastrami

-

- Cultured Sandwich Fillings

- Hybrid & Blended Products

-

- Meat and Plant Blends

-

- Conventional Meat Blends

-

- Cultured Protein–Infused Snacks

-

- Bakery Fillings

- Ready-to-Eat / Ready-to-Cook Meals

-

- Frozen Meals

-

- Pre-Cooked Meals

-

- Cultured Meat Meal

-

- Soups & Stews with Cultured Meat

- Ethnic & Regional Foods

- Others

- U.K Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

-

- Hypermarkets & Supermarkets

-

- Convenience Stores

-

- Food & Drink Specialty Stores

-

- Online

- U.K End Use Outlook (Revenue, USD Million; 2019-2032)

-

- HoReCa

-

- Household / Retail

-

- Processed Food Industry

-

- Pet Food Industry

-

- Others

- Italy

- Italy Source Type Outlook (Revenue, USD Million 2019-2032)

-

- Poultry

-

- Beef

-

- Pork

-

- Seafood

-

- Duck

-

- Lamb / Mutton

-

- Goat

-

- Rabbit

-

- Kangaroo

-

- Horse Meat

-

- Bison / Buffalo

-

- Camel Meat

-

- Reptile Meat

-

- Others

- Italy Production Technique Outlook (Revenue, USD Million; 2019-2032)

-

- Scaffold-Based Technique

-

- Suspension (Scaffold-Free / Pellet-Based) Cultivation

-

- 3D Bioprinting

-

- Self-Organizing Cell Cultures

-

- Extrusion + Hybrid Plant-Cell Technology

-

- Microcarrier-Based Bioreactor Systems

-

- Organoid Intelligence & Stem Cell-Derived Techniques

-

- Other

- Italy Application Outlook (Revenue, USD Million; 2019-2032)

-

- Processed Meat

-

- Bars

-

- Nuggets

-

- Burgers & Burger Patties

-

- Meatballs

-

- Sausages

-

- Hot Dogs

-

- Minced Meat / Strips

- Whole-Cut & Premium Meats

-

- Cultured Steak

-

- Cultured Chicken Breast

-

- Cultured Pork Chops

-

- Cultured Lamb

-

- Duck Breast & Exotic Cuts

- Cultured Seafood Products

-

- Cultured Salmon

-

- Cultured Tuna

-

- Cultured Shrimp

-

- Cultured Crab / Lobster

-

- Cultured Whitefish

-

- Other

- Deli & Processed Specialties

-

- Cultured Cold Cuts

-

- Cultured Salami

-

- Cultured Pepperoni

-

- Cultured Pastrami

-

- Cultured Sandwich Fillings

- Hybrid & Blended Products

-

- Meat and Plant Blends

-

- Conventional Meat Blends

-

- Cultured Protein–Infused Snacks

-

- Bakery Fillings

- Ready-to-Eat / Ready-to-Cook Meals

-

- Frozen Meals

-

- Pre-Cooked Meals

-

- Cultured Meat Meal

-

- Soups & Stews with Cultured Meat

- Ethnic & Regional Foods

- Others

- Italy Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

-

- Hypermarkets & Supermarkets

-

- Convenience Stores

-

- Food & Drink Specialty Stores

-

- Online

- Italy End Use Outlook (Revenue, USD Million; 2019-2032)

-

- HoReCa

-

- Household / Retail

-

- Processed Food Industry

-

- Pet Food Industry

-

- Others

- Spain

- Spain Source Type Outlook (Revenue, USD Million 2019-2032)

-

- Poultry

-

- Beef

-

- Pork

-

- Seafood

-

- Duck

-

- Lamb / Mutton

-

- Goat

-

- Rabbit

-

- Kangaroo

-

- Horse Meat

-

- Bison / Buffalo

-

- Camel Meat

-

- Reptile Meat

-

- Others

- Spain Production Technique Outlook (Revenue, USD Million; 2019-2032)

-

- Scaffold-Based Technique

-

- Suspension (Scaffold-Free / Pellet-Based) Cultivation

-

- 3D Bioprinting

-

- Self-Organizing Cell Cultures

-

- Extrusion + Hybrid Plant-Cell Technology

-

- Microcarrier-Based Bioreactor Systems

-

- Organoid Intelligence & Stem Cell-Derived Techniques

-

- Other

- Spain Application Outlook (Revenue, USD Million; 2019-2032)

