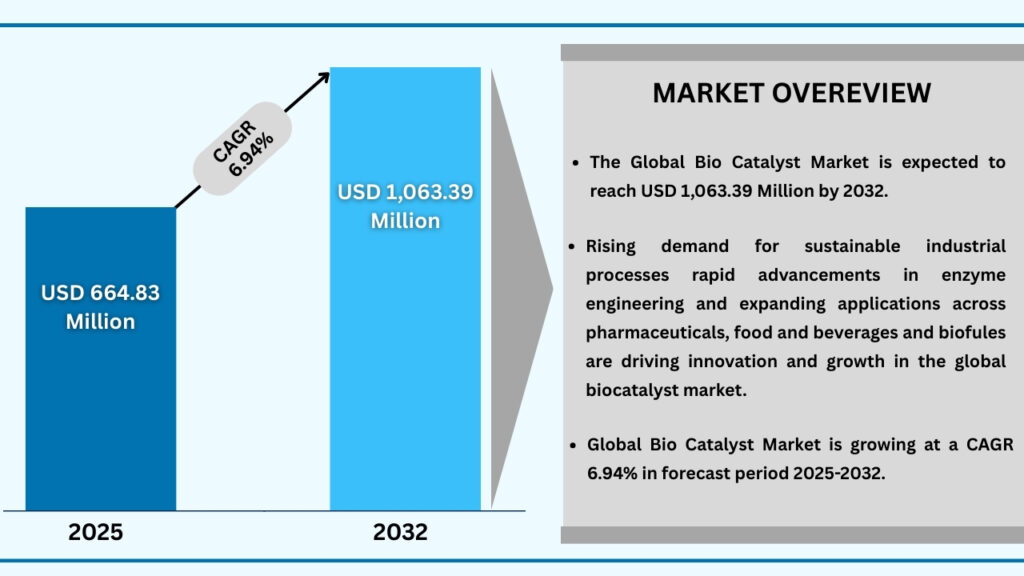

Market Synopsis

The global biocatalyst market size was USD 621.68 million in 2024 and is expected to reach USD 1,063.39 million at a CAGR of 6.94% during the forecast period from 2025 to 2032. The global biocatalyst market is experiencing steady growth as industries increasingly shift toward sustainable and eco-friendly solutions. Biocatalysts naturally derived enzymes and microorganisms are being widely adopted across sectors like food and beverages, pharmaceuticals, biofuels, agriculture, and cleaning products due to their efficiency, specificity, and lower environmental impact compared to traditional chemical processes. Demand is particularly strong in the pharmaceutical and biofuel industries, where biocatalysts play a critical role in producing high-value compounds and renewable energy. North America and Europe currently dominate the market, supported by advanced biotechnology research and strong regulatory backing, while Asia-Pacific is emerging as a high-growth region fuelled by rapid industrialization, expanding chemical and food processing industries, and rising environmental concerns. Despite challenges such as high production costs, stability issues, and scale-up limitations, ongoing advancements in enzyme engineering, synthetic biology, and protein optimization are creating exciting opportunities. With growing emphasis on green chemistry and circular economy practices, biocatalysts are set to become an essential driver of innovation in sustainable industrial processes worldwide.

Global Bio Catalyst Market (USD million)

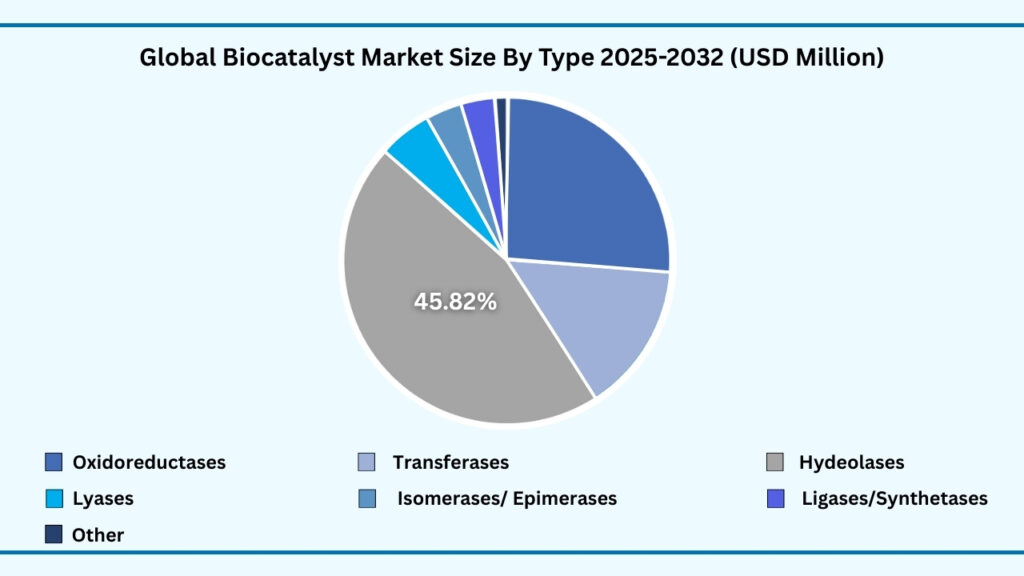

Global Bio Catalyst Market by Type Insights:

Hydrolases segment accounted for market share of share 45.89% in 2024 in the global bio catalyst market.

The Hydrolases segment holds the leading position in the global biocatalyst market, capturing 45.89% of the share in 2024. Revenues in this category are projected to reach USD 489.15 million, growing at a CAGR of 6.97% during the forecast period from 2025 to 2032. Hydrolases dominate the type segment due to their broad applications in industries such as food and beverages, biofuels, and pharmaceuticals. Their efficiency in breaking down complex molecules like starches, fats, and proteins has made them indispensable in processes ranging from brewing and baking to detergent formulation and drug synthesis. Companies like Novozymes, DuPont (IFF), and BASF SE are at the forefront of innovation, leveraging hydrolases to develop enzymes with enhanced stability and efficiency tailored for industrial-scale operations.

Beyond hydrolases, other enzyme classes are steadily carving their niche. Oxidoreductases are gaining traction in biofuel production, specialty chemicals, and green chemistry applications due to their role in oxidation-reduction reactions. Transferases and Lyases are finding increasing utility in pharmaceuticals, agrochemicals, and polymer synthesis, particularly as industries explore biocatalysts for sustainable production pathways. Likewise, Isomerases/Epimerases are being studied for their potential in carbohydrate processing and rare sugar production, which are vital for nutraceuticals and functional foods. Ligases/Synthetases, while relatively smaller in market share, are critical in DNA manipulation and biotechnological research, with expanding relevance in synthetic biology and genetic engineering.

The others category, comprising emerging and specialized enzyme classes, is also showing promise, particularly with advances in enzyme engineering and protein design. Academic and industrial collaborations are opening new avenues for tailoring these biocatalysts to meet industry-specific needs. For example, customized enzyme cocktails are being developed for bioplastic degradation, waste valorisation, and pharmaceutical intermediates. Collectively, the diversification across enzyme types is expanding the functional scope of the global biocatalyst market, ensuring that innovation extends well beyond traditional applications and enabling industries to embrace greener and more efficient production systems.

Global Bio Catalyst Market, By Type (USD million)

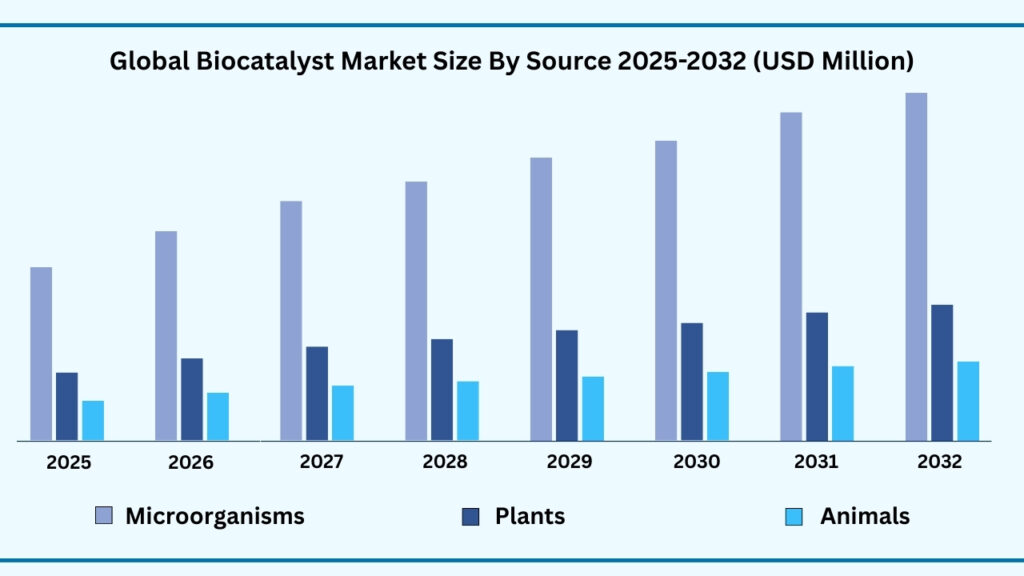

Global Bio Catalyst Market by Source Insights:

Microorganisms segment accounted for market share of share 71.40% in 2024 in the global bio catalyst market.

The Microorganisms segment leads the global biocatalyst market, accounting for the largest share of 71.40% in 2024. Revenues in this category are projected to reach USD 759.82 million during the forecast period from 2025 to 2032, expanding at a CAGR of 6.95%. Microorganisms dominate as a source due to their versatility, scalability, and efficiency in enzyme production. Bacteria, fungi, and yeast are widely used to produce industrial enzymes for applications in pharmaceuticals, food processing, detergents, and biofuels. Their ability to be genetically engineered and optimized through protein engineering has made them indispensable for large-scale biocatalytic processes. Industry leaders such as Novozymes and DSM are actively investing in microbial enzyme platforms, creating tailored solutions for diverse industries and driving the segment’s strong performance.

Alongside microorganisms, plants serve as an important source of biocatalysts, particularly in food, beverages, and specialty chemical production. Plant-derived enzymes like papain (from papaya), bromelain (from pineapple), and lipoxygenases play a critical role in food processing, meat tenderization, brewing, and nutraceutical applications. While plants represent a smaller market share compared to microorganisms, their natural availability, ease of extraction, and consumer-friendly perception make them a valuable option, especially for clean-label and natural product segments. Companies focusing on plant-based enzyme development are aligning with the rising demand for natural and sustainable products in the food and wellness industries.

The animal-derived biocatalysts segment, though relatively limited in scale, retains significance in pharmaceutical and clinical applications. Enzymes such as trypsin, pepsin, and rennin are widely used in drug development, protein digestion studies, and dairy processing. However, ethical considerations, higher production costs, and sourcing challenges have somewhat restricted their growth compared to microbial and plant sources. Nonetheless, innovations in purification and recombinant production are helping mitigate these limitations, ensuring their continued relevance in specialized applications. Together, the combination of microbial dominance, plant-based opportunities, and animal-derived specificity highlights the diverse sourcing strategies that underpin the global biocatalyst market, reflecting its adaptability to meet the evolving demands of multiple industries.

Global Bio Catalyst Market, By Source (USD million)

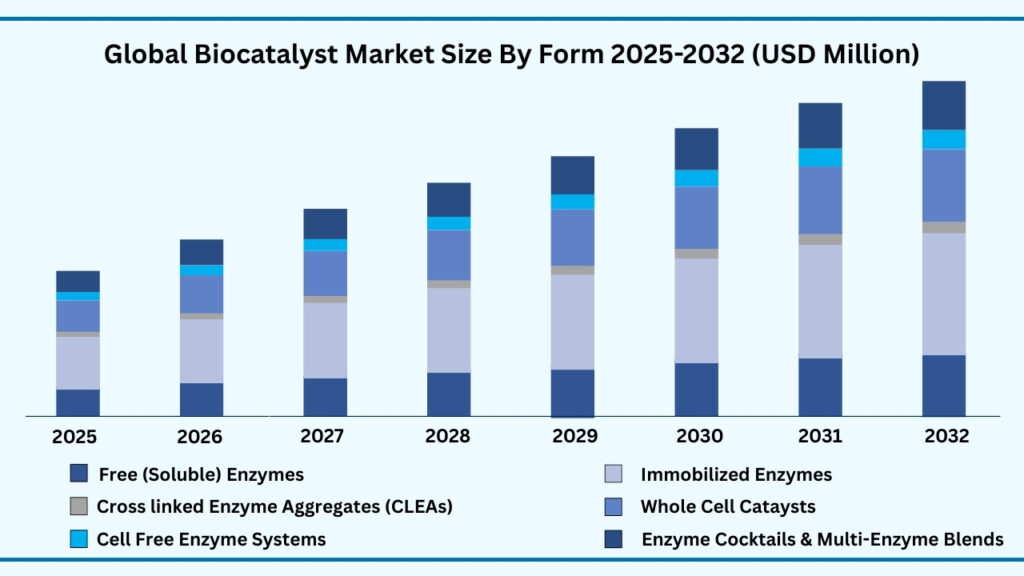

Global Bio Catalyst Market by Form Insights:

Immobilized Enzymes segment accounted for market share of share 34.14% in 2024 in the global bio catalyst market.

The Immobilized enzymes segment leads the global biocatalyst market, accounting for the largest share of 34.14% in 2024. Revenues in this category are projected to reach USD 363.30 million during the forecast period from 2025 to 2032, expanding at a CAGR of 6.95%. Immobilized enzymes dominate this segment due to their high stability, reusability, and efficiency in industrial applications. By anchoring enzymes onto solid supports, industries are able to enhance catalytic activity while reducing costs associated with repeated enzyme use. This has made immobilized enzymes indispensable in food and beverage processing, pharmaceuticals, and biofuel production. Leading players such as Novozymes and Codexis are innovating advanced immobilization techniques to improve enzyme robustness, further reinforcing the leadership of this segment.

Beyond immobilized enzymes, other forms are steadily contributing to the market’s growth. Free (soluble) enzymes remain widely used in research and laboratory-scale processes due to their ease of application and straightforward reaction kinetics, though their limited stability restricts broader adoption at the industrial level. Cross-linked enzyme aggregates (CLEAs) are emerging as a cost-effective and versatile alternative, offering enhanced stability and activity without requiring complex immobilization supports. Meanwhile, whole-cell catalysts are gaining traction in pharmaceuticals, fine chemicals, and agro-industrial processes, as they allow the use of naturally occurring enzyme systems within living or engineered microbial cells, reducing the need for costly purification steps.

Looking ahead, advanced formats such as cell-free enzyme systems and enzyme cocktails or multi-enzyme blends are expected to create new opportunities. Cell-free systems enable precise control over metabolic pathways and are being explored in synthetic biology and biopharmaceutical manufacturing. Enzyme cocktails, on the other hand, are increasingly used in lignocellulosic biomass conversion and bioplastic degradation, where a combination of enzymes is required to efficiently break down complex substrates. Together, these diverse forms reflect the adaptability of the biocatalyst market, with immobilized enzymes anchoring current revenues while emerging technologies pave the way for next-generation industrial bioprocesses.

Global Bio Catalyst Market, By Form (USD million)

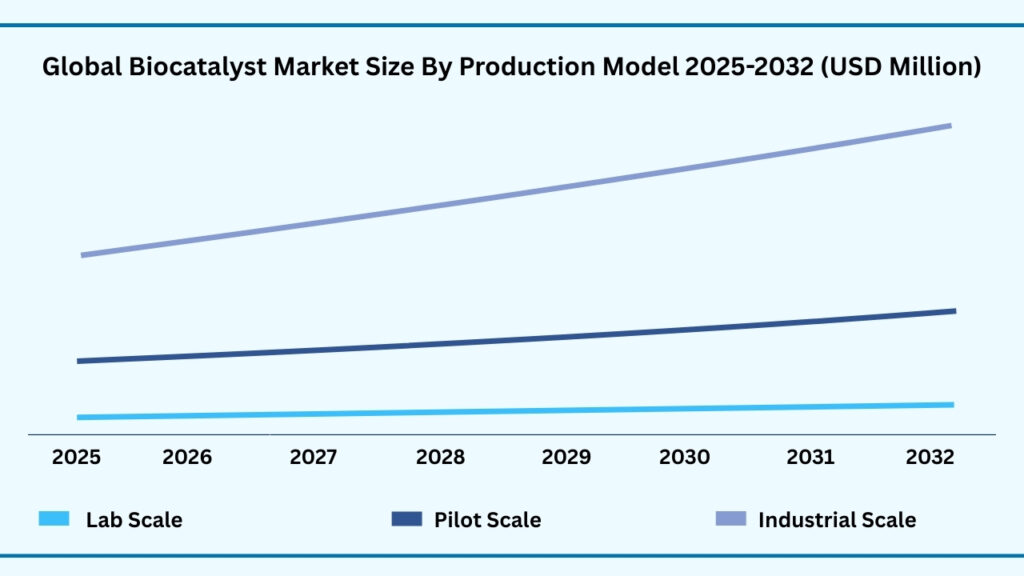

Global Bio Catalyst Market by Production Model Insights:

Industrial Scale segment accounted for market share of share 64.23% in 2024 in the global bio catalyst market.

The Industrial scale segment dominates the global biocatalyst market, capturing the largest share of 64.23% in 2024. Revenues from this category are expected to reach USD 683.42 million by the end of the forecast period, growing at a CAGR of 6.95%. This leadership is driven by the widespread use of biocatalysts in large-scale production processes across industries such as food and beverages, biofuels, pharmaceuticals, and specialty chemicals. Industrial-scale deployment allows companies to achieve cost efficiencies, high throughput, and consistent product quality. For instance, biocatalysts are extensively used in brewing, dairy processing, detergent manufacturing, and the synthesis of active pharmaceutical ingredients (APIs). Industry giants like BASF SE, Novozymes, and DuPont (IFF) are heavily investing in process optimization and enzyme engineering to enhance performance at commercial production levels, ensuring the segment’s strong market hold.

In comparison, the Pilot scale segment serves as an essential bridge between laboratory innovation and full-scale industrial application. Pilot-scale operations enable companies to test enzyme formulations, evaluate process efficiency, and optimize reaction conditions before committing to large-scale investments. This stage is particularly valuable in biofuel development, pharmaceutical intermediates, and specialty chemical production, where cost and regulatory considerations are significant. Academic–industry collaborations and biotech start-ups often rely on pilot-scale facilities to validate proof-of-concept studies, making this segment a critical stepping stone in translating biocatalyst research into commercial success.

The Lab scale segment, while accounting for a smaller share, plays a vital role in advancing fundamental research and innovation. Laboratory-scale applications are primarily focused on enzyme discovery, protein engineering, and proof-of-concept experiments. Universities, research institutes, and early-stage biotech firms drive this space, often experimenting with novel enzyme variants, immobilization techniques, or synthetic biology approaches to expand the scope of biocatalysis. Although revenues from lab-scale use are limited, breakthroughs at this level often lay the foundation for pilot and industrial-scale commercialization. Collectively, the strong dominance of industrial-scale applications, supported by pilot-scale validation and lab-scale innovation, highlights the interconnected nature of the biocatalyst market, ensuring a balanced ecosystem that fosters both scientific discovery and large-scale economic impact.

Global Bio Catalyst Market, By Form (USD million)

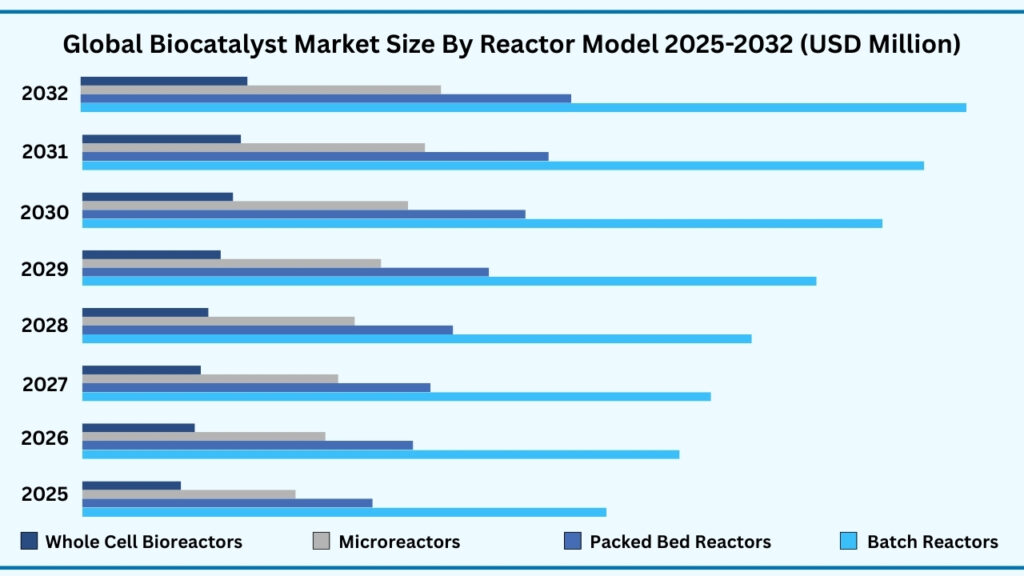

Global Bio Catalyst Market by Reactor Mode Insights:

Batch reactors segment accounted for market share of share 46.34% in 2024 in the global bio catalyst market.

The Batch reactor segment leads the global biocatalyst market, capturing the largest share of 46.34% in 2024. Revenues from this category are expected to reach USD 494.38 million during the forecast period, growing at a CAGR of 6.98%. Batch reactors dominate due to their flexibility, ease of operation, and suitability for a wide range of enzymatic processes. They are particularly well-suited for small- to medium-scale production, specialty chemical synthesis, and pharmaceutical applications where precision and control are critical. Their ability to handle varying reaction conditions without the need for continuous feed makes them highly attractive for R&D and pilot-scale operations. Global players such as Codexis and Novozymes often rely on batch processing during early product development stages, highlighting its importance as both a research and commercial tool.

Beyond batch reactors, other reactor modes are steadily expanding their role in industrial biocatalysis. Packed-bed reactors are increasingly preferred for continuous operations, particularly in large-scale processes like biofuel production and wastewater treatment. Their design allows immobilized enzymes or whole cells to remain fixed while substrates flow through, improving stability and reusability. Microreactors, though relatively new, are gaining attention for their ability to conduct reactions at microscale with high efficiency and precision, making them valuable in high-value applications such as pharmaceuticals, fine chemicals, and diagnostics. These compact systems also offer advantages in process intensification and scalability, aligning with the industry’s push toward cost-effective and sustainable production.

The Whole-cell bioreactor segment represents another promising frontier, leveraging the power of living or engineered microorganisms to catalyse complex biochemical reactions. These reactors are especially important in producing bio-based chemicals, therapeutic proteins, and nutraceuticals, where multi-enzyme pathways are required. Their ability to bypass costly enzyme isolation steps gives them a competitive edge in certain applications. Together, the dominance of batch reactors, the growing relevance of packed-bed and microreactors, and the innovation potential of whole-cell systems illustrate a diverse and evolving reactor landscape. This balanced mix ensures that the global biocatalyst market can cater to both established industrial applications and emerging frontiers in biotechnology.

Global Bio Catalyst Market, By Reactor Mode (USD million)

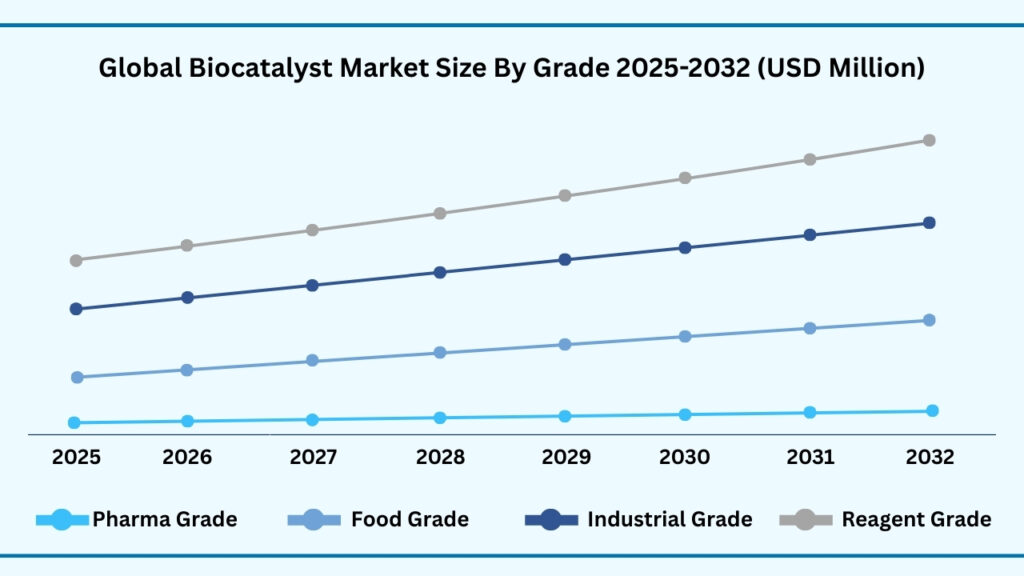

Global Bio Catalyst Market by Grade Insights:

Industrial Grade segment accounted for market share of share 44.39% in 2024 in the global bio catalyst market.

The Industrial Grade segment holds the leading position in the global biocatalyst market, capturing the largest share of 44.39% in 2024, with revenues projected to reach USD 472.84 million by the end of the forecast period, growing at a CAGR of 6.96%. This dominance is primarily driven by the widespread use of industrial-grade enzymes and biocatalysts in large-scale applications such as biofuel production, detergents, textiles, and pulp & paper processing. Their ability to replace harsh chemical processes with eco-friendly and cost-efficient alternatives has made them indispensable across industries seeking sustainable solutions. For instance, the growing reliance on enzymatic biofuel production highlights how industrial-grade biocatalysts are at the heart of reducing carbon emissions while meeting global energy needs.

Alongside industrial applications, the Pharma Grade sub-segment represents a crucial area of growth, propelled by the rising demand for high-purity biocatalysts in drug synthesis, chiral intermediate production, and biopharmaceutical manufacturing. Enzymes such as lipases and transaminases are being widely used to achieve high selectivity in pharmaceutical compounds, ensuring better yields and reduced side reactions compared to traditional chemical synthesis. The increasing adoption of green chemistry principles in drug development, along with regulatory encouragement for sustainable production methods, is reinforcing the importance of pharma-grade biocatalysts. Companies like Codexis and Novozymes are actively advancing biocatalytic processes tailored for pharmaceutical innovations, signalling strong long-term opportunities in this space.

Meanwhile, Food Grade and Reagent Grade sub-segments are carving out significant and complementary roles. Food-grade biocatalysts are gaining popularity in bakery, dairy, and beverage industries, where enzymes enhance product texture, flavour, and nutritional profile, aligning with the consumer shift toward healthier and clean-label foods. Reagent-grade biocatalysts, though smaller in market share, remain critical in academic research, diagnostics, and laboratory-scale experiments, serving as the backbone of innovation and proof-of-concept studies. Together, these sub-segments demonstrate the diverse functionality of biocatalysts, where industrial grade drives large-scale adoption, pharma grade ensures precision and sustainability in healthcare, and food and reagent grades foster consumer wellness and scientific exploration.

Global Bio Catalyst Market, By Grade (USD million)

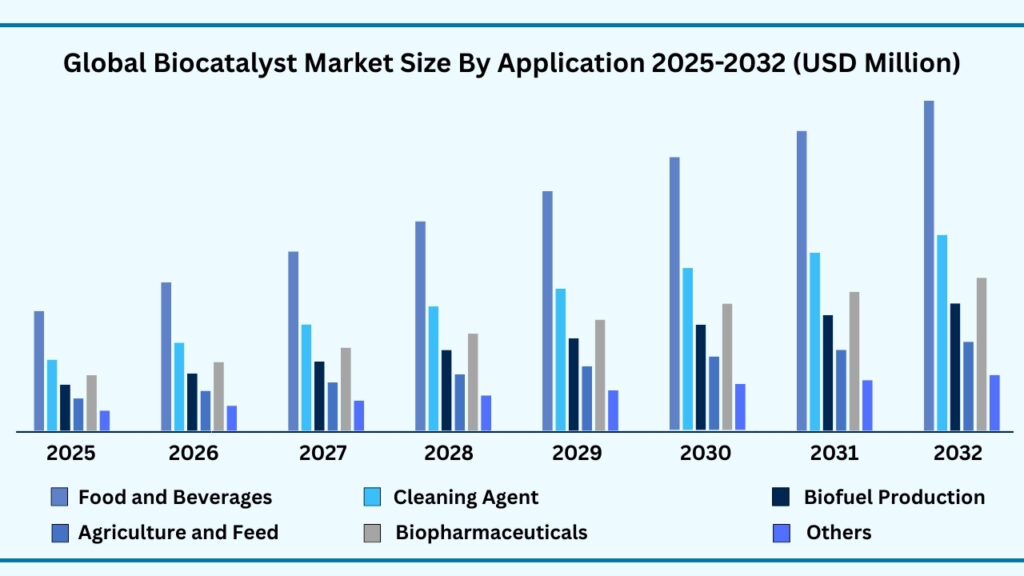

Global Bio Catalyst Market by Application Insights:

Food and Beverages segment accounted for market share of share 41.30% in 2024 in the global bio catalyst market.

The Food and Beverages segment represents the largest share of the global biocatalyst market, accounting for 41.30% in 2024. Revenues from this segment are projected to reach USD 439.90 million during the forecast period, expanding at a CAGR of 6.96%. The food and beverage industry has become the core adopter of biocatalyst technologies because enzymes are directly linked to improving quality, flavour, and efficiency in food processing. Biocatalysts are widely used in baking, dairy, brewing, and juice clarification, where they enhance texture, shelf life, and taste while supporting clean-label production. For instance, amylases are commonly applied in bakeries to improve dough handling and bread softness, while lactase enzymes are making lactose-free dairy a mainstream option for health-conscious consumers. With rising demand for healthier, natural, and functional food products, food manufacturers are heavily investing in enzyme-driven innovations to meet evolving consumer expectations.

Beyond food applications, Cleaning Agents and Biofuel Production are two fast-expanding areas of biocatalyst utilization. Enzymes in detergents have revolutionized the cleaning industry by enabling stain removal at lower temperatures, reducing both energy consumption and environmental impact. Their popularity is reinforced by consumer and regulatory push for eco-friendly household and industrial cleaning products. In biofuels, biocatalysts play a central role in breaking down biomass into fermentable sugars, supporting sustainable ethanol and biodiesel production. As global energy policies emphasize reducing carbon footprints, enzymatic biofuel processes are being scaled up as viable alternatives to fossil fuels. These applications highlight the dual impact of biocatalysts—not only improving performance in everyday products but also helping industries transition toward greener practices.

Meanwhile, Agriculture and Feed, Biopharmaceuticals, and Others are carving out complementary roles in the broader application landscape. In agriculture and animal nutrition, enzymes are being applied to improve feed digestibility and crop yield, offering farmers sustainable tools to increase productivity. Biopharmaceutical applications are gaining importance as biocatalysts enable the synthesis of complex drugs and therapeutic proteins with higher precision and lower environmental costs compared to traditional methods. Smaller but vital applications grouped under “Others,” such as textiles and cosmetics, demonstrate the versatility of enzymes in enhancing sustainability across diverse industries. Together, these segments create a balanced ecosystem where food and beverages lead in adoption, cleaning agents and biofuels accelerate growth through sustainability, and agriculture, healthcare, and specialty use expand the market’s reach into high-value applications.

Global Bio Catalyst Market, By Application (USD million)

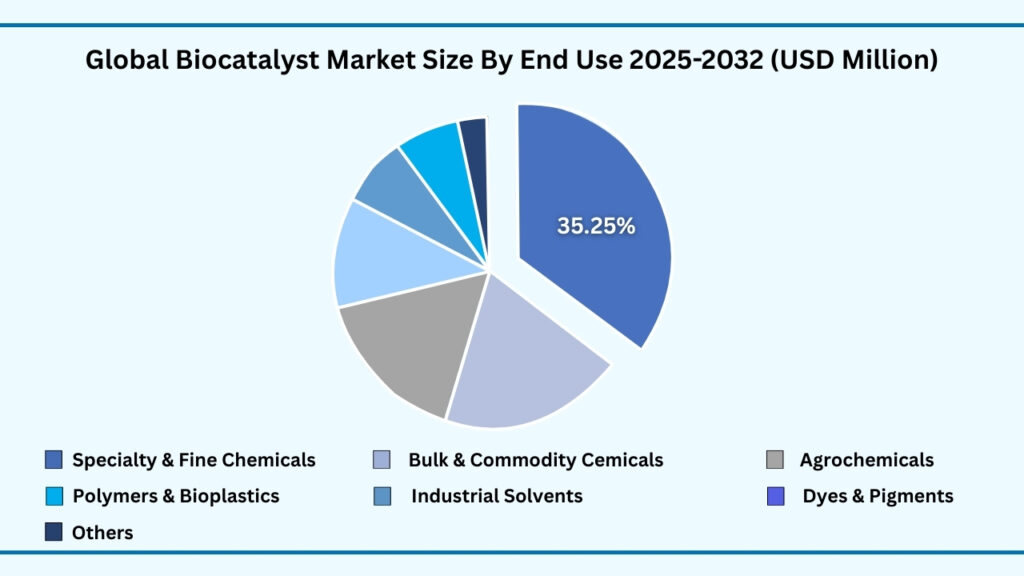

Global Bio Catalyst Market by End Use Insights:

Speciality & Fine Chemicals segment accounted for market share of share 35.30% in 2024 in the global bio catalyst market.

The Specialty & Fine Chemicals segment represents the largest share of the global biocatalyst market, accounting for 35.30% in 2024. Revenues from this segment are projected to reach USD 376.31 million during the forecast period, expanding at a CAGR of 6.97%. Specialty and fine chemicals have emerged as the leading end-use area because biocatalysts enable high selectivity, efficiency, and greener production processes. Enzymes are widely applied in synthesizing flavors, fragrances, vitamins, and active pharmaceutical intermediates, where precision and purity are critical. For example, lipases and oxidoreductases are increasingly used to replace harsh chemical catalysts in fine chemical manufacturing, reducing energy consumption and hazardous by-products. With sustainability and efficiency becoming key priorities, chemical companies are investing in biocatalytic processes to gain both cost advantages and regulatory compliance.

Beyond fine chemicals, Bulk & Commodity Chemicals, Agrochemicals, and Polymers & Bioplastics are gaining momentum as biocatalysts expand their industrial reach. In bulk and commodity chemicals, enzymes help simplify large-scale processes, making them more energy-efficient and cost-effective. The agrochemical industry is using biocatalysts to create safer, biodegradable crop protection solutions and improve the synthesis of plant growth regulators. Similarly, in polymers and bioplastics, biocatalysts are enabling the production of bio-based and degradable alternatives to conventional plastics. Companies like BASF and Novozymes are already integrating enzyme-based methods into polymer production, aligning with the growing demand for eco-friendly packaging and sustainable materials. These segments illustrate how biocatalysts are transforming traditional chemical industries into more responsible and innovative sectors.

Meanwhile, Industrial Solvents, Dyes & Pigments, and Others continue to play supportive but important roles in diversifying the end-use landscape. In solvents, enzymes facilitate the production of bio-based options that are less toxic and more sustainable compared to petroleum-derived alternatives. The dyes and pigments sector is also exploring enzyme-based synthesis to reduce reliance on hazardous chemicals, especially in textile and coating industries. The “Others” category, including emerging applications in electronics and specialty coatings, highlights the adaptability of biocatalysts to niche but high-value markets. Together, these segments create a balanced ecosystem where specialty & fine chemicals dominate due to their precision and market demand, while commodity, agro, polymer, and niche applications expand the overall market reach, driving the transition toward greener and more sustainable chemical production.

Global Bio Catalyst Market, By End Use (USD million)

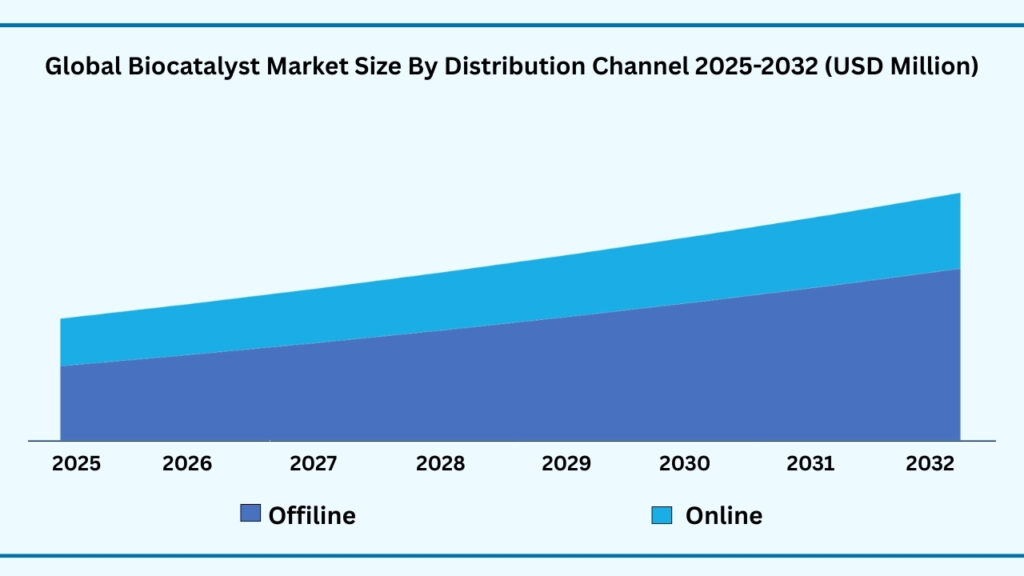

Global Bio Catalyst Market by Distribution Channel Insights:

Offline segment accounted for market share of share 77.39% in 2024 in the global bio catalyst market.

The Offline segment represents the largest share of the global biocatalyst market, accounting for 77.39% in 2024. Revenues from this segment are projected to reach USD 823.60 million during the forecast period, expanding at a CAGR of 6.95%. Offline channels, including distributors, specialized dealers, and direct sales to industrial clients, have remained the preferred mode of purchasing biocatalysts due to the technical complexity and need for expert guidance in selecting the right enzyme or catalyst for specific applications. Many industries, such as pharmaceuticals, food processing, and specialty chemicals, rely on offline consultation to ensure optimal product performance, correct storage conditions, and compliance with safety standards. Companies like Novozymes and DSM maintain strong offline networks to provide hands-on support, training, and post-sale service, reinforcing the dominance of this channel.

In comparison, Online distribution is gaining momentum as digital platforms and e-commerce portals offer convenient access to a wider range of biocatalysts, especially for research institutions, small-scale labs, and start-ups. Online channels enable quick comparison of products, easier procurement, and access to technical datasheets, making them increasingly attractive for buyers with smaller orders or specialized requirements. Companies are also integrating digital tools such as live chat support, virtual demonstrations, and detailed application guides to assist customers in selecting the right biocatalysts, thereby bridging the expertise gap that offline channels traditionally provided.

Meanwhile, both offline and online channels together are shaping a comprehensive distribution ecosystem. Offline channels continue to dominate industrial-scale and high-value applications where expert consultation and quality assurance are critical, while online sales are expanding market accessibility and driving adoption among smaller enterprises, educational institutions, and research labs. This dual-channel approach ensures that biocatalysts reach both traditional industrial buyers and digitally savvy consumers, enhancing market penetration and supporting steady growth across diverse end-use segments.

Global Bio Catalyst Market, By Distribution Channel (USD million)

Global Bio Catalyst Market by Region Insights:

Asia Pacific segment accounted for market share of share 36.23% in 2024 in the global bio catalyst market.

The Asia Pacific region dominates the global biocatalyst market, accounting for 36.23% of the share in 2024. Revenues from this region are projected to reach USD 385.84 million during the forecast period, expanding at a CAGR of 6.96%. This leadership is largely driven by rapidly expanding industrial and biopharmaceutical sectors, rising adoption of sustainable and eco-friendly manufacturing processes, and supportive government initiatives in countries such as China, India, Japan, and South Korea. Biocatalysts are increasingly applied in food processing, biofuel production, and specialty chemicals, where industries seek cost-efficient and environmentally sustainable solutions. Companies like Novozymes and Codexis are partnering with regional manufacturers to implement enzyme-driven processes, further solidifying Asia Pacific’s position as the largest and fastest-growing market for biocatalysts.

In North America, the market remains highly mature due to advanced industrial infrastructure, strong R&D investments, and widespread adoption of cutting-edge enzyme technologies. Biocatalysts are extensively used in pharmaceuticals, specialty chemicals, and food industries to enhance product quality, improve process efficiency, and reduce environmental impact. The U.S. and Canada host major biocatalyst producers and research hubs, enabling rapid innovation and commercialization of enzyme-based solutions. Similarly, Europe continues to maintain significant market presence, supported by stringent environmental regulations, sustainability goals, and strong industrial applications across Germany, France, and the U.K. European companies increasingly focus on developing high-performance enzymes for fine chemicals, bio-based polymers, and industrial solvents, reflecting a commitment to green manufacturing practices.

Latin America (LATAM) and the Middle East & Africa (MEA) represent emerging markets that are gradually expanding their biocatalyst adoption. LATAM countries such as Brazil and Mexico are increasingly implementing enzyme technologies in biofuels, food processing, and agrochemical production, while MEA markets like South Africa and the UAE are exploring sustainable solutions for industrial and pharmaceutical applications. Although infrastructure and funding limitations remain challenges, growing awareness of eco-friendly technologies, coupled with government incentives and international collaborations, is creating a strong foundation for future growth. Collectively, Asia Pacific anchors the market with rapid adoption and industrial expansion, North America and Europe sustain steady growth through technological leadership, and LATAM and MEA are emerging as new frontiers driving the long-term global outlook for biocatalyst applications.

Global Bio Catalyst Market, By Region (USD million)

Major Companies and Competitive Landscape

The global biocatalyst market is expanding rapidly, driven by growing demand for sustainable and efficient solutions across industries such as food & beverages, pharmaceuticals, chemicals, and biofuels. Companies are focusing on partnerships, acquisitions, and technological collaborations to enhance enzyme innovation, optimize industrial processes, and develop high-performance, eco-friendly biocatalysts. Efforts are also directed toward scaling up production, improving enzyme stability and selectivity, and exploring emerging applications in bio-based chemicals and therapeutics. Key companies active in the global biocatalyst market include:

- Novozymes A/S

- Codexis, Inc.

- BASF SE

- DuPont de Nemours, Inc.

- Royal DSM N.V.

- Chr. Hansen Holding A/S

- Dyadic International, Inc.

- AB Enzymes GmbH

- Amano Enzyme Inc.

- Biocatalysts Limited

- Lonza Group Ltd.

- Prozomix Limited

- Givaudan S.A.

- Carbios

- HydRegen Limited

- Debut Biotech

- EnginZyme AB

- Unilever PLC

- Soufflet Group

- Fermenta Biotech Ltd.

- Piramal Enterprises Ltd.

- Zymtronix Catalytic Systems Inc.

- RP Management LLC

- Panacea Biotec

- Aladdin Scientific

Scope of Research

| Report Details | Outcome |

|---|---|

| Market size in 2024 | USD 664.83 Million |

| CAGR (2024–2032) | 6.94% |

| Revenue forecast to 2033 | USD 1,063.39 Million |

| Base year for estimation | 2024 |

| Historical data | 2019–2023 |

| Forecast period | 2025–2032 |

| Quantitative units | Revenue in USD Million and CAGR in % from 2025 to 2032 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Type, By Source, By Form, By Production Model, By Reactor Mode, By Grade, By Application, By End User, By Distribution Channel and By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Country scope | U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Benelux, Russia, Finland, Sweden, Rest of Europe, China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia, New Zealand Rest of APAC, Brazil, Rest of LATAM, Saudi Arabia, Rest of MEA |

| Key companies profiled | Novozymes A/S, Codexis, Inc., BASF SE, DuPont de Nemours, Inc., Royal DSM N.V., Chr. Hansen Holding A/S, Dyadic International, Inc., AB Enzymes GmbH, Amano Enzyme Inc., Biocatalysts Limited, Lonza Group Ltd., Prozomix Limited, Givaudan S.A., Carbios, HydRegen Limited, Debut Biotech, EnginZyme AB, Unilever PLC, Soufflet Group, Fermenta Biotech Ltd., Piramal Enterprises Ltd., Zymtronix Catalytic Systems Inc., RP Management LLC, Panacea Biotec, Aladdin Scientific. |

| Customization scope | 10 hours of free customization and expert consultation |

Follow us on: Facebook, Twitter, Instagram and LinkedIn.

Chapter 1. Introduction

1.1. Market Definition

1.2. Objectives of the study

1.3. Overview of Bio-Catalyst Market

1.4. Currency and pricing

1.5. Limitation

1.6. Markets covered

1.7. Research Scope

Chapter 2. Research Methodology

2.1. Research Sources

2.1.1.Primary

2.1.2.Secondary

2.1.3.Paid Sources

2.2. Years considered for the study

2.3. Assumptions

2.3.1.Market value

2.3.2.Market volume

2.3.3.Exchange rate

2.3.4.Price

2.3.5.Economic & political stability

Chapter 3. Executive Summary

3.1. Summary Snapshot, 2025–2032

Chapter 4. Key Insights

4.1. Production consumption analysis

4.2. Strategic partnerships & alliances

4.3. Joint ventures

4.4. Acquisition of local players

4.5. Contract manufacturing

4.6. Digital & e-commerce sales channels

4.7. Compliance with standards

4.8. Value chain analysis

4.9. Raw material sourcing

4.10. Formulation & manufacturing

4.11. Distribution & retail

4.12. Import-export analysis

4.13. Brand comparative analysis

4.14. Technological advancements

4.15. Porter’s five force

4.15.1. Threat of new entrants

4.15.1.1. Capital requirment

4.15.1.2. Product knowledge

4.15.1.3. Technical knowledge

4.15.1.4. Customer relation

4.15.1.5. Access to appliation and technology

4.15.2. Threat of substitutes

4.15.2.1. Cost

4.15.2.2. Performance

4.15.2.3. Availability

4.15.2.4. Technical knowledge

4.15.2.5. Durability

4.15.3. Bargainning power of buyers

4.15.3.1. Numbers of buyers relative to suppliers

4.15.3.2. Product differentiation

4.15.3.3. Threat of forward integration

4.15.3.4. Buyers volume

4.15.4. Bargainning power of suppliers

4.15.4.1. Suppliers concentration

4.15.4.2. Buyers switching cost to other suppliers

4.15.4.3. Threat of backward integration

4.15.5. Bargainning power of suppliers

4.15.5.1. Industry concentration

4.15.5.2. Industry growth rate

4.15.5.3. Product differentiation

4.16. Patent analysis

4.17. Regulation coverage

4.18. Pricing analysis

4.19. Competitive Metric Space Analysis

Chapter 5. Market Overview

5.1. Drivers

5.1.1.Growing Demand for Sustainable Industrial Processes

5.1.2.Rising Applications in Pharmaceuticals & Healthcare

5.1.3.Advancements in Enzyme Engineering & Biotechnology

5.2. Restraints

5.2.1.High Production & Purification Costs

5.2.2.Limited Stability Under Extreme Conditions

5.3. Opportunities

5.3.1.Expansion in Biofuels & Renewable Energy

5.3.2.Growing Role in Food & Beverage Industry

5.3.3.Integration with Green Chemistry

5.4. Challenges

5.4.1.Scaling from Lab to Industry

5.4.2.Intellectual Property & Regulatory Issues

Chapter 6. Global Bio-Catalyst Market By Type Insights & Trends, Revenue (USD Million), Volume

(Kiloton)

6.1. Type Dynamics & Market Share, 2019–2032

6.1.1. Oxidoreductases

6.1.2. Transferases

6.1.3. Hydrolases

6.1.4. Lyases

6.1.5. Isomerases / Epimerases

6.1.6. Ligases / Synthetases

6.1.7. Other

Chapter 7. Global Bio-Catalyst Market By Source Insights & Trends, Revenue (USD Million),

7.1. Source Dynamics & Market Share, 2019–2032

7.1.1.Microorganisms

7.1.2.Plants

7.1.3.Animal

Chapter 8. Global Bio-Catalyst Market By Form Insights & Trends, Revenue (USD Million),

8.1. Form Dynamics & Market Share, 2019–2032

8.1.1. Free (soluble) enzymes

8.1.2. Immobilized enzymes

8.1.3. Cross-linked enzyme aggregates (CLEAs)

8.1.4. Whole-cell catalysts

8.1.5. Cell-free enzyme systems

8.1.6. Enzyme cocktails & multi-enzyme blends

Chapter 9. Global Bio-Catalyst Market By Production Model Insights & Trends, Revenue (USD

Million),

9.1. Production Model Dynamics & Market Share, 2019–2032

9.1.1. Lab Scale

9.1.2. Pilot Scale

9.1.3. Industrial Scale

Chapter 10. Global Bio-Catalyst Market By Reactor Mode Insights & Trends, Revenue (USD

Million),

10.1. Reactor Mode Dynamics & Market Share, 2019–2032

10.1.1. Batch reactors

10.1.2. Packed-bed reactors

10.1.3. Microreactors

10.1.4. Whole-cell bioreactors

Chapter 11. Global Bio-Catalyst Market By Grade Insights & Trends, Revenue (USD Million),

11.1. Grade Form Dynamics & Market Share, 2019–2032

11.1.1. Pharma Grade

11.1.2. Food Grade

11.1.3. Industrial Grade

11.1.4. Reagent grade

Chapter 12. Global Bio-Catalyst Market By Application Insights & Trends, Revenue (USD Million)

12.1. Application Dynamics & Market Share, 2019–2032

12.1.1. Food and Beverages

12.1.2. Cleaning Agent

12.1.3. Biofuel Production

12.1.4. Agriculture and Feed

12.1.5. Biopharmaceuticals

12.1.6. Others

Chapter 13. Global Bio-Catalyst Market By End Use Insights & Trends, Revenue (USD Million)

13.1. End Use Dynamics & Market Share, 2019–2032

13.1.1. Specialty & Fine Chemicals

13.1.2. Bulk & Commodity Chemicals

13.1.3. Agrochemicals

13.1.4. Polymers & Bioplastics

13.1.5. Industrial Solvents

13.1.6. Dyes & Pigments

13.1.7. Others

Chapter 14. Global Bio-Catalyst Market By Distribution Channel Insights & Trends, Revenue (USD

Million),

14.1. Distribution Channel & Market Share, 2019–2032

14.1.1.Offline

14.1.1.1. Direct Sales (B2B)

14.1.1.2. Distributors / Wholesalers

14.1.1.3. Specialty Chemical Stores / Agents

14.1.1.4. Trade Shows & Industrial Networking

14.1.1.5. Hypermarkets & Supermarkets

14.1.2.Online

14.1.2.1. E-commerce Platforms

14.1.2.2. Direct-to-Consumer (D2C) Websites

14.1.2.3. Subscription & API-Based Ordering

Chapter 15. Global Bio-Catalyst Market Regional Outlook

15.1.Bio-Catalyst Share By Region, 2019–2032

15.2.North America

15.2.1. Market By Type Estimates and Forecast, USD Million, 2019-2032

15.2.1.1. Oxidoreductases

15.2.1.2. Transferases

15.2.1.3. Hydrolases

15.2.1.4. Lyases

15.2.1.5. Isomerases / Epimerases

15.2.1.6. Ligases / Synthetases

15.2.1.7. Other

15.2.2. Market By Source, Market Estimates and Forecast, USD Million, 2019-2032

15.2.2.1. Microorganisms

15.2.2.2. Plants

15.2.2.3. Animal

15.2.3. Market By Form, Market Estimates and Forecast, USD Million, 2019-2032

15.2.3.1. Free (soluble) enzymes

15.2.3.2. Immobilized enzymes

15.2.3.3. Cross-linked enzyme aggregates (CLEAs)

15.2.3.4. Whole-cell catalysts

15.2.3.5. Cell-free enzyme systems

15.2.3.6. Enzyme cocktails & multi-enzyme blends

15.2.4. Market By Production Model, Market Estimates and Forecast, USD Million,

2019-2032

15.2.4.1. Lab Scale

15.2.4.2. Pilot Scale

15.2.4.3. Industrial Scale

15.2.5. Market By Reactor Mode, Market Estimates and Forecast, USD Million,

2019-2032

15.2.5.1. Batch reactors

15.2.5.2. Packed-bed reactors

15.2.5.3. Microreactors

15.2.5.4. Whole-cell bioreactors

15.2.6. Market By Grade, Market Estimates and Forecast, USD Million, 2019-2032

15.2.6.1. Pharma Grade

15.2.6.2. Food Grade

15.2.6.3. Industrial Grade

15.2.6.4. Reagent grade

15.2.7. Market By Application, Market Estimates and Forecast, USD Million, 2019-2032

15.2.7.1. Food and Beverages

15.2.7.2. Cleaning Agent

15.2.7.3. Biofuel Production

15.2.7.4. Agriculture and Feed

15.2.7.5. Biopharmaceuticals

15.2.7.6. Others

15.2.8. Market By End Use, Market Estimates and Forecast, USD Million, 2019-2032

15.2.8.1. Specialty & Fine Chemicals

15.2.8.2. Bulk & Commodity Chemicals

15.2.8.3. Agrochemicals

15.2.8.4. Polymers & Bioplastics

15.2.8.5. Industrial Solvents

15.2.8.6. Dyes & Pigments

15.2.8.7. Others

15.2.9. Market By Distribution Channel, Market Estimates and Forecast, USD

Million,2019-2032

15.2.9.1. Offline

15.2.9.1.1. Direct Sales (B2B)

15.2.9.1.2. Distributors / Wholesalers

15.2.9.1.3. Specialty Chemical Stores / Agents

15.2.9.1.4. Trade Shows & Industrial Networking

15.2.9.1.5. Hypermarkets & Supermarkets

15.2.9.2. Online

15.2.9.2.1. E-commerce Platforms

15.2.9.2.2. Direct-to-Consumer (D2C) Websites

15.2.9.2.3. Subscription & API-Based Ordering

15.2.10. Market By Country, Market Estimates and Forecast, USD Million, 2019-2032

15.2.10.1. US

15.2.10.2. Canada

15.2.10.3. Mexico

15.3.Europe

15.3.1. Market By Type Estimates and Forecast, USD Million, 2019-2032

15.3.1.1. Oxidoreductases

15.3.1.2. Transferases

15.3.1.3. Hydrolases

15.3.1.4. Lyases

15.3.1.5. Isomerases / Epimerases

15.3.1.6. Ligases / Synthetases

15.3.1.7. Other

15.3.2. Market By Source, Market Estimates and Forecast, USD Million, 2019-2032

15.3.2.1. Microorganisms

15.3.2.2. Plants

15.3.2.3. Animal

15.3.3. Market By Form, Market Estimates and Forecast, USD Million, 2019-2032

15.3.3.1. Free (soluble) enzymes

15.3.3.2. Immobilized enzymes

15.3.3.3. Cross-linked enzyme aggregates (CLEAs)

15.3.3.4. Whole-cell catalysts

15.3.3.5. Cell-free enzyme systems

15.3.3.6. Enzyme cocktails & multi-enzyme blends

15.3.4. Market By Production Model, Market Estimates and Forecast, USD Million,

2019-2032

15.3.4.1. Lab Scale

15.3.4.2. Pilot Scale

15.3.4.3. Industrial Scale

15.3.5. Market By Reactor Mode, Market Estimates and Forecast, USD Million,

2019-2032

15.3.5.1. Batch reactors

15.3.5.2. Packed-bed reactors

15.3.5.3. Microreactors

15.3.5.4. Whole-cell bioreactors

15.3.6. Market By Grade, Market Estimates and Forecast, USD Million, 2019-2032

15.3.6.1. Pharma Grade

15.3.6.2. Food Grade

15.3.6.3. Industrial Grade

15.3.6.4. Reagent grade

15.3.7. Market By Application, Market Estimates and Forecast, USD Million, 2019-2032

15.3.7.1. Food and Beverages

15.3.7.2. Cleaning Agent

15.3.7.3. Biofuel Production

15.3.7.4. Agriculture and Feed

15.3.7.5. Biopharmaceuticals

15.3.7.6. Others

15.3.8. Market By End Use, Market Estimates and Forecast, USD Million, 2019-2032

15.3.8.1. Specialty & Fine Chemicals

15.3.8.2. Bulk & Commodity Chemicals

15.3.8.3. Agrochemicals

15.3.8.4. Polymers & Bioplastics

15.3.8.5. Industrial Solvents

15.3.8.6. Dyes & Pigments

15.3.8.7. Others

15.3.9. Market By Distribution Channel, Market Estimates and Forecast, USD

Million,2019-2032

15.3.9.1. Offline

15.3.9.1.1. Direct Sales (B2B)

15.3.9.1.2. Distributors / Wholesalers

15.3.9.1.3. Specialty Chemical Stores / Agents

15.3.9.1.4. Trade Shows & Industrial Networking

15.3.9.1.5. Hypermarkets & Supermarkets

15.3.9.2. Online

15.3.9.2.1. E-commerce Platforms

15.3.9.2.2. Direct-to-Consumer (D2C) Websites

15.3.9.2.3. Subscription & API-Based Ordering

15.3.10. Market By Country, Market Estimates and Forecast, USD Million, 2019-2032

15.3.10.1. Germany

15.3.10.2. France

15.3.10.3. U.K

15.3.10.4. Italy

15.3.10.5. Spain

15.3.10.6. Benelux

15.3.10.7. Russia

15.3.10.8. Finland

15.3.10.9. Sweden

15.3.10.10. Rest Of Europe

15.4. Asia-Pacific

15.4.1. Market By Type Estimates and Forecast, USD Million, 2019-2032

15.4.1.1. Oxidoreductases

15.4.1.2. Transferases

15.4.1.3. Hydrolases

15.4.1.4. Lyases

15.4.1.5. Isomerases / Epimerases

15.4.1.6. Ligases / Synthetases

15.4.1.7. Other

15.4.2. Market By Source, Market Estimates and Forecast, USD Million, 2019-2032

15.4.2.1. Microorganisms

15.4.2.2. Plants

15.4.2.3. Animal

15.4.3. Market By Form, Market Estimates and Forecast, USD Million, 2019-2032

15.4.3.1. Free (soluble) enzymes

15.4.3.2. Immobilized enzymes

15.4.3.3. Cross-linked enzyme aggregates (CLEAs)

15.4.3.4. Whole-cell catalysts

15.4.3.5. Cell-free enzyme systems

15.4.3.6. Enzyme cocktails & multi-enzyme blends

15.4.4. Market By Production Model, Market Estimates and Forecast, USD Million,

2019-2032

15.4.4.1. Lab Scale

15.4.4.2. Pilot Scale

15.4.4.3. Industrial Scale

15.4.5. Market By Reactor Mode, Market Estimates and Forecast, USD Million,

2019-2032

15.4.5.1. Batch reactors

15.4.5.2. Packed-bed reactors

15.4.5.3. Microreactors

15.4.5.4. Whole-cell bioreactors

15.4.6. Market By Grade, Market Estimates and Forecast, USD Million, 2019-2032

15.4.6.1. Pharma Grade

15.4.6.2. Food Grade

15.4.6.3. Industrial Grade

15.4.6.4. Reagent grade

15.4.7. Market By Application, Market Estimates and Forecast, USD Million, 2019-2032

15.4.7.1. Food and Beverages

15.4.7.2. Cleaning Agent

15.4.7.3. Biofuel Production

15.4.7.4. Agriculture and Feed

15.4.7.5. Biopharmaceuticals

15.4.7.6. Others

15.4.8. Market By End Use, Market Estimates and Forecast, USD Million, 2019-2032

15.4.8.1. Specialty & Fine Chemicals

15.4.8.2. Bulk & Commodity Chemicals

15.4.8.3. Agrochemicals

15.4.8.4. Polymers & Bioplastics

15.4.8.5. Industrial Solvents

15.4.8.6. Dyes & Pigments

15.4.8.7. Others

15.4.9. Market By Distribution Channel, Market Estimates and Forecast, USD

Million,2019-2032

15.4.9.1. Offline

15.4.9.1.1. Direct Sales (B2B)

15.4.9.1.2. Distributors / Wholesalers

15.4.9.1.3. Specialty Chemical Stores / Agents

15.4.9.1.4. Trade Shows & Industrial Networking

15.4.9.1.5. Hypermarkets & Supermarkets

15.4.9.2. Online

15.4.9.2.1. E-commerce Platforms

15.4.9.2.2. Direct-to-Consumer (D2C) Websites

15.4.9.2.3. Subscription & API-Based Ordering

15.4.10. Market By Country, Market Estimates and Forecast, USD Million, 2019-2032

15.4.10.1.1. China

15.4.10.1.2. India

15.4.10.1.3. Japan

15.4.10.1.4. South Korea

15.4.10.1.5. Indonesia

15.4.10.1.6. Thailand

15.4.10.1.7. Vietnam

15.4.10.1.8. Australia

15.4.10.1.9. New Zeland

15.4.10.1.10. Rest of APAC

15.5. Latin America

15.5.1. Market By Type Estimates and Forecast, USD Million, 2019-2032

15.5.1.1. Oxidoreductases

15.5.1.2. Transferases

15.5.1.3. Hydrolases

15.5.1.4. Lyases

15.5.1.5. Isomerases / Epimerases

15.5.1.6. Ligases / Synthetases

15.5.1.7. Other

15.5.2. Market By Source, Market Estimates and Forecast, USD Million, 2019-2032

15.5.2.1. Microorganisms

15.5.2.2. Plants

15.5.2.3. Animal

15.5.3. Market By Form, Market Estimates and Forecast, USD Million, 2019-2032

15.5.3.1. Free (soluble) enzymes

15.5.3.2. Immobilized enzymes

15.5.3.3. Cross-linked enzyme aggregates (CLEAs)

15.5.3.4. Whole-cell catalysts

15.5.3.5. Cell-free enzyme systems

15.5.3.6. Enzyme cocktails & multi-enzyme blends

15.5.4. Market By Production Model, Market Estimates and Forecast, USD Million,

2019-2032

15.5.4.1. Lab Scale

15.5.4.2. Pilot Scale

15.5.4.3. Industrial Scale

15.5.5. Market By Reactor Mode, Market Estimates and Forecast, USD Million,

2019-2032

15.5.5.1. Batch reactors

15.5.5.2. Packed-bed reactors

15.5.5.3. Microreactors

15.5.5.4. Whole-cell bioreactors

15.5.6. Market By Grade, Market Estimates and Forecast, USD Million, 2019-2032

15.5.6.1. Pharma Grade

15.5.6.2. Food Grade

15.5.6.3. Industrial Grade

15.5.6.4. Reagent grade

15.5.7. Market By Application, Market Estimates and Forecast, USD Million, 2019-2032

15.5.7.1. Food and Beverages

15.5.7.2. Cleaning Agent

15.5.7.3. Biofuel Production

15.5.7.4. Agriculture and Feed

15.5.7.5. Biopharmaceuticals

15.5.7.6. Others

15.5.8. Market By End Use, Market Estimates and Forecast, USD Million, 2019-2032

15.5.8.1. Specialty & Fine Chemicals

15.5.8.2. Bulk & Commodity Chemicals

15.5.8.3. Agrochemicals

15.5.8.4. Polymers & Bioplastics

15.5.8.5. Industrial Solvents

15.5.8.6. Dyes & Pigments

15.5.8.7. Others

15.5.9. Market By Distribution Channel, Market Estimates and Forecast, USD

Million,2019-2032

15.5.9.1. Offline

15.5.9.1.1. Direct Sales (B2B)

15.5.9.1.2. Distributors / Wholesalers

15.5.9.1.3. Specialty Chemical Stores / Agents

15.5.9.1.4. Trade Shows & Industrial Networking

15.5.9.1.5. Hypermarkets & Supermarkets

15.5.9.2. Online

15.5.9.2.1. E-commerce Platforms

15.5.9.2.2. Direct-to-Consumer (D2C) Websites

15.5.9.2.3. Subscription & API-Based Ordering

15.5.10. Market By Country, Market Estimates and Forecast, USD Million, 2019-2032

15.5.10.1. Brazil

15.5.10.2. Rest of LATAM

15.6. Middle East & Africa

15.6.1. Market By Type Estimates and Forecast, USD Million, 2019-2032

15.6.1.1. Oxidoreductases

15.6.1.2. Transferases

15.6.1.3. Hydrolases

15.6.1.4. Lyases

15.6.1.5. Isomerases / Epimerases

15.6.1.6. Ligases / Synthetases

15.6.1.7. Other

15.6.2. Market By Source, Market Estimates and Forecast, USD Million, 2019-2032

15.6.2.1. Microorganisms

15.6.2.2. Plants

15.6.2.3. Animal

15.6.3. Market By Form, Market Estimates and Forecast, USD Million, 2019-2032

15.6.3.1. Free (soluble) enzymes

15.6.3.2. Immobilized enzymes

15.6.3.3. Cross-linked enzyme aggregates (CLEAs)

15.6.3.4. Whole-cell catalysts

15.6.3.5. Cell-free enzyme systems

15.6.3.6. Enzyme cocktails & multi-enzyme blends

15.6.4. Market By Production Model, Market Estimates and Forecast, USD Million,

2019-2032

15.6.4.1. Lab Scale

15.6.4.2. Pilot Scale

15.6.4.3. Industrial Scale

15.6.5. Market By Reactor Mode, Market Estimates and Forecast, USD Million,

2019-2032

15.6.5.1. Batch reactors

15.6.5.2. Packed-bed reactors

15.6.5.3. Microreactors

15.6.5.4. Whole-cell bioreactors

15.6.6. Market By Grade, Market Estimates and Forecast, USD Million, 2019-2032

15.6.6.1. Pharma Grade

15.6.6.2. Food Grade

15.6.6.3. Industrial Grade

15.6.6.4. Reagent grade

15.6.7. Market By Application, Market Estimates and Forecast, USD Million, 2019-2032

15.6.7.1. Food and Beverages

15.6.7.2. Cleaning Agent

15.6.7.3. Biofuel Production

15.6.7.4. Agriculture and Feed

15.6.7.5. Biopharmaceuticals

15.6.7.6. Others

15.6.8. Market By End Use, Market Estimates and Forecast, USD Million, 2019-2032

15.6.8.1. Specialty & Fine Chemicals

15.6.8.2. Bulk & Commodity Chemicals

15.6.8.3. Agrochemicals

15.6.8.4. Polymers & Bioplastics

15.6.8.5. Industrial Solvents

15.6.8.6. Dyes & Pigments

15.6.8.7. Others

15.6.9. Market By Distribution Channel, Market Estimates and Forecast, USD

Million,2019-2032

15.6.9.1. Offline

15.6.9.1.1. Direct Sales (B2B)

15.6.9.1.2. Distributors / Wholesalers

15.6.9.1.3. Specialty Chemical Stores / Agents

15.6.9.1.4. Trade Shows & Industrial Networking

15.6.9.1.5. Hypermarkets & Supermarkets

15.6.9.2. Online

15.6.9.2.1. E-commerce Platforms

15.6.9.2.2. Direct-to-Consumer (D2C) Websites

15.6.9.2.3. Subscription & API-Based Ordering

15.6.10. Market By Country, Market Estimates and Forecast, USD Million, 2019-2032

15.6.10.1. Saudi Arabia

15.6.10.2. Rest of MEA

Chapter 16. Competitive Landscape

16.1. Market Revenue Share By Manufacturers

16.2. Mergers & Acquisitions

16.3. Competitor’s Positioning

16.4. Strategy Benchmarking

16.5. Vendor Landscape

16.5.1. Distributors

16.5.1.1. North America

16.5.1.2. Europe

16.5.1.3. Asia Pacific

16.5.1.4. Middle East & Africa

16.5.1.5. Latin America

Chapter 17. Company Profiles

17.1. Novozymes A/S

17.1.1. Company Overview

17.1.2. Product & Service Offerings

17.1.3. Strategic Initiatives

17.1.4. Financials

17.1.5. Conclusion

17.2. Codexis, Inc.

17.2.1. Company Overview

17.2.2. Product & Service Offerings

17.2.3. Strategic Initiatives

17.2.4. Financials

17.2.5. Conclusion

17.3. BASF SE

17.3.1. Company Overview

17.3.2. Product & Service Offerings

17.3.3. Strategic Initiatives

17.3.4. Financials

17.3.5. Conclusion

17.4. DuPont de Nemours, Inc.

17.4.1. Company Overview

17.4.2. Product & Service Offerings

17.4.3. Strategic Initiatives

17.4.4. Financials

17.5. Royal DSM N.V.

17.5.1. Company Overview

17.5.2. Product & Service Offerings

17.5.3. Strategic Initiatives

17.5.4. Financials

17.5.5. Conclusion

17.6. Chr. Hansen Holding A/S

17.6.1. Company Overview

17.6.2. Product & Service Offerings

17.6.3. Strategic Initiatives

17.6.4. Financials

17.6.5. Conclusion

17.7. Dyadic International, Inc.

17.7.1. Company Overview

17.7.2. Product & Service Offerings

17.7.3. Strategic Initiatives

17.7.4. Financials

17.7.5. Conclusion

17.8. AB Enzymes GmbH

17.8.1. Company Overview

17.8.2. Product & Service Offerings

17.8.3. Strategic Initiatives

17.8.4. Financials

17.8.5. Conclusion

17.9. Amano Enzyme Inc.

17.9.1. Company Overview

17.9.2. Product & Service Offerings

17.9.3. Strategic Initiatives

17.9.4. Financials

17.9.5. Conclusion

17.10. Biocatalysts Limited

17.10.1. Company Overview

17.10.2. Product & Service Offerings

17.10.3. Strategic Initiatives

17.10.4. Financials

17.10.5. Conclusion

17.11. Lonza Group Ltd.

17.11.1. Company Overview

17.11.2. Product & Service Offerings

17.11.3. Strategic Initiatives

17.11.4. Financials

17.11.5. Conclusion

17.12. Prozomix Limited

17.12.1. Company Overview

17.12.2. Product & Service Offerings

17.12.3. Strategic Initiatives

17.12.4. Financials

17.12.5. Conclusion

17.13. Givaudan S.A.

17.13.1. Company Overview

17.13.2. Product & Service Offerings

17.13.3. Strategic Initiatives

17.13.4. Financials

17.13.5. Conclusion

17.14. Carbios

17.14.1. Company Overview

17.14.2. Product & Service Offerings

17.14.3. Strategic Initiatives

17.14.4. Financials

17.14.5.Conclusion

17.15. HydRegen Limited

17.15.1. Company Overview

17.15.2. Product & Service Offerings

17.15.3. Strategic Initiatives

17.15.4. Financials

17.15.5. Conclusion

17.16. Debut Biotech

17.16.1. Company Overview

17.16.2. Product & Service Offerings

17.16.3. Strategic Initiatives

17.16.4. Financials

17.16.5. Conclusion

17.17. EnginZyme AB

17.17.1. Company Overview

17.17.2. Product & Service Offerings

17.17.3. Strategic Initiatives

17.17.4. Financials

17.17.5. Conclusion

17.18. Unilever PLC

17.18.1. Company Overview

17.18.2. Product & Service Offerings

17.18.3. Strategic Initiatives

17.18.4. Financials

17.18.5. Conclusion

17.19. Soufflet Group

17.19.1. Company Overview

17.19.2. Product & Service Offerings

17.19.3. Strategic Initiatives

17.19.4. Financials

17.19.5. Conclusion

17.20. Fermenta Biotech Ltd.

17.20.1. Company Overview

17.20.2. Product & Service Offerings

17.20.3. Strategic Initiatives

17.20.4. Financials

17.20.5. Conclusion

17.21. Piramal Enterprises Ltd.

17.21.1. Company Overview

17.21.2. Product & Service Offerings

17.21.3. Strategic Initiatives

17.21.4. Financials

17.21.5. Conclusion

17.22. Zymtronix Catalytic Systems Inc.

17.22.1. Company Overview

17.22.2. Product & Service Offerings

17.22.3. Strategic Initiatives

17.22.4. Financials

17.22.5. Conclusion

17.23. RP Management LLC

17.23.1. Company Overview

17.23.2. Product & Service Offerings

17.23.3. Strategic Initiatives

17.23.4. Financials

17.23.5. Conclusion

17.24. Panacea Biotec

17.24.1. Company Overview

17.24.2. Product & Service Offerings

17.24.3. Strategic Initiatives

17.24.4. Financials

17.24.5. Conclusion

17.25. Aladdin Scientific

17.25.1. Company Overview

17.25.2. Product & Service Offerings

17.25.3. Strategic Initiatives

17.25.4. Financials

17.25.5. Conclusion

Segments Covered in Report

For the purpose of this report, Advantia Business Consulting LLP. has segmented global bio catalyst market on the basis of By Type, By Source, By Form, By Production Model, By Reactor mode, By Grade, By Application, By End Use, By Distribution Channel and By region for 2019 to 2032.

- Global Type Outlook (Revenue, USD Million; 2019-2032)

- Oxidoreductases

- Transferases

- Hydrolases

- Lyases

- Isomerases / Epimerases

- Ligases / Synthetases

- Other

- Global Source Outlook (Revenue, USD Million; 2019-2032)

- Microorganisms

- Plants

- Animal

- Global Form Outlook (Revenue, USD Million; 2019-2032)

- Free (soluble) enzymes

- Immobilized enzymes

- Cross-linked enzyme aggregates (CLEAs)

- Whole-cell catalysts

- Cell-free enzyme systems

- Enzyme cocktails & multi-enzyme blends

- Global Production Model Outlook (Revenue, USD Million; 2019-2032)

- Lab Scale

- Pilot Scale

- Industrial Scale

- Global Reactor Mode Outlook (Revenue, USD Million; 2019-2032)

- Batch reactors

- Packed-bed reactors

- Microreactors

- Whole-cell bioreactors

- Global Grade Outlook (Revenue, USD Million; 2019-2032)

- Pharma Grade

- Food Grade

- Industrial Grade

- Reagent grade

- Global Application Outlook (Revenue, USD Million; 2019-2032)

- Food and Beverages

- Cleaning Agent

- Biofuel Production

- Agriculture and Feed

- Biopharmaceuticals

- Others

- Global End Use Outlook (Revenue, USD Million; 2019-2032)

- Specialty & Fine Chemicals

- Bulk & Commodity Chemicals

- Agrochemicals

- Polymers & Bioplastics

- Industrial Solvents

- Dyes & Pigments

- Others

- Global Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Offline

- Direct Sales (B2B)

- Distributors / Wholesalers

- Specialty Chemical Stores / Agents

- Trade Shows & Industrial Networking

- Hypermarkets & Supermarkets

- Online

- E-commerce Platforms

- Direct-to-Consumer (D2C) Websites

- Subscription & API-Based Ordering

- Offline

- North America

- North America Type Outlook (Revenue, USD Million; 2019-2032)

- Oxidoreductases

- Transferases

- Hydrolases

- Lyases

- Isomerases / Epimerases

- Ligases / Synthetases

- Other

- North America Source Outlook (Revenue, USD Million; 2019-2032)

- Microorganisms

- Plants

- Animal

- North America Form Outlook (Revenue, USD Million; 2019-2032)

- Free (soluble) enzymes

- Immobilized enzymes

- Cross-linked enzyme aggregates (CLEAs)

- Whole-cell catalysts

- Cell-free enzyme systems

- Enzyme cocktails & multi-enzyme blends

- North America Production Model Outlook (Revenue, USD Million; 2019-2032)

- Lab Scale

- Pilot Scale

- Industrial Scale

- North America Reactor Mode Outlook (Revenue, USD Million; 2019-2032)

- Batch reactors

- Packed-bed reactors

- Microreactors

- Whole-cell bioreactors

- North America Grade Outlook (Revenue, USD Million; 2019-2032)

- Pharma Grade

- Food Grade

- Industrial Grade

- Reagent grade

- North America Application Outlook (Revenue, USD Million; 2019-2032)

- Food and Beverages

- Cleaning Agent

- Biofuel Production

- Agriculture and Feed

- Biopharmaceuticals

- Others

- North America End Use Outlook (Revenue, USD Million; 2019-2032)

- Specialty & Fine Chemicals

- Bulk & Commodity Chemicals

- Agrochemicals

- Polymers & Bioplastics

- Industrial Solvents

- Dyes & Pigments

- Others

- North America Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Offline

- Direct Sales (B2B)

- Distributors / Wholesalers

- Specialty Chemical Stores / Agents

- Trade Shows & Industrial Networking

- Hypermarkets & Supermarkets

- Online

- E-commerce Platforms

- Direct-to-Consumer (D2C) Websites

- Subscription & API-Based Ordering

- Offline

- U.S

- U.S Type Outlook (Revenue, USD Million; 2019-2032)

- Oxidoreductases

- Transferases

- Hydrolases

- Lyases

- Isomerases / Epimerases

- Ligases / Synthetases

- Other

- U.S Source Outlook (Revenue, USD Million; 2019-2032)

- Microorganisms

- Plants

- Animal

- U.S Form Outlook (Revenue, USD Million; 2019-2032)

- Free (soluble) enzymes

- Immobilized enzymes

- Cross-linked enzyme aggregates (CLEAs)

- Whole-cell catalysts

- Cell-free enzyme systems

- Enzyme cocktails & multi-enzyme blends

- U.S Production Model Outlook (Revenue, USD Million; 2019-2032)

- Lab Scale

- Pilot Scale

- Industrial Scale

- U.S Reactor Mode Outlook (Revenue, USD Million; 2019-2032)

- Batch reactors

- Packed-bed reactors

- Microreactors

- Whole-cell bioreactors

- U.S Grade Outlook (Revenue, USD Million; 2019-2032)

- Pharma Grade

- Food Grade

- Industrial Grade

- Reagent grade

- U.S Application Outlook (Revenue, USD Million; 2019-2032)

- Food and Beverages

- Cleaning Agent

- Biofuel Production

- Agriculture and Feed

- Biopharmaceuticals

- Others

- U.S End Use Outlook (Revenue, USD Million; 2019-2032)

- Specialty & Fine Chemicals

- Bulk & Commodity Chemicals

- Agrochemicals

- Polymers & Bioplastics

- Industrial Solvents

- Dyes & Pigments

- Others

- U.S Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Offline

- Direct Sales (B2B)

- Distributors / Wholesalers

- Specialty Chemical Stores / Agents

- Trade Shows & Industrial Networking

- Hypermarkets & Supermarkets

- Online

- E-commerce Platforms

- Direct-to-Consumer (D2C) Websites

- Subscription & API-Based Ordering

- Offline

- Canada

- Canada Type Outlook (Revenue, USD Million; 2019-2032)

- Oxidoreductases

- Transferases

- Hydrolases

- Lyases

- Isomerases / Epimerases

- Ligases / Synthetases

- Other

- Canada Source Outlook (Revenue, USD Million; 2019-2032)

- Microorganisms

- Plants

- Animal

- Canada Form Outlook (Revenue, USD Million; 2019-2032)

- Free (soluble) enzymes

- Immobilized enzymes

- Cross-linked enzyme aggregates (CLEAs)

- Whole-cell catalysts

- Cell-free enzyme systems

- Enzyme cocktails & multi-enzyme blends

- Canada Production Model Outlook (Revenue, USD Million; 2019-2032)

- Lab Scale

- Pilot Scale

- Industrial Scale

- Canada Reactor Mode Outlook (Revenue, USD Million; 2019-2032)

- Batch reactors

- Packed-bed reactors

- Microreactors

- Whole-cell bioreactors

- Canada Grade Outlook (Revenue, USD Million; 2019-2032)

- Pharma Grade

- Food Grade

- Industrial Grade

- Reagent grade

- Canada Application Outlook (Revenue, USD Million; 2019-2032)

- Food and Beverages

- Cleaning Agent

- Biofuel Production

- Agriculture and Feed

- Biopharmaceuticals

- Others

- Canada End Use Outlook (Revenue, USD Million; 2019-2032)

- Specialty & Fine Chemicals

- Bulk & Commodity Chemicals

- Agrochemicals

- Polymers & Bioplastics

- Industrial Solvents

- Dyes & Pigments

- Others

- Canada Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Offline

- Direct Sales (B2B)

- Distributors / Wholesalers

- Specialty Chemical Stores / Agents

- Trade Shows & Industrial Networking

- Hypermarkets & Supermarkets

- Online

- E-commerce Platforms

- Direct-to-Consumer (D2C) Websites

- Subscription & API-Based Ordering

- Offline

- Mexico

- Mexico Type Outlook (Revenue, USD Million; 2019-2032)

- Oxidoreductases

- Transferases

- Hydrolases

- Lyases

- Isomerases / Epimerases

- Ligases / Synthetases

- Other

- Mexico Source Outlook (Revenue, USD Million; 2019-2032)

- Microorganisms

- Plants

- Animal

- Mexico Form Outlook (Revenue, USD Million; 2019-2032)

- Free (soluble) enzymes

- Immobilized enzymes

- Cross-linked enzyme aggregates (CLEAs)

- Whole-cell catalysts

- Cell-free enzyme systems

- Enzyme cocktails & multi-enzyme blends

- Mexico Production Model Outlook (Revenue, USD Million; 2019-2032)

- Lab Scale

- Pilot Scale

- Industrial Scale

- Mexico Reactor Mode Outlook (Revenue, USD Million; 2019-2032)

- Batch reactors

- Packed-bed reactors

- Microreactors

- Whole-cell bioreactors

- Mexico Grade Outlook (Revenue, USD Million; 2019-2032)

- Pharma Grade

- Food Grade

- Industrial Grade

- Reagent grade

- Mexico Application Outlook (Revenue, USD Million; 2019-2032)

- Food and Beverages

- Cleaning Agent

- Biofuel Production

- Agriculture and Feed

- Biopharmaceuticals

- Others

- Mexico End Use Outlook (Revenue, USD Million; 2019-2032)

- Specialty & Fine Chemicals

- Bulk & Commodity Chemicals

- Agrochemicals

- Polymers & Bioplastics

- Industrial Solvents

- Dyes & Pigments

- Others

- Mexico Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Offline

- Direct Sales (B2B)

- Distributors / Wholesalers

- Specialty Chemical Stores / Agents

- Trade Shows & Industrial Networking

- Hypermarkets & Supermarkets

- Online

- E-commerce Platforms

- Direct-to-Consumer (D2C) Websites

- Subscription & API-Based Ordering

- Offline

- Europe

- Europe Type Outlook (Revenue, USD Million; 2019-2032)

- Oxidoreductases

- Transferases

- Hydrolases

- Lyases

- Isomerases / Epimerases

- Ligases / Synthetases

- Other

- Europe Source Outlook (Revenue, USD Million; 2019-2032)

- Microorganisms

- Plants

- Animal

- Europe Form Outlook (Revenue, USD Million; 2019-2032)

- Free (soluble) enzymes

- Immobilized enzymes

- Cross-linked enzyme aggregates (CLEAs)

- Whole-cell catalysts

- Cell-free enzyme systems

- Enzyme cocktails & multi-enzyme blends

- Europe Production Model Outlook (Revenue, USD Million; 2019-2032)

- Lab Scale

- Pilot Scale

- Industrial Scale

- Europe Reactor Mode Outlook (Revenue, USD Million; 2019-2032)

- Batch reactors

- Packed-bed reactors

- Microreactors

- Whole-cell bioreactors

- Europe Grade Outlook (Revenue, USD Million; 2019-2032)

- Pharma Grade

- Food Grade

- Industrial Grade

- Reagent grade

- Europe Application Outlook (Revenue, USD Million; 2019-2032)

- Food and Beverages

- Cleaning Agent

- Biofuel Production

- Agriculture and Feed

- Biopharmaceuticals

- Others

- Europe End Use Outlook (Revenue, USD Million; 2019-2032)

- Specialty & Fine Chemicals

- Bulk & Commodity Chemicals

- Agrochemicals

- Polymers & Bioplastics

- Industrial Solvents

- Dyes & Pigments

- Others

- Europe Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Offline

- Direct Sales (B2B)

- Distributors / Wholesalers

- Specialty Chemical Stores / Agents

- Trade Shows & Industrial Networking

- Hypermarkets & Supermarkets

- Online

- E-commerce Platforms

- Direct-to-Consumer (D2C) Websites

- Subscription & API-Based Ordering

- Offline

- Germany

- Germany Type Outlook (Revenue, USD Million; 2019-2032)

- Oxidoreductases

- Transferases

- Hydrolases

- Lyases

- Isomerases / Epimerases

- Ligases / Synthetases

- Other

- Germany Source Outlook (Revenue, USD Million; 2019-2032)

- Microorganisms

- Plants

- Animal

- Germany Form Outlook (Revenue, USD Million; 2019-2032)

- Free (soluble) enzymes

- Immobilized enzymes

- Cross-linked enzyme aggregates (CLEAs)

- Whole-cell catalysts

- Cell-free enzyme systems

- Enzyme cocktails & multi-enzyme blends

- Germany Production Model Outlook (Revenue, USD Million; 2019-2032)

- Lab Scale

- Pilot Scale

- Industrial Scale

- Germany Reactor Mode Outlook (Revenue, USD Million; 2019-2032)

- Batch reactors

- Packed-bed reactors

- Microreactors

- Whole-cell bioreactors

- Germany Grade Outlook (Revenue, USD Million; 2019-2032)

- Pharma Grade

- Food Grade

- Industrial Grade

- Reagent grade

- Germany Application Outlook (Revenue, USD Million; 2019-2032)

- Food and Beverages

- Cleaning Agent

- Biofuel Production

- Agriculture and Feed

- Biopharmaceuticals

- Others

- Germany End Use Outlook (Revenue, USD Million; 2019-2032)

- Specialty & Fine Chemicals

- Bulk & Commodity Chemicals

- Agrochemicals

- Polymers & Bioplastics

- Industrial Solvents

- Dyes & Pigments

- Others

- Germany Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Offline

- Direct Sales (B2B)

- Distributors / Wholesalers

- Specialty Chemical Stores / Agents

- Trade Shows & Industrial Networking

- Hypermarkets & Supermarkets

- Online

- E-commerce Platforms

- Direct-to-Consumer (D2C) Websites

- Subscription & API-

- Based Ordering

- Offline

- France

- France Type Outlook (Revenue, USD Million; 2019-2032)

- Oxidoreductases

- Transferases

- Hydrolases

- Lyases

- Isomerases / Epimerases

- Ligases / Synthetases

- Other

- France Source Outlook (Revenue, USD Million; 2019-2032)

- Microorganisms

- Plants

- Animal

- France Form Outlook (Revenue, USD Million; 2019-2032)

- Free (soluble) enzymes

- Immobilized enzymes

- Cross-linked enzyme aggregates (CLEAs)

- Whole-cell catalysts

- Cell-free enzyme systems

- Enzyme cocktails & multi-enzyme blends

- France Production Model Outlook (Revenue, USD Million; 2019-2032)

- Lab Scale

- Pilot Scale

- Industrial Scale

- France Reactor Mode Outlook (Revenue, USD Million; 2019-2032)

- Batch reactors

- Packed-bed reactors

- Microreactors

- Whole-cell bioreactors

- France Grade Outlook (Revenue, USD Million; 2019-2032)

- Pharma Grade

- Food Grade

- Industrial Grade

- Reagent grade

- France Application Outlook (Revenue, USD Million; 2019-2032)

- Food and Beverages

- Cleaning Agent

- Biofuel Production

- Agriculture and Feed

- Biopharmaceuticals

- Others

- France End Use Outlook (Revenue, USD Million; 2019-2032)

- Specialty & Fine Chemicals

- Bulk & Commodity Chemicals

- Agrochemicals

- Polymers & Bioplastics

- Industrial Solvents

- Dyes & Pigments

- Others

- France Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Offline

- Direct Sales (B2B)

- Distributors / Wholesalers

- Specialty Chemical Stores / Agents

- Trade Shows & Industrial Networking

- Hypermarkets & Supermarkets

- Online

- E-commerce Platforms

- Direct-to-Consumer (D2C) Websites

- Subscription & API-Based Ordering

- Offline

- U.K

- U.K Type Outlook (Revenue, USD Million; 2019-2032)

- Oxidoreductases

- Transferases

- Hydrolases

- Lyases

- Isomerases / Epimerases

- Ligases / Synthetases

- Other

- U.K Source Outlook (Revenue, USD Million; 2019-2032)

- Microorganisms

- Plants

- Animal

- U.K Form Outlook (Revenue, USD Million; 2019-2032)

- Free (soluble) enzymes

- Immobilized enzymes

- Cross-linked enzyme aggregates (CLEAs)

- Whole-cell catalysts

- Cell-free enzyme systems

- Enzyme cocktails & multi-enzyme blends

- U.K Production Model Outlook (Revenue, USD Million; 2019-2032)

- Lab Scale

- Pilot Scale

- Industrial Scale

- U.K Reactor Mode Outlook (Revenue, USD Million; 2019-2032)

- Batch reactors

- Packed-bed reactors

- Microreactors

- Whole-cell bioreactors

- U.K Grade Outlook (Revenue, USD Million; 2019-2032)

- Pharma Grade

- Food Grade

- Industrial Grade

- Reagent grade

- U.K Application Outlook (Revenue, USD Million; 2019-2032)

- Food and Beverages

- Cleaning Agent

- Biofuel Production

- Agriculture and Feed

- Biopharmaceuticals

- Others

- U.K End Use Outlook (Revenue, USD Million; 2019-2032)

- Specialty & Fine Chemicals

- Bulk & Commodity Chemicals

- Agrochemicals

- Polymers & Bioplastics

- Industrial Solvents

- Dyes & Pigments

- Others

- U.K Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Offline

- Direct Sales (B2B)

- Distributors / Wholesalers

- Specialty Chemical Stores / Agents

- Trade Shows & Industrial Networking

- Hypermarkets & Supermarkets

- Online

- E-commerce Platforms

- Direct-to-Consumer (D2C) Websites

- Subscription & API-Based Ordering

- Offline

- Italy

- Italy Type Outlook (Revenue, USD Million; 2019-2032)

- Oxidoreductases

- Transferases

- Hydrolases

- Lyases

- Isomerases / Epimerases

- Ligases / Synthetases

- Other

- Italy Source Outlook (Revenue, USD Million; 2019-2032)

- Microorganisms

- Plants

- Animal

- Italy Form Outlook (Revenue, USD Million; 2019-2032)

- Free (soluble) enzymes

- Immobilized enzymes

- Cross-linked enzyme aggregates (CLEAs)

- Whole-cell catalysts

- Cell-free enzyme systems

- Enzyme cocktails & multi-enzyme blends

- Italy Production Model Outlook (Revenue, USD Million; 2019-2032)

- Lab Scale

- Pilot Scale

- Industrial Scale

- Italy Reactor Mode Outlook (Revenue, USD Million; 2019-2032)

- Batch reactors

- Packed-bed reactors

- Microreactors

- Whole-cell bioreactors

- Italy Grade Outlook (Revenue, USD Million; 2019-2032)

- Pharma Grade

- Food Grade

- Industrial Grade

- Reagent grade

- Italy Application Outlook (Revenue, USD Million; 2019-2032)

- Food and Beverages

- Cleaning Agent

- Biofuel Production

- Agriculture and Feed

- Biopharmaceuticals

- Others

- Italy End Use Outlook (Revenue, USD Million; 2019-2032)

- Specialty & Fine Chemicals

- Bulk & Commodity Chemicals

- Agrochemicals

- Polymers & Bioplastics

- Industrial Solvents

- Dyes & Pigments

- Others

- Italy Distribution Channel Outlook (Revenue, USD Million; 2019-2032)

- Offline

- Direct Sales (B2B)

- Distributors / Wholesalers

- Specialty Chemical Stores / Agents

- Trade Shows & Industrial Networking

- Hypermarkets & Supermarkets

- Online

- E-commerce Platforms

- Direct-to-Consumer (D2C) Websites

- Subscription & API-Based Ordering

- Offline

- Spain

- Spain Type Outlook (Revenue, USD Million; 2019-2032)

- Oxidoreductases

- Transferases

- Hydrolases

- Lyases

- Isomerases / Epimerases

- Ligases / Synthetases

- Other

- Spain Source Outlook (Revenue, USD Million; 2019-2032)

- Microorganisms

- Plants

- Animal

- Spain Form Outlook (Revenue, USD Million; 2019-2032)

- Free (soluble) enzymes

- Immobilized enzymes

- Cross-linked enzyme aggregates (CLEAs)

- Whole-cell catalysts

- Cell-free enzyme systems

- Enzyme cocktails & multi-enzyme blends

- Spain Production Model Outlook (Revenue, USD Million; 2019-2032)

- Lab Scale

- Pilot Scale

- Industrial Scale

- Spain Reactor Mode Outlook (Revenue, USD Million; 2019-2032)

- Batch reactors

- Packed-bed reactors

- Microreactors

- Whole-cell bioreactors

- Spain Grade Outlook (Revenue, USD Million; 2019-2032)

- Pharma Grade

- Food Grade

- Industrial Grade

- Reagent grade

- Spain Application Outlook (Revenue, USD Million; 2019-2032)

- Food and Beverages

- Cleaning Agent