-

- Processed Meat

-

- Bars

-

- Nuggets

-

- Burgers & Burger Patties

-

- Meatballs

-

- Sausages

-

- Hot Dogs

-

- Minced Meat / Strips

- Whole-Cut & Premium Meats

-

- Cultured Steak

-

- Cultured Chicken Breast

-

- Cultured Pork Chops

-

- Cultured Lamb

-

- Duck Breast & Exotic Cuts

- Cultured Seafood Products

-

- Cultured Salmon

-

- Cultured Tuna

-

- Cultured Shrimp

-

- Cultured Crab / Lobster

-

- Cultured Whitefish

-

- Other

- Deli & Processed Specialties

-

- Cultured Cold Cuts

-

- Cultured Salami

-

- Cultured Pepperoni

-

- Cultured Pastrami

-

- Cultured Sandwich Fillings

- Hybrid & Blended Products

-

- Meat and Plant Blends

-

- Conventional Meat Blends

-

- Cultured Protein–Infused Snacks

-

- Bakery Fillings

- Ready-to-Eat / Ready-to-Cook Meals

-

- Frozen Meals

-

- Pre-Cooked Meals

-

- Cultured Meat Meal

-

- Soups & Stews with Cultured Meat

- Ethnic & Regional Foods

- Others

- Spain Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

-

- Hypermarkets & Supermarkets

-

- Convenience Stores

-

- Food & Drink Specialty Stores

-

- Online

- Spain End Use Outlook (Revenue, USD Million; 2019-2032)

-

- HoReCa

-

- Household / Retail

-

- Processed Food Industry

-

- Pet Food Industry

-

- Others

- Benelux

- Benelux Source Type Outlook (Revenue, USD Million 2019-2032)

-

- Poultry

-

- Beef

-

- Pork

-

- Seafood

-

- Duck

-

- Lamb / Mutton

-

- Goat

-

- Rabbit

-

- Kangaroo

-

- Horse Meat

-

- Bison / Buffalo

-

- Camel Meat

-

- Reptile Meat

-

- Others

- Benelux Production Technique Outlook (Revenue, USD Million; 2019-2032)

-

- Scaffold-Based Technique

-

- Suspension (Scaffold-Free / Pellet-Based) Cultivation

-

- 3D Bioprinting

-

- Self-Organizing Cell Cultures

-

- Extrusion + Hybrid Plant-Cell Technology

-

- Microcarrier-Based Bioreactor Systems

-

- Organoid Intelligence & Stem Cell-Derived Techniques

-

- Other

- Benelux Application Outlook (Revenue, USD Million; 2019-2032)

-

- Processed Meat

-

- Bars

-

- Nuggets

-

- Burgers & Burger Patties

-

- Meatballs

-

- Sausages

-

- Hot Dogs

-

- Minced Meat / Strips

- Whole-Cut & Premium Meats

-

- Cultured Steak

-

- Cultured Chicken Breast

-

- Cultured Pork Chops

-

- Cultured Lamb

-

- Duck Breast & Exotic Cuts

- Cultured Seafood Products

-

- Cultured Salmon

-

- Cultured Tuna

-

- Cultured Shrimp

-

- Cultured Crab / Lobster

-

- Cultured Whitefish

-

- Other

- Deli & Processed Specialties

-

- Cultured Cold Cuts

-

- Cultured Salami

-

- Cultured Pepperoni

-

- Cultured Pastrami

-

- Cultured Sandwich Fillings

- Hybrid & Blended Products

-

- Meat and Plant Blends

-

- Conventional Meat Blends

-

- Cultured Protein–Infused Snacks

-

- Bakery Fillings

- Ready-to-Eat / Ready-to-Cook Meals

-

- Frozen Meals

-

- Pre-Cooked Meals

-

- Cultured Meat Meal

-

- Soups & Stews with Cultured Meat

- Ethnic & Regional Foods

- Others

- Benelux Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

-

- Hypermarkets & Supermarkets

-

- Convenience Stores

-

- Food & Drink Specialty Stores

-

- Online

- Benelux End Use Outlook (Revenue, USD Million; 2019-2032)

-

- HoReCa

-

- Household / Retail

-

- Processed Food Industry

-

- Pet Food Industry

-

- Others

- Russia

- Russia Source Type Outlook (Revenue, USD Million 2019-2032)

-

- Poultry

-

- Beef

-

- Pork

-

- Seafood

-

- Duck

-

- Lamb / Mutton

-

- Goat

-

- Rabbit

-

- Kangaroo

-

- Horse Meat

-

- Bison / Buffalo

-

- Camel Meat

-

- Reptile Meat

-

- Others

- Russia Production Technique Outlook (Revenue, USD Million; 2019-2032)

-

- Scaffold-Based Technique

-

- Suspension (Scaffold-Free / Pellet-Based) Cultivation

-

- 3D Bioprinting

-

- Self-Organizing Cell Cultures

-

- Extrusion + Hybrid Plant-Cell Technology

-

- Microcarrier-Based Bioreactor Systems

-

- Organoid Intelligence & Stem Cell-Derived Techniques

-

- Other

- Russia Application Outlook (Revenue, USD Million; 2019-2032)

-

- Processed Meat

-

- Bars

-

- Nuggets

-

- Burgers & Burger Patties

-

- Meatballs

-

- Sausages

-

- Hot Dogs

-

- Minced Meat / Strips

- Whole-Cut & Premium Meats

-

- Cultured Steak

-

- Cultured Chicken Breast

-

- Cultured Pork Chops

-

- Cultured Lamb

-

- Duck Breast & Exotic Cuts

- Cultured Seafood Products

